|

市场调查报告书

商品编码

1851892

自动贴标机:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Automatic Labeling Machine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

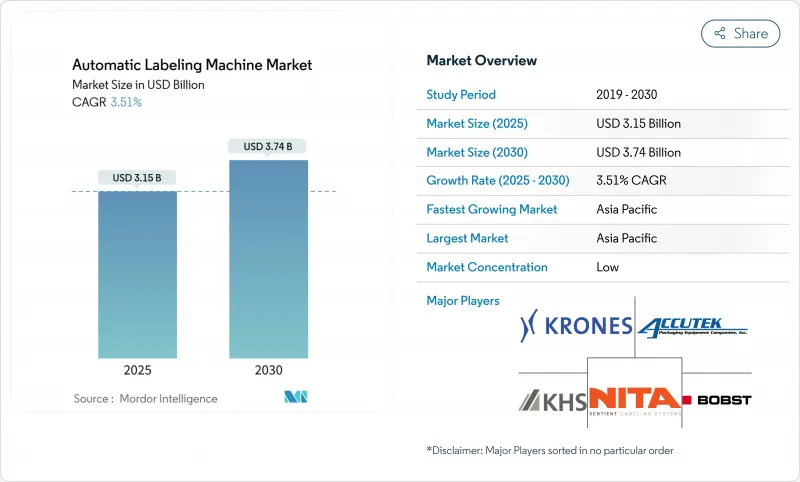

预计到 2024 年,自动贴标机市场规模将达到 30.6 亿美元,到 2030 年将扩大到 37.4 亿美元,复合年增长率为 3.51%。

这一前景反映了包装产业日趋成熟但稳定扩张的趋势,监管合规、工厂级自动化和智慧包装能力不断推动设备升级。药品产业更严格的序列化法规、精酿饮料SKU的激增、物流自动化以及无内衬永续性要求,都在增强对设备的需求。如今,竞争优势的关键在于整合RFID/NFC功能、人工智慧主导的品管和预测性维护,以减少停机时间和整体拥有成本。儘管黏合剂和标籤价格波动以及劳动力短缺仍然是限制因素,但由于合规期限依然紧迫且产能压力持续存在,大多数终端用户仍在继续投资自动化。

全球自动贴标机市场趋势与洞察

对智慧包装可追溯性的需求日益增长

品牌拥有者如今将标籤视为认证和消费者互动的重要触点。区块链溯源计画要求所有商品都必须拥有唯一的数位ID,引导买家使用视觉认证和RFID编码的列印贴上系统。製药公司正在积极回应,因为序列化包装已成为强制性要求;而食品和个人护理品牌则利用QR码来储存食谱资料、进行会员宣传活动并提供仿冒品保障。因此,生产线製造商正在整合物联网感测器和人工智慧演算法,以即时检验二维码并将精细的生产数据传输到ERP系统中。即将出台的欧盟数位产品护照法案很可能将智慧标籤确立为基本要求,而非一项进阶功能。因此,资本预算越来越重视连结性和资料完整性,而非原始的处理能力。

小批量精酿饮料SKU的激增

独立啤酒厂和特色饮料品牌正在大力推动前所未有的口味轮换和季节性包装。 500 至 5000 件的大量生产要求印刷机能够在几分钟内而非几小时内完成换版。模组化印刷头和伺服控制送料器最大限度地减少了停机时间,而整合式数位印刷机无需储存印刷捲即可处理可变图形。这项技术在美国和西欧的应用最为广泛,但在澳洲和日本的精酿啤酒产业也开始兴起。供应商正在积极回应,推出将印刷、防篡改封条贴附和摄影机侦测整合在单一托盘上的紧凑型系统。这种多功能性使小型生产商能够快速推出小众口味,同时也能满足大型零售商对标籤精度的要求。

高资本支出与租赁/合约打包方案的比较

配备序列化、视觉识别和OEE分析功能的先进模组化贴标机售价可能超过50万美元,这令注重现金流的小型品牌望而却步。合约包装公司正在大力推广计量型的服务模式,虽然降低了固定成本,但随着时间的推移却会推高单价。设备製造商正在尝试租赁和机器人即服务(RaaS)模式,但用户担心技术锁定和合约期间内升级带来的干扰。製药和个人护理公司由于其产品需要频繁更新包装设计,因此倾向于外包,并可能推迟内部投资,直到销售稳定下来。

