|

市场调查报告书

商品编码

1906262

欧洲硬质塑胶包装市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)Europe Rigid Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

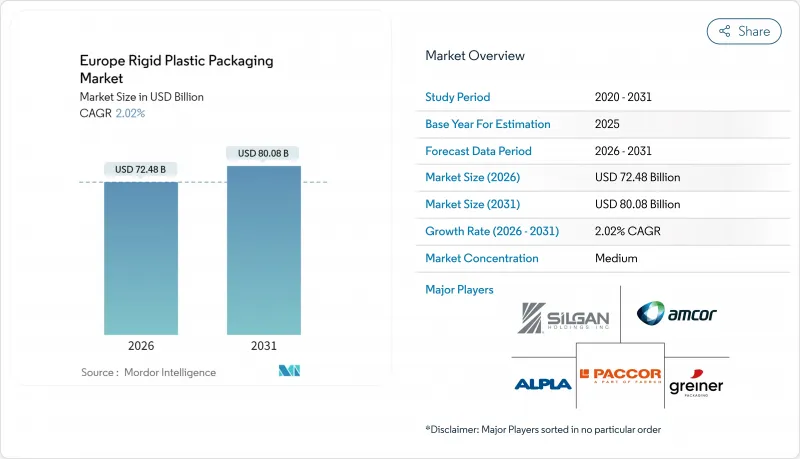

欧洲硬质塑胶包装市场预计将从 2025 年的 710.4 亿美元成长到 2026 年的 724.8 亿美元,预计到 2031 年将达到 800.8 亿美元,2026 年至 2031 年的复合年增长率为 2.02%。

更严格的回收目标、最低再生材料含量标准和材料税正在重塑设计选择、筹资策略和资本配置。押金返还计画 (DRS) 正在推动对再生 PET 的需求成长,而能源价格波动和原材料成本上涨则加速了营运效率提升计画的实施。大规模加工商正在合併以共用合规资源,而早期投资于闭合迴路基础设施的生产商正在与饮料、食品和医疗保健品牌所有者建立商业性优势。来自纤维基替代品的材料替代压力加剧了竞争,但在阻隔性、可回收性和抗衝击性要求高于轻量化奖励的领域,硬质塑胶仍然占据主导地位。

欧洲硬质塑胶包装市场趋势与洞察

饮料业对可再生硬质宝特瓶的需求激增

在德国,押金返还制度的回收率已超过90%,促使欧盟其他地区也纷纷效仿,并提振了对食品级再生PET(rPET)的需求。葡萄牙的一个试点计画验证了该制度的技术可行性,仅使用一台反向自动贩卖机,每天即可回收1281个容器。在回收的容器中,透明蓝色PET占绝大多数,凸显了颜色标准化对于提高分类效率的重要性。欧盟规定,到2025年宝特瓶再生材料含量必须达到25%,到2030年达到30%,儘管欧洲拥有300万吨的清洗能力和140万吨的造粒能力,但仍导致再生原料供不应求。这促使品牌商签订双边承购协议,并推动清洗线和挤出反应器的改造。因此, 宝特瓶仍然是成长最快的硬包装形式,支撑着未来塑胶回收投资计画的一半以上。

快速成长的电子商务推动了防护性硬质包装的发展

到2024年,线上销售额将占欧洲零售总额的22%以上,这将推动对能够承受多站履约链衝击的抗衝击包装的需求。为了降低小包裹在自动化分类中心的破损率和保固索赔,零售商正在采用硬质桶、硬桶和可堆迭式包装。如果减少产品破损带来的效益大于增加重量所带来的损失,零售商愿意接受材料重量的少量增加。预计到2030年,人均包装废弃物将达到209公斤,监管机构要求提供包装尺寸合理性的证据。然而,防护性强、坚固耐用的包装解决方案因其能够预防产品全生命週期的损坏而备受青睐,这为致力于打造电商适用包装设计的加工商带来了持续的短期需求增长。

一次性塑胶税和生产者延伸责任制

将于2025年生效的环境调整附加税将对可回收性有限的硬质包装征收,这将增加传统包装设计的遵循成本。例如,义大利对聚苯乙烯托盘征收每吨800欧元(866美元)的税,法国对单一材料PET征收每吨456附加税(494美元)的税,附加税将促使包装转型和产品种类精简。大型加工商可以透过规模经济来分担成本,而小规模模塑商则面临利润率下降甚至退出市场的风险,这将加速产业整合。

