|

市场调查报告书

商品编码

1852159

二甲苯:市场占有率分析、产业趋势、统计数据、成长预测(2025-2030 年)Xylene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

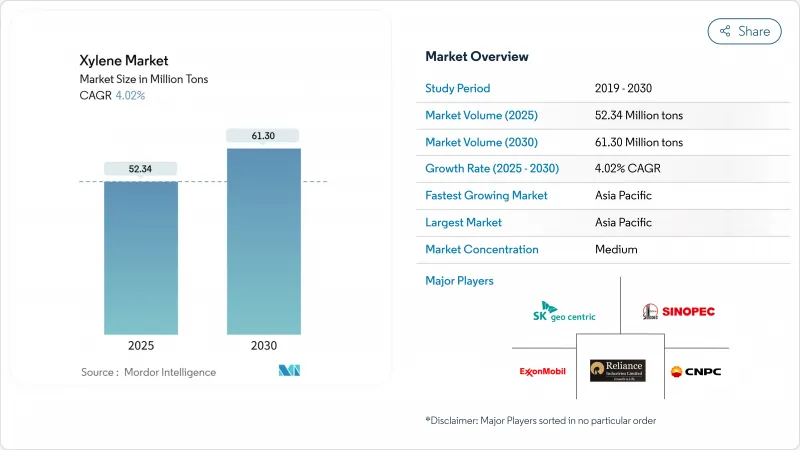

预计到 2025 年二甲苯市场规模将达到 5,234 万吨,到 2030 年将达到 6,130 万吨,年复合成长率为 4.02%。

对二甲苯在聚酯生产中的主导地位、亚洲和中东的大型芳烃一体化计划以及北美对工程塑胶日益增长的需求,是推动成长的主要因素。中国和印度的综合设施快速资本投资正在提升区域自给自足能力,而生物基化学品在日益增长的监管压力和品牌所有者压力下正获得初步发展势头。儘管利润前景受石脑油价格波动的影响,但拥有后向整合的製造商正在炼油、芳烃和衍生品产业链中获取价值。竞争优势正向那些能够兼顾原料灵活性、数位优化和可靠的脱碳蓝图的公司倾斜。

全球二甲苯市场趋势与洞察

亚洲PET树脂需求激增,推动对二甲苯消费。

大规模聚酯生产正在重塑原料流向。中国计划在2024年至2028年间大幅增加对二甲苯产能。此次扩产将确保对聚对苯二甲酸乙二醇酯(PTA)的供应,以满足快速增长的聚对苯二甲酸乙二醇酯(PET)薄膜和瓶子生产的需求。生产商正在进行垂直整合以控製成本和物流,同时,不断增长的石脑油进口正在填补亚洲的短缺。

中东和亚洲各地综合芳烃联合装置的产能扩张

沙特阿美公司的阿米拉尔综合体等计划将炼油与下游芳烃生产相结合,从而节省原料成本并提高对二甲苯的产率。共享公用设施、先进催化剂和即时优化降低了单位成本,增强了区域出口竞争力。这些大型专案正在改变供应格局,迫使老旧的独立装置进行合理化改造和升级。

欧洲和北美严格的VOC法规限制了芳香族溶剂的使用。

监管机构正在扩大挥发性有机化合物(VOC)的限制范围,涵盖消费品涂料、清洁剂和室内装饰产品。为了符合规定,生产商必须减少或重新配製产品中的化学成分,这限制了成熟经济体的成长。为了维持市场进入,生产商正在转向低芳烃或生物基混合物。

细分市场分析

由于对二甲苯在PTA和PET产业链中的关键作用,到2024年,对二甲苯将占据二甲苯市场90%的份额。强大的下游一体化使主要炼油商能够对冲利润波动并确保强劲的需求。邻二甲苯的市占率远小于对二甲苯,但其复合年增长率将达到4.09%,主要受邻邻苯二甲酐等柔性塑化剂需求的推动。间二甲苯主要面向小众涂料和特殊树脂领域,而混合二甲苯则可透过异构体分离提供多种供应选择。催化剂和异构化装置的进步使营运商能够根据价格讯号微调产量,从而在商品化产品组合中提高盈利。这种适应性将使对二甲苯即使在衍生性商品交易格局改变的情况下,也能维持其核心地位。