细分市场分析

由于压敏贴标机能够处理玻璃、PET 和金属等多种材质,且只需极少的更换零件,预计到 2024 年,其收入将保持 39.84% 的成长。这类贴标机占据自动化贴标机市场最大的份额,规模达 12.2 亿美元。收缩套标和拉伸套成长最为强劲,复合年增长率 (CAGR) 为 5.65%,这主要得益于饮料公司对全方位品牌推广和防拆封的需求,尤其是在精酿产品方面。套标还能增强薄壁宝特瓶的强度,因为轻量化设计需要结构支撑。湿式贴标机将在大批量啤酒和罐头食品生产线上蓬勃发展,因为在这些行业中,单张标籤的成本比多功能性更为重要。套模技术虽然仍处于小众市场,但在个人护理标籤领域正逐渐获得认可,因为这些标籤需要具有防潮性和高端美观。

容器重量的减轻和优质化趋势正朝着相反的方向推动技术发展。轻质瓶身更适合使用套标,而顶级烈酒则偏好纹理纸,这种纸张只能透过压敏喷头以极高的精度进行贴标。可在胶合和套标模式之间切换的混合工作站有助于管理SKU多样性,而无需增加平行生产线,从而增强了市场对可转换平台的需求。数位印刷单元现在可以直接连接到扭矩控制施用器上,无需单独的仓库即可实现符合当地法规的后期图形设计。无论采用何种技术,供应商都透过可回收标籤材料、水溶性黏合剂和智慧标籤相容性来满足未来工厂布局的需求,从而实现差异化竞争。

至2024年,线上式贴标机将占总销售量的62.54%,凸显其作为高速填充、罐装和装箱生产线基准的地位。这一地位使其成为自动化贴标机市场份额中占比最大的部分。然而,随着生产商优先考虑缩短产品週期所需的灵活规格,模组化/混合式架构正以6.36%的复合年增长率成长。伺服分度器和滑入式施用器头使操作人员能够在10分钟内完成从环绕式贴标到顶部贴标的切换。虽然旋转式转盘贴标机对于每小时产量5万瓶的啤酒厂仍然至关重要,但基于伺服的线性平台现在可以在降低零件尺寸复杂性的同时,达到类似的贴标速度。

配置决策越来越依赖数位化连接。使用者希望整合 OPC UA 或 MQTT 网关,将 OEE 资料流传输到 MES 控制面板,并倾向于选择拥有成熟的工业 4.0 库的供应商。列印贴标模组在电商平台中占据主导地位,每个标籤都由可变数据驱动;协作机器人将贴标头安装在移动底座上,以支援多行列印的灵活性。供应商透过预测性维护演算法来区分其产品,这些演算法可以标记潜在的胶水加热器故障或捲材断裂,从而在严格的履约等级协定 (SLA) 下减少非计划性停机时间。

区域分析

亚太地区预计到2024年将占全球销售额的40.36%,并将在2030年之前保持领先地位,年复合成长率(CAGR)为6.35%。中国的饮料工厂现代化改造正在蓬勃发展,而印度的标准化生产措施正在推动单厂投资超过2,000万美元的大型计划。劳动力短缺促使日本和韩国的工厂部署人工智慧辅助视觉和预测性维护系统,以维持设备综合效率(OEE)在85%以上。随着跨国消费品公司供应链的区域化,东南亚的合约包装商正在崛起,推动了对中阶贴标机的需求。

北美市场的需求仍受监管主导。 《药品供应链安全法案》设定了2027年的明确里程碑,确保了改造和新药品订单的稳定成长。由于产品库存週转快,美国和加拿大的精酿饮料製造商越来越多地采用模组化系统。加州强制使用再生材料等永续性倡议,正在推动无衬纸包装和可回收黏合剂的应用,并促使与大学和设备原始设备製造商开展先导计画。

欧洲整体经济成长放缓,但产品规格水准却在不断提高。德国啤酒製造商正大力投资产能超过每小时6万瓶的旋转式包装机,而义大利化妆品工厂则采用套贴技术打造高阶产品。欧盟的循环经济目标正在加速无底纸非标籤药物的普及,并促使供应商在报价阶段提供碳足迹认证。受电子和汽车供应链近岸外包的推动,东欧正在升级为符合规范的危险品运输标籤列印贴上系统。

拉丁美洲和中东/非洲地区仍蕴藏着巨大的机会。巴西价值2,310亿美元的食品业正在投资半自动化设备,以提高出口到美国和欧盟产品的包装一致性。墨西哥的标籤市场规模将从2025年的13.1亿美元成长到2030年的16.2亿美元,这将使提供西班牙语人机介面和本地服务网点的供应商受益。海湾地区的饮料製造商和非洲的农产品加工商正在试行使用云端贴标机,以弥补现场技术人员的短缺,并在宽频网路不稳定的地区利用卫星连接进行远距离诊断。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 智慧包装对可追溯性的需求日益增长

