|

市场调查报告书

商品编码

1907280

神经型态晶片:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Neuromorphic Chip - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

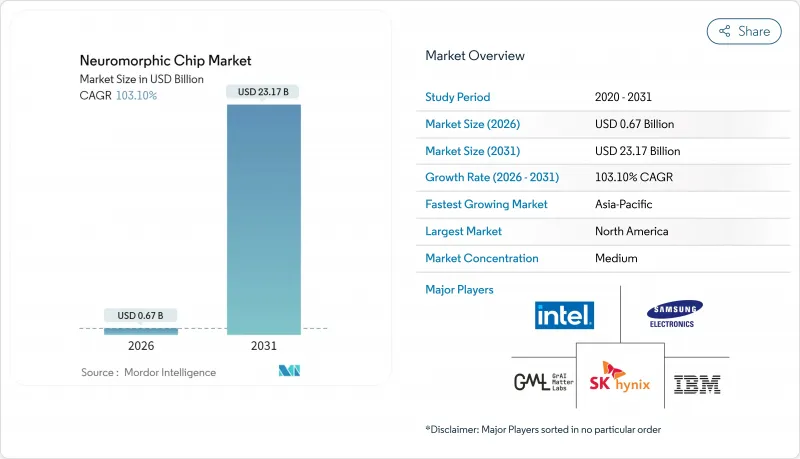

预计到 2025 年,神经型态晶片市场价值将达到 3.3 亿美元,到 2031 年将达到 231.7 亿美元,高于 2026 年的 6.7 亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 103.1%。

随着类脑处理器突破冯诺依曼瓶颈,实现极高的能源效率并支援网路边缘的即时决策,神经型态晶片市场正迅速扩张。智慧型手机和汽车中的边缘人工智慧、不断上涨的资料中心电力成本以及政府对类脑研发投入的增加,共同构成了一个良性循环,持续吸引资金和人才流入新产品开发领域。虽然汽车高级驾驶辅助系统(ADAS)目前占据最大的商业性需求,但医疗、工业IoT和航太应用正在进一步拓展市场需求。由于类比、数位或混合讯号架构尚未形成事实上的标准,各厂商透过专有的储存技术、软体堆迭和特定领域的最佳化来凸显自身优势,因此市场竞争依然激烈。

全球神经型态晶片市场趋势与洞察

消费和汽车领域对边缘人工智慧的需求不断增长

搭载高通骁龙8 Gen 3处理器的智慧型手机可提供45 TOPS的装置端运算效能,彻底消除云端延迟。这项技术为车载感知系统类似架构的开发铺平了道路。汽车製造商正在采用神经形态处理器来满足毫秒级响应目标和严格的散热设计要求,而这一转变正使ADAS(高级驾驶辅助系统)运行期间的电池消耗降低两位数。

资料中心能源危机推动超低功耗运算

2023年,全球资料中心将消耗176兆瓦时(TWh)的电力,而人工智慧推理工作负载预计到2028年将使这项需求翻倍。 IBM的NorthPole晶片证明,与GPU相比,神经形态硬体在保持相似精确度的同时,可以达到25倍的节能效果。超大规模资料中心业者目前正在试验混合机架,将Loihi 2丛集与传统加速器结合,以协助控制不断飙升的电力成本。

软体和工具链生态系尚不成熟

开发人员被迫同时使用 Nengo、Lava 和 MetaTF 等编译器,而缺乏所有硬体平台的统一编译器导致计划进度和整合成本大幅增加。企业 IT 团队对采用 CUDA 等标准持谨慎态度,这抑制了短期采购热情。

细分市场分析

儘管混合讯号装置体积小巧,但预计它们将成为神经型态晶片市场的主要成长引擎,复合成长率高达105.2%。类比-数位混合拓朴结构比纯数位逻辑更能自然捕捉突触的连续动态特性,同时利用CMOS製程来实现可扩展性。预计到2025年,数位晶片仍将占据神经型态晶片市场43.62%的份额,这主要得益于成熟的EDA支援和便利的软体移植性。虽然用于数位产品的神经型态晶片市场规模预计将会扩大,但由于混合讯号技术的兴起,其相对重要性预计将会下降。三星等厂商正在致力于将混合讯号技术应用于行动AI推理,而Start-Ups则在改进用于微瓦级感测器节点的类比模组。投资重点集中在製程相容的电阻式储存阵列上,这种阵列可以减少突触的体积和刷新开销。

