|

市场调查报告书

商品编码

1906929

欧洲数位电子看板市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Europe Digital Signage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

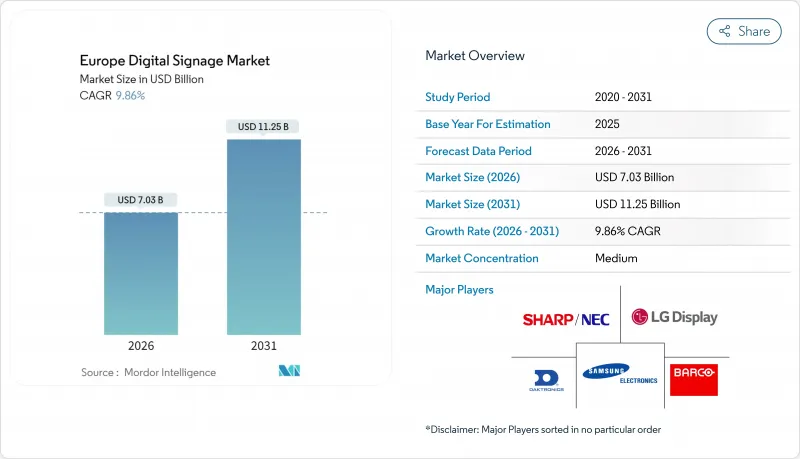

预计到 2026 年,欧洲数位电子看板市场规模将达到 70.3 亿美元,从 2025 年的 64 亿美元成长到 2031 年的 112.5 亿美元,2026 年至 2031 年的复合年增长率为 9.86%。

零售商将电视墙升级至 4K 和 8K 解析度、交通部门将乘客资讯系统数位化以及程式化数位户外广告 (DOOH) 平台普及的小型品牌自动化购买,共同推动了成长。欧洲数位电子看板市场受益于欧盟生态设计法规,该法规旨在减少一次性印刷媒体的使用,并鼓励使用节能显示器。硬体供应商正积极响应,推出低功耗微型 LED 和覆晶显示屏,软体供应商则将人工智慧融入其中,以实现近乎实时的内容个性化。同时,STRATACACHE、ZetaDisplay 和 Vertiseit 等公司的合併正在重组供应链结构,并创建覆盖整个欧洲大陆的服务网络,从而能够支援复杂的跨国部署。

欧洲数位电子看板市场趋势与洞察

数位户外广告支出稳定成长

随着广告主将预算从静态海报转向能够根据天气和人群移动等条件触发因素做出响应的数据驱动型萤幕,程式化户外数位广告 (DOOH) 的份额正在迅速增长。 Clear Channel累计,到 2024 年,北欧地区的营收将达到 6.62 亿美元,其中一半已经来自数位面板。此外,与循环广告销售相比,程序化交易的 CPM 溢价已达到 30% 至 300%。北欧国家是该领先指标,因为其智慧型手机的高普及率和开放的数据政策促进了即时竞价。不断增长的媒体收入正在为更多萤幕的部署资金筹措,从而加强了支撑欧洲数位电子看板市场的反馈循环。

承包解决方案的演变

企业越来越倾向于选择整合显示器、媒体播放机、内容管理、分析和本地服务的单一供应商合约。三星的VXT云端内容管理系统(CMS)託管于法兰克福,并通过了GDPR合规认证,这是一个降低复杂性并确保资料主权的整合解决方案的提案。 LG与BrightSign的合作将系统晶片媒体播放机直接嵌入专业面板,无需笨重的外部硬体。承包模式缩短了引进週期,对于正在从纸质时刻表过渡到动态显示器的机场和铁路营运商而言,这是一个决定性因素。整合商和终端客户之间的风险共担也降低了全生命週期成本,从而鼓励中型企业进入欧洲数位电子看板产业。

客户隐私问题

GDPR 对脸部辨识、人口统计分析和影像分析施加了严格的同意规则,迫使企业即时匿名化资料或完全避免资料收集。零售商若部署摄影机进行受众测量,则必须张贴醒目的通知并提供退出机制,这增加了其资本和法律成本。儘管人工智慧驱动的定向技术已被证明能够有效提升用户参与度,但这些强制规定正在减缓其普及速度,并限制欧洲数位电子看板市场近期的商机。