细分市场分析

到2025年,瓶罐包装将占欧洲硬质塑胶包装市场307.1亿美元,占43.22%,预计到2031年将维持最快成长速度,年复合成长率达2.74%。这一成长动能主要得益于饮料业对符合DRS标准的PET容器的依赖,以及製药业对可消毒HDPE片容器的需求。冷藏食品配送对托盘和容器的需求保持稳定,但PFAS禁令正在推动阻隔涂层技术的创新。盖子与封口装置正朝着固定式设计发展,到2024年7月,所有一次性饮料包装都必须采用这种设计,这将促使封口供应商更新模具。

中型散货箱和桶在化学品物流领域占据稳固的地位。然而,电子商务小包裹的密度尚未达到足以柔软性软包装被广泛替代的程度。托盘和其他硬质配件的需求持续增长,这主要得益于回收站运营商对高密度聚苯乙烯)托盘的回收利用。因此,目前产品组合仍以瓶装为主,预计PET和HDPE将继续主导欧洲硬质塑胶包装市场的树脂消费量。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 饮料业对可再生硬质宝特瓶的需求激增

- 快速成长的电子商务推动了硬质防护包装形式的发展

- 透过扩大欧盟押金退款计画来加速收款基础设施建设

- 可重复填充和再利用商店试点计画推动高密度聚乙烯瓶重新设计

- 欧洲生质塑胶产能迅速扩张

- 由于医药低温运输的扩展,对阻隔性硬质包装材料的需求增加。

- 市场限制

- 一次性塑胶税和生产者延伸责任制(EPR)成本

- 转向使用纸张和柔性替代品以减轻重量

- 再生PET(rPET)和再生高密度聚苯乙烯(rHDPE)价格的波动给加工商的利润率带来了压力。

- 能源价格飙升推高了挤出和射出成型的成本。

- 产业供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依产品类型

- 瓶子和罐子

- 托盘和容器

- 瓶盖和封口

- 中型散货箱(IBC)

- 鼓

- 调色盘

- 其他产品类型

- 材料

- 聚乙烯(PE)

- 聚对苯二甲酸乙二醇酯(PET)

- 聚丙烯(PP)

- 聚苯乙烯(PS)和发泡聚苯乙烯(EPS)

- 聚氯乙烯(PVC)

- 其他硬质塑胶材料

- 按最终用户行业划分

- 食物

- 饮料

- 卫生保健

- 化妆品和个人护理

- 工业的

- 建筑/施工

- 车

- 其他终端用户产业

- 按国家/地区

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 波兰

- 荷兰

- 其他欧洲地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Alpla Werke Alwin Lehner GmbH & Co KG

- Mauser Packaging Solutions Holding Company

- Amcor plc

- Greiner Packaging International GmbH

- Greif, Inc.

- PACCOR Packaging GmbH(Faerch Group)

- Plastipak Holdings, Inc.

- Schoeller Allibert Services BV

- Silgan Holdings Inc.

- Albea Group

- Coda Plastics Ltd.

- Frapak Packaging BV

- Schutz GmbH & Co. KGaA

- WERIT Kunststoffwerke W. Schneider GmbH & Co. KG

- ACTI PACK SAS

- RETAL Industries Ltd.

- RIKUTEC Group

- AST Kunststoffverarbeitung GmbH

- Robinson plc

- Esterform Packaging Ltd.

第七章 市场机会与未来展望

The Europe rigid plastic packaging market is expected to grow from USD 71.04 billion in 2025 to USD 72.48 billion in 2026 and is forecast to reach USD 80.08 billion by 2031 at 2.02% CAGR over 2026-2031.

Stricter collection targets, minimum recycled-content thresholds, and material taxes are reshaping design choices, procurement strategies, and capital allocation. Deposit-return schemes (DRS) underpin rising recycled PET demand, while energy-price volatility and feedstock inflation accelerate operational efficiency programs. Large converters pursue mergers to pool compliance resources, and producers that invest early in closed-loop infrastructure secure commercial advantages with beverage, food, and healthcare brand owners. Material substitution pressures from fiber-based alternatives intensify competition, yet rigid formats retain defensible positions wherever high barrier, reusability, or impact resistance requirements outweigh lightweighting incentives.