混合讯号技术的强劲发展势头源于其能够以低于100毫瓦的功耗提供即时边缘智能,从而推动自主无人机、智慧耳机和植入式医疗设备的普及。一款于2025年发布的碳基三元逻辑原型展示了材料创新将如何进一步降低面积和能耗。数位技术厂商正透过片上SRAM整合来降低资料传输延迟,但类比技术的动态范围和局部优势仍需迎头赶上。随着晶圆代工厂不断改进製程配方,混合讯号技术的产量比率挑战将有所缓解,并有望在2031年之前削弱数位科技的统治地位。

由于脉衝神经网路具有软体亲和性,预计到2025年,其收入将占36.35%。同时,ReRAM交叉阵列将在神经型态晶片市场维持最快的成长速度,复合年增长率高达104.8%。交叉阵列将多位元权重储存在记忆体中,融合了运算和储存功能,从而最大限度地减少资料传输。概念验证系统在功耗仅为个位数毫瓦的情况下,实现了94.6%的MNIST准确率。虽然与脉衝神经元相关的神经型态晶片的市场规模将继续增长,但随着电阻式装置尺寸的缩小,其市场份额将会下降。相变记忆体将在对寿命要求极高的工作负载中发挥辅助作用。

这种架构转变也标誌着设计理念正从以神经元为中心转变为以记忆体为中心。 DenRAM 图将时间动态直接编码到电阻状态中,进而提升序列学习能力。然而,脉衝神经网路在稀疏事件处理方面仍然具有优势,使其在视觉感测器和雷达领域极具吸引力。产业蓝图越来越多地采用异质晶片提案,将这些范式整合到单一中介层上,从而加速软体重用和系统整合。

区域分析

2025年,北美在神经型态晶片市场将维持34.85%的份额,这得益于DARPA的资助以及英特尔拥有11.5亿个神经元的Hala Point平台。该地区产学研合作蓬勃发展,麻省理工学院的整合光子处理器能够在亚纳秒内完成神经运算,准确率超过92%,预示未来有望衍生出商业化产品。加拿大Nengo Software等公司的工具开发技术正在推动整个生态系统的成熟,并吸引创业投资涌入硅谷新兴企业。

儘管亚太地区绝对规模较小,但却是神经型态晶片市场成长最快的地区,预计到2031年将以104.7%的复合年增长率成长。中国的达尔文猴系统由960个达尔文3晶片组成,包含20亿个神经元,展现了中国在人工智慧硬体领域实现战略自主的决心。韩国正透过与欧盟500万欧元的伙伴关係来推进自旋电子半导体的发展,而日本的一个财团则将相变记忆体与边缘摄影机结合,以推进工厂自动化。印度的国家光子晶片计画和新加坡的神经形态机器人研究所完善了该地区多元化的研发版图。

欧洲仍然是重要的第二大研发中心,利用「地平线」计画的资金大力投资电阻式记忆体和事件驱动视觉研究。德国汽车製造商主导ADAS试点项目,整合脉衝神经网路协处理器,并利用本地一级供应商提供汽车级封装。瑞士公司SynSense正向欧洲无人机OEM厂商供应功耗低于1毫瓦的DSP模组,凸显了跨国供应链的综效。监管机构在隐私和永续性的领导地位正在影响全球设计目标,鼓励晶片製造商实施透明的功耗报告和设备端资料保存。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 消费和汽车领域对边缘人工智慧的需求不断增长

- 资料中心能源危机推动超低功耗运算

- 政府主导脑研究与发展计划

- 事件驱动型感测器和SoC整合浪潮

- 对卫星搭载式人工智慧处理的需求

- OT网路安全异常检测要求

- 市场限制

- 软体和工具链生态系尚不成熟

- 模拟非挥发性记忆体(NVM)的製造差异

- 缺乏尖峰系统测试和检验标准

- 医疗设备监管的路径尚不明朗。

- 产业价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 神经型态晶片的新应用案例

- 宏观经济趋势如何影响市场

- 投资分析

第五章 市场规模与成长预测

- 按晶片类型

- 模拟

- 数位的

- 混合讯号

- 建筑设计

- 脉衝神经网路

- 基于ReRAM的架构

- 相变记忆体架构

- 按最终用户行业划分

- 汽车(ADAS/AV)

