|

市场调查报告书

商品编码

1851809

数位交易管理(DTM):市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Digital Transaction Management (DTM) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

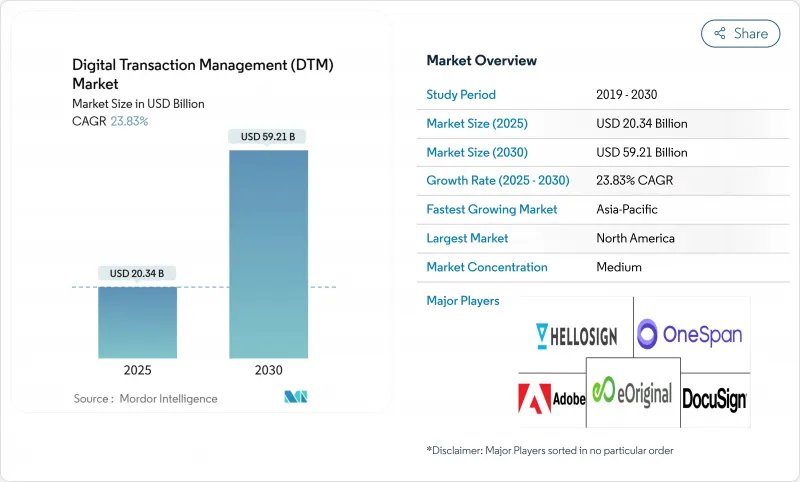

数位交易管理市场预计到 2025 年将达到 203.4 亿美元,到 2030 年将达到 592.1 亿美元,复合年增长率高达 23.83%。

投资人认为,这一发展趋势表明,企业如今已将数位化工作流程视为核心策略的一部分,而非后勤部门优化措施。区块链技术在防篡改审核追踪方面的加速应用、远端办公政策的快速普及以及云端交付模式的兴起,以及生成式人工智慧文件工具的稳步发展,都在推动市场需求。以 HIPAA、GDPR 和 eIDAS 为代表的网路安全法规的整合,进一步强化了确保资料完整性、身分验证和全球可执行性的解决方案的必要性。

全球数位交易管理 (DTM) 市场趋势与洞察

电子签章在受监管产业的应用加速发展

目前,美国已有43个州允许在选举法规中使用电子签章,运输部也正在最终敲定修正案,将电子认证视为药物检测纪录的法律效力来源。这些先例表明,法律的公开透明可以消除残余的疑虑,并使企业在确保合规的前提下,将文件处理週期缩短75%。例如,大型医疗机构正在使用合格的电子签章来跨州同步同意书,避免了邮件延误,从而提高了病患满意度并降低了行政成本。

银行、金融服务和保险机构以及政府机构转向端到端合约生命週期自动化

银行同时处理超过2万份活跃合约,由于监管不力,可能面临高达9%的收入损失。花旗银行推出的基于区块链的代币服务,展示了即时结算如何降低营运风险,并为负责人释放营运成本效益。政府机构也纷纷效仿,将采购文件集中到搜寻的储存库中,以实现近乎即时的政策审核并减少诈欺行为。这些倡议凸显了为何超越简单电子签章的全面自动化正成为资讯长预算中必不可少的项目。

复杂的跨境加密签名法规

儘管eIDAS高度重视合格电子签章的证据效力,但欧盟以外的相互核准仍然不足(helpx.adobe.com)。此外,诸如GDPR之类的资料主权指令与美国《云端法案》(CLOUD Act)规定的域外权利主张存在衝突(isaca.org)。这种监管体系的复杂性限制了数位交易管理市场近期的发展,因为其增加了法律咨询成本,并延长了寻求支持跨国工作流程的供应商的市场推广计划。

细分市场分析

到2024年,解决方案将占总收入的70%,但在数位交易管理市场中,预计到2030年,服务将维持最高的复合成长率,达到28.3%。金融机构在升级其传统系统时,往往缺乏内部监管方面的专业知识,这增加了对整合、合规和託管支援的需求。在2024年的一个案例中,一个顾问团队将电子签章工作流程与核心银行帐簿集成,从而减少了处理错误和营运成本。