亚洲生产商持续推动二甲苯萃取装置的产能提升,以充分利用规模经济效益,满足不断增长的宝特瓶订单需求。北美供应商则着重生产用于薄膜应用的高附加价值产品,以满足低乙醛产量的需求。欧洲炼油商正逐步从混合溶剂转向氢化溶剂,以应对排放法规。到2030年,这一趋势将催生对各种异构体的特定需求。

到2024年,技术级二甲苯将占二甲苯市场的85%,因为被覆剂配方商、黏合剂配方商和工业清洁剂优先考虑成本、可得性和中等溶解度。从重整油和BTX池中提取的简单生产路线可提供充足的供应和具有竞争力的价格。新兴国家的大宗消费商在基础设施和製造业快速扩张时期吸收了这些产品,从而巩固了其核心地位。

相反,纯度高达99.9%的高纯度材料在半导体、製药和高性能树脂应用领域正以4.7%的复合年增长率成长。满足其严格的规格要求需要复杂的结晶、蒸馏和线上分析技术,这构成了较高的市场准入门槛和可观的净利率。拥有整合实验室服务和完善品质系统的生产商正利用这些专业管道,与大宗商品相比,获得更高的每吨息税折旧摊提前利润(EBITDA)。

区域分析

到2024年,亚太地区将占二甲苯市场55%的份额,并将在2030年前以每年4.51%的速度持续成长。预计到2028年,中国的对二甲苯产能将每年增加2500万吨,从而支持区域自给自足;而印度的PET生产线将满足强劲的饮料需求。东协主要国家正在进口混合二甲苯以弥补缺口,从而维持亚洲内部的贸易流动。日益激烈的竞争正在缩小价差,并促使下游企业结盟和签署优惠贸易协定。

北美市场保持稳定,儘管成长缓慢。页岩原料的经济效益为炼油厂带来了可观的苯、甲苯、甲苯(BTX)产率。轻量化汽车法规的实施提高了工程塑胶的使用量,儘管涂料行业对挥发性有机化合物(VOC)的监管十分严格,但工程塑胶衍生品的需求仍然强劲。监管政策的明朗化,加上成熟的物流体系,将促使企业加大产能瓶颈的消除,而非新建工厂。

在永续性指令的推动下,欧洲成熟的市场需求环境正在重塑:德国化工产业丛集正致力于提升生产效率,英国和法国正在建造循环溶剂回收装置,而欧盟范围内的REACH法规则推动了低芳烃混合物的再製造。在政策奖励的支持下,生物基试点计画力求在可再生芳烃领域抢占先机,其特色产品将瞄准高端涂料和电子产品市场。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- PET树脂需求激增推动二甲苯生产

- 中东和亚洲芳烃联合装置产能扩张

- 汽车轻量化推动北美工程塑胶市场发展

- 二甲苯使用量增加

- 製药公司在供应链中断的情况下策略性地囤积溶剂

- 市场限制

- 欧洲和北美严格的VOC法规限制了芳香族溶剂的使用。

- 健康毒性问题促使人们转向使用含氧溶剂

- 石脑油价格波动挤压生产商利润空间

- 价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 按类型

- 邻二甲苯

- 间二甲苯

- 对二甲苯

- 混合二甲苯

- 按年级

- 技术级

- 高纯度等级(99.9)

- 按来源

- 石油基二甲苯

- 生物基二甲苯

- 透过使用

- 溶剂

- 单体

- 其他用途

- 按最终用户行业划分

- 塑胶和聚合物

- 油漆和涂料

- 胶水

- 其他终端用户产业

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲国家

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Braskem

- Chevron Phillips Chemical Company LLC

- China Petrochemical Corporation

- CNPC

- ENEOS Corporation

- Exxon Mobil Corporation

- Formosa Chemicals & Fibre Corp

- FUJAN REFINING & PETROCHEMICAL COMPANY LIMITED

- GS Caltex Corporation

- Indian Oil Corporation Ltd

- INEOS AG

- LOTTE Chemical Corporation

- Mangalore Refinery and Petrochemicals limited

- MITSUBISHI GAS CHEMICAL COMPANY, INC.

