|

市场调查报告书

商品编码

1851834

机械安全:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Machine Safety - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

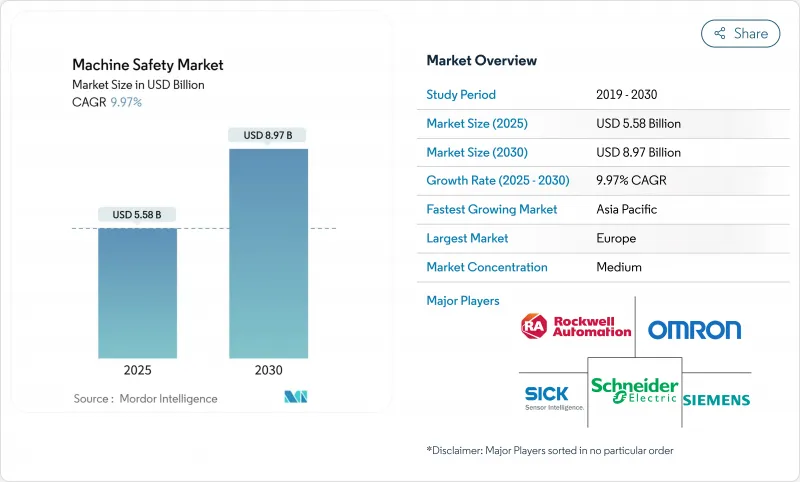

预计到 2025 年,机械安全市场规模将达到 55.8 亿美元,到 2030 年将达到 89.7 亿美元,年复合成长率为 9.97%。

日益增长的监管压力、快速发展的工业自动化以及功能安全与网路安全的整合是推动这一成长的核心动力。欧洲即将实施的《机械法规2023/1230》正促使全球製造商采用性能等级e(Performance Level e)功能,并加强安全系统以抵御数位威胁(ec.europa.eu)。同时,北美食品饮料製造商正在进行数位化维修,将工业4.0资料流与安全合规性结合(automate.org)。随着终端用户从硬线继电器转向软体定义安全逻辑,能够提供整合安全PLC、预测性维护分析和经认证的网路安全架构的供应商正在赢得市场份额。

全球机械安全市场趋势与洞察

协作机器人在东亚电子组装线的应用加速

中国、韩国和台湾的电子产品製造商正在用协作机器人取代孤立的工业机器人,这些机器人可以与操作人员共用工作空间。动态感应光栅和3D视觉防护区域仅在人员处于危险之中时才会停止协作机器人,从而将生产线整体生产率提高18%,并将可记录事故减少27%。嵌入机器人控制器的AI安全逻辑能够实现速度与距离监控,而非强制停止,进而进一步缩短生产週期。因此,为电子代工製造商提供认证安全扫描器、安全扭矩切断驱动器和软体可配置PLC的元件供应商的订单量显着增长。随着电子组装竞相填补区域劳动力短缺并保持出口竞争力,预计未来三年协作机器人的应用浪潮将达到顶峰。

欧盟机械法规 2023/1230 要求自 2027 年起,新设备必须具备性能等级为 e 的安全特性。

该法规将于2027年1月20日生效,对关键功能引入了具有法律约束力的PL-e要求,并包含明确的网路安全条款,将骇客攻击导致的故障归类为安全隐患。因此,向欧盟供货的机械製造商必须检验其安全相关的控制部件能够承受随机硬体故障和蓄意攻击。这种双重合规要求推动了对整合式安全控制器和经认证的安全远端更新机制的需求。由于该法规无需各国自行转换即可直接生效,供应商可以将单一架构扩展到所有27个成员国,从而简化其产品开发流程。德国和义大利的原始设备製造商(OEM)为了避免最后时刻的重新设计,已经明显感受到了包括风险评估、软体修补程式管理和数数位双胞胎模拟在内的准备成本。

棕地遗留控制架构和安全网路的高度整合复杂性

许多 1980 年代的分散式控制系统使用专有总线,这些总线缺乏安全流量的确定性频宽。这迫使整合商依赖通讯协定网关和影子控制器,导致计划成本增加高达 65%,并延长试运行週期。连续流程工厂不愿承受这种停机时间,因此倾向于采取最低限度的合规性措施,减缓了网路安全技术的普及。儘管供应商正在发布「即插即用」的迁移式桥接器和基于模拟的检验工具,但传统硬体与现代功能安全标准之间的结构性不匹配问题可能会持续存在,直到控制系统进行重大改造。