区块链模组嵌入了不可篡改的审核追踪,人工智慧分类实现了数据采集的自动化,供应商也迅速发布了符合 HIPAA 和 SOC 2 标准的行业特定模板,从而缩短了医疗保健和金融客户的价值实现时间。儘管如此,关键任务工作流程的复杂性仍然需要依赖外部专业知识,这也支撑了服务收入的成长。

2024年,云端平台将占75%的市场份额,年复合成长率达26.1%,到2030年,云端部署的数位交易管理市场规模可望翻倍。企业重视订阅定价模式、快速部署以及通过ISO 27001和FedRAMP审核的资料中心。多重云端架构透过将敏感资料路由到本地主权云,同时在公共基础架构中预留突发容量,从而在敏捷性和合规性之间取得平衡。

国防、关键基础设施和部分金融机构仍然保留本地部署,但即使是这些用户也开始采用混合控制平面,在其防火墙后部署云端功能。随着加密金钥管理、机密运算和零信任框架的日趋成熟,对全面云端化的抵制可能会降低,从而继续保持云端采用率上升的趋势。

区域分析

到2024年,北美将占数位交易管理市场收入的30.21%。围绕电子记录的成熟法律法规正在推动私营部门和联邦政府的采用。美国运输部即将出台的关于电子药物试纸的规则表明,对数位信任的监管力度将继续加强(federalregister.gov)。美国医疗保健合规蓝图同样加速了电子记录的普及,医疗服务提供者正在利用符合HIPAA标准的电子签章系统来简化理赔流程(iclg.com)。总部位于该地区的技术供应商不断部署人工智慧功能,以提升服务品质并使其高价许可证更具吸引力。

亚太地区正经历最快的成长,复合年增长率高达28.6%。该地区处理着全球一半以上的数位支付,预计到2027年,B2C电子商务规模将超过4兆欧元(4.3兆美元)(tmcnet.com)。印度的统一支付介面(UPI)旨在实现每年超过2000亿笔交易,这将推动可扩展签名引擎的需求。酒店、物流和政府部门也在积极采用数位合同,以满足其移动优先的消费群的需求。儘管监管方面仍存在差异,但像印尼这样的国家现在允许使用数位合同,只要满足基本的同意原则即可(mondaq.com),这标誌着监管正在逐步趋同。

欧洲已实施eIDAS系统,该系统赋予电子签章与手写签名同等的法律效力(helpx.adobe.com)。即将推出的eDAS 2.0法规和欧盟数位身分钱包预计将实现无缝的跨境签名,从而增强市场信心。拉丁美洲和中东及非洲地区正经历高速成长,儘管基准较小。巴西和海湾国家的政府数位化项目,以及不断扩大的宽频接入,为这些地区的数位交易管理产业创造了有利条件。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 加速受监管产业电子签章的普及应用

- 银行、金融服务和保险机构以及政府机构转向端到端合约生命週期自动化

- 强制远端办公促进了云端基础管理(DTM)的普及。

- 生成式人工智慧助理缩短了文件处理时间

- 点击式广告推动亚洲电子商务转换率

- 数位身分框架(eIDAS 2.0、Aadhaar、NID)将推动其普及应用。

- 市场限制

- 复杂的跨境加密签名法规

- 新兴市场合格远距身分认证的高成本

- 碎片化的传统核心银行工作流程阻碍了全面自动化。

- 农村地区5G/Edge基础设施有限,减缓了行动数位地图模型(DTM)的普及。

- 价值链分析

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 宏观经济趋势影响评估

- 投资分析

第五章 市场规模与成长预测

- 按组件

- 解决方案

- 服务

- 透过部署模式

- 云

- 本地部署

- 按组织规模

- 小型企业

- 大公司

- 按最终用户行业划分

- 银行、金融服务和保险

- 医疗保健和生命科学

- 零售与电子商务

- 政府和公共部门

- 资讯科技/通讯

- 教育

- 其他终端用户产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 其他中东地区

- 非洲

- 南非

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Adobe Inc.

