|

市场调查报告书

商品编码

1910431

袋装包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Pouch Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

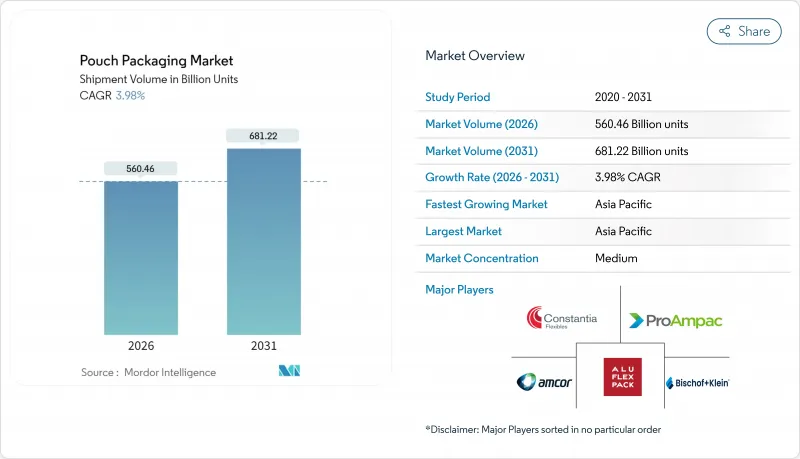

2025年,袋装包装市场价值为5,390.1亿美元,预计到2031年将达到6,812.2亿美元,而2026年为5,604.6亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 3.98%。

这种稳定成长的趋势表明,软包装市场正从早期快速成长阶段过渡到更为谨慎的扩张阶段,而电子商务物流、便利食品趋势以及更严格的永续性法规都为其提供了支撑。品牌所有者仍然倾向于选择软包装而非硬包装,因为软包装具有更高的材料利用率;监管机构也鼓励采用轻量化解决方案,以减少运输排放。技术投资目前优先考虑单一材料阻隔薄膜和可回收性,竞争优势也正从单纯的规模经济转向其他方面。

全球软包装市场趋势与洞察

对经济实惠的包装和品牌差异化的需求日益增长

消费品利润率面临的通膨压力不断增加,促使企业寻求既能减少材料用量又不影响货架陈列效果的包装形式。与同类硬质包装相比,软包装袋通常可减少70%的基材用量,并提供更大的印刷面积,从而实现高解析度影像。根据ProAmpac发布的2024年报告,可回收的软包装袋可为品牌所有者节省15-20%的材料成本。小型品牌正利用这些成本优势,实现与跨国公司相同的视觉衝击力,从而推动市场细分,并在价格敏感型品类中提升销售量。

便利食品和即食食品消费激增

都市化加快和家庭规模缩小导致人们对单份微波炉加热食品的依赖性增强,而这类食品非常适合软包装。根据美国农业部数据显示,中国二线城市的调理食品市场正以每年12%的速度成长,其中,能够均匀加热和排放蒸气的袋装包装占了越来越大的市场份额。像「Once Upon a Farm」这样的高端婴幼儿食品生产商,正利用吸嘴袋延长保质期并提供更优的功能,从而为其产品设定更高的价格。

日益严重的环境与回收问题

柔软性薄膜的回收基础设施远落后于宝特瓶和金属罐,这使得品牌商面临承担生产者延伸责任(EPR)成本的风险。据软包装协会称,美国仅有4%的柔软性薄膜以机械方式回收,迫使加工商投入资金资金筹措高成本的回收系统。同时,提案的PFAS禁令威胁到对食品安全至关重要的阻隔化学技术,造成不确定性,并减缓了对新生产线的资本投资。

细分市场分析

到2025年,塑胶仍将占据软包装市场60.72%的份额,这主要得益于聚乙烯和聚丙烯的低成本和易加工性。然而,随着监管机构发出讯号,未来废弃物处理解决方案的性价比将超越传统的成本绩效,生物基和可堆肥材料将稳定成长,年复合成长率将达到6.05%。领先的加工商正在将植物来源树脂与奈米纤维素基阻隔涂层相结合,以开发出在氧气阻隔性能方面可与EVOH媲美的产品。

软包装市场正青睐那些既能确保产品保护又能实现可回收性的单一材料创新。预计到2024年,结构简化相关的专利申请将成长40%,预示着材料科学领域的竞争将日益激烈。投资于相容剂和无溶剂复合技术的加工商已做好充分准备,能够在2030年截止日期前满足欧盟的回收标准。同时,在对氧气渗透要求极高的高端应用中,铝箔的使用量保持稳定,而对更薄壁材的需求仍在持续。

