|

市场调查报告书

商品编码

1906865

混合云端:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Hybrid Cloud - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

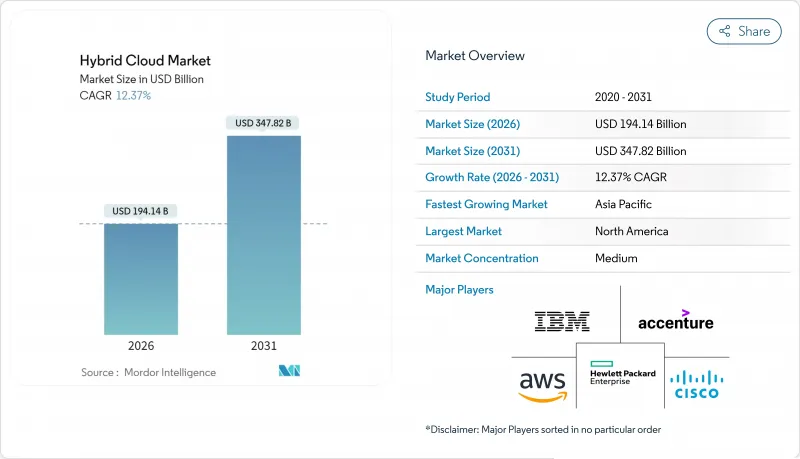

预计到 2025 年,混合云端市场规模将达到 1,727.7 亿美元,到 2026 年将达到 1,941.4 亿美元,到 2031 年将达到 3,478.2 亿美元,预测期(2026-2031 年)的复合年增长率为 12.37%。

企业正朝着分散式架构转型,力求在维运控制和云端原生速度之间取得平衡,尤其是在生成式人工智慧工作负载需要边缘运算资源和集中式运算资源之间更紧密协调的情况下。更严格的主权监管、日益增长的多重云端趋势以及日益成熟的容器编排管理框架,都在推动对混合部署模式的需求。边缘运算投资能够降低人工智慧推理延迟,同时保留本地数据以满足合规性要求。大型资料中心营运商正在将基础设施计划与企业脱碳目标结合,并将永续性纳入采购标准。超大规模资料中心业者和专业边缘运算供应商的策略性收购,正在加剧混合云端市场的竞争差异化。

全球混合云端市场趋势与洞察

大型企业多重云端采用率激增

混合环境如今已成为精心建构的多重云端策略的基础,87% 的企业都在多个云端服务供应商之间运行工作负载。平台团队正在标准化工具,以减少重复支出并提高管治的一致性。从设计之初就建立财务营运实践,正在减少混合云端市场的浪费。供应商也积极回应,提供统一的计费仪表板,将使用情况与成本中心关联起来。随着多重云端成熟度的提高,工作负载的无缝迁移已成为混合云端市场的关键采购标准。

资料主权架构的需求日益增长

严格的隐私法规正在重塑工作负载部署决策。尤其在欧洲,84% 的组织正在使用主权云端解决方案,或计划在未来 12 个月内部署此类解决方案。澳洲和亚洲部分地区也采用了类似的法规,迫使服务提供者推出区域特定的控制平面。专门的主权解决方案承诺提供资料居住、金钥管理和本地运营商支援。超大规模云端服务超大规模资料中心业者目前正在为欧盟整合机密运算和专用支援模式,以维持其在混合云端市场的份额。日益复杂的合规性要求推动了对架构设计的需求,这种设计既能将高度监管的工作负载保留在特定司法管辖区内,又能利用全球规模来处理监管较少的工作负载。

迁移复杂性与遗留系统整合成本

现代化计划常常会暴露出未记录的依赖关係,导致工期和预算大幅超支。大型银行在为混合环境重构核心支付系统时,都遭遇了严重的超支。如今,73% 的公司选择重构而非直接迁移,以延长工期为代价,换取了更高的系统弹性。持续整合管道和 API 闸道在一定程度上缓解了瓶颈问题,但技术债仍然是混合云端市场短期内的一大阻力。

细分市场分析

预计到 2031 年,业务收益将以 14.68% 的复合年增长率增长,而解决方案在 2025 年将保持 64.80% 的混合云端市场份额。这一高成长率主要得益于企业对多重云端编配、主权映射和 AI 技术栈对齐方面的专家指导的需求。 Rackspace 和 AWS 已推出“快速迁移方案”,将工具和专业服务结合,以缩短迁移时间。

託管式财务运维 (FinOps)、容器安全和平台运维的需求不断增长,迫使服务提供者扩展其服务范围。 Nutanix 推出了一款融合软体和咨询服务的企业级人工智慧平台,旨在填补技能短缺的空白。这些趋势表明,随着企业将复杂维运外包,服务领域将在混合云端市场中占据更大的份额。