- DocuSign, Inc.

- Dropbox, Inc.

- Nintex Global Ltd.

- Namirial SpA

- OneSpan Inc.

- Wolters Kluwer NV

- Entrust Corporation

- SignEasy Inc.

- Mitratech Holdings Inc.

- Sertifi, Inc.

- Thales Group(Gemalto NV)

- Nitro Software Ltd.

- airSlate Inc.

- PandaDoc Inc.

- Conga(Apttus Corporation)

- Zoho Corporation Pvt. Ltd.

- ZorroSign, Inc.

- Topaz Systems Inc.

- InfoCert SpA

- AssureSign LLC

- eOriginal, Inc.

第七章 市场机会与未来展望

The digital transaction management market stands at USD 20.34 billion in 2025 and is projected to reach USD 59.21 billion by 2030, sustaining a robust 23.83% CAGR.

Investors view this trajectory as evidence that organizations now treat digital workflows as part of core strategy rather than back-office optimization. Accelerated deployment of blockchain for tamper-proof audit trails, rapid adoption of remote-work policies that favor cloud delivery, and a steady rise in generative-AI document tools collectively reinforce demand. Cyber-regulation alignment-most notably HIPAA, GDPR, and eIDAS-further legitimizes solutions that guarantee data integrity, identity assurance, and global enforceability.

Global Digital Transaction Management (DTM) Market Trends and Insights

Accelerating E-Signature Adoption Across Regulated Industries

U.S. election rules now allow e-signatures in 43 states, and the Department of Transportation is finalizing amendments that treat electronic attestations as legally valid for drug-testing records. These precedents demonstrate how statutory openness removes residual skepticism, letting enterprises shorten document cycles by 75% while maintaining compliance. Large health providers, for example, rely on qualified electronic signatures to synchronize cross-state consent forms without postal delays, thereby elevating patient satisfaction and trimming administrative overhead.

Shift Toward End-to-End Contract Lifecycle Automation in BFSI and Government

Banks process more than 20,000 active contracts simultaneously, exposing them to revenue leakage of up to 9% when oversight is weak. The rollout of blockchain-backed Citi Token Services shows how real-time settlement can shrink operational risk and unlock working-capital benefits for treasurers. Government agencies follow suit by centralizing procurement documents into searchable repositories, enabling near-instant policy audits and mitigating fraud. Together, these moves underscore why holistic automation-beyond simple e-signatures-is becoming mandatory budgeting line-item for CIOs.

Complex Cross-Border Crypto-Signature Regulations

eIDAS assigns top evidentiary weight to Qualified Electronic Signatures, yet mutual recognition outside the EU remains uneven (helpx.adobe.com). Additionally, data sovereignty mandates such as GDPR conflict with extraterritorial requests under the US CLOUD Act (isaca.org). This patchwork raises legal counsel costs and elongates go-to-market plans for providers trying to support multinational workflows, therefore tempering the digital transaction management market's near-term acceleration.

Other drivers and restraints analyzed in the detailed report include:

- Generative-AI Assistants Reducing Document Turn-Around Times

- Digital Identity Frameworks Catalyzing Adoption

- Limited 5G / Edge Infrastructure in Rural Areas Slowing Mobile DTM Usage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions generated 70% of 2024 revenue, but services are forecast to expand at a 28.3% compound rate to 2030, the highest within the digital transaction management market. Financial institutions upgrading legacy stacks often lack in-house regulatory expertise, fueling demand for integration, compliance, and managed support. Example engagements in 2024 reduced processing errors and operating expense when consultancy teams unified e-signature workflows with core banking ledgers.