- 小批量精酿饮料SKU的激增

- 履约中心的成长

- 更严格的序列化/UDI规则(药品和医疗设备)

- 数位按需印刷集成

- 永续性主导的无衬纸标籤转型

- 市场限制

- 高资本支出与租赁/合约打包方案的比较

- 缺乏控制和维护技能

- 原料(标籤库存)价格不稳定

- 多厂商产品线之间的互通性差距

- 供应链分析

- 监管环境

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 进出口分析

- 投资分析

第五章 市场规模与成长预测

- 透过技术

- 压敏/自黏标籤机

- 收缩套标机

- 胶黏式(冷熔、热熔)标籤机

- 袖标机(拉伸,耐热)

- 套模贴标机

- 其他技术

- 透过机器配置

- 线上贴标机

- 旋转式/旋转伺服贴标机

- 列印贴上系统

- 模组化/混合系统

- 透过标记速度

- 低于每分钟 60 次

- 61-200 BPM

- 201-400 BPM

- 超过 400 BPM

- 最终用户

- 食物

- 饮料

- 製药

- 个人护理和化妆品

- 化学和工业

- 物流与电子商务

- 其他最终用户

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲和纽西兰

- 亚太其他地区

- 中东和非洲

- 中东

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 埃及

- 其他非洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Krones AG

- Sidel Group(Tetra Laval)

- KHS GmbH

- SACMI Imola SC

- Accutek Packaging Company, Inc.

- ProMach Inc.

- HERMA GmbH

- Domino Printing Sciences PLC

- Fuji Seal International

- Avery Dennison Corporation

- Weber Packaging Solutions

- Markem-Imaje(Dover)

- Videojet Technologies

- PE Labellers SpA

- Nita Labeling Systems

- Quadrel Labeling Systems

- Pack Leader Machinery

- World Pack Automation Systems

- Arca Labeling & Marking

- Bobst Group SA

- Sato Holdings Corporation

第七章 市场机会与未来展望

The automatic labeling machine market size generated USD 3.06 billion in 2024 and is projected to advance to USD 3.74 billion by 2030 while registering a 3.51% CAGR.

The outlook reflects a maturing but steadily expanding sector where regulatory compliance, plant-level automation, and smart packaging features continue to stimulate equipment upgrades. Heightened serialization rules in pharmaceuticals, craft beverage SKU proliferation, logistics automation, and linerless sustainability mandates all reinforce equipment demand. Competitive differentiation now hinges on integrating RFID/NFC functionality, AI-driven quality control, and predictive maintenance to lower downtime and total cost of ownership. Volatile adhesive and label-stock pricing plus technician shortages remain limiting factors, yet most end users keep automation investments in place because compliance deadlines are non-negotiable and throughput pressures persist.

Global Automatic Labeling Machine Market Trends and Insights

Rising Demand for Smart Packaging Traceability

Brand owners now see labeling as an authentication and consumer-engagement touchpoint. Blockchain traceability programs oblige every item to carry a unique digital identity, nudging purchasers toward print-and-apply systems with vision verification and RFID encoding. Pharma producers comply because serialized packs are mandatory, while food and personal-care brands leverage QR codes for recipe data, loyalty campaigns, and anti-counterfeit assurance. Line builders thus embed IoT sensors plus AI algorithms to validate codes in real time and feed ERP systems with granular production data. The upcoming EU Digital Product Passport law will cement smart labels as a baseline requirement rather than a premium feature. Consequently, capital budgets increasingly prioritize connectivity and data integrity over raw throughput.

Surge in Craft Beverage Short-Run SKUs

Independent breweries and specialty drink brands push unprecedented flavor rotations and seasonal packaging. Batch volumes of 500-5,000 units demand presses that change formats in minutes instead of hours. Modular heads and servo-controlled feeders minimize downtime, while integrated digital printers handle variable graphics without storing pre-printed rolls. Adoption is strongest in the United States and Western Europe, but is now visible in the Australian and Japanese craft segments. Suppliers respond with compact systems combining printing, tamper-band application, and camera inspection within a single skid. Such versatility allows smaller producers to launch niche flavors quickly yet still meet labeling accuracy targets that large retailers enforce.

