|

市场调查报告书

商品编码

1906022

药品包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Pharmaceutical Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

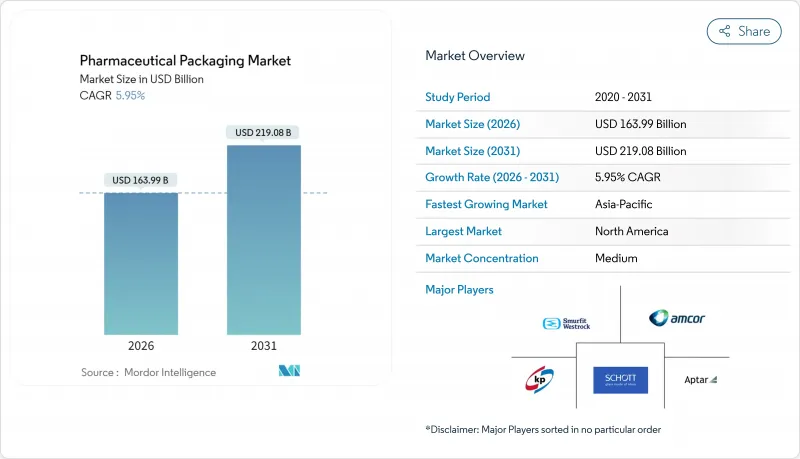

预计药品包装市场将从 2025 年的 1,547.8 亿美元成长到 2026 年的 1,639.9 亿美元,到 2031 年将达到 2,190.8 亿美元,2026 年至 2031 年的复合年增长率为 5.95%。

未来五年,生物製药需求的成长、全球可追溯性法规的加强以及永续性推进,预计将继续推动对新型灌装和包装生产线、阻隔性材料以及循环设计领域的资本投资。随着基因和细胞疗法达到商业规模,对能够容纳小规模个人化治疗药物的柔性包装产能的需求预计将会成长。由于《药品分销和安全法案》(DSCSA) 推动了药品序列化,北美仍将保持其最大的区域贡献;而亚太地区将呈现8.96%的高复合年增长率,这反映出该地区国内药品产量的增加和医疗保健覆盖范围的扩大。材料策略正在改变:儘管塑胶仍占据主导地位,但在欧盟和美国即将出台的PFAS法规的背景下,生物基聚合物、无铝泡壳和消费后回收薄膜正迅速从试点阶段过渡到大规模生产。同时,聚乙烯、聚丙烯和PET价格的波动正在收紧利润空间,促使大型加工商签订长期供应合约并进行垂直整合。

全球医药包装市场趋势及展望

人口老化和慢性病流行

随着平均年龄的增长,长期照护需求也随之增加,这支撑了对日历式泡壳包装、大写字母标籤和单手开启管瓶等产品的稳定需求,这些产品有助于提高行动不便患者的用药依从性。德国2024年疫苗接种计画的调整(肺炎链球菌疫苗接种量增加23%,B群脑膜炎双球菌疫苗接种量增加52%)显示老年人对预防性照护的接受度较高。包装供应商正在积极回应,推出包含开启记录并将依从性资料传输给医疗团队的智慧包装。随着支付方将报销与实际治疗效果挂钩,智慧封口和支援NFC功能的纸盒预计将加速成长。

不断扩大的生物製药和注射产品线

预填充式注射器是新型生物製剂的核心,因为它们简化了患者自行给药流程,最大限度地降低了污染风险,并减少了填充和表面处理工程中的废弃物。 BD 的 iDFill 注射器整合了 RFID 技术,可即时检验;Neopak XtraFlow 设计则可容纳以前只能使用管瓶的高黏度製剂。修订后的 GMP 附录 1 正在加速市场对即用型玻璃管和聚合物容器的需求,这些产品无需清洗和冷却过程,使 CDMO 能够在不新建无尘室的情况下扩大产能。

