|

市场调查报告书

商品编码

1906959

欧洲农业机械市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)Europe Agricultural Machinery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

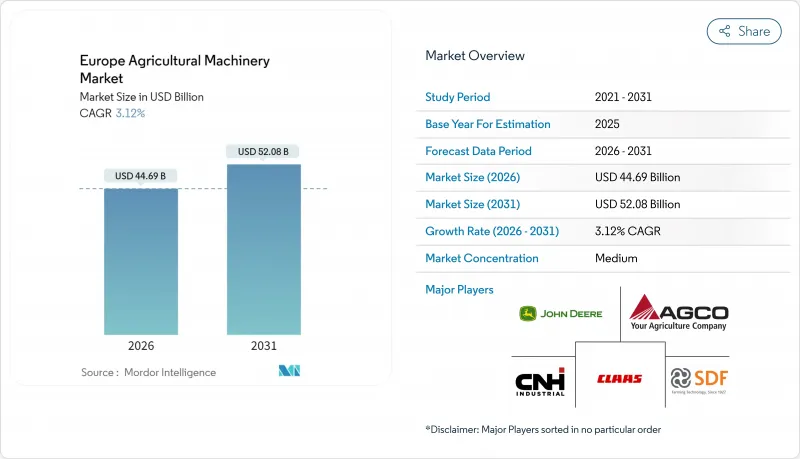

预计到 2026 年,欧洲农业机械市场规模将达到 446.9 亿美元,从 2025 年的 433.4 亿美元成长到 2031 年的 520.8 亿美元,2026 年至 2031 年的复合年增长率为 3.12%。

农业劳动力短缺、欧盟严格的环境法规以及数位化普及正在重塑资本支出重点,使农业机械转向低排放、配备丰富感测器的设备。农民不再追求更高的马力,而是转向能够自动执行重复性任务、追踪永续性并与企业软体整合的智慧系统。为了应对这一趋势,原始设备製造商(OEM)正在提供模组化平台,允许持续进行软体和感测器升级,从而缩短产品生命週期并增加经常性收入来源。预计从2027年起,半导体供应量的增加和电池成本的下降将稳定交付时间并加速电气化进程。这将缩小欧洲农业机械市场早期采用者和后期采用者之间的差距。

欧洲农业机械市场趋势与洞察

欧盟和各国政府的补贴加速了机械化进程

欧洲投资银行(EIB)提供的10亿欧元(10.5亿美元)永续发展农业技术贷款机制,可为排放的设备采购提供高达70%的标价补贴。加上德国联邦政府提供的20%机械补贴,这使得符合第五阶段排放标准的拖拉机的净购买成本与传统的第三阶段排放标准拖拉机持平,从而缩短了保守型买家的投资回收期。法国和义大利也实施了类似的补贴计划,并将补贴预算提前至2025年至2027年发放,导致预订量激增。为了鼓励用户采用符合排放标准的拖拉机,原始设备製造商(OEM)正在调整产品发布计划,以配合补贴申请截止日期。租赁公司则将合约期限延长至七年,与补贴偿还期一致,从而减轻年度现金流压力,并鼓励用户提前续约40马力以下的拖拉机。

农业机械的快速型号升级

由于排放气体法规的修订和数位子系统的引入,主流拖拉机产品线的平均更新周期已从六年缩短至不到两年。迪尔公司(Deere & Company)2025年的自动驾驶拖拉机配备了全新的雷射雷达阵列和无线韧体,无需更换硬体即可优化路径规划。农机设备被视为一个不断发展的平台,47%的德国受访者计划每季进行软体更新以获得农艺优势。这种快速的更新週期迫使经销商投资于先进的服务工具。在欧洲农业设备市场,製造商正转向功能解锁的订阅定价模式,以实现收入来源多元化,不再仅依赖产品销售。

初始成本和维护成本不断上涨

预计2024年至2025年间,配备丰富感测器的联合收割机和自动喷药机的标价将上涨18%,某些配置的单价甚至将超过100万美元。管理200至400公顷土地的中型农场主面临着农机和土地改良计画之间的艰难抉择,尤其是在东欧地区,那里的平均净利率徘徊在7%左右。由于专有电子设备需要经销商介入,维修成本也不断上升。目前,法国的平均每小时服务费用为105欧元(110美元),高于2020年的68欧元(71美元)。小规模农场可以透过组成机械联盟来降低成本,但协调工作的成本可能会抵消效率提升所带来的效益。