预计从2026年到2031年,IaaS将以13.62%的复合年增长率成长。同时,由于企业套件的普及,SaaS将维持54.10%的市场占有率。生成式人工智慧训练需要配备丰富GPU的丛集,客户通常会在IaaS平台上建立这些集群以进行自订调优。 Oracle已扩展其分散式云端产品组合,提供可在恶劣环境下部署运算资源的粗纱边缘设备,凸显了IaaS的多功能性。

平台即服务 (PaaS) 是一座策略桥樑,它提供抽象层,同时允许自订运行时。 Snowflake 已将其平台与 Azure OpenAI 服务集成,以简化分析开发人员的模型使用。随着人工智慧和开发工作流程的融合,这三种模式将在混合云端市场中继续互通。

混合云端市场按组件(解决方案、服务)、服务模式(IaaS、PaaS、SaaS)、组织规模(大型企业、中小企业)、最终用户行业(政府及公共部门、医疗保健及生命科学、银行、金融服务和保险等)以及地区进行细分。市场预测以美元(USD)计价。

区域分析

北美地区预计到 2025 年将占据 25.30% 的市场份额,这得益于其密集的超大规模超大规模资料中心业者网络,简化了多重云端部署。 TP ICAP 计划在 2026 年将其 80% 的系统迁移到 AWS,同时建立一个人工智慧实验室,用于资本市场创新。联邦隐私法规仍然可控,使企业能够自由优化混合云端市场的工作负载部署。

亚太地区到2031年将以12.89%的复合年增长率领跑,主要受产能扩张和数位服务需求成长的推动。微软已承诺在日本投资29亿美元建造新的人工智慧和云端运算园区,以满足日益增长的推理处理需求。随着国内成长放缓,中国服务供应商正积极拓展海外市场。目前,亚太地区资料中心已投入运作中12,206兆瓦,在建容量达14,338兆瓦,这将为混合云端市场的未来成长提供有力支撑。

欧洲正稳步推进,84% 的企业正在实施或计划建立主权云端框架。微软已部署了多层主权解决方案,涵盖逻辑隔离、本地金钥管理和欧盟本地支援团队。俄罗斯和沙乌地阿拉伯严格的资料在地化法律增加了复杂性,但也为本地专家创造了机会。在中东和非洲 (MEA) 以及南美等新兴市场,随着海底电缆线路和可再生能源计划的发展降低了准入门槛,投资正在加速成长,从而推动了混合云端市场的发展。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 大型企业多重云端采用率激增

- 资料主权架构的需求日益增长

- 加速生成式人工智慧工作负载需要云端到边缘的接近性。

- 边缘原生容器编排管理框架正在日趋成熟

- 企业对成本优化和财务营运能力的兴趣日益浓厚

- 绿色资料中心指令推动混合环境回归

- 市场限制

- 迁移复杂性与遗留系统整合成本

- 云端原生安全和财务维运技能短缺

- 隐藏的资料传输费用限制了工作负载的可携性。

- 地缘政治资料本地化法规使架构碎片化

- 供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 对影响市场的宏观经济因素进行评估

第五章 市场规模与成长预测

- 按组件

- 解决方案

- 服务

- 按服务模式

- 基础设施即服务 (IaaS)

- 平台即服务 (PaaS)

- 软体即服务 (SaaS)

- 按组织规模

- 大公司

- 中小企业

- 按最终用户行业划分

- 政府和公共部门

- 医疗保健和生命科学

- 银行、金融服务和保险(BFSI)

- 零售与电子商务

- 资讯通信技术和电讯

- 製造业

- 媒体与娱乐

- 其他的

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 澳洲

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 埃及

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Amazon Web Services Inc.

- Microsoft Corporation

- Google LLC

- IBM Corporation

- Cisco Systems Inc.

- Hewlett Packard Enterprise Company

- VMware Inc.

- Oracle Corporation

- Alibaba Cloud

- Dell Technologies Inc.

- Rackspace Technology Inc.

- Accenture PLC

- Equinix Inc.

- Fujitsu Ltd.

- NTT Communications Corporation

- DXC Technology Company

- Lumen Technologies Inc.

- Panzura Inc.

- Flexera Software LLC

- Intel Corporation

- Nutanix Inc.

- Red Hat(IBM)

- NetApp Inc.

- Citrix Systems(Cloud Software Group)

第七章 市场机会与未来展望

The hybrid cloud market was valued at USD 172.77 billion in 2025 and estimated to grow from USD 194.14 billion in 2026 to reach USD 347.82 billion by 2031, at a CAGR of 12.37% during the forecast period (2026-2031).