石油衍生树脂的价格波动

供应中断和不可抗力事件导致PET价格在2024年6月上涨1.1%,进一步挤压了加工业者本已微薄的利润空间。医药契约製造材料规格限制了快速更换等级,迫使许多加工商要么自行承担成本飙升,要么重新谈判长期合约。瓦楞纸箱生产商也面临纤维成本上涨的困境,预计2025年1月起每吨将上涨70美元。

细分市场分析

2025年,塑胶在医药包装市场仍占45.05%的份额,主要得益于高密度聚乙烯(HDPE)瓶、聚丙烯(PP)瓶盖和聚对苯二甲酸乙二醇酯(PET)泡壳,这些产品在成本和阻隔性实现了良好的平衡。然而,随着品牌所有者追求循环经济目标,该领域的成长速度正在放缓。在塑胶产业内部,由于具有优异抗破损性能的环烯烃基材料的出现,用于PP注射器的医药包装市场正在稳步扩张。玻璃仍然是光敏性和湿敏性生物製药包装的必备材料。儘管重量较大且易碎,但优质硼硅酸管瓶在细胞毒性填充剂市场中占据主导地位。金属在气雾剂和植入式医疗设备则扮演独特的角色。

人们对生物基树脂、再生PET阻隔性膜和纸质药瓶(例如,阿勒格尼健康网络的TallyTube试点计画)的兴趣日益浓厚。儘管开发商在产品上市前会仔细考虑保质期保证、萃取物成分和生产线转换成本,但早期采用者往往能够从将永续性评估纳入供应商审核的医院中赢得采购竞标。

区域分析

到2025年,北美将占据全球药品包装市场35.01%的份额,这主要得益于生物製药领域的巨额投资以及《药品供应链安全法案》(DSCSA)先进的序列化要求。预计到2025年,光是美国製造商就将投资1,600亿美元用于新建灌装和原料药生产工厂,这将推动可灭菌聚合物、即用型玻璃容器和高容量低温运输运输容器的需求。该地区还在试点应用人工智慧视觉系统,以生产线速度扫描小于100微米的颗粒,有助于降低召回风险并增强品牌可靠性。

欧洲正努力在雄心勃勃的永续性法规与能源成本压力之间寻求平衡。随着即将实施的《包装和包装废弃物法规》(该法规要求在2030年回收所有形式的包装),人们对单一材料泡壳包装和纸质药瓶的兴趣日益浓厚。儘管德国2024年的药品产量下降了1.5%,但开发平臺仍丰富,其中包括需要超低温包装的mRNA和基因疗法。将于2026年生效的PFAS法规将要求对材料进行重新认证,这将为无氟阻隔膜供应商带来先发优势。

亚太地区将达到最高成长率,到2031年复合年增长率将达到8.73%。这一增长主要得益于中国和印度合约研发生产机构(CDMO)的扩张以及公共医疗保险覆盖范围的扩大。当地监管机构正努力使无菌标准与人用药品註册技术要求国际协调会议(ICH)和人用药品註册技术要求国际协调理事会(PIC/S)的标准接轨,并推动包装厂实施ISO 5级阻隔性能和全线序列化。然而,该地区也面临地缘政治的挑战。中国修订后的反间谍法使追踪系统技术的转移变得更加复杂,跨国公司正在将其采购来源多元化,转向东协市场。以精密模塑技术着称的日本加工商正在赢得COP注射器的出口订单,因为全球品牌正在减少对单一国家的依赖。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 人口老化和慢性病流行

- 不断拓展的生物製药和注射产品线

- 永续性材料替代

- 强制性数位可追溯性(例如,DSCSA、欧盟FMD)