High CAPEX vs. Rental/Contract Packaging Options

A state-of-the-art modular labeler with serialization, vision, and OEE analytics can exceed USD 500,000, deterring small brands that value cash preservation. Contract packagers pitch pay-as-you-go service models, reducing fixed costs yet often raising unit economics over time. Equipment builders experiment with leasing and Robotics-as-a-Service, but users fear technological lock-in or disruptive mid-contract upgrades. Pharmaceutical and personal-care firms, whose products demand frequent artwork updates, find outsourcing appealing and may postpone in-house investments until volumes stabilize.

Other drivers and restraints analyzed in the detailed report include:

- Growth of E-commerce Fulfillment Centers

- Stricter Serialization/UDI Rules (Pharma and Med-Device)

- Skill Shortage in Controls and Maintenance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pressure-sensitive units retained 39.84% revenue in 2024 because they handle glass, PET, and metal formats with minimal change parts. That share equates to the largest slice of the automatic labeling machine market size at USD 1.22 billion. Shrink and stretch sleeves, however, clock the most vigorous 5.65% CAGR, propelled by beverage firms seeking 360-degree branding and tamper evidence, especially among craft SKUs. Sleeve labels also bolster thin-wall PET bottles, which need structural support once supplied in lightweight designs. Wet-glue machines survive in mass-volume beer and canned food lines where the cost per label eclipses versatility concerns. In-mold technology, while niche, gains traction in personal-care tubs that demand moisture resistance and premium aesthetics.

Container-lightweighting and premiumization pull technology trends in opposite directions. Lightweight bottles favor sleeve support, whereas premium spirits prefer tactile paper stocks only pressure-sensitive heads can dispense at low tolerances. Hybrid stations that switch between adhesive and sleeve modes help users manage SKU diversity without adding a parallel line, reinforcing market appetite for convertible platforms. Digital print units now bolt directly onto torque-controlled applicators, enabling late-stage graphics that meet regional regulations without separate warehousing. Across technology types, vendors court differentiation via recyclable label materials, water-soluble glues, and smart-label compatibility to future-proof capital layouts.

In-line equipment captured 62.54% of 2024 unit sales, underscoring its role as the baseline for high-speed bottling, canning, and case-packing lines. That position equals the largest component of the automatic labeling machine market share. Yet modular/hybrid architectures are rising at 6.36% CAGR as producers prioritize format agility for shorter product cycles. Servo indexers plus slide-in applicator heads let operators swap from wrap-around to top-apply in under 10 minutes. Rotary carousel machines remain essential for 50,000-bottles-per-hour beer plants, but servo-based linear platforms now reach similar speeds while easing size-part complexity.

Configuration decisions increasingly hinge on digital connectivity. Users want embedded OPC UA or MQTT gateways to stream OEE data into MES dashboards, favoring suppliers with proven Industry 4.0 libraries. Print-and-apply modules dominate e-commerce hubs where variable data drives each label, while collaborative robots mount label heads on mobile bases to support multi-line flexibility. Vendors distinguish offers through predictive-maintenance algorithms that flag glue-heater faults or web-break probability, trimming unplanned downtime under tight fulfillment SLAs.

The Automatic Labeling Machine Market Report is Segmented by Technology (Pressure-Sensitive/Self-Adhesive Labelers, Shrink Sleeve Labelers, and More), Machine Configuration(In-Line Labeling Machines, Rotary/Rotary-Servo Labelers, and More), Labelling Speed (61-200 BPM, 201-400 BPM, and More), End User (Food, Beverages, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 40.36% of global revenue in 2024 and preserves first-place momentum with a 6.35% CAGR to 2030. Surging beverage-plant modernization in China and serialization compliance in India underpin big-ticket projects exceeding USD 20 million per facility. Japanese and South Korean factories, pressured by labor shortages, install AI-assisted vision and predictive-maintenance suites to maintain OEE above 85%. Southeast Asian contract packagers multiply as multinational CPG firms regionalize supply chains, boosting mid-range labeler purchases.

North America's demand remains regulatory-driven. The Drug Supply Chain Security Act sets firm milestones through 2027, keeping a steady pipeline of retrofit and greenfield pharmaceutical orders. Craft beverage producers in the United States and Canada account for many modular system deployments owing to brisk SKU turnover. Sustainability pushes, such as California's recycled-content mandate, encourage linerless adoption and recyclable adhesive chemistries, fostering pilot projects with universities and equipment OEMs.