Enterprises are steering toward distributed architectures that balance operational control with cloud-native speed, especially as generative-AI workloads require tight linkage between edge and centralized compute resources. Growing sovereignty rules, multicloud preferences, and maturing container orchestration frameworks spur demand for hybrid deployment models. Edge computing investments shorten latency for AI inference while retaining on-premises data for compliance. Large data-center operators are aligning infrastructure projects with corporate decarbonization targets, adding sustainability as a procurement criterion. Strategic acquisitions by hyperscalers and specialized edge providers intensify competitive differentiation across the hybrid cloud market.

Global Hybrid Cloud Market Trends and Insights

Surge in Multicloud Adoption Among Large Enterprises

Hybrid environments now underpin deliberate multicloud strategies, with 87% of enterprises operating workloads across more than one provider.Platform teams standardize tooling to curb redundant spend and improve governance consistency. Financial-operations practices are embedded at design stages to cut waste in the hybrid cloud market. Vendors respond by offering unified billing dashboards that map usage to cost centers. As multicloud maturity rises, seamless workload portability becomes a core purchase criterion for the hybrid cloud market.

Rising Demand for Data-Sovereign Architectures

Strict privacy regimes reshuffle workload placement decisions, particularly in Europe where 84% of organizations either use or plan sovereign cloud solutions within 12 months.Australia and parts of Asia adopt similar rules, pressing providers to launch region-specific control planes. Specialized sovereign offerings promise residency, key management, and local operator staffing. Hyperscalers now integrate confidential computing and dedicated EU support models to retain share in the hybrid cloud market. Compliance complexity therefore fuels demand for architecture designs that keep sensitive data in jurisdiction while leveraging global scale for less regulated workloads.

Migration Complexity and Legacy Integration Costs

Modernization projects often reveal undocumented dependencies that inflate timelines and budgets. Large banks report significant overruns when refactoring core payment systems for hybrid environments. Seventy-three percent of enterprises now refactor rather than lift-and-shift, extending schedules yet delivering better resilience. Continuous integration pipelines and API gateways partly mitigate the hurdle, but technical debt remains a near-term drag on the hybrid cloud market.

Other drivers and restraints analyzed in the detailed report include:

- GenAI Workload Acceleration Needs Cloud-Edge Proximity

- Green Datacenter Mandates Push Hybrid Repatriation

- Skills Shortage in Cloud-Native Security and FinOps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services revenue is forecast to rise at 14.68% CAGR through 2031, even though solutions retained 64.80% hybrid cloud market share in 2025. The higher growth stems from enterprises requesting expert guidance for multicloud orchestration, sovereignty mapping, and AI stack tuning. Rackspace and AWS launched Rapid Migration Offer programs that bundle tooling with professional services to shorten cut-over durations.

Demand for managed FinOps, container security, and platform operations pushes providers to expand service lines. Nutanix introduced an Enterprise AI platform that blends software with consulting to offset skills shortages. These trends suggest the services segment will account for a larger slice of hybrid cloud market size as organizations outsource complexity.

IaaS is projected to grow at 13.62% CAGR during 2026-2031, while SaaS keeps 54.10% share thanks to entrenched enterprise suites. Generative-AI training needs GPU-rich clusters that customers often build on IaaS for custom tuning. Oracle extended its distributed cloud line with Roving Edge devices that place compute in austere locations, underscoring the versatility of IaaS.

Platform-as-a-Service occupies a strategic bridge, offering abstraction yet permitting custom runtimes. Snowflake linked its platform with Azure OpenAI Service to simplify model usage for analytics developers. The convergence of AI and development workflows will keep all three models interlinked within the hybrid cloud market.

Hybrid Cloud Market is Segmented by Component (Solutions, Services), Service Model (IaaS, Paas, Saas), Organization Size (Large Enterprises, Smes), End-User Industry (Government and Public Sector, Healthcare and Life Sciences, BFSI, and More) and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 25.30% revenue share in 2025 and benefits from dense hyperscaler footprints that simplify multicloud adoption. TP ICAP plans to shift 80% of systems to AWS by 2026 while creating AI labs for capital-markets innovation. Federal privacy rules remain manageable, allowing firms to optimize workload placement freely across the hybrid cloud market.

Asia-Pacific exhibits the steepest 12.89% CAGR through 2031, driven by capacity additions and rising digital-service demand. Microsoft pledged USD 2.9 billion for new AI and cloud zones in Japan to address growing inference requirements. China's providers pursue overseas expansion as domestic growth moderates. Regional data-center capacity now totals 12,206 MW in operation with 14,338 MW under build, underpinning future hybrid cloud market growth.

Europe advances at a steady clip as 84% of firms either deploy or plan sovereign cloud framework adoption. Microsoft rolled out a layered sovereignty solution spanning logical isolation, local key control, and EU-native support teams. Stricter data-localization laws in Russia and Saudi Arabia add complexity but also create opportunities for regional specialists. Emerging markets across MEA and South America accelerate investment as submarine cable routes and renewable energy projects reduce barriers, expanding the hybrid cloud market.