细分市场分析

到2025年,硬体将占据欧洲数位电子看板市场65.78%的份额,凸显了萤幕基础设施的资本密集特性。 LCD和LED面板主导订单,例如伊丽莎白线等交通计划就采用了55英寸、700尼特亮度的面板,用于多语言乘客提示。 OLED显示器在高端精品店中越来越受欢迎,其深邃的黑色和宽广的可视角度使其较高的价格物有所值。同时,MicroLED已从原型阶段进入小批量生产阶段,预示着它未来将取代拼接式LED。媒体播放机正朝着基于ARM架构、无风扇设计的方向发展,能够全天候运作,这进一步巩固了硬体作为欧洲数位电子看板市场基础的地位。

随着广告商转向程式化竞标和人工智慧驱动的创新优化,预计到2031年,软体产业将以10.88%的复合年增长率成长。开放API实现了自助服务终端、行动应用程式和网路商店之间的跨平台集成,从而打造全通路体验。正如Navori Labs的收购案例所示,针对内容管理系统(CMS)供应商的投资表明,经常性授权收入超过了一次性硬体利润。服务提供从设计、安装到营运管理的完整解决方案,既能帮助供应商抵御硬体价格下跌的风险,也能满足企业对承包工程的需求。

在身临其境型故事叙述和动态定价的驱动下,到2025年,零售业将占据欧洲数位电子看板市场35.62%的份额。服饰连锁店正在利用店内LED显示器上的3D产品渲染图,以强化社群媒体趋势并提升即时。杂货店则采用与会员资料库连结的电子货架标籤,以提供个人化优惠。这些创新使实体店在电商时代保持竞争力,而欧洲数位电子看板市场仍是全通路策略的核心支柱。

到2031年,交通运输计划将成为成长最快的领域,复合年增长率将达到10.95%。例如,法兰克福机场正在出发大厅安装多功能显示屏,用于交替显示航班资讯和与乘客人口统计相关的程式化广告。铁路营运商正在月台上安装耐环境的2.5毫米像素LED灯带,以提供即时服务资讯。这些投资正在透过广告空间促进收入来源多元化,也印证了欧洲数位电子看板市场对基础设施所有者的巨大吸引力。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 数位户外广告支出稳定成长

- 承包解决方案的演变

- 零售业对4K/8K电视墙的需求

- 透过POS系统整合实现动态定价

- 根据欧盟生态设计法规进行印刷品更换

- 小型企业的程式化数位户外广告接入

- 市场限制

- 客户隐私问题

- 大型网路中的高额资本支出(CAPEX)和营运费用(OPEX)

- CMS相容性片段化

- 半导体供应波动

- 产业供应链分析

- 监管环境

- 宏观经济因素的影响

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按类型

- 硬体

- LCD/LED显示器

- OLED显示器

- 媒体播放机

- 投影机/萤幕

- 其他硬体

- 软体

- 服务

- 硬体

- 按最终用户行业划分

- 零售

- 运输

- 饭店业

- 对于企业

- 教育

- 政府机构

- 其他终端用户产业

- 透过分销管道

- 直接的

- 系统整合商

- 透过使用

- 室内数位电子看板

- 户外数位电子看板

- 互动式数位电子看板

- 电视墙

- 数位海报/资讯亭

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Samsung Electronics Co. Ltd(Display Solutions)

- LG Display Co. Ltd

- Sharp NEC Display Solutions Ltd

- Barco NV

- Daktronics Inc.

- Leyard Europe Srl

- Innolux Corp.

- Sony Group Corp.

- Planar Systems Inc.

- BrightSign LLC

- Stratacache Inc.(Scala)

- ZetaDisplay AB

- Broadsign International LLC

- Mvix(USA)Inc.

- Unilumin Group Co. Ltd

- Absen Optoelectronic Co. Ltd

- AOPEN Inc.

- 22Miles Inc.

- Navori Labs SA

- FocusNeo AB

第七章 市场机会与未来展望

Europe digital signage market size in 2026 is estimated at USD 7.03 billion, growing from 2025 value of USD 6.4 billion with 2031 projections showing USD 11.25 billion, growing at 9.86% CAGR over 2026-2031.

Growth accelerates as retailers upgrade video walls to 4K and 8K resolution, transportation authorities digitize passenger information systems, and programmatic digital-out-of-home (DOOH) platforms democratize automated buying for small and mid-sized brands. The Europe digital signage market benefits from EU eco-design rules that discourage single-use print media and incentivize energy-efficient displays. Hardware vendors respond with lower-power microLED and flip-chip displays, while software providers embed AI to personalize content in near real time. At the same time, mergers involving STRATACACHE, ZetaDisplay, Vertiseit, and others are reshaping supply dynamics and creating continental service networks able to support complex, multi-country deployments.