- 人工智慧驱动的自适应填充和收尾线

- 增加居家/分散式检测,需邮寄包裹

- 市场限制

- 石油衍生树脂的价格波动

- 资本密集的无菌和验证要求

- 欧盟和美国对 PFAS/氟聚合物的监管问题

- 产业供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 材料

- 塑胶

- HDPE

- 低密度聚乙烯和线性低密度聚乙烯

- PET

- 其他塑胶製品

- 玻璃

- I型硼硼硅酸玻璃

- II 型处理钠石灰

- III型钠石灰

- 金属

- 纸和纸板

- 生物聚合物和其他材料

- 塑胶

- 按包装级别

- 初级包装

- 瓶子

- 预填充式注射器

- 管瓶和安瓿

- 泡壳包装

- 二级包装

- 纸箱和纸套

- 标籤和插页

- 三级包装

- 纸板运输容器

- 托盘和防护系统

- 初级包装

- 依产品类型

- 瓶子

- 预填充式注射器

- 管瓶和安瓿

- 泡壳包装

- 瓶盖和封口

- 管状和袋状

- 其他产品类型

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 中东和非洲

- 中东

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 埃及

- 其他非洲地区

- 中东

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Amcor plc

- Gerresheimer AG

- Schott AG

- West Pharmaceutical Services Inc.

- AptarGroup Inc.

- Smurfit WestRock

- Becton, Dickinson & Company

- Catalent Inc.

- CCL Industries Inc.

- Klockner Pentaplast Group

- Nipro Corporation

- Vetter Pharma International GmbH

- McKesson Corporation

- FlexiTuff International Ltd.

- WL Gore & Associates Inc.

- Stevanato Group

- Corning Incorporated

- Owen-Illinois Inc.

- SGD Pharma

第七章 市场机会与未来展望

The pharmaceutical packaging market is expected to grow from USD 154.78 billion in 2025 to USD 163.99 billion in 2026 and is forecast to reach USD 219.08 billion by 2031 at 5.95% CAGR over 2026-2031.

Over the next five years, the increasing demand for biologics, stricter global traceability regulations, and widespread sustainability targets will continue to drive capital investment in new fill-finish lines, high-barrier materials, and circular-ready designs. Demand for flexible pack volumes that match smaller, personalized therapy batches is expected to expand as gene and cell therapies reach commercial scale. North America remains the largest regional contributor, supported by DSCSA-driven serialization, while the Asia-Pacific's sizable 8.96% CAGR reflects rising domestic drug production and broadening health coverage.Material strategies are in flux: plastics still dominate, yet bio-based polymers, aluminum-free blisters, and post-consumer-recycled films are quickly transitioning from pilot to production as EU and US PFAS curbs near enforcement. Meanwhile, price swings in polyethylene, polypropylene, and PET keep margins tight, encouraging longer supplier contracts and vertical integration by larger converters.

Global Pharmaceutical Packaging Market Trends and Insights

Aging population and chronic disease prevalence

Rising median ages drive up long-term therapy volumes, underpinning consistent demand for calendar blisters, large-print labels, and one-hand-open vials that aid adherence among patients with reduced dexterity. Germany's 2024 vaccination shifts, with pneumococcal doses up 23% and meningococcal B up 52%, illustrate broader preventive care uptake among seniors. Packaging suppliers respond with connected packs that log opening events and forward adherence data to care teams. Growth in smart closures and NFC-enabled cartons is expected to intensify as payers link reimbursement to real-world outcomes.

Biologics and injectable pipeline expansion

Prefilled syringes sit at the core of new biologic launches because they simplify self-administration, minimize contamination risks, and reduce waste during the fill-finish process. BD's iDFill syringe embeds RFID for instant verification, while its Neopak XtraFlow design handles viscous formulations that were once vial-only. GMP Annex 1 revisions are accelerating demand for ready-to-use glass tubing and polymer containers that bypass washing and depyrogenation steps, helping CDMOs scale capacity without the need to construct new cleanrooms.

Petro-derivative resin price volatility

Supply disruptions and force majeure events led to a 1.1% increase in PET prices in June 2024, further tightening already narrow converter margins. Pharmaceutical contract material specs restrict rapid grade switches, forcing many converters to absorb cost spikes or renegotiate long contracts. Corrugated shippers also face higher fibre costs, with a USD 70 per-ton increase announced for January 2025.