- Amazon Web Services Inc.

- Microsoft Corporation

- Google LLC

- IBM Corporation

- Cisco Systems Inc.

- Hewlett Packard Enterprise Company

- VMware Inc.

- Oracle Corporation

- Alibaba Cloud

- Dell Technologies Inc.

- Rackspace Technology Inc.

- Accenture PLC

- Equinix Inc.

- Fujitsu Ltd.

- NTT Communications Corporation

- DXC Technology Company

- Lumen Technologies Inc.

- Panzura Inc.

- Flexera Software LLC

- Intel Corporation

- Nutanix Inc.

- Red Hat (IBM)

- NetApp Inc.

- Citrix Systems (Cloud Software Group)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in multicloud adoption among large enterprises

- 4.2.2 Rising demand for data-sovereign architectures

- 4.2.3 GenAI workload acceleration needs cloud-edge proximity

- 4.2.4 Edge-native container orchestration frameworks mature

- 4.2.5 Rising enterprise focus on cost optimization and FinOps capabilities

- 4.2.6 Green datacenter mandates push hybrid repatriation

- 4.3 Market Restraints

- 4.3.1 Migration complexity and legacy integration costs

- 4.3.2 Skills shortage in cloud-native security and FinOps

- 4.3.3 Hidden egress-fee economics limit workload portability

- 4.3.4 Geo-political data localization rules fragment architectures

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assesment of Macroeconomic Factors on the market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Service Model

- 5.2.1 Infrastructure as a Service (IaaS)

- 5.2.2 Platform as a Service (PaaS)

- 5.2.3 Software as a Service (SaaS)

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-user Industry

- 5.4.1 Government and Public Sector

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Banking, Financial Services and Insurance (BFSI)

- 5.4.4 Retail and E-Commerce

- 5.4.5 Information and Communication Technology and Telecom

- 5.4.6 Manufacturing

- 5.4.7 Media and Entertainment

- 5.4.8 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon Web Services Inc.

- 6.4.2 Microsoft Corporation

- 6.4.3 Google LLC

- 6.4.4 IBM Corporation

- 6.4.5 Cisco Systems Inc.

- 6.4.6 Hewlett Packard Enterprise Company

- 6.4.7 VMware Inc.

- 6.4.8 Oracle Corporation

- 6.4.9 Alibaba Cloud

- 6.4.10 Dell Technologies Inc.

- 6.4.11 Rackspace Technology Inc.

- 6.4.12 Accenture PLC

- 6.4.13 Equinix Inc.

- 6.4.14 Fujitsu Ltd.

- 6.4.15 NTT Communications Corporation

- 6.4.16 DXC Technology Company

- 6.4.17 Lumen Technologies Inc.

- 6.4.18 Panzura Inc.

- 6.4.19 Flexera Software LLC

- 6.4.20 Intel Corporation

- 6.4.21 Nutanix Inc.

- 6.4.22 Red Hat (IBM)

- 6.4.23 NetApp Inc.

- 6.4.24 Citrix Systems (Cloud Software Group)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

2026年全球託管混合云端市场报告2026年全球混合云端市场报告

2026年全球託管混合云端市场报告2026年全球混合云端市场报告 全球混合云端市场规模、份额、趋势和成长分析报告(2026-2034年)

全球混合云端市场规模、份额、趋势和成长分析报告(2026-2034年) 混合云端市场 - 全球产业规模、份额、趋势、机会和预测(按组件、交付模式、组织规模、最终用户、地区和竞争格局划分),2021-2031 年

混合云端市场 - 全球产业规模、份额、趋势、机会和预测(按组件、交付模式、组织规模、最终用户、地区和竞争格局划分),2021-2031 年 日本混合云端市场规模、份额、趋势和预测:按组件、组织规模、行业和地区划分,2026-2034 年

日本混合云端市场规模、份额、趋势和预测:按组件、组织规模、行业和地区划分,2026-2034 年 混合云端市场规模、份额和成长分析(按组件、服务模型、组织规模、垂直产业和地区划分)-2026-2033年产业预测

混合云端市场规模、份额和成长分析(按组件、服务模型、组织规模、垂直产业和地区划分)-2026-2033年产业预测 DDR5 供应短缺推高价格;预计到 2026 年利润将超过 HBM3e混合云端市场:2025-2030 年未来预测

DDR5 供应短缺推高价格;预计到 2026 年利润将超过 HBM3e混合云端市场:2025-2030 年未来预测 混合云端部署卫星遥感探测、影像和资讯服务的全球市场

混合云端部署卫星遥感探测、影像和资讯服务的全球市场 DDR4 供应短缺与价格上涨:全球市场趋势(2025 年下半年)

DDR4 供应短缺与价格上涨:全球市场趋势(2025 年下半年)