扁平袋仍占袋装包装市场36.33%的份额,反映出其在干货领域的广泛应用。然而,随着零售商重视在拥挤的货架上展示垂直标识,立式袋正以5.43%的复合年增长率加速成长。品牌商正利用风琴式底部和逼真的印刷技术,即使在零食坚果和宠物食品等质化品类中,也能传递高端价值。

功能性包装形式不断扩展:杀菌袋可用于生产常温保存的蒸馏食品,无菌复合技术瞄准饮料市场,条状包装则主导单份营养补充剂市场。从捲材到填充的一体化工作流程为大批量生产的单品提供了成本优势,而预製包装则适用于小批量生产。 Guarapac 在巴西提供的整合式复合-注塑-射出成型解决方案就是一个很好的例子,它展示了端到端控制如何降低故障率并加快产品上市速度。

区域分析

亚太地区预计到2025年将占据全球软包装市场39.54%的份额,并预计在2031年之前以6.74%的复合年增长率持续成长。中国市场需求的快速成长得益于其对包装食品的快速消费,而这又受到有组织零售业和严格的食品安全法规的推动。在印度,现代化分销网络的扩张正在推动销售成长;而在韩国,韩妆产业正将柔性化妆品包装出口到全球各地。区域性加工商正利用其接近性原生树脂供应商和具有成本优势的劳动力资源,强化其本地化的供应链,同时,跨国品牌所有者也在寻求包装规格的全球统一化。

北美市场的需求模式日趋成熟,优质化和电子商务成为主导。轻量化设计降低了以体积重量计价下的运输成本,促使零售商采用自有品牌袋。在欧洲,监管部门为提高可回收性而采取的措施加速了单一材料产品的推广,软包装在生命週期指标方面优于硬质玻璃和多层纸盒。斯堪地那维亚市场正在试行软包装薄膜押金制度,为欧盟范围内的推广提供数据支援。

南美洲、中东和整个非洲都蕴藏着新的成长潜力。巴西乳製品产业正在采用吸嘴袋包装酵母菌饮料,因为这种包装可以节省低温运输能源。波湾合作理事会(GCC)国家正在进口袋装蒸馏食品,这种包装能够适应沙漠地区的物流运输。非洲最大的城市则使用小袋包装经济实惠的必需品。儘管基础设施挑战依然存在,但人口成长动能和可支配收入的增加将逐步缩小与已开发地区的差距。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 对经济高效的包装和品牌差异化的需求日益增长

- 方便食品和即食食品的消费量激增

- 向永续性、轻巧、灵活的包装转型

- 加速电子商务和直接面向消费者的物流

- 工业散装应用中自吸袋的成长

- 创新研发出高阻隔单材料薄膜,使其可回收利用

- 市场限制

- 日益严重的环境与回收问题

- 塑胶树脂原料价格波动

- 来自新兴纤维基柔性包装材料的竞争

- 生物基高阻隔树脂的供应限制

- 产业价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 宏观经济因素如何影响市场

- 回收和永续性趋势

第五章 市场规模与成长预测

- 材料

- 塑胶

- 聚乙烯(PE)

- 聚丙烯(PP)

- 聚对苯二甲酸乙二醇酯(PET)

- 聚氯乙烯树脂(PVC)

- 其他塑料

- 纸

- 铝箔

- 可生物降解/可堆肥

- 塑胶

- 依产品类型

- 平型(枕形和侧边密封)

- 起来

- 喷口

- 蒸馏

- 无菌

- 条状包装/小袋

- 卷材/预製袋

- 封装类型

- 紧固件

- 壶嘴和盖子

- 蒂尔诺奇

- 滑桿

- 其他封装类型

- 按最终用户行业划分

- 食物

- 糖果和糖果甜点

- 冷冻食品

- 生鲜食品

- 乳製品

- 干货和谷物

- 肉类、家禽和水产品

- 宠物食品

- 其他食品(酱料、调味品、抹酱)

- 饮料

- 酒精饮料

- 不含酒精的饮料

- 医疗/製药

- 个人护理和化妆品

- 家居护理和家用产品

- 其他终端用户产业

- 食物

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 肯亚

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Amcor plc

- Mondi plc

- ProAmpac Intermediate, Inc.

- Constantia Flexibles Group GmbH

- Huhtamaki Oyj

- Sealed Air Corporation

- Sonoco Products Company

- Coveris Management GmbH

- Bischof+Klein SE and Co. KG

- FlexPak Services, LLC

- Goglio SpA

- Scholle IPN Corporation

- Gualapack SpA

- Aluflexpack AG

- Flair Flexible Packaging Corporation

- Hood Packaging Corporation

- Toppan Printing Co., Ltd.