The solutions category is not stagnant; blockchain modules embed immutable audit trails while AI classification automates data capture. Vendors release vertical-specific templates that satisfy HIPAA and SOC 2 out-of-the-box, shortening time-to-value for healthcare and finance clients. Nevertheless, the intricate nature of mission-critical workflows implies ongoing reliance on external specialists, which sustains the services revenue curve.

Cloud platforms held 75% share in 2024, and their 26.1% CAGR means the digital transaction management market size for cloud deployments could double well before 2030. Enterprises value subscription pricing, rapid provisioning, and certified data centers that pass ISO 27001 and FedRAMP audits. Multi-cloud architectures now route sensitive data to local sovereign clouds while reserving burst capacity on public infrastructure, balancing agility with compliance.

On-premise installations still exist for defense, critical infrastructure, and select financial institutions, yet even these buyers adopt hybrid control planes that mirror cloud features behind the firewall. As encryption key management, confidential computing, and zero-trust frameworks mature, resistance to full cloud conversion will erode, maintaining the upward bias in cloud uptake.

The Digital Transaction Management Market Report is Segmented by Component (Solutions, Services), Deployment Mode (Cloud, On-Premise), Organization Size (Small and Medium Enterprises, Large Enterprises), End-User Industry (Banking, Financial Services and Insurance, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 30.21% of digital transaction management market revenue in 2024. Mature legal clarity around electronic records encourages both private-sector and federal adoption. The U.S. Department of Transportation's pending rule on electronic drug-testing forms demonstrates continuous regulatory reinforcement of digital trust (federalregister.gov). Healthcare compliance roadmaps in the United States similarly accelerate usage, as providers exploit HIPAA-compatible e-signature stacks to streamline claims (iclg.com). Technology vendors headquartered in the region continue to roll out AI features that differentiate service quality and justify premium licensing.

Asia-Pacific is the fastest-growing arena with a 28.6% CAGR. The region processes more than half of the world's digital payments, and B2C e-commerce is projected to exceed EUR 4 trillion (USD 4.3 trillion) by 2027 (tmcnet.com). India's Unified Payments Interface aims beyond 200 billion annual transactions, intensifying demand for scalable signature engines. Hospitality, logistics, and public administration segments likewise embrace digital contracts to keep pace with a mobile-first consumer base. Regulatory heterogeneity remains, yet countries such as Indonesia recognize digital contracts provided core consent principles are satisfied (mondaq.com), signaling gradual convergence.

Europe benefits from the harmonized eIDAS regime, where qualified electronic signatures hold equivalence with handwritten ones (helpx.adobe.com). The forthcoming eIDAS 2.0 provisions and the EU Digital Identity Wallet promise seamless cross-border signing, reinforcing market confidence. Latin America and the Middle East and Africa record smaller baselines but high growth rates. Government digitization programs in Brazil and Gulf economies, coupled with expanding broadband access, create favorable conditions for the digital transaction management industry in those territories.

- Adobe Inc.

- DocuSign, Inc.

- Dropbox, Inc.

- Nintex Global Ltd.

- Namirial S.p.A.

- OneSpan Inc.

- Wolters Kluwer N.V.

- Entrust Corporation

- SignEasy Inc.

- Mitratech Holdings Inc.

- Sertifi, Inc.

- Thales Group (Gemalto N.V.)

- Nitro Software Ltd.

- airSlate Inc.

- PandaDoc Inc.

- Conga (Apttus Corporation)

- Zoho Corporation Pvt. Ltd.

- ZorroSign, Inc.

- Topaz Systems Inc.

- InfoCert S.p.A.