- 工业IoT和机器人技术

- 家用电子电器

- 金融服务及网路安全

- 医疗和医疗设备

- 航太/国防

- 按部署模式

- 边缘设备

- 资料中心/云

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 亚太其他地区

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东地区

- 非洲

- 南非

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Intel Corporation

- International Business Machines Corporation

- Samsung Electronics Co., Ltd.

- SK hynix Inc.

- BrainChip Holdings Ltd

- SynSense AG

- GrAI Matter Labs SAS

- Nepes Corporation

- Qualcomm Technologies, Inc.

- Micron Technology, Inc.

- Synaptics Incorporated

- Innatera Nanosystems BV

- Prophesee SA

- MemryX Inc.

- Mythic Inc.

- Syntiant Corp.

- Gyrfalcon Technology Inc.

- Applied Brain Research Inc.

- General Vision Inc.

- Vicarious Corp.

第七章 市场机会与未来展望

The neuromorphic chip market was valued at USD 0.33 billion in 2025 and estimated to grow from USD 0.67 billion in 2026 to reach USD 23.17 billion by 2031, at a CAGR of 103.1% during the forecast period (2026-2031).

The neuromorphic chip market is accelerating because brain-inspired processors overcome the von Neumann bottleneck, unlock extreme energy efficiency, and enable real-time decision-making at the network edge. Edge artificial intelligence in smartphones and vehicles, mounting data-center electricity costs, and rising government funding for brain-inspired R&D collectively create a flywheel that keeps capital and talent flowing into new product launches. Automotive advanced driver-assistance systems (ADAS) currently absorb the largest commercial volumes, while healthcare, industrial IoT, and aerospace applications provide additional demand diversity. Competition remains intense because no single architecture, analog, digital, or mixed-signal, has emerged as a de facto standard, pushing vendors to differentiate through proprietary memory technologies, software stacks, and domain-specific optimizations.

Global Neuromorphic Chip Market Trends and Insights

Rising Edge-AI Demand in Consumer and Automotive

Smartphones built on Qualcomm's Snapdragon 8 Gen 3 now perform 45 TOPS on-device, eliminating cloud latency and inspiring similar architectures for in-car perception systems. Automotive OEMs adopt neuromorphic processors to meet millisecond response targets and stringent thermal envelopes, a shift that lowers battery drain by double-digit margins during ADAS operation.

Data-Center Energy Crisis Favoring Ultra-Low-Power Compute

Global data centers consumed 176 TWh in 2023, and AI inference workloads threaten to double electricity demand by 2028. IBM's NorthPole chip proves neuromorphic hardware can deliver 25-fold energy savings over GPUs while sustaining similar accuracy. Hyperscalers now pilot hybrid racks that pair Loihi 2 clusters with conventional accelerators to curb spiraling utility bills.

Immature Software and Toolchain Ecosystem

Developers juggle Nengo, Lava, and MetaTF because no unified compiler spans every hardware platform, inflating project timelines and integration costs. Enterprise IT teams hesitate until a CUDA-like standard emerges, dampening short-term procurement.

Other drivers and restraints analyzed in the detailed report include:

- Government Brain-Inspired R&D Programs

- Event-Driven Sensor-SoC Integration Wave

- Fabrication Variability of Analog NVM

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mixed-signal devices, though representing a smaller base, will compound at 105.2% to become the principal growth engine for the neuromorphic chip market. Their hybrid analog-digital topology captures continuous synaptic dynamics more naturally than purely digital logic, yet still leverages CMOS toolflows for scale. Digital chips preserved a 43.62% neuromorphic chip market share in 2025, owing to mature EDA support and easier software portability. The neuromorphic chip market size allocated to digital products is projected to expand, but its relative weight will slip as mixed-signal gains traction. Vendors such as Samsung pursue mixed-signal for mobile AI inference, while start-ups refine analog blocks for micro-watt sensor nodes. Investment gravitates toward process-compatible resistive memory arrays that shrink synapse footprints and cut refresh overhead.