Europe Rigid Plastic Packaging Market Trends and Insights

Surging Demand for Recyclable Rigid PET Bottles in Beverages

Deposit-return schemes already deliver collection rates above 90% in Germany and inspire similar adoption across the bloc, lifting demand for food-grade rPET feedstock. Portugal's pilot proved technical viability with 1,281 packages captured per reverse-vending unit daily, and transparent blue PET accounted for most returns, underlining the power of color standardization to streamline sorting. The EU obligation for 25% recycled content in PET bottles by 2025 and 30% by 2030 creates an undersupplied secondary-material pool despite Europe's 3 million-tonne washing and 1.4 million-tonne pellet capacity. Brand owners therefore lock in bilateral offtake agreements, stimulating retrofits of washing lines and extrusion reactors. As a result, PET bottles remain the fastest-growing rigid format and anchor more than half of the upcoming resin recycling investments.

Booming E-commerce Boosting Protective Rigid Formats

Online retail penetration exceeded 22% of total European goods sales in 2024, heightening the need for impact-resistant containers that survive multi-node fulfillment chains. Rigid drums, pails, and stackable tubs reduce breakage rates and warranty claims as parcels transit automated sorting hubs, and retailers accept marginal material increases when product-damage savings offset weight penalties. With packaging waste generation projected at 209 kg per capita by 2030, regulators now demand right-sizing evidence; nonetheless, protective rigid solutions often score favorably on life-cycle damage avoidance, sustaining a near-term boost for converters targeting e-commerce-ready designs.

Single-Use Plastic Taxes and Extended Producer Responsibility Fees

Eco-modulated fees, effective from 2025, penalize rigid packs with limited recyclability, inflating compliance outlays for legacy designs. Differential levies-EUR 800/ton (USD 866/ton) on polystyrene trays in Italy versus EUR 456/ton (USD 494/ton) on mono-material PET in France, drive format migration and prompt SKU rationalization. Large converters absorb charges via scale efficiencies, but small molders risk margin erosion or exit, accelerating sector consolidation.

Other drivers and restraints analyzed in the detailed report include:

- Growth of EU Deposit-Return Schemes Accelerating Collection Infrastructure

- Rapid Scale-up of European Bioplastics Capacity

- Shift Toward Paper and Flexible Substitutes for Lightweighting

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bottles and jars contributed USD 30.71 billion, equal to 43.22% of Europe's rigid plastic packaging market size in 2025, and will keep expanding fastest at a 2.74% CAGR to 2031. This momentum stems from beverage-sector reliance on DRS-compatible PET formats and pharma demand for sterilizable HDPE pill containers. Tray and container demand hold steady in chilled-food distribution, yet PFAS bans compel barrier-coating innovation. Caps and closures evolve toward tethered designs, mandated on all single-use beverage packs by July 2024, spurring tooling upgrades across closure suppliers.

Intermediate bulk containers and drums carved a resilient niche in chemical logistics; however, e-commerce parcel density has yet to justify the broad replacement of flexible liners. Pallets and other rigid accessories maintain incremental growth, driven by circular pool operators that refurbish high-density polyethylene decks. The product mix thus remains weighted toward bottles, ensuring that PET and HDPE dominate resin off-take in the European rigid plastic packaging market.

The Europe Rigid Plastic Packaging Market Report is Segmented by Product Type (Bottles and Jars, Trays and Containers, Caps and Closures, Intermediate Bulk Containers, and More), Material (Polyethylene (PE), Polyethylene Terephthalate (PET), Polypropylene (PP), and More), End-User Industry (Food, Beverage, Healthcare, Cosmetics and Personal Care, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Alpla Werke Alwin Lehner GmbH & Co KG

- Mauser Packaging Solutions Holding Company

- Amcor plc

- Greiner Packaging International GmbH

- Greif, Inc.

- PACCOR Packaging GmbH (Faerch Group)

- Plastipak Holdings, Inc.

- Schoeller Allibert Services B.V.

- Silgan Holdings Inc.

- Albea Group

- Coda Plastics Ltd.

- Frapak Packaging B.V.

- Schutz GmbH & Co. KGaA

- WERIT Kunststoffwerke W. Schneider GmbH & Co. KG

- ACTI PACK S.A.S.

- RETAL Industries Ltd.