- AssureSign LLC

- eOriginal, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating E-Signature Adoption Across Regulated Industries

- 4.2.2 Shift Toward End-to-End Contract Lifecycle Automation in BFSI and Government

- 4.2.3 Mandatory Remote-Work Compliance Spurring Cloud-Based DTM Uptake

- 4.2.4 Generative-AI Assistants Reducing Document Turn-Around Times

- 4.2.5 Click-Wrap Acceptance Driving E-Commerce Conversion in Asia

- 4.2.6 Digital Identity Frameworks (eIDAS 2.0, Aadhaar, NID) Catalyzing Adoption

- 4.3 Market Restraints

- 4.3.1 Complex Cross-Border Crypto-Signature Regulations

- 4.3.2 High Cost of Qualified Remote ID Assurance in Emerging Markets

- 4.3.3 Fragmented Legacy Core-Banking Workflows Hindering Full Automation

- 4.3.4 Limited 5G / Edge Infrastructure in Rural Areas Slowing Mobile DTM Usage

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Macroeconomic Trend Impact Assessment

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-premise

- 5.3 By Organization Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By End-user Industry

- 5.4.1 Banking, Financial Services and Insurance

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Retail and E-commerce

- 5.4.4 Government and Public Sector

- 5.4.5 IT and Telecommunications

- 5.4.6 Education

- 5.4.7 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Adobe Inc.

- 6.4.2 DocuSign, Inc.

- 6.4.3 Dropbox, Inc.

- 6.4.4 Nintex Global Ltd.

- 6.4.5 Namirial S.p.A.

- 6.4.6 OneSpan Inc.

- 6.4.7 Wolters Kluwer N.V.

- 6.4.8 Entrust Corporation

- 6.4.9 SignEasy Inc.

- 6.4.10 Mitratech Holdings Inc.

- 6.4.11 Sertifi, Inc.

- 6.4.12 Thales Group (Gemalto N.V.)

- 6.4.13 Nitro Software Ltd.

- 6.4.14 airSlate Inc.

- 6.4.15 PandaDoc Inc.

- 6.4.16 Conga (Apttus Corporation)

- 6.4.17 Zoho Corporation Pvt. Ltd.

- 6.4.18 ZorroSign, Inc.

- 6.4.19 Topaz Systems Inc.

- 6.4.20 InfoCert S.p.A.

- 6.4.21 AssureSign LLC

- 6.4.22 eOriginal, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

数位交易管理市场:依部署模式、组件、产业及企业规模划分-2026-2032年全球市场预测

数位交易管理市场:依部署模式、组件、产业及企业规模划分-2026-2032年全球市场预测 全球数位交易管理市场规模、份额、趋势和成长分析报告(2026-2034)

全球数位交易管理市场规模、份额、趋势和成长分析报告(2026-2034) 数位交易管理市场-全球产业规模、份额、趋势、机会、预测:按解决方案、组件、最终用户、地区和竞争对手划分,2021-2031年

数位交易管理市场-全球产业规模、份额、趋势、机会、预测:按解决方案、组件、最终用户、地区和竞争对手划分,2021-2031年 数位交易管理市场规模、份额和成长分析(按组件、解决方案、部署模式、最终用户、垂直产业和地区划分)-2026-2033年产业预测

数位交易管理市场规模、份额和成长分析(按组件、解决方案、部署模式、最终用户、垂直产业和地区划分)-2026-2033年产业预测 2025年数位交易管理全球市场报告

2025年数位交易管理全球市场报告 全球数位交易管理市场

全球数位交易管理市场 数位交易管理市场(按组件和地区)数位交易管理市场,2026-2032:按组件、部署模型、垂直产业和地区划分

数位交易管理市场(按组件和地区)数位交易管理市场,2026-2032:按组件、部署模型、垂直产业和地区划分 欧洲数位交易管理 (DTM):市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

欧洲数位交易管理 (DTM):市场占有率分析、行业趋势和统计、成长预测(2025-2030 年) 数位交易管理市场规模、份额、趋势分析报告:按组件、按解决方案、按最终用户、按行业、按地区、细分市场预测,2025-2030 年

数位交易管理市场规模、份额、趋势分析报告:按组件、按解决方案、按最终用户、按行业、按地区、细分市场预测,2025-2030 年