Mixed-signal's momentum reflects its capacity to deliver real-time edge intelligence at sub-100 mW levels, enabling autonomous drones, smart ear buds, and implantable medical devices. Carbon-based ternary logic prototypes unveiled in 2025 illustrate how material innovation could further compress area and energy envelopes. Digital incumbents respond by integrating on-chip SRAM to reduce data shuttling penalties, yet must match analog's dynamic range and locality advantages. As foundries refine process recipes, mixed-signal yield headwinds will abate, positioning the category to erode digital's dominance through 2031.

Spiking neural networks commanded 36.35% of 2025 revenue thanks to software familiarity, but ReRAM crossbars are on track for a 104.8% CAGR, the fastest within the neuromorphic chip market. Crossbar arrays store multi-bit weights in-memory, fusing compute and storage to minimize data movement. Proof-of-concept systems achieved 94.6% MNIST accuracy while consuming single-digit milliwatts. The neuromorphic chip market size tied to spiking neurons will still expand in absolute terms, though its share slides as resistive devices scale. Phase-change memory holds a supporting role for endurance-critical workloads.

The architecture shift also signals a broader move from neuron-centric to memory-centric design; DenRAM diagrams encode temporal dynamics directly in resistive states, improving sequence learning. Spiking networks, however, retain an edge in sparse event processing, keeping them attractive for vision sensors and radar. Industry roadmaps increasingly propose heterogeneous chips that combine these paradigms on a single interposer, accelerating software reuse and system integration.

The Neuromorphic Chip Market Report is Segmented by Chip Type (Analog, Digital, Mixed-Signal), Architecture (Spiking Neural Network, ReRAM-Based Architectures, and More), End-User Industry (Automotive, Industrial IoT & Robotics, and More), Deployment Model (Edge Devices, Data-centre/Cloud), and Geography (North America, South America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America preserved 34.85% neuromorphic chip market share in 2025 on the back of DARPA funding and Intel's 1.15 billion-neuron Hala Point platform. The region hosts robust academic-industry linkages; MIT's integrated photonic processor completed neural computations in sub-nanosecond intervals while retaining more than 92% accuracy, signaling future spin-outs into commercial stacks. Canadian tooling expertise, highlighted by Nengo software, further entrenches the ecosystem's maturity and draws venture capital to Silicon Valley start-ups.

Asia-Pacific, though smaller in absolute terms, is the neuromorphic chip market's fastest-growing territory with a forecast 104.7% CAGR to 2031. China's Darwin Monkey system offers 2 billion neurons across 960 Darwin 3 chips, demonstrating the state's commitment to strategic autonomy in AI hardware. South Korea's EUR 5 million EU partnership advances spintronic semiconductors, while Japanese consortia pair phase-change memory with edge cameras for factory automation. India's national photonic-chip initiative and Singapore's neuromorphic robotics labs round out the region's diversified R&D map.

Europe remains a pivotal secondary hub, channeling Horizon funds into resistive memory and event-driven vision research. German automakers spearhead ADAS pilots that integrate Spiking Neural Network coprocessors, leveraging local tier-ones for vehicle-grade packaging. Swiss firm SynSense supplies sub-1 mW DSP blocks to European drone OEMs, underscoring cross-border supply-chain synergies. Regulatory leadership in privacy and sustainability influences global design targets, nudging chipmakers toward transparent power reporting and on-device data retention.

- Intel Corporation

- International Business Machines Corporation

- Samsung Electronics Co., Ltd.

- SK hynix Inc.

- BrainChip Holdings Ltd

- SynSense AG

- GrAI Matter Labs SAS

- Nepes Corporation

- Qualcomm Technologies, Inc.

- Micron Technology, Inc.

- Synaptics Incorporated

- Innatera Nanosystems BV

- Prophesee SA

- MemryX Inc.

- Mythic Inc.

- Syntiant Corp.

- Gyrfalcon Technology Inc.

- Applied Brain Research Inc.