Europe Digital Signage Market Trends and Insights

Steady increase in DOOH ad spend

Programmatic DOOH is gaining share rapidly as advertisers migrate budgets from static posters to data-driven screens that support conditional triggers such as weather or audience movement. Clear Channel generated USD 662 million across Northern Europe in 2024, half of which already came from digital panels, while CPM premiums on programmatic transactions reached 30%-300% over loop-based sales. The Nordic cluster acts as a bellwether because its high smartphone penetration and open data policies foster real-time bidding environments. Higher media yields finance additional screen rollouts, reinforcing a feedback loop that underpins the Europe digital signage market.

Evolution of turnkey solutions

Enterprises increasingly favor single-vendor contracts that bundle displays, media players, content management, analytics, and on-site services. Samsung's VXT cloud CMS, hosted in Frankfurt and certified for GDPR compliance, illustrates how vendors position integrated offers that reduce complexity and ensure data sovereignty. LG's collaboration with BrightSign packages system-on-chip media players directly inside professional panels, eliminating bulky external hardware. Turnkey models shorten deployment cycles, a decisive factor for airports and rail operators migrating from paper timetables to dynamic displays. They also lower lifetime costs by sharing risk between integrators and end clients, encouraging mid-sized enterprises to join the Europe digital signage industry.

Concerns over customer privacy

GDPR imposes strict consent rules on facial recognition, demographic analytics, and video analytics, forcing operators to anonymize data immediately or avoid collection altogether. Retailers that deploy cameras for audience metrics must install visible notices and offer opt-out mechanisms, adding capital and legal costs. These obligations slow the rollout of AI-driven targeting despite proven engagement benefits, dampening near-term revenue opportunities for the Europe digital signage market.

Other drivers and restraints analyzed in the detailed report include:

- Retail demand for 4K / 8K video walls

- Dynamic pricing via POS integration

- High CAPEX and OPEX of large networks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware accounted for 65.78% of Europe digital signage market share in 2025, underscoring the capital intensity of screen infrastructure. LCD and LED panels dominate orders, with transportation projects such as the Elizabeth line adopting 55-inch, 700-nit boards for multi-lingual passenger alerts. OLED displays gain favor in premium boutiques where deep blacks and wide angles justify higher pricing, while microLED moves from prototype to limited production and signals future displacement of tiled LED. Media players transition to ARM-based, fanless designs that withstand 24/7 cycles, further reinforcing hardware as the bedrock of the Europe digital signage market.

Software is poised for an 10.88% CAGR through 2031 as advertisers pivot to programmatic bidding and AI-driven creative optimization. Open APIs enable cross-platform orchestration of kiosks, mobile apps, and web storefronts, creating omnichannel journeys. Investment vehicles targeting CMS suppliers, as seen in the Navori Labs sale, reveal confidence that recurring license income will outpace one-off hardware margins. Services round out solutions through design, installation, and managed operations, offering vendors a hedge against hardware price compression while meeting enterprise demand for turnkey contracts.

Retail commanded 35.62% of Europe digital signage market in 2025, driven by immersive storytelling and dynamic price labeling. Apparel chains use 3D product renders on in-store LED portals to amplify social media trends and drive immediacy. Grocery stores adopt electronic shelf labels that synchronize with loyalty databases to push individualized offers. These innovations keep physical outlets relevant in an e-commerce era and sustain the Europe digital signage market as a core pillar of omnichannel strategies.

Transportation projects are expanding at an 10.95% CAGR, making them the fastest-growing vertical through 2031. Airports like Frankfurt retrofit departure halls with dual-purpose displays that alternate between flight data and programmatic ads linked to passenger demographic data. Rail operators deploy ruggedized 2.5-millimeter-pixel LED ribbons along platforms for real-time service alerts. Such investments diversify revenue streams via advertising concessions, reinforcing the Europe digital signage market's appeal to infrastructure owners.

The Europe Digital Signage Market Report is Segmented by Type (Hardware, Software, and Services), End-User Vertical (Retail, Transportation, Hospitality, Corporate, and More), Distribution Channel (Direct and System Integrators), and Application (Indoor Digital Signage, Outdoor Digital Signage, Interactive Digital Signage, Video Walls, and Digital Posters/Kiosks). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Samsung Electronics Co. Ltd (Display Solutions)

- LG Display Co. Ltd

- Sharp NEC Display Solutions Ltd

- Barco NV

- Daktronics Inc.

- Leyard Europe Srl

- Innolux Corp.

- Sony Group Corp.

- Planar Systems Inc.

- BrightSign LLC

- Stratacache Inc. (Scala)

- ZetaDisplay AB

- Broadsign International LLC

- Mvix (USA) Inc.