细分市场分析

到2025年,拖拉机仍将维持其市场主导地位,市占率高达48.85%,这反映了其作为欧洲大部分农业主要动力来源的根本性作用。在拖拉机类别中,100-150马力细分市场在平均耕地面积为65公顷的欧洲农场中占最大份额。同时,150匹马力以上的细分市场成长最快,这主要得益于大型农场为提高效率而对高功率设备的需求。犁地和耕作设备是第二大类别,其中耕耘机和动力耕耘机的需求特别强劲,因为保护性耕作方式在欧洲的普及程度越来越高。欧盟委员会2023年推出的4.3亿欧元(约4.55亿美元)农民补贴计画(包括高成本投入品和设备的补贴)也是推动这项成长的关键因素。

灌溉设备正以3.74%的复合年增长率成为成长最快的细分市场,其成长主要受降雨模式日益不稳定以及用水法规要求提高效率的推动。滴灌系统是推动此成长的主要动力,与传统喷灌系统相比,滴灌系统可节水40-60%,同时也能精准施肥,提高作物产量。收割设备的需求保持稳定,联合收割机在该领域占据主导地位,但随着关键收割期劳动力短缺问题日益严重,智慧自动收割机已成为成长最快的细分市场。干草和饲料设备为欧洲庞大的酪农行业提供支持,其中,随着农民优化饲料生产效率,对打捆机的需求尤其增长。 「其他」类别(包括无人机和精准播种机)正经历爆发式增长,该类别基数小规模,但农民们正在尝试新兴技术,这些技术有望在操作上优于传统方法。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 长期农业劳动力短缺

- 欧盟和各成员国的补贴正在加速机械化进程。

- 农业机械的快速模型更新

- 远端资讯处理与预测性维护技术应用广泛

- 低排放机械的环保计画奖励

- OEM农业软硬体捆绑融资

- 市场限制

- 高昂的初始成本和维修成本

- 连网装置的网路安全风险

- 半导体供应受限

- 遵守柴油排放法规的成本不断增加

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按类型

- 联结机

- 不到50马力

- 50-100马力

- 100-150马力

- 马力超过150匹的车型

- 犁地和栽培设备

- 耕耘机

- 光环

- 耕耘机和中耕机

- 其他设备(起独占机、旋耕机等)

- 灌溉机械

- 喷灌

- 滴灌

- 其他灌溉设备(微灌、中心支轴式喷灌等)

- 收割机

- 结合

- 饲料收割机

- 智慧/自主收割机

- 干草和饲料机械

- 死神

- 打包机

- 其他干草收割设备(耙草机、翻晒机等)

- 其他类型(无人机、精密播种机)

- 联结机

- 按地区

- 德国

- 法国

- 英国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Deere & Company

- CNH Industrial NV

- AGCO Corporation

- Kubota Corporation

- CLAAS KGaA mbH

- SDF SpA

- Kuhn SAS(Bucher Industries AG)

- Yanmar Holdings Co., Ltd.

- GRIMME Landmaschinenfabrik GmbH & Co. KG

- Horsch Maschinen GmbH(HORSCH PIRK Forestry GmbH)

- Mahindra & Mahindra Ltd.

- Pottinger Landtechnik GmbH

- Tractors and Farm Equipment Limited(TAFE)

第七章 市场机会与未来展望

The Europe agricultural machinery market size in 2026 is estimated at USD 44.69 billion, growing from 2025 value of USD 43.34 billion with 2031 projections showing USD 52.08 billion, growing at 3.12% CAGR over 2026-2031.

Tight farm-labor supply, stringent European Union environmental mandates, and widespread digitalization are reshaping capital-spending priorities toward low-emission, sensor-rich equipment. Farmers are shifting from horsepower upgrades to intelligent systems that automate repetitive tasks, document sustainability performance, and integrate with enterprise software. Original Equipment Manufacturers (OEMs) are responding with modular platforms that accept continuous software and sensor retrofits, shortening model life cycles and expanding recurring-revenue streams. Rising semiconductor availability and falling battery costs from 2027 onward are anticipated to stabilize delivery schedules and accelerate electrification, closing the gap between early-adopter and late-adopter regions of the Europe agricultural machinery market.

Europe Agricultural Machinery Market Trends and Insights

European Union and National Subsidies are Accelerating Mechanization

The European Investment Bank's EUR 1 billion (USD 1.05 billion) sustainability-linked agtech loan window covers up to 70% of equipment list prices for emissions-verified purchases. When stacked with Germany's federal 20% machinery grant, net acquisition costs for Stage V tractors drop to parity with legacy Tier III units, flattening payback curves for conservative buyers. France and Italy deploy similar top-up schemes, ensuring that subsidy budgets are front-loaded into the 2025-2027 window, which drives a spike in advance orders. OEMs are synchronizing product-launch calendars with grant-application deadlines to maximize uptake. Leasing companies are extending contracts to seven years to align with subsidy claw-back periods, lowering annual cash footprints and fostering premature retirement of sub-40-horsepower fleets.

Rapid Model Upgrades in Agricultural Machinery

Average release cycles for mainstream tractor lines have compressed from six years to fewer than two, propelled by emission revisions and the influx of digital subsystems. Deere & Company's 2025 autonomous tractors debuted new LiDAR arrays and over-the-air firmware that optimize path planning without hardware swaps. Farmers now view machinery as an evolving platform, with 47% of German survey respondents plan to upgrade software quarterly to capture agronomic gains. The speed of iteration pushes dealers to invest in advanced service tools. Manufacturers in the Europe agricultural machinery market are pivoting to subscription pricing for feature unlocks, diversifying revenue beyond unit sales.

High Upfront and Maintenance Costs

List prices for sensor-rich combines and autonomous sprayers jumped 18% between 2024 and 2025, pushing some configurations beyond USD 1 million per unit. Mid-sized growers operating 200-400 hectares face difficult trade-offs between machinery and land-improvement projects, especially in Eastern Europe where average net margins hover near 7%. Maintenance expenses have also climbed as proprietary electronics require dealer intervention. Hourly service rates in France now average EUR 105 (USD 110) compared with EUR 68 (USD 71) in 2020. Smaller farms mitigate costs by forming machinery rings, but coordination overhead can erode efficiency gains.

Other drivers and restraints analyzed in the detailed report include:

- High Adoption of Telematics and Predictive Maintenance

- Eco-Scheme Incentives for Low-Emission Machinery

- Cybersecurity Risks in Connected Equipment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tractors maintain commanding market leadership with a 48.85% share in 2025, reflecting their fundamental role as the primary power source for most European farming operations. Within the tractor category, the 100-150 HP segment captures the largest share among European farms that average 65 hectares, while the greater than 150 HP segment experiences the fastest growth as large-scale operations pursue efficiency through higher-capacity equipment. Plowing and cultivating equipment represents the second-largest category, with cultivators and tillers showing particular strength as conservation tillage practices gain adoption across the continent. The financial grant of Euro 430 million (USD 455 million) by the European Commission for the farmers opting for high-cost inputs in 2023, including agricultural equipment such as plows, is also one of the major factors increasing the adoption rates.

Irrigation machinery emerges as the fastest-growing segment at 3.74% CAGR, driven by increasingly erratic precipitation patterns and water usage regulations that mandate efficiency improvements. Drip irrigation systems lead this expansion as they deliver 40-60% water savings compared to traditional sprinkler systems while enabling precise nutrient delivery that enhances crop yields. Harvesting machinery maintains steady demand with combine harvesters dominating the category, though smart and autonomous harvesters represent the highest-growth subsegment as labor shortages intensify during critical harvest windows. Haying and forage machinery serves the substantial European dairy sector, with balers experiencing particular demand as farmers optimize feed production efficiency. The "Other Types" category, including drones and precision seeders, shows explosive growth from a small base as farmers experiment with emerging technologies that promise operational advantages over conventional approaches.

The Europe Agricultural Machinery Market Report is Segmented by Type (Tractors, Plowing and Cultivating Equipment, Irrigation Machinery, Harvesting Machinery, and More), and by Geography (Germany, France, United Kingdom, Italy, Spain, Russia, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Deere & Company

- CNH Industrial N.V.

- AGCO Corporation

- Kubota Corporation

- CLAAS KGaA mbH

- SDF S.p.A

- Kuhn SAS (Bucher Industries AG)

- Yanmar Holdings Co., Ltd.

- GRIMME Landmaschinenfabrik GmbH & Co. KG

- Horsch Maschinen GmbH (HORSCH PIRK Forestry GmbH)

- Mahindra & Mahindra Ltd.

- Pottinger Landtechnik GmbH

- Tractors and Farm Equipment Limited (TAFE)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Chronic farm-labor shortage

- 4.2.2 European Union and national subsidies are accelerating mechanization

- 4.2.3 Rapid model upgrades in agricultural machinery

- 4.2.4 High adoption of telematics and predictive maintenance

- 4.2.5 Eco-scheme incentives for low-emission machinery

- 4.2.6 OEM ag-software hardware-bundle financing

- 4.3 Market Restraints

- 4.3.1 High upfront and maintenance costs

- 4.3.2 Cybersecurity risks in connected equipment

- 4.3.3 Semiconductor supply constraints

- 4.3.4 Diesel-emission compliance cost escalation

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Tractor

- 5.1.1.1 Less than 50 HP

- 5.1.1.2 50 to 100 HP

- 5.1.1.3 100 to 150 HP

- 5.1.1.4 More than 150 HP

- 5.1.2 Plowing and Cultivating Equipment

- 5.1.2.1 Plows

- 5.1.2.2 Harrows

- 5.1.2.3 Cultivators and Tillers

- 5.1.2.4 Other Equipment (Ridger, Rotary tillers, etc.)

- 5.1.3 Irrigation Machinery

- 5.1.3.1 Sprinkler

- 5.1.3.2 Drip

- 5.1.3.3 Other Irrigation Machinery (Micro-irrigation, Pivot irrigation, etc.)

- 5.1.4 Harvesting Machinery

- 5.1.4.1 Combine Harvesters

- 5.1.4.2 Forage Harvesters

- 5.1.4.3 Smart/Autonomous Harvesters

- 5.1.5 Haying and Forage Machinery

- 5.1.5.1 Mowers

- 5.1.5.2 Balers

- 5.1.5.3 Other Haying Equipment (Rakes, Tedders, etc.)

- 5.1.6 Other Types (Drones, Precision Seeders)

- 5.1.1 Tractor

- 5.2 By Geography

- 5.2.1 Germany

- 5.2.2 France

- 5.2.3 United Kingdom

- 5.2.4 Italy

- 5.2.5 Spain

- 5.2.6 Russia

- 5.2.7 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Deere & Company

- 6.4.2 CNH Industrial N.V.

- 6.4.3 AGCO Corporation

- 6.4.4 Kubota Corporation

- 6.4.5 CLAAS KGaA mbH

- 6.4.6 SDF S.p.A

- 6.4.7 Kuhn SAS (Bucher Industries AG)

- 6.4.8 Yanmar Holdings Co., Ltd.

- 6.4.9 GRIMME Landmaschinenfabrik GmbH & Co. KG

- 6.4.10 Horsch Maschinen GmbH (HORSCH PIRK Forestry GmbH)

- 6.4.11 Mahindra & Mahindra Ltd.

- 6.4.12 Pottinger Landtechnik GmbH

- 6.4.13 Tractors and Farm Equipment Limited (TAFE)

7 Market Opportunities and Future Outlook

除草机器人市场:按组件、类型、运作方式、销售管道、应用和最终用途划分-2026-2032年全球市场预测农作物残渣处理机械市场:按类型、机械化程度、动力来源、应用、最终用途和分销管道划分-2026-2032年全球市场预测

除草机器人市场:按组件、类型、运作方式、销售管道、应用和最终用途划分-2026-2032年全球市场预测农作物残渣处理机械市场:按类型、机械化程度、动力来源、应用、最终用途和分销管道划分-2026-2032年全球市场预测 2026年全球自主作物残茬管理机器人市场报告农业橡胶履带市场:2026-2032年全球市场预测(依应用程式、销售管道、履带宽度、橡胶配方类型、履带长度及最终用户类型划分)

2026年全球自主作物残茬管理机器人市场报告农业橡胶履带市场:2026-2032年全球市场预测(依应用程式、销售管道、履带宽度、橡胶配方类型、履带长度及最终用户类型划分) 自主农业车辆市场:策略性洞察与预测(2026-2031年)全球农业机械市场规模、份额、趋势和成长分析报告(2026-2034年)溶离设备市场:2026-2032年全球市场预测(依设备类型、自动化程度、技术、应用、最终用户及销售管道)农业和施工机械市场:按产品类型、功率范围、发动机类型、应用、最终用户和分销管道划分——2026-2032年全球预测谷物螺旋输送机市场:按类型、动力来源、容量、应用、最终用户和分销管道划分-2026-2032年全球预测红外线沥青加热器市场:按产品类型、电源、移动性、应用、最终用户、分销管道划分,全球预测(2026-2032年)

自主农业车辆市场:策略性洞察与预测(2026-2031年)全球农业机械市场规模、份额、趋势和成长分析报告(2026-2034年)溶离设备市场:2026-2032年全球市场预测(依设备类型、自动化程度、技术、应用、最终用户及销售管道)农业和施工机械市场:按产品类型、功率范围、发动机类型、应用、最终用户和分销管道划分——2026-2032年全球预测谷物螺旋输送机市场:按类型、动力来源、容量、应用、最终用户和分销管道划分-2026-2032年全球预测红外线沥青加热器市场:按产品类型、电源、移动性、应用、最终用户、分销管道划分,全球预测(2026-2032年)