- General Vision Inc.

- Vicarious Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising edge-AI demand in consumer and automotive

- 4.2.2 Data-center energy crisis favouring ultra-low-power compute

- 4.2.3 Government brain-inspired R&D programmes

- 4.2.4 Event-driven sensor-SoC integration wave

- 4.2.5 On-board satellite AI processing need

- 4.2.6 OT-cybersecurity anomaly detection requirements

- 4.3 Market Restraints

- 4.3.1 Immature software and toolchain ecosystem

- 4.3.2 Fabrication variability of analog NVM

- 4.3.3 Lack of spike-system test/validation standards

- 4.3.4 Unclear medical-device regulatory path

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Emerging Use-Cases for Neuromorphic Chips

- 4.9 Impact of Macroeconomic Trends on the Market

- 4.10 Investment Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 By Chip Type

- 5.1.1 Analog

- 5.1.2 Digital

- 5.1.3 Mixed-Signal

- 5.2 By Architecture

- 5.2.1 Spiking Neural Network

- 5.2.2 ReRAM-based Architectures

- 5.2.3 Phase-Change-Memory Architectures

- 5.3 By End-User Industry

- 5.3.1 Automotive (ADAS / AV)

- 5.3.2 Industrial IoT and Robotics

- 5.3.3 Consumer Electronics

- 5.3.4 Financial Services and Cybersecurity

- 5.3.5 Healthcare and Medical Devices

- 5.3.6 Aerospace and Defense

- 5.4 By Deployment Model

- 5.4.1 Edge Devices

- 5.4.2 Data-centre / Cloud

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Intel Corporation

- 6.4.2 International Business Machines Corporation

- 6.4.3 Samsung Electronics Co., Ltd.

- 6.4.4 SK hynix Inc.

- 6.4.5 BrainChip Holdings Ltd

- 6.4.6 SynSense AG

- 6.4.7 GrAI Matter Labs SAS

- 6.4.8 Nepes Corporation

- 6.4.9 Qualcomm Technologies, Inc.

- 6.4.10 Micron Technology, Inc.

- 6.4.11 Synaptics Incorporated

- 6.4.12 Innatera Nanosystems BV

- 6.4.13 Prophesee SA

- 6.4.14 MemryX Inc.

- 6.4.15 Mythic Inc.

- 6.4.16 Syntiant Corp.

- 6.4.17 Gyrfalcon Technology Inc.

- 6.4.18 Applied Brain Research Inc.

- 6.4.19 General Vision Inc.

- 6.4.20 Vicarious Corp.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

神经形态半导体晶片市场分析及预测(至2035年):类型、产品、技术、组件、应用、材料类型、装置、最终用户、功能、安装模式

神经形态半导体晶片市场分析及预测(至2035年):类型、产品、技术、组件、应用、材料类型、装置、最终用户、功能、安装模式 全球神经形态晶片市场规模、份额、趋势和成长分析报告(2026-2034)

全球神经形态晶片市场规模、份额、趋势和成长分析报告(2026-2034) 日本神经形态晶片市场规模、份额、趋势及预测(依供应类型、应用、最终用户产业及地区划分,2026-2034年)

日本神经形态晶片市场规模、份额、趋势及预测(依供应类型、应用、最终用户产业及地区划分,2026-2034年) 2026年全球神经形态晶片市场报告神经形态晶片市场-2026-2031年预测

2026年全球神经形态晶片市场报告神经形态晶片市场-2026-2031年预测 用于自动驾驶汽车的神经形态晶片市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

用于自动驾驶汽车的神经形态晶片市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 神经形态晶片市场,按产品、应用、类型、最终用户、国家和地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测

神经形态晶片市场,按产品、应用、类型、最终用户、国家和地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测 拉丁美洲的神经型态晶片:市场占有率分析、行业趋势和成长预测(2025-2030)欧洲神经型态晶片:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)神经形态晶片市场、机会、成长动力、产业趋势分析与预测,2024-2032

拉丁美洲的神经型态晶片:市场占有率分析、行业趋势和成长预测(2025-2030)欧洲神经型态晶片:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)神经形态晶片市场、机会、成长动力、产业趋势分析与预测,2024-2032