- Unilumin Group Co. Ltd

- Absen Optoelectronic Co. Ltd

- AOPEN Inc.

- 22Miles Inc.

- Navori Labs SA

- FocusNeo AB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Steady increase in DOOH ad spend

- 4.2.2 Evolution of turnkey solutions

- 4.2.3 Retail demand for 4K/8K video walls

- 4.2.4 Dynamic pricing via POS integration

- 4.2.5 EU eco-design rules replacing print media

- 4.2.6 Programmatic DOOH access for SMBs

- 4.3 Market Restraints

- 4.3.1 Concerns over customer privacy

- 4.3.2 High CAPEX and OPEX of large networks

- 4.3.3 CMS compatibility fragmentation

- 4.3.4 Semiconductor supply volatility

- 4.4 Industry Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Impact of Macroeconomic Factors

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Hardware

- 5.1.1.1 LCD / LED Displays

- 5.1.1.2 OLED Displays

- 5.1.1.3 Media Players

- 5.1.1.4 Projectors / Screens

- 5.1.1.5 Other Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.1.1 Hardware

- 5.2 By End-User Vertical

- 5.2.1 Retail

- 5.2.2 Transportation

- 5.2.3 Hospitality

- 5.2.4 Corporate

- 5.2.5 Education

- 5.2.6 Government

- 5.2.7 Other End-User Verticals

- 5.3 By Distribution Channel

- 5.3.1 Direct

- 5.3.2 System Integrators

- 5.4 By Application

- 5.4.1 Indoor Digital Signage

- 5.4.2 Outdoor Digital Signage

- 5.4.3 Interactive Digital Signage

- 5.4.4 Video Walls

- 5.4.5 Digital Posters / Kiosks

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Samsung Electronics Co. Ltd (Display Solutions)

- 6.4.2 LG Display Co. Ltd

- 6.4.3 Sharp NEC Display Solutions Ltd

- 6.4.4 Barco NV

- 6.4.5 Daktronics Inc.

- 6.4.6 Leyard Europe Srl

- 6.4.7 Innolux Corp.

- 6.4.8 Sony Group Corp.

- 6.4.9 Planar Systems Inc.

- 6.4.10 BrightSign LLC

- 6.4.11 Stratacache Inc. (Scala)

- 6.4.12 ZetaDisplay AB

- 6.4.13 Broadsign International LLC

- 6.4.14 Mvix (USA) Inc.

- 6.4.15 Unilumin Group Co. Ltd

- 6.4.16 Absen Optoelectronic Co. Ltd

- 6.4.17 AOPEN Inc.

- 6.4.18 22Miles Inc.

- 6.4.19 Navori Labs SA

- 6.4.20 FocusNeo AB

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

数位电子看板市场:2026-2032年全球市场预测(按组件、显示技术、内容类型、解析度、萤幕大小、连接方式、应用、安装位置和部署模式划分)

数位电子看板市场:2026-2032年全球市场预测(按组件、显示技术、内容类型、解析度、萤幕大小、连接方式、应用、安装位置和部署模式划分) 2026-2030年全球商用大尺寸显示指示牌市场LED指示牌市场:按应用程式、显示类型、技术、安装方式、像素间距和最终用户划分-2026-2032年全球市场预测

2026-2030年全球商用大尺寸显示指示牌市场LED指示牌市场:按应用程式、显示类型、技术、安装方式、像素间距和最终用户划分-2026-2032年全球市场预测 数位相机显示器市场报告:趋势、预测和竞争分析(至2035年)橱窗数位电子看板市场报告:趋势、预测及竞争分析(至2035年)

数位相机显示器市场报告:趋势、预测和竞争分析(至2035年)橱窗数位电子看板市场报告:趋势、预测及竞争分析(至2035年) 2026年全球数位电子看板市场报告

2026年全球数位电子看板市场报告 全球智慧指示牌市场规模、份额、趋势和成长分析报告(2026-2034)

全球智慧指示牌市场规模、份额、趋势和成长分析报告(2026-2034) 数位看板市场:依产品、组件(硬体、服务)、应用和行业划分 - 至2036年的全球预测

数位看板市场:依产品、组件(硬体、服务)、应用和行业划分 - 至2036年的全球预测 LED数位记分板市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、形状、材质、最终用户、安装类型划分医疗数位电子看板市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、部署模式、最终用户、功能和安装类型划分

LED数位记分板市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、形状、材质、最终用户、安装类型划分医疗数位电子看板市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、部署模式、最终用户、功能和安装类型划分