Other drivers and restraints analyzed in the detailed report include:

- Sustainability-driven material substitution

- Digital traceability mandates (DSCSA, EU-FMD)

- Capital-intensive sterility and validation requirements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastics retained 45.05% of the pharmaceutical packaging market share in 2025, primarily driven by HDPE bottles, PP closures, and PET blisters that strike a balance between cost and barrier needs. Yet the segment's growth moderates as brand owners court circularity objectives. Within the plastics industry, the pharmaceutical packaging market size for PP-based syringes is rising steadily, thanks to break-resistant cyclic olefin options. Glass remains indispensable for light- and moisture-sensitive biologics; Type I borosilicate vials dominate cytotoxic fills, despite their higher weight and shatter risk. Metals play a niche role in aerosol and implantable devices.

Momentum is gathering around bio-attributed resins, recycled PET mid-barrier webs, and paper-based pill bottles, such as Allegheny Health Network's Tully Tube pilot. Developers weigh shelf-life assurance, extractables profiles, and line changeover costs before a wide release, yet early adopters often win procurement tenders from hospitals, incorporating sustainability scoring into vendor audits.

The Pharmaceutical Packaging Market Report is Segmented by Material (Plastics, Glass, Metal, and More), Packaging Level (Primary Packaging, Secondary Packaging, and More), Product Type (Bottles, Prefilled Syringes, Vials and Ampoules, Blister Packs, Caps and Closures, and More), and Geography (North America, South America, Europe, Asia Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 35.01% of the pharmaceutical packaging market share in 2025, driven by significant investments in biologics and advanced DSCSA serialization mandates. U.S. manufacturers alone are investing USD 160 billion in new fill-finish and API plants through 2025, a trend that drives demand for sterilizable polymers, ready-to-use glass, and high-capacity cold-chain shippers. The region also pilots AI vision systems that scan for sub-100 µm particulates at line speed, lowering recall risk and strengthening brand trust.

Europe balances ambitious sustainability regulations with energy cost pressures. The forthcoming Packaging and Packaging Waste Regulation requires every format to be recyclable by 2030, escalating interest in monomaterial blisters and paper-based pill bottles. Germany's pharmaceutical output slipped 1.5% in 2024, yet its R&D pipelines remain rich in mRNA and gene therapies that require ultra-low-temperature packaging. PFAS restrictions, effective in 2026, force material requalification, offering an early-mover advantage to suppliers with fluorine-free barrier films.

The Asia-Pacific region grows at the fastest rate of 8.73% CAGR through 2031, driven by the expanding CDMO footprints of China and India, as well as the widening of public health coverage. Local regulators align sterility rules with ICH and PIC/S guides, pushing packaging plants to adopt ISO 5 barriers and full-line serialization. Yet the region faces geopolitical headwinds; China's updated Anti-Espionage Law complicates technology transfer for track-and-trace systems, prompting multinationals to diversify sourcing across ASEAN markets. Japanese converters, renowned for their precision molding, secure export orders for COP syringes as global brands hedge against dependence on a single country.

- Amcor plc

- Gerresheimer AG

- Schott AG

- West Pharmaceutical Services Inc.

- AptarGroup Inc.

- Smurfit WestRock

- Becton, Dickinson & Company

- Catalent Inc.

- CCL Industries Inc.

- Klockner Pentaplast Group

- Nipro Corporation

- Vetter Pharma International GmbH

- McKesson Corporation

- FlexiTuff International Ltd.

- W. L. Gore & Associates Inc.

- Stevanato Group

- Corning Incorporated

- Owen-Illinois Inc.

- SGD Pharma

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ageing population and chronic disease prevalence

- 4.2.2 Biologics and injectable pipeline expansion

- 4.2.3 Sustainability-driven material substitution

- 4.2.4 Digital traceability mandates (e.g., DSCSA, EU-FMD)