- RIKUTEC Group

- AST Kunststoffverarbeitung GmbH

- Robinson plc

- Esterform Packaging Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for recyclable rigid PET bottles in beverages

- 4.2.2 Booming e-commerce boosting protective rigid formats

- 4.2.3 Growth of EU deposit-return schemes accelerating collection infrastructure

- 4.2.4 Refill-and-reuse store pilots driving HDPE bottle redesigns

- 4.2.5 Rapid scale-up of European bioplastics capacity

- 4.2.6 Pharma cold-chain expansion needing high-barrier rigid packs

- 4.3 Market Restraints

- 4.3.1 Single-use-plastic taxes and Extended Producer Responsibility fees

- 4.3.2 Shift toward paper and flexible substitutes for lightweighting

- 4.3.3 Volatile rPET and rHDPE prices squeezing converter margins

- 4.3.4 Energy-price shocks raising extrusion and injection costs

- 4.4 Industry Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Bottles and Jars

- 5.1.2 Trays and Containers

- 5.1.3 Caps and Closures

- 5.1.4 Intermediate Bulk Containers (IBCs)

- 5.1.5 Drums

- 5.1.6 Pallets

- 5.1.7 Other Product Types

- 5.2 By Material

- 5.2.1 Polyethylene (PE)

- 5.2.2 Polyethylene Terephthalate (PET)

- 5.2.3 Polypropylene (PP)

- 5.2.4 Polystyrene (PS) and Expanded PS (EPS)

- 5.2.5 Polyvinyl Chloride (PVC)

- 5.2.6 Other Rigid Plastic Materials

- 5.3 By End-user Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Healthcare

- 5.3.4 Cosmetics and Personal Care

- 5.3.5 Industrial

- 5.3.6 Building and Construction

- 5.3.7 Automotive

- 5.3.8 Other End-user Industries

- 5.4 By Country

- 5.4.1 United Kingdom

- 5.4.2 Germany

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Poland

- 5.4.7 Netherlands

- 5.4.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Alpla Werke Alwin Lehner GmbH & Co KG

- 6.4.2 Mauser Packaging Solutions Holding Company

- 6.4.3 Amcor plc

- 6.4.4 Greiner Packaging International GmbH

- 6.4.5 Greif, Inc.

- 6.4.6 PACCOR Packaging GmbH (Faerch Group)

- 6.4.7 Plastipak Holdings, Inc.

- 6.4.8 Schoeller Allibert Services B.V.

- 6.4.9 Silgan Holdings Inc.

- 6.4.10 Albea Group

- 6.4.11 Coda Plastics Ltd.

- 6.4.12 Frapak Packaging B.V.

- 6.4.13 Schutz GmbH & Co. KGaA

- 6.4.14 WERIT Kunststoffwerke W. Schneider GmbH & Co. KG

- 6.4.15 ACTI PACK S.A.S.

- 6.4.16 RETAL Industries Ltd.

- 6.4.17 RIKUTEC Group

- 6.4.18 AST Kunststoffverarbeitung GmbH

- 6.4.19 Robinson plc

- 6.4.20 Esterform Packaging Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

硬质塑胶包装市场:依产品类型、材料类型、製造流程和最终用途产业划分-2026-2032年全球市场预测

硬质塑胶包装市场:依产品类型、材料类型、製造流程和最终用途产业划分-2026-2032年全球市场预测 硬质塑胶包装市场分析及预测(至2035年):类型、产品类型、材质类型、技术、应用、最终用户、功能、製程和设备

硬质塑胶包装市场分析及预测(至2035年):类型、产品类型、材质类型、技术、应用、最终用户、功能、製程和设备 全球硬质塑胶包装市场规模、份额、趋势和成长分析报告(2026-2034年)

全球硬质塑胶包装市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球硬质塑胶包装市场报告

2026年全球硬质塑胶包装市场报告 硬质塑胶包装市场报告:按材料类型、产品类型、最终用途产业和地区划分

硬质塑胶包装市场报告:按材料类型、产品类型、最终用途产业和地区划分 硬质塑胶包装市场规模、份额和趋势分析报告:按材料、产品、应用、地区和细分市场预测(2026-2033 年)

硬质塑胶包装市场规模、份额和趋势分析报告:按材料、产品、应用、地区和细分市场预测(2026-2033 年) 硬质塑胶包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

硬质塑胶包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 硬质塑胶包装的印度市场:类别,各流程,各产品,各终端用户产业,各地区,机会,预测,2019年~2033年

硬质塑胶包装的印度市场:类别,各流程,各产品,各终端用户产业,各地区,机会,预测,2019年~2033年 硬质塑胶包装的未来(~2030年)

硬质塑胶包装的未来(~2030年) 2025 年至 2033 年硬质塑胶包装市场规模、份额、趋势及预测(依产品、材料、生产流程、最终用途产业及地区)

2025 年至 2033 年硬质塑胶包装市场规模、份额、趋势及预测(依产品、材料、生产流程、最终用途产业及地区)