- Mitsui Chemicals, Inc.

- Petro Rabigh

- PTT Global Chemical Public Company Limited

- QatarEnergy

- Reliance Industries Limited

- SK Geocentric Co., Ltd.

- S-OIL CORPORATION

- TotalEnergies

第七章 市场机会与未来展望

The xylene market size stands at 52.34 million tons in 2025 and is forecast to touch 61.3 million tons by 2030, advancing at a 4.02% CAGR.

Growth rests on para-xylene's dominant role in polyester production, large-scale integrated aromatics projects across Asia and the Middle East, and rising demand for engineering plastics in North America. Rapid equipment investments in Chinese and Indian complexes are lifting regional self-sufficiency, while bio-based chemistries gain early-stage momentum as regulatory and brand-owner pressures intensify. Margin outlook hinges on naphtha price volatility, yet backward-integrated producers capture value across refining, aromatics, and derivative chains. Competitive advantage is tilting toward firms that combine feedstock flexibility, digital optimization, and credible decarbonization roadmaps.

Global Xylene Market Trends and Insights

Surging PET Resin Demand Fueling Para-xylene Consumption in Asia

Massive polyester build-outs are realigning feedstock flows. China plans to massive para-xylene capacity between 2024-2028. The escalation secures PTA supply for rapidly growing PET film and bottle output. Producers are vertically integrating to manage cost and logistics exposure, while increasing naphtha imports backfill Asian shortfalls.

Capacity Expansions in Integrated Aromatics Complexes across Middle East and Asia

Projects such as Saudi Aramco's Amiral Complex couple refining with downstream aromatics to unlock feedstock savings and high para-xylene yields. Shared utilities, advanced catalysts, and real-time optimization cut unit costs and strengthen regional export competitiveness. These mega-sites are shifting supply balances and forcing older standalone plants to rationalize or upgrade.

Stringent VOC Norms Limiting Aromatic Solvent Use in Europe and North America

Regulators are extending VOC limits to consumer paints, cleaners, and indoor products. Compliance forces reformulators to cut xylene loadings or redesign entire chemistries, constraining growth in mature economies. Producers pivot toward low-aromatic or bio-based blends to retain market access.

Other drivers and restraints analyzed in the detailed report include:

- Automotive Lightweighting Driving Engineering Plastics in North America

- Growing Usage of Xylene as Solvents and Monomers

- Health-toxicity Concerns Prompting Shift to Oxygenated Solvents

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Para-xylene held 90% of xylene market share in 2024, anchored by its indispensable role in PTA and PET chains. Robust downstream integration lets leading refiners hedge margin swings and assure captive demand. Ortho-xylene, though much smaller, leads growth at 4.09% CAGR on the back of flexible plasticizer demand in phthalic anhydride. Meta-xylene addresses niche coatings and specialty resins, while mixed xylene offers supply optionality for isomer separation. Catalyst advances and isomerization units let operators fine-tune output to price signals, enhancing profitability within an otherwise commoditized slate. This adaptive capability sustains para-xylene's centrality even as derivative trade flows reorganize.

Producers continue debottlenecking para-xylene extraction units in Asia to exploit economies of scale and meet swelling PET bottle orders. North American suppliers emphasize value-added grades for film applications that demand low acetaldehyde formation. European refiners increasingly channel mixed streams toward hydrogenated solvents to comply with tightening emission rules, a trend set to carve out specialized demand niches for each isomer through 2030.

Technical grade captured 85% of the xylene market in 2024 as coatings formulators, adhesive blenders, and industrial cleaners prioritize cost, availability, and mid-range solvency. Its straightforward production route from reformate and BTX pools yields abundant supply and competitive pricing. Bulk consumers in emerging economies absorb this volume for infrastructure and manufacturing surge phases, reinforcing its central role.

Conversely, high-purity 99.9% material is growing at 4.7% CAGR on semiconductor, pharmaceutical, and high-performance resin applications. Meeting its exacting specifications demands advanced crystallization, distillation, and on-stream analytics, creating high entry barriers and attractive margins. Producers with integrated lab services and robust quality systems capitalize on this specialized lane, carving higher EBITDA per ton against commodity counterparts.

The Xylene Market Report Segments the Industry by Type (Ortho-Xylene, Meta-Xylene, and More), Grade (Technical Grade and High-Purity Grade (99. 9%)), Source (Petroleum-Based Xylene and Bio-Based Xylene), Application (Solvent, Monomer, and Other Applications), End-User Industry (Plastics and Polymers, Paints and Coatings, Adhesives, and Other End-User Industries), and Geography (Asia-Pacific, North America, and More).

Geography Analysis

Asia-Pacific controlled 55% of the xylene market in 2024 and is growing 4.51% yearly to 2030. Chinese para-xylene capacity expansions of 25 million tons/year through 2028 underpin regional self-sufficiency, while Indian PET lines supply booming beverage demand. Major ASEAN economies import mixed xylenes to backfill shortfalls, sustaining intra-Asian trade flows. Intensifying competition is compressing spreads, spurring alliances and downstream PTA linkages.

North America shows stable albeit lower growth. Shale-based feedstock economics give refiners advantaged BTX yields. Automotive lightweighting regulations elevate engineering plastic use, fortifying derivative demand despite stringent VOC curbs in paints. Regulatory clarity combined with established logistics encourage incremental debottlenecks rather than greenfield builds.

Europe's mature demand landscape is reshaping under sustainability mandates. Germany's chemical clusters refine high-efficiency processes, the United Kingdom and France deploy circular solvent recovery units, and EU-wide REACH classifications prompt reformulation into lower-aromatic blends. Bio-based pilots supported by policy incentives aim to cement early footholds in renewable aromatics, with niche grades targeting premium coating and electronics markets.

- Braskem

- Chevron Phillips Chemical Company LLC

- China Petrochemical Corporation

- CNPC

- ENEOS Corporation

- Exxon Mobil Corporation

- Formosa Chemicals & Fibre Corp

- FUJAN REFINING & PETROCHEMICAL COMPANY LIMITED

- GS Caltex Corporation

- Indian Oil Corporation Ltd

- INEOS AG

- LOTTE Chemical Corporation

- Mangalore Refinery and Petrochemicals limited

- MITSUBISHI GAS CHEMICAL COMPANY, INC.

- Mitsui Chemicals, Inc.

- Petro Rabigh

- PTT Global Chemical Public Company Limited

- QatarEnergy

- Reliance Industries Limited

- SK Geocentric Co., Ltd.

- S-OIL CORPORATION

- TotalEnergies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging PET Resin Demand Fueling Para-xylene Consumption in Asia

- 4.2.2 Capacity Expansions in Integrated Aromatics Complexes across Middle east and Asia

- 4.2.3 Automotive Lightweighting Driving Engineering Plastics in North America

- 4.2.4 Growing Usage of Xylene as Solvents and Monomers

- 4.2.5 Strategic Stockpiling of Solvents by Pharma amid Supply-chain Volatility

- 4.3 Market Restraints

- 4.3.1 Stringent VOC Norms Limiting Aromatic Solvent Use in Europe and North America

- 4.3.2 Health-toxicity Concerns Prompting Shift to Oxygenated Solvents

- 4.3.3 Volatile Naphtha Prices Compressing Producer Margins

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Ortho-xylene

- 5.1.2 Meta-xylene

- 5.1.3 Para-xylene

- 5.1.4 Mixed xylene

- 5.2 By Grade

- 5.2.1 Technical Grade

- 5.2.2 High-Purity Grade (99.9 %)