Europe exhibits modest headline growth yet commands high specification levels. German brewers spend heavily on carousel machines surpassing 60,000 BPH, while Italian cosmetics plants adopt sleeve-over-sleeve techniques for premium finishes. EU circular-economy targets accelerate linerless and wash-off label uptake, spurring suppliers to certify carbon footprints at quote stage. Eastern Europe, buoyed by near-shoring electronics and automotive supply chains, upgrades to print-apply systems that comply with hazardous-substance transport labels.

Latin America, Middle East, and Africa remain opportunity pockets. Brazil's USD 231 billion food sector invests in semi-automatic units to lift packaging consistency for exports to the United States and EU. Mexico's label market will stretch from USD 1.31 billion in 2025 to USD 1.62 billion by 2030, rewarding vendors who offer Spanish-language HMIs and regional service depots. Gulf States beverages and African agro-processors pilot cloud-linked labelers to compensate for scarce on-site engineering talent, using remote diagnostics via satellite connections where broadband is unreliable.

- Krones AG

- Sidel Group (Tetra Laval)

- KHS GmbH

- SACMI Imola SC

- Accutek Packaging Company, Inc.

- ProMach Inc.

- HERMA GmbH

- Domino Printing Sciences PLC

- Fuji Seal International

- Avery Dennison Corporation

- Weber Packaging Solutions

- Markem-Imaje (Dover)

- Videojet Technologies

- P.E. Labellers S.p.A.

- Nita Labeling Systems

- Quadrel Labeling Systems

- Pack Leader Machinery

- World Pack Automation Systems

- Arca Labeling & Marking

- Bobst Group SA

- Sato Holdings Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for smart packaging traceability

- 4.2.2 Surge in craft beverage short-run SKUs

- 4.2.3 Growth of e-commerce fulfillment centers

- 4.2.4 Stricter serialization/UDI rules (pharma and med-device)

- 4.2.5 Digital print-on-demand integration

- 4.2.6 Sustainability-driven shift to linerless labels

- 4.3 Market Restraints

- 4.3.1 High CAPEX vs. rental/contract packaging options

- 4.3.2 Skill shortage in controls and maintenance

- 4.3.3 Volatile raw-material (label stock) prices

- 4.3.4 Interoperability gaps across multi-vendor lines

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Anlaysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Import and Export Analysis

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Pressure-Sensitive / Self-Adhesive Labelers

- 5.1.2 Shrink-Sleeve Labelers

- 5.1.3 Glue-Based (Cold, Hot-Melt) Labelers

- 5.1.4 Sleeve (Stretch, Heat) Labelers

- 5.1.5 In-mold Labelers

- 5.1.6 Other Technologies

- 5.2 By Machine Configuration

- 5.2.1 In-line Labeling Machines

- 5.2.2 Rotary / Rotary-Servo Labelers

- 5.2.3 Print-and-Apply Systems

- 5.2.4 Modular / Hybrid Systems

- 5.3 By Labelling Speed

- 5.3.1 less than 60 BPM

- 5.3.2 61-200 BPM

- 5.3.3 201-400 BPM

- 5.3.4 More than 400 BPM

- 5.4 By End User

- 5.4.1 Food

- 5.4.2 Beverages

- 5.4.3 Pharmaceutical

- 5.4.4 Personal Care and Cosmetics

- 5.4.5 Chemicals and Industrial

- 5.4.6 Logistics and E-commerce

- 5.4.7 Other End Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 United Arab Emirates

- 5.5.4.1.2 Saudi Arabia

- 5.5.4.1.3 Turkey

- 5.5.4.1.4 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Nigeria

- 5.5.4.2.3 Egypt

- 5.5.4.2.4 Rest of Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Krones AG

- 6.4.2 Sidel Group (Tetra Laval)

- 6.4.3 KHS GmbH

- 6.4.4 SACMI Imola SC

- 6.4.5 Accutek Packaging Company, Inc.

- 6.4.6 ProMach Inc.

- 6.4.7 HERMA GmbH

- 6.4.8 Domino Printing Sciences PLC

- 6.4.9 Fuji Seal International

- 6.4.10 Avery Dennison Corporation

- 6.4.11 Weber Packaging Solutions

- 6.4.12 Markem-Imaje (Dover)

- 6.4.13 Videojet Technologies

- 6.4.14 P.E. Labellers S.p.A.

- 6.4.15 Nita Labeling Systems

- 6.4.16 Quadrel Labeling Systems

- 6.4.17 Pack Leader Machinery

- 6.4.18 World Pack Automation Systems

- 6.4.19 Arca Labeling & Marking

- 6.4.20 Bobst Group SA

- 6.4.21 Sato Holdings Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment