|

市场调查报告书

商品编码

1906966

燃油添加剂:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Fuel Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

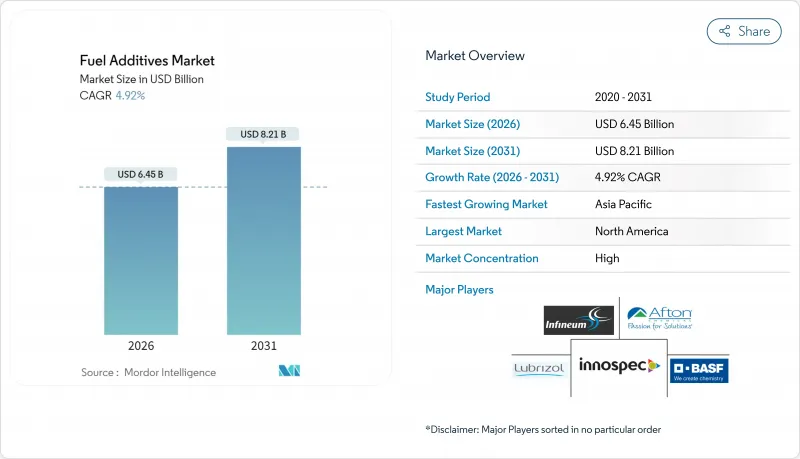

预计燃油添加剂市场将从 2025 年的 61.5 亿美元成长到 2026 年的 64.5 亿美元,到 2031 年将达到 82.1 亿美元,2026 年至 2031 年的复合年增长率为 4.92%。

全球排放法规日益严格,刺激了对燃油添加剂的需求,而电池式电动车的普及预计将导致燃油消费量的长期下降。喷射机燃料的持续需求,以及新兴国家超低硫柴油(ULSD)的引入,支撑了燃油添加剂市场的上升趋势。航空业的復苏、生质柴油强制掺混比例的提高以及重质和低品质原油炼製技术的进步,都在推动产品不断创新。随着供应商转向多功能、生质燃料相容型产品,并整合原料采购以应对成本压力,市场竞争日益激烈。

全球燃油添加剂市场趋势与洞察

严格执行环境法规

随着全球监管日益严格,燃料生产商面临更复杂的合规要求,添加剂的消费格局正在重塑。美国可再生燃料标准 (RFS) 强制规定了乙醇和生质柴油混合燃料的添加剂要求,而欧盟的欧7排放气体标准则要求更高的清洁性能,以在更长的换油週期内保持后处理效率。儘管加州计划在2035年逐步淘汰内燃机,但其「先进清洁汽车II (ACCII)」框架仍在推动对优质汽油添加剂的短期需求,以控制排放和粒状物排放。国际海事组织 (IMO) 2020 年的硫排放法规也对陆基柴油燃料市场产生了影响,进一步扩大了多功能添加剂包的潜在市场。诸如 ISO 8217 和 ASTM D975 等正式的测试通讯协定促使业务流向拥有认证测试实验室的供应商,从而提高了新进入者的进入门槛。

原油品质劣化加剧了沉淀物问题。

重质原油(污染性较强)在炼油厂原料混合物中的占比越来越大,增加了储存和燃烧循环过程中沉积物形成的风险。页岩气衍生的石蜡基原油会促进蜡沉积,而加拿大油砂原料则会在长途运输过程中加剧腐蚀和氧化压力。这些趋势推动了对沉积物抑制剂、抗氧化剂和防腐蚀添加剂的需求,这些添加剂能够在严苛的热负荷和化学负荷下保持燃料的完整性。在中东,寻求销售柔软性的重质原料处理炼油厂也面临类似的挑战。随着炼油厂寻求从低品质原料中获取经济价值,集清洁、金属惰性和稳定功能于一体的添加剂组合正日益受到欢迎。

电动车的激增

电动出行正在重塑能源格局。到2024年,中国的电动车渗透率将超过45%,国际能源总署(IEA)预测,到2030年,电动车将占全球轻型车销量的60%。随着汽油和柴油消费量达到峰值,道路运输添加剂的需求正面临结构性阻力。重型车辆的电气化将加剧这种影响,尤其对柴油添加剂供应商而言。然而,航空、船舶和非道路领域仍保持韧性,供应商正将研发和资金集中投入这些高价值领域,同时也在探索氨和氢载体等替代燃料的添加剂。

细分市场分析

到2025年,积碳控制添加剂将占据燃油添加剂市场28.78%的份额,巩固其作为现代燃油品管系统基石的地位。它们能够确保进气阀和喷油器清洁,满足美国环保署第三阶段排放标准(EPA Tier 3)和欧洲标准EN 228汽油标准的要求,从而保护燃烧效率和排气系统耐久性。缸内喷油引擎的日益普及也推动了这个细分市场的发展,因为这类引擎更容易产生气门积碳。同样重要的是,高压柴油喷射系统也需要清洁剂来防止喷嘴结焦。

预计到2031年,低温流动改良剂将成为所有产品类别中成长最快的,复合年增长率将达到5.43%,这主要得益于生物柴油掺混比例的扩大以及加拿大、北欧和中国东北地区对冬季运作日益增长的需求。随着这些法规的不断完善,流动点降低剂技术正受到越来越多的关注,以解决生质柴油的浊点和倾点过高的问题。随着商用车辆向更高效的引擎转型,对十六烷改良剂的需求也在不断增长,这些引擎需要可靠的冷启动性能和更短的点火延迟。多功能组合药物因其能够降低炼油厂和下游燃料经销商添加剂配比的复杂性而日益普及,使他们能够将性能目标整合到单一产品单元(SKU)中。

燃油添加剂、腐蚀抑制剂、低温流动十六烷改良剂、防腐蚀添加剂及其他产品类型)、应用领域(柴油、汽油、喷射机燃料及其他应用领域)和地区(亚太地区、北美地区、欧洲地区、南美地区以及中东和非洲地区)进行细分。市场预测以以金额为准和销售两种形式呈现。

区域分析

截至2025年,北美占据了燃油添加剂市场35.55%的份额。长期有效的美国环保署(EPA)法规和成熟的炼油厂支撑了稳定的需求,而加拿大严酷的冬季气候则推动了对低温流动改进剂的需求。在「顶级汽油」(TOP TIER)零售计画的推动下,汽油清洁剂的需求仍然强劲,该计画要求更高的沉积物控制水平以保持引擎清洁。

预计亚太地区将成为成长最快的地区,到2031年复合年增长率将达到5.48%。随着炼油厂升级其加氢脱硫装置,中国国六和印度国六标准的实施正在加速对润滑性添加剂和十六烷改良剂的需求。快速的都市化正在扩大商用车辆保有量,搭乘用电动车(EV)的日益普及也增加了柴油添加剂的消费量。东南亚国家超低硫柴油(ULSD)和E10汽油的日益普及,也催生了对多种产品的需求,包括生物柴油稳定剂、抗氧化剂和润滑性促进剂。

在欧洲,随着积极的脱碳目标推动产品结构向生质燃料相容型添加剂转变,绝对成长将保持温和但稳健。欧盟航空和海运硫排放法规将创造对利润丰厚的特殊添加剂的需求,从而抵消道路燃料需求的下降。在中东和非洲,沙乌地阿拉伯和奈及利亚炼油厂的扩建将扩大该地区的成品燃料供应,并增加符合出口标准的添加剂的进口。在巴西乙醇计画的推动下,南美洲对高混合汽油等级的抗氧化剂和腐蚀抑制剂的需求将继续保持强劲。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 严格执行环境法规

- 原油品质劣化会导致沉淀物问题加剧。

- 新兴经济体严格的超低硫柴油(ULSD)标准

- 全球航空运输量和喷射机燃料需求不断增长

- 生质燃料相容添加剂化学品(E10-E85)

- 市场限制

- 电池式电动车越来越受欢迎

- 多功能添加剂包的高昂研发成本

- 禁止使用含金属添加剂(例如,限制使用蒙脱石)

- 价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模及成长预测(以金额为准/数量)

- 依产品类型

- 泥沙控制

- 十六烷改良剂

- 润滑添加剂

- 抗氧化剂

- 防腐蚀

- 低温流动改善剂

- 抗爆剂

- 其他产品类型

- 透过使用

- 柴油引擎

- 汽油

- 喷射机燃料

- 其他用途

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- AFTON CHEMICAL

- Baker Hughes Company

- BASF

- Cargill Incorporated

- Chevron Corporation

- Clariant

- Dorf Ketal Chemicals

- Evonik Industries AG

- Exxon Mobil Corporation

- Infineum International Limited

- Innospec

- Lanxess

- The Lubrizol Corporation

- TotalEnergies

第七章 市场机会与未来展望

The Fuel Additives market is expected to grow from USD 6.15 billion in 2025 to USD 6.45 billion in 2026 and is forecast to reach USD 8.21 billion by 2031 at 4.92% CAGR over 2026-2031.

The outlook balances tightening global emission rules that stimulate additive demand against the long-run decline in fuel consumption tied to battery-electric vehicle adoption. Sustained jet-fuel needs, coupled with emerging-economy rollouts of ultra-low sulfur diesel (ULSD), keep the fuel additives market on an upward trajectory. Aviation recovery, expanding biodiesel mandates, and the refinement of heavy, lower-quality crudes collectively underpin steady product innovation. Competitive intensity has risen as suppliers pivot to multifunctional, biofuel-ready packages while securing raw-material integration to offset cost pressures.

Global Fuel Additives Market Trends and Insights

Enactment of Stringent Environmental Regulations

Global regulatory tightening is reshaping additive consumption as fuel producers align with more complex compliance layers. The U.S. Renewable Fuel Standard embeds additive requirements for ethanol and biodiesel blending, while Euro 7 emission rules in the European Union call for higher detergency to preserve after-treatment efficiency across longer drain intervals. California's Advanced Clean Cars II framework, despite its 2035 internal-combustion phase-out target, lifts near-term demand for premium gasoline additives that curb evaporative and particulate emissions. Maritime sulfur caps under IMO 2020 have spilled into land-based diesel pools, further widening the addressable market for multifunctional packages. Formal test protocols such as ISO 8217 and ASTM D975 channel business toward suppliers that operate accredited laboratories, tightening the qualification bar for new entrants.

Degrading Crude-Oil Quality Raising Deposit Issues

Heavier, higher-contaminant opportunity crudes now fill a larger slice of refinery slates, escalating deposit formation risks throughout storage and combustion cycles. Shale-derived paraffinic crudes elevate wax precipitation, while Canadian oil-sands feedstocks heighten corrosion and oxidation stress during long-haul transport. These dynamics bolster demand for deposit control, antioxidant, and anticorrosion additives that maintain fuel integrity under harsher thermal and chemical loads. In the Middle East, refineries running heavier feed face similar issues as they chase merchandising flexibility. As refiners squeeze economics from lower-grade inputs, additive packages that combine detergency, metal-deactivating, and stabilization functions gain favor.

Surging Adoption of Battery-Electric Vehicles

Electric mobility is redrawing the energy map. China surpassed 45% EV penetration in 2024, and the International Energy Agency sees EVs reaching 60% of global light-duty sales by 2030. As gasoline and diesel consumption peaks, additive volumes linked to road transport face a structural headwind. Heavy-duty fleet electrification compounds the effect, especially for diesel additive vendors. Nevertheless, aviation, marine, and off-road segments remain insulated, prompting suppliers to concentrate research and development and capital around these higher-value niches while exploring additives for alternative fuels such as ammonia and hydrogen carriers.

Other drivers and restraints analyzed in the detailed report include:

- Tight ULSD Specifications in Emerging Economies

- Rising Global Aviation Traffic and Jet-Fuel Demand

- High Research and Development Cost for Multi-Functional Additive Packages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Deposit control additives commanded 28.78% of the fuel additives market share in 2025, cementing their role as the cornerstone of modern fuel quality regimes. They ensure intake-valve and injector cleanliness demanded by EPA Tier 3 and EN 228 gasoline standards, safeguarding combustion efficiency and emission-system longevity. The segment benefits from the proliferation of gasoline direct-injection engines, which are more prone to valve deposits. Equally important, high-pressure diesel injection systems demand detergents to prevent nozzle coking.

Cold flow improvers register a 5.43% CAGR to 2031, the fastest within the product spectrum, as biodiesel blending widens and winter operability becomes mission-critical in Canada, Northern Europe, and Northeast China. As these mandates scale, pour-point depressant technologies that manage biodiesel's higher cloud and pour points gain traction. Cetane improvers follow as commercial fleets upgrade to higher-efficiency engines requiring reliable cold starts and reduced ignition delay. Multifunctional formulations are gaining favor because they reduce treat-rate complexity for refiners and downstream fuel marketers, consolidating performance goals into one SKU.

The Fuel Additives Report is Segmented by Product Type (Deposit Control, Cetane Improvers, Lubricity Additives, Antioxidants, Anticorrosion, Cold Flow Improvers, Antiknock Agents, and Other Product Types), Application (Diesel, Gasoline, Jet Fuel, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value and Volume.

Geography Analysis

North America accounted for 35.55% of the fuel additives market share in 2025. Long-standing EPA rules and mature refining assets foster dependable volume, while extreme winter conditions in Canada stimulate cold flow improver uptake. Gasoline detergent demand remains buoyant under the TOP TIER retail program, which mandates higher deposit-control levels to maintain engine cleanliness.

Asia-Pacific is the fastest-growing region, charting a 5.48% CAGR to 2031. China's enforcement of National VI and India's BS-VI standards accelerates lubricity and cetane additive demand as refineries update hydrodesulfurization units. Rapid urbanization expands commercial vehicle fleets, boosting diesel additive consumption even as passenger EV adoption rises. Southeast Asian economies pursue ULSD and E10 gasoline rollouts, creating multi-product pull across biodiesel stabilizers, antioxidants, and lubricity improvers.

Europe shows steady but lower absolute growth, underpinned by aggressive decarbonization goals that shift the product mix toward biofuel-compatible additives. ReFuelEU Aviation and maritime sulfur caps generate high-margin specialty demand, offsetting declining road-fuel volumes. In the Middle East and Africa, expanding refinery complexes in Saudi Arabia and Nigeria widen regional availability of finished fuels, drawing additive imports to hit export-grade specifications. South America, led by Brazil's ethanol program, sustains robust antioxidant and corrosion-inhibitor demand for high-blend gasoline grades.

- AFTON CHEMICAL

- Baker Hughes Company

- BASF

- Cargill Incorporated

- Chevron Corporation

- Clariant

- Dorf Ketal Chemicals

- Evonik Industries AG

- Exxon Mobil Corporation

- Infineum International Limited

- Innospec

- Lanxess

- The Lubrizol Corporation

- TotalEnergies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Enactment of stringent environmental regulations

- 4.2.2 Degrading crude-oil quality raising deposit issues

- 4.2.3 Tight ULSD specifications in emerging economies

- 4.2.4 Rising global aviation traffic and jet-fuel demand

- 4.2.5 Biofuel-compatible additive chemistries (E10-E85)

- 4.3 Market Restraints

- 4.3.1 Surging adoption of battery-electric vehicles

- 4.3.2 High research and development cost for multi-functional additive packages

- 4.3.3 Metal-containing additive bans (e.g., MMT limits)

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Product Type

- 5.1.1 Deposit Control

- 5.1.2 Cetane Improvers

- 5.1.3 Lubricity Additives

- 5.1.4 Antioxidants

- 5.1.5 Anticorrosion

- 5.1.6 Cold Flow Improvers

- 5.1.7 Antiknock Agents

- 5.1.8 Other Product Types

- 5.2 By Application

- 5.2.1 Diesel

- 5.2.2 Gasoline

- 5.2.3 Jet Fuel

- 5.2.4 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 AFTON CHEMICAL

- 6.4.2 Baker Hughes Company

- 6.4.3 BASF

- 6.4.4 Cargill Incorporated

- 6.4.5 Chevron Corporation

- 6.4.6 Clariant

- 6.4.7 Dorf Ketal Chemicals

- 6.4.8 Evonik Industries AG

- 6.4.9 Exxon Mobil Corporation

- 6.4.10 Infineum International Limited

- 6.4.11 Innospec

- 6.4.12 Lanxess

- 6.4.13 The Lubrizol Corporation

- 6.4.14 TotalEnergies

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment

售后燃油添加剂市场:2026-2032年全球市场预测(按产品类型、车辆类型、包装、应用和分销管道划分)

售后燃油添加剂市场:2026-2032年全球市场预测(按产品类型、车辆类型、包装、应用和分销管道划分) 2034年再生燃料添加剂市场预测:按添加剂类型、燃料类型、应用和地区分類的全球分析柴油引擎油添加剂市场:依添加剂类型、化学成分、通路和应用划分-2026-2032年全球预测

2034年再生燃料添加剂市场预测:按添加剂类型、燃料类型、应用和地区分類的全球分析柴油引擎油添加剂市场:依添加剂类型、化学成分、通路和应用划分-2026-2032年全球预测 燃油添加剂市场-全球产业规模、份额、趋势、机会及按类型、应用、地区和竞争格局分類的预测(2021-2031年)

燃油添加剂市场-全球产业规模、份额、趋势、机会及按类型、应用、地区和竞争格局分類的预测(2021-2031年) 北美燃油添加剂:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)

北美燃油添加剂:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年) 冷流改进剂市场规模、份额及成长分析(依产品类型、配方、应用类型、最终用途产业及地区划分)-2026-2033年产业预测

冷流改进剂市场规模、份额及成长分析(依产品类型、配方、应用类型、最终用途产业及地区划分)-2026-2033年产业预测 燃油添加剂市场规模、份额和成长分析(按类型、应用和地区划分)—2026-2033年产业预测

燃油添加剂市场规模、份额和成长分析(按类型、应用和地区划分)—2026-2033年产业预测 柴油市场:按类型、应用和地区划分

柴油市场:按类型、应用和地区划分 燃料添加剂市场:未来预测(2025-2030)

燃料添加剂市场:未来预测(2025-2030) 全球燃料添加剂市场:按类型和应用分类 - 预测(截至 2029 年)

全球燃料添加剂市场:按类型和应用分类 - 预测(截至 2029 年)