- 5.3 By Source

- 5.3.1 Petroleum-based Xylene

- 5.3.2 Bio-based Xylene

- 5.4 By Application

- 5.4.1 Solvents

- 5.4.2 Monomer

- 5.4.3 Other Applications

- 5.5 By End-user Industry

- 5.5.1 Plastics and Polymers

- 5.5.2 Paints and Coatings

- 5.5.3 Adhesives

- 5.5.4 Other End-user Industries

- 5.6 Geography

- 5.6.1 Asia-Pacific

- 5.6.1.1 China

- 5.6.1.2 India

- 5.6.1.3 Japan

- 5.6.1.4 South Korea

- 5.6.1.5 Rest of Asia-Pacific

- 5.6.2 North America

- 5.6.2.1 United States

- 5.6.2.2 Canada

- 5.6.2.3 Mexico

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 South Africa

- 5.6.5.3 Rest of Middle East and Africa

- 5.6.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Braskem

- 6.4.2 Chevron Phillips Chemical Company LLC

- 6.4.3 China Petrochemical Corporation

- 6.4.4 CNPC

- 6.4.5 ENEOS Corporation

- 6.4.6 Exxon Mobil Corporation

- 6.4.7 Formosa Chemicals & Fibre Corp

- 6.4.8 FUJAN REFINING & PETROCHEMICAL COMPANY LIMITED

- 6.4.9 GS Caltex Corporation

- 6.4.10 Indian Oil Corporation Ltd

- 6.4.11 INEOS AG

- 6.4.12 LOTTE Chemical Corporation

- 6.4.13 Mangalore Refinery and Petrochemicals limited

- 6.4.14 MITSUBISHI GAS CHEMICAL COMPANY, INC.

- 6.4.15 Mitsui Chemicals, Inc.

- 6.4.16 Petro Rabigh

- 6.4.17 PTT Global Chemical Public Company Limited

- 6.4.18 QatarEnergy

- 6.4.19 Reliance Industries Limited

- 6.4.20 SK Geocentric Co., Ltd.

- 6.4.21 S-OIL CORPORATION

- 6.4.22 TotalEnergies

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Bio-based Xylene Commercialization

日本混合二甲苯市场规模、份额、趋势和预测:按等级、最终用途和地区划分,2026-2034年

日本混合二甲苯市场规模、份额、趋势和预测:按等级、最终用途和地区划分,2026-2034年 2026年全球二甲苯市场报告

2026年全球二甲苯市场报告 二甲苯市场规模、份额和成长分析(按类型、等级、原料、应用、终端用户产业和地区划分)-2026-2033年产业预测

二甲苯市场规模、份额和成长分析(按类型、等级、原料、应用、终端用户产业和地区划分)-2026-2033年产业预测 二甲苯市场规模、占有率、成长、全球产业分析:按类型、应用和地区划分的洞察,预测(2026-2034 年)

二甲苯市场规模、占有率、成长、全球产业分析:按类型、应用和地区划分的洞察,预测(2026-2034 年) 混合二甲苯市场规模、份额及成长分析(依等级、应用、最终用途及地区划分)-2026-2033年产业预测

混合二甲苯市场规模、份额及成长分析(依等级、应用、最终用途及地区划分)-2026-2033年产业预测 二甲苯市场按应用、产品类型和最终用途行业划分-2025-2032年全球预测

二甲苯市场按应用、产品类型和最终用途行业划分-2025-2032年全球预测 全球二甲苯市场:2032 年预测-按类型、配方、应用、最终用户和地区进行分析

全球二甲苯市场:2032 年预测-按类型、配方、应用、最终用户和地区进行分析 混合二甲苯市场报告:趋势、预测和竞争分析(至 2031 年)2025 年至 2033 年邻二甲苯市场报告(按应用、最终用途和地区)

混合二甲苯市场报告:趋势、预测和竞争分析(至 2031 年)2025 年至 2033 年邻二甲苯市场报告(按应用、最终用途和地区) 2025 - 2034 年混合二甲苯市场机会、成长动力、产业趋势分析与预测

2025 - 2034 年混合二甲苯市场机会、成长动力、产业趋势分析与预测