细分市场分析

由于分立元件与棕地设备具有即插即用的兼容性,预计到2024年,它们仍将主导机械安全市场,市场份额将达到65%。然而,随着PLC、驱动器和HMI等设备整合安全韧体,嵌入式元件预计将以11.8%的复合年增长率超越分立元件,从而减少控制柜空间和布线。汽车白车身设计就反映了这一趋势。如今,单一控制器即可同时承载标准运动曲线和PL-e互锁逻辑,无需重复配置处理器。在电子组装,基于微控制器的安全协处理器能够实现低于10毫秒的回应时间,满足高速取放设备在机械安全市场的规模要求。如果供应商能够使其组合控制晶片同时通过IEC 61508和ISO 26262认证,则有望赢得OEM设计订单,因为它们的成本已接近分立继电器。

在改装领域,独立式光栅和联锁装置仍然很受欢迎,因为安装人员可以在周末停机期间更换硬件,而无需重新检验基础PLC代码。然而,即使在改造领域,具有双通道安全输入的「切片式」I/O模组也越来越受欢迎,它允许机柜在单一背板上同时容纳标准线路和安全线路。一旦安全CPU获得认证,即可在现场下载软体更改,而无需重新连接实体继电器,从而加快投资回报,尤其适用于季节性包装作业。

到2024年,存在感应式安全感测器将占总收入的30%,几乎为所有安全系统提供支持,从弯折压床到堆垛机,无所不包。光学和雷达感测器整合了静音逻辑,能够区分负载和人员,从而最大限度地减少输送系统中的误停。安全PLC是成长最快的细分市场,年复合成长率达12.5%,因为柔性製造需要可程式区域和快速逻辑重配置。从硬连线触点到参数化功能块的转变,可将电气图减少高达60%,并支援数位双胞胎在实施前检验变更。

最新的安全PLC还整合了安全启动韧体和加密通讯,满足欧盟机械法规对网路安全和功能安全的双重要求。随着OEM厂商向整合控制面板的迁移,安全PLC的机械安全市场规模进一步扩大。在整合控制面板中,单一CPU即可执行符合IEC 61131标准的各项任务以及SIL-3等级的诊断功能。组件供应商正在捆绑提供经过认证的安全扭力切割、安全限速和安全位置库,从而缩短了机械製造商的应用开发时间。

区域分析

欧洲预计到2024年将占据31%的市场份额,凸显了其作为监管引领者和自动化先驱的地位。德国的汽车、化学和工具机製造商正在将连网安全系统整合到几乎所有新生产线中,其中68%的设备已将诊断资料传输到中央控制面板。义大利的包装OEM厂商正在向北美和南美出口符合PL-e标准的灌装剂,进一步增强了欧洲的技术外溢效应。英国正在效仿欧盟标准以保障出口准入,而法国的航太工厂正在引入协作机器人防护装置,以实现人机在机翼组装单元中的协同工作。

亚太地区是一个至关重要的成长区域,预计复合年增长率将达到11.6%。中国的电子组装正竞相满足国内GB安全标准和出口所需的CE认证,促使他们对光栅和安全运动驱动器的需求激增。日本机器人製造商正在其机械手臂中整合双通道扭力感测器,以实现ISO 13849合规性,并提高人机共用工作站的接受度。在印度,跨国製药和汽车製造商正在新建待开发区安装3类和4类系统,以提高当地安全意识并鼓励供应商在地化。韩国晶片製造厂正在为超高纯度化学品生产线采购SIL等级的阀组,这些阀组将功能安全性与低颗粒物结构相结合,以保护人员和晶圆的安全。

北美仍是技术领先者,但成长更为稳定。美国加工商正在升级安全措施以降低责任和保险成本,42%的食品加工厂计划在2025年进行重大现代化改造。加拿大采矿业正在矿用卡车通道采用无线SIL-3紧急停机网路。拉丁美洲的普及程度不一。巴西汽车产业丛集正在适应欧盟和美国客户的需求,但小型工厂的投资相对落后。中东和非洲地区在高风险能源领域发展最为迅速,正在炼油厂和LNG接收站部署整合式火灾和气体防护以及紧急停机系统。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 协作机器人在东亚电子组装线的应用加速

- 欧盟机械法规 2023/1230 将要求自 2027 年起,新设备必须具备 e 级安全性能。

- 北美某食品饮料厂快速棕地数位化改造项目,引进安全I/O连结感测器

- 中东地区液化天然气大型企划的快速成长增加了对SIL-3级紧急停车系统的需求。

- 超过 OSHA TRIR基准值的工厂工伤保险费上涨,将促使美国小型企业寻求第四类安全解决方案。

- 欧洲包装生产线从硬线继电器转向软体可配置安全PLC,实现了灵活包装。

- 市场限制

- 棕地安全网路与传统控制架构的高度整合复杂性

- 受电动车需求波动影响,二级汽车供应商冻结资本预算

- 新兴市场缺乏符合IEC 61508/62061标准的、具备功能安全软体程式设计技能的人才。

- 东南亚中小企业对四类安全系统过度设计与投资报酬率不确定性的认知

- 价值/供应链分析

- 监理展望

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 竞争对手之间的竞争

- 替代品的威胁

- 投资分析

第五章 市场规模与成长预测

- 透过实施

- 各个部件

- 内建零件

- 改装安全升级

- 按组件

- 存在检测安全感测器

- 安全光栅

- 安全雷射扫描仪

- 紧急停止装置

- 安全联锁切换

- 安全控制器/模组/继电器

- 安全PLC

- 双手控制和启用开关

- 其他零件(垫子、边缘、缓衝垫)

- 透过使用

- 物料输送

- 机器人技术与协作机器人

- 包装和托盘堆垛

- 切割、成型、加工

- 组装和拾取放置

- 按最终用途行业划分

- 车

- 饮食

- 电子和半导体

- 石油和天然气

- 医药和医疗保健

- 化学

- 金属和采矿

- 航太/国防

- 包装产业

- 其他行业

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 中东

- 以色列

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Rockwell Automation, Inc.

- Siemens AG

- Schneider Electric SE

- Omron Corporation

- Sick AG

- Pilz GmbH and Co. KG

- Mitsubishi Electric Corporation

- ABB Ltd.

- Honeywell International Inc.

- Keyence Corporation

- IDEC Corporation

- Banner Engineering Corp.

- Phoenix Contact GmbH and Co. KG

- Datalogic SpA

- Bihl+Wiedemann GmbH

- Euchner GmbH+Co. KG

- Leuze electronic GmbH+Co. KG

- Wenglor sensoric GmbH

- Rockford Systems LLC

- Fortress Safety

第七章 市场机会与未来展望

The machine safety market size at USD 5.58 billion in 2025 and is forecast to climb to USD 8.97 billion by 2030, advancing at a 9.97% CAGR.

Heightened regulatory pressure, rapid industrial automation and the growing convergence of functional-safety with cybersecurity are the core forces behind this growth. Europe's upcoming Machinery Regulation 2023/1230 is compelling manufacturers worldwide to embed Performance Level e functions and to harden safety systems against digital threats ec.europa.eu. Asia-Pacific's expanding electronics and automotive bases are accelerating demand for adaptive safeguarding, while North American food and beverage processors are pursuing digital retrofits that combine Industry 4.0 data flows with safety compliance automate.org. Vendors that can offer integrated safety PLCs, predictive-maintenance analytics and certified cyber-secure architectures are capturing share as end-users transition from hard-wired relays to software-defined safety logic.

Global Machine Safety Market Trends and Insights

Accelerated Adoption of Collaborative Robots in Electronics Assembly Lines across East Asia

Electronics producers in China, South Korea and Taiwan are replacing isolated industrial robots with collaborative units that share workspaces with operators. Dynamic presence-sensing light curtains and 3D vision guard zones now stop cobots only when a person is at risk, lifting overall line productivity by 18% while cutting recordable incidents by 27%. AI-powered safety logic embedded in the robot controller enables speed-and-separation monitoring rather than hard stops, which further shortens cycle times. Component vendors supplying certified safety scanners, safe torque off drives and software-configurable PLCs are therefore experiencing outsized order growth from contract electronics manufacturers. The wave of cobot deployment is expected to peak over the next three years as electronics assemblers race to offset regional labor shortages and maintain export competitiveness.