- 4.2.5 AI-enabled adaptive fill-finish lines

- 4.2.6 Rise of at-home/decentralised trials needing mail-ready packs

- 4.3 Market Restraints

- 4.3.1 Petro-derivative resin price volatility

- 4.3.2 Capital-intensive sterility and validation requirements

- 4.3.3 Looming PFAS/fluoropolymer restrictions in EU and US

- 4.4 Industry Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Plastics

- 5.1.1.1 HDPE

- 5.1.1.2 LDPE and LLDPE

- 5.1.1.3 PET

- 5.1.1.4 Other Plastics

- 5.1.2 Glass

- 5.1.2.1 Type I Borosilicate

- 5.1.2.2 Type II Treated Soda-lime

- 5.1.2.3 Type III Soda-lime

- 5.1.3 Metal

- 5.1.4 Paper and Paperboard

- 5.1.5 Biopolymers and Other Materials

- 5.1.1 Plastics

- 5.2 By Packaging Level

- 5.2.1 Primary Packaging

- 5.2.1.1 Bottles

- 5.2.1.2 Prefilled Syringes

- 5.2.1.3 Vials and Ampoules

- 5.2.1.4 Blister Packs

- 5.2.2 Secondary Packaging

- 5.2.2.1 Cartons and Sleeves

- 5.2.2.2 Labels and Inserts

- 5.2.3 Tertiary Packaging

- 5.2.3.1 Corrugated Shippers

- 5.2.3.2 Pallets and Protective Systems

- 5.2.1 Primary Packaging

- 5.3 By Product Type

- 5.3.1 Bottles

- 5.3.2 Prefilled Syringes

- 5.3.3 Vials and Ampoules

- 5.3.4 Blister Packs

- 5.3.5 Caps and Closures

- 5.3.6 Tubes and Pouches

- 5.3.7 Other Product Types

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 Middle East

- 5.4.4.1.1 United Arab Emirates

- 5.4.4.1.2 Saudi Arabia

- 5.4.4.1.3 Turkey

- 5.4.4.1.4 Rest of Middle East

- 5.4.4.2 Africa

- 5.4.4.2.1 South Africa

- 5.4.4.2.2 Nigeria

- 5.4.4.2.3 Egypt

- 5.4.4.2.4 Rest of Africa

- 5.4.4.1 Middle East

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 Gerresheimer AG

- 6.4.3 Schott AG

- 6.4.4 West Pharmaceutical Services Inc.

- 6.4.5 AptarGroup Inc.

- 6.4.6 Smurfit WestRock

- 6.4.7 Becton, Dickinson & Company

- 6.4.8 Catalent Inc.

- 6.4.9 CCL Industries Inc.

- 6.4.10 Klockner Pentaplast Group

- 6.4.11 Nipro Corporation

- 6.4.12 Vetter Pharma International GmbH

- 6.4.13 McKesson Corporation

- 6.4.14 FlexiTuff International Ltd.

- 6.4.15 W. L. Gore & Associates Inc.

- 6.4.16 Stevanato Group

- 6.4.17 Corning Incorporated

- 6.4.18 Owen-Illinois Inc.

- 6.4.19 SGD Pharma

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

2026年全球药品单剂量包装市场报告

2026年全球药品单剂量包装市场报告 医药包装市场分析及预测(至2035年):依类型、产品类型、材质、技术、应用、组件、最终用户、功能、製程及解决方案划分容器密封完整性测试市场分析及预测(至2035年):类型、产品、服务、技术、应用、材质类型、设备、製程、最终用户、设施

医药包装市场分析及预测(至2035年):依类型、产品类型、材质、技术、应用、组件、最终用户、功能、製程及解决方案划分容器密封完整性测试市场分析及预测(至2035年):类型、产品、服务、技术、应用、材质类型、设备、製程、最终用户、设施 亚太地区医药包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

亚太地区医药包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 全球疫苗包装市场规模、份额、趋势和成长分析报告(2026-2034年)

全球疫苗包装市场规模、份额、趋势和成长分析报告(2026-2034年) 日本生物製药包装市场规模、份额、趋势及预测(依材料、包装类型、应用及地区划分),2026-2034年2026年全球微型离心管盒市场报告2026年全球益生菌包装市场报告2026年全球药品包装检测设备市场报告2026年全球药局包装机械市场报告

日本生物製药包装市场规模、份额、趋势及预测(依材料、包装类型、应用及地区划分),2026-2034年2026年全球微型离心管盒市场报告2026年全球益生菌包装市场报告2026年全球药品包装检测设备市场报告2026年全球药局包装机械市场报告