EU Machinery Regulation 2023/1230 Mandating Performance Level e Safety Functions in New Equipment from 2027

The regulation, entering force on 20 January 2027, introduces legally binding PL-e requirements for critical functions and embeds explicit cybersecurity clauses that classify hacking-induced malfunction as a safety hazard. Machine builders supplying the EU must therefore validate that safety-related control parts withstand both random hardware faults and intentional attacks. This dual compliance need is fueling demand for integrated safety-security controllers and certified secure remote-update mechanisms. Because the rule applies directly without national transposition, suppliers can scale one architecture across all 27 member states, streamlining product-development pipelines. Preparatory spending on risk assessments, software patch management and digital-twin simulation is already evident among German and Italian OEMs looking to avoid last-minute redesigns.

High Integration Complexity of Safety Networks with Legacy Control Architecture in Brownfield Sites

Many 1980s-era distributed-control systems use proprietary buses lacking deterministic bandwidth for safety traffic. Integrators therefore resort to protocol gateways and shadow controllers, inflating project costs by up to 65% and extending commissioning windows. Continuous-process plants resist such downtime, opting for minimum-compliance fixes that slow the adoption of networked safety. Although vendors are releasing "plug-in" migration bridges and simulation-based validation tools, the structural mismatch between legacy hardware and modern functional-safety standards will persist until large-scale control-system overhauls occur.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Brownfield Digital Retrofit Programs in North-American Food & Beverage Plants Incorporating Safety I/O-Link Sensors

- Surge in LNG Megaprojects in the Middle East Elevating Demand for SIL-3 Rated Emergency Shutdown Systems

- Capital Budget Freezes in Automotive Tier-2 Suppliers Amid EV Demand Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Individual components continued to dominate in 2024 with a 65% machine safety market share due to their plug-and-play compatibility with brownfield equipment. However, embedded components are forecast to outpace at an 11.8% CAGR as PLCs, drives and HMIs ship with integrated safety firmware, trimming cabinet space and wiring. Automotive body-in-white lines illustrate the trend: a single controller now hosts both standard motion profiles and PL-e interlock logic, eliminating duplicate processors. In electronics assembly, microcontroller-based safety co-processors handle reaction times below 10 ms, satisfying the machine safety market size requirement for high-speed pick-and-place equipment. Suppliers that certify combo-control chips under both IEC 61508 and ISO 26262 are positioned to capture OEM design wins as cost parity with discrete relays approaches.

The retrofit arena still favors discrete light curtains and interlocks because installers can swap hardware during weekend shutdowns without revalidating the base PLC code. Yet even here, "slice" I/O modules with dual-channel safety inputs are edging in, allowing cabinets to host standard and safety wiring on one backplane. Regulatory harmonization across Europe and the Americas is also tilting investment toward embedded solutions; once a safety CPU is certified, software changes can be field-downloaded rather than rewiring physical relays, delivering faster ROI especially in seasonal packaging operations.

Presence-sensing safety sensors accounted for 30% of revenue in 2024, underpinning virtually every safeguarding scheme from press brakes to palletizers. Optical and radar variants now incorporate muting logic that differentiates payload from personnel, minimizing nuisance stops in conveyor systems. Safety PLCs represent the fastest-growing sub-segment at 12.5% CAGR because flexible manufacturing demands programmable zones and high-speed logic reconfiguration. The transition from hard-wired contacts to parameterized function blocks reduces electrical drawings by up to 60% and enables digital twins that validate changes before deployment.

Modern safety PLCs also embed secure-boot firmware and encrypted communications, satisfying the dual requirement of cybersecurity and functional safety posed by the EU Machinery Regulation. The machine safety market size for safety PLCs is further lifted by the migration of OEMs to unified control panels where one CPU executes both standard IEC 61131 tasks and SIL-3 diagnostics. Component suppliers are bundling pre-certified libraries for safe torque off, safe limited speed and safe position, shortening application development time for machine builders.

The Machine Safety Market Report is Segmented by Implementation (Individual Components, Embedded Components, and More), Component (Presence-Sensing Safety Sensors, Safety Light Curtains, Safety Laser Scanners, and More), Application (Material Handling, Robotics & Collaborative Robots, and More), End User (Automotive, Food & Beverage, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe's 31% share in 2024 underscores its role as regulatory pacesetter and automation pioneer. German automotive, chemical and machine-tool builders integrate networked safety backbones on virtually every new line, and 68% of installations already stream diagnostic data to central dashboards. Italian packaging OEMs export PL-e compliant fillers to North and South America, amplifying Europe's technology spillover. The United Kingdom mirrors EU norms to protect export access, while French aerospace plants deploy collaborative-robot guarding to co-locate humans and robots in wing-assembly cells.

Asia-Pacific, projected to post an 11.6% CAGR, is the pivotal growth arena. China's electronics assemblers rush to meet both domestic GB safety codes and CE marking for export, driving volume orders of light curtains and safe-motion drives. Japan's robotics makers embed dual-channel torque sensors in arms, enabling built-in ISO 13849 compliance and boosting acceptance of humans and robots in shared workstations. India sees multinational pharma and automotive OEMs installing Category 3 and 4 systems at new greenfield sites, lifting local awareness and triggering supplier localization. South Korean chip fabs procure SIL-rated valve-manifolds for ultrapure chemical lines, combining functional-safety with low-particulate construction to safeguard both personnel and wafers.

North America remains a technology leader, yet growth is steadier. US processors upgrade safety to mitigate liability and insurance costs, with 42% of food plants planning major modernizations in 2025. Canada's mining sector adopts wireless SIL-3 emergency-stop networks for haul-truck corridors. Latin American adoption is uneven: Brazil's automotive clusters align with EU and US customer mandates, whereas smaller factories delay investments. The Middle East & Africa region expands fastest in high-risk energy sectors, installing integrated fire-and-gas plus ESD systems at refineries and LNG terminals.

- Rockwell Automation, Inc.

- Siemens AG

- Schneider Electric SE

- Omron Corporation

- Sick AG

- Pilz GmbH and Co. KG

- Mitsubishi Electric Corporation

- ABB Ltd.

- Honeywell International Inc.

- Keyence Corporation

- IDEC Corporation

- Banner Engineering Corp.

- Phoenix Contact GmbH and Co. KG

- Datalogic S.p.A.

- Bihl + Wiedemann GmbH

- Euchner GmbH + Co. KG

- Leuze electronic GmbH + Co. KG

- Wenglor sensoric GmbH

- Rockford Systems LLC

- Fortress Safety

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Adoption of Collaborative Robots in Electronics Assembly Lines across East Asia

- 4.2.2 EU Machinery Regulation 2023/1230 Mandating Performance Level e Safety Functions in New Equipment from 2027

- 4.2.3 Rapid Brownfield Digital Retrofit Programs in North American Food and Beverage Plants Incorporating Safety I/O-Link Sensors

- 4.2.4 Surge in LNG Megaprojects in Middle East Elevating Demand for SIL-3 Rated Emergency Shutdown Systems

- 4.2.5 Rising Insurance Premium Penalties for Plant Injuries Above OSHA TRIR Thresholds Pushing US SMEs toward Category 4 Safety Solutions

- 4.2.6 Shift from Hard-wired Relays to Software-Configurable Safety PLCs Enabling Flexible Packaging Lines in Europe

- 4.3 Market Restraints

- 4.3.1 High Integration Complexity of Safety Networks with Legacy Control Architecture in Brownfield Sites

- 4.3.2 Capital Budget Freezes in Automotive Tier-2 Suppliers Amid EV Demand Volatility

- 4.3.3 Limited Skilled Workforce to Program Functional-Safety Software per IEC 61508/62061 in Emerging Markets

- 4.3.4 Perception of Over-Engineering and ROI Uncertainty for Category-4 Safety Systems among Southeast-Asian SMEs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitutes

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Implementation

- 5.1.1 Individual Components

- 5.1.2 Embedded Components

- 5.1.3 Retrofit Safety Upgrades

- 5.2 By Component

- 5.2.1 Presence-Sensing Safety Sensors

- 5.2.2 Safety Light Curtains

- 5.2.3 Safety Laser Scanners

- 5.2.4 Emergency Stop Devices

- 5.2.5 Safety Interlock Switches

- 5.2.6 Safety Controllers / Modules / Relays

- 5.2.7 Safety PLCs

- 5.2.8 Two-Hand Controls and Enabling Switches

- 5.2.9 Other Components (Mats, Edges, Bumpers)

- 5.3 By Application

- 5.3.1 Material Handling

- 5.3.2 Robotics and Collaborative Robots

- 5.3.3 Packaging and Palletizing

- 5.3.4 Cutting, Forming and Machining

- 5.3.5 Assembly and Pick-and-Place

- 5.4 By End-Use Industry

- 5.4.1 Automotive

- 5.4.2 Food and Beverage

- 5.4.3 Electronics and Semiconductor

- 5.4.4 Oil and Gas

- 5.4.5 Pharmaceuticals and Healthcare

- 5.4.6 Chemicals

- 5.4.7 Metals and Mining

- 5.4.8 Aerospace and Defense

- 5.4.9 Packaging Industry

- 5.4.10 Other Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Rockwell Automation, Inc.

- 6.4.2 Siemens AG

- 6.4.3 Schneider Electric SE

- 6.4.4 Omron Corporation

- 6.4.5 Sick AG

- 6.4.6 Pilz GmbH and Co. KG

- 6.4.7 Mitsubishi Electric Corporation

- 6.4.8 ABB Ltd.

- 6.4.9 Honeywell International Inc.

- 6.4.10 Keyence Corporation

- 6.4.11 IDEC Corporation

- 6.4.12 Banner Engineering Corp.

- 6.4.13 Phoenix Contact GmbH and Co. KG

- 6.4.14 Datalogic S.p.A.

- 6.4.15 Bihl + Wiedemann GmbH

- 6.4.16 Euchner GmbH + Co. KG

- 6.4.17 Leuze electronic GmbH + Co. KG

- 6.4.18 Wenglor sensoric GmbH

- 6.4.19 Rockford Systems LLC

- 6.4.20 Fortress Safety

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

机械安全市场(按组件、安全功能、连接方式、安装类型和最终用途行业)—2025-2032 年全球预测

机械安全市场(按组件、安全功能、连接方式、安装类型和最终用途行业)—2025-2032 年全球预测 2025年机械安全全球市场报告

2025年机械安全全球市场报告 机械安全市场,按实施、按组件、按最终用途行业、按国家和地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额及预测

机械安全市场,按实施、按组件、按最终用途行业、按国家和地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额及预测 全球机器风险评估市场

全球机器风险评估市场 2025 年至 2033 年机械安全市场报告(按实施、组件、最终用途行业和地区)

2025 年至 2033 年机械安全市场报告(按实施、组件、最终用途行业和地区) 机械安全市场-2025-2035年全球产业分析、规模、份额、成长、趋势及预测

机械安全市场-2025-2035年全球产业分析、规模、份额、成长、趋势及预测 机械安全市场规模、份额和成长分析(按实施、销售管道、应用、产品、组件、垂直和地区)- 2025-2032 年产业预测2024 - 2032 年机器安全市场机会、成长动力、产业趋势分析与预测

机械安全市场规模、份额和成长分析(按实施、销售管道、应用、产品、组件、垂直和地区)- 2025-2032 年产业预测2024 - 2032 年机器安全市场机会、成长动力、产业趋势分析与预测 2030 年机械安全市场预测:按类型、组件、应用、最终用户和地区进行的全球分析

2030 年机械安全市场预测:按类型、组件、应用、最终用户和地区进行的全球分析 2023-2030 年全球机器安全市场规模研究与预测(按产品、零件、程序工业、离散产业和区域分析)

2023-2030 年全球机器安全市场规模研究与预测(按产品、零件、程序工业、离散产业和区域分析)