- Winpak Ltd.

- Glenroy, Inc.

第七章 市场机会与未来展望

The pouch packaging market was valued at USD 539.01 billion in 2025 and estimated to grow from USD 560.46 billion in 2026 to reach USD 681.22 billion by 2031, at a CAGR of 3.98% during the forecast period (2026-2031).

This steady trajectory underscores the pouch packaging market's transition from rapid early-stage growth to a more measured expansion supported by e-commerce logistics, convenience food trends, and tightening sustainability regulations. Brand owners continue to favor material-efficient flexible packs over rigid formats, while regulatory bodies endorse lightweight solutions that cut transport emissions. Technology investments now prioritize mono-material barrier films and recyclability compliance, shifting competitive advantage away from pure scale economics.

Global Pouch Packaging Market Trends and Insights

Rising Demand for Cost-Effective Packaging and Brand Differentiation

Inflationary pressure on consumer goods margins intensifies the search for packaging formats that cut material usage without compromising shelf appeal. Pouches typically use 70% less substrate than comparable rigid packs and provide a larger printable surface that supports high-resolution graphics. ProAmpac's 2024 report shows curbside-recyclable pouches delivering 15-20% material cost savings for brand owners. Smaller brands leverage these economics to match the visual impact of multinationals, fostering market fragmentation and stimulating additional unit volumes across price-sensitive categories.

Surge in Convenience and Ready-to-Eat Food Consumption

Rising urbanization and smaller household sizes translate into greater reliance on single-serve, microwave-ready meals best suited to flexible formats. USDA data indicates 12% annual growth in ready meals across China's tier-2 cities, with pouches gaining share due to uniform heating and steam venting capabilities. Premium baby-food players such as Once Upon a Farm capitalize on spouted pouches that extend shelf life and justify price premiums through superior functionality.

Escalating Environmental and Recycling Challenges

Flexible-film recycling infrastructure lags far behind that of PET bottles or metal cans, exposing brands to Extended Producer Responsibility fees. The Flexible Packaging Association notes only 4% of flexible films are mechanically recycled in the United States, leaving converters to fund costly take-back schemes. Meanwhile, proposed PFAS bans threaten barrier chemistries vital for food safety, creating uncertainty that slows capital spending on new lines.

Other drivers and restraints analyzed in the detailed report include:

- Sustainability-Driven Shift Toward Lightweight Flexible Packs

- Acceleration of E-Commerce and Direct-to-Consumer Logistics

- Volatility in Plastic-Resin Feedstock Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastics retained a 60.72% pouch packaging market share in 2025, anchored by the affordability and processability of polyethylene and polypropylene. Yet bio-based and compostable materials are gaining a 6.05% CAGR foothold as regulators signal a future where end-of-life solutions trump historic cost-performance ratios. Leading converters integrate plant-derived resins with barrier coatings based on nanofibrillated cellulose that rival EVOH in oxygen-blocking capacity.

The pouch packaging market rewards mono-material breakthroughs that ensure recyclability while maintaining product protection. Patent filings for simplified structures rose 40% in 2024, demonstrating a material-science arms race. Converters investing in compatibilizers and solvent-free lamination position themselves to meet EU recyclability quotas ahead of the 2030 deadline. Meanwhile, aluminum foil usage holds steady in premium applications that demand near-zero oxygen ingress, though downgauging efforts continue.

Flat formats still constitute 36.33% of the pouch packaging market size, reflecting entrenched applications in dry goods. Stand-up pouches, however, outpace at a 5.43% CAGR as retailers reward the vertical billboard effect on crowded shelves. Brands exploit gusseted bases and photo-realistic printing to signal premium value, even in commoditized categories such as snack nuts or pet treats.

Function-specific variants proliferate. Retort pouches enable shelf-stable ready meals, aseptic laminates chase beverage opportunities, and stick packs dominate single-serve nutraceuticals. Integrated rollstock-to-fill workflows deliver cost advantages for high-volume SKUs, whereas premade formats suit small batch runs. Gualapack's integrated laminate, injection, and filling solution in Brazil exemplifies how end-to-end control lowers failure rates while accelerating time to market.

The Pouch Packaging Market Report is Segmented by Material (Plastics, Paper, Aluminum Foil, Bio-degradable/Compostable), Product Type (Flat, Stand-Up, Spouted, Retort, Aseptic, Stick-Pack/Sachet, Rollstock/Premade Pouch), Closure Type (Zipper, Spout and Cap, and More), End-User Industry (Food, Beverage, Medical and Pharmaceutical, and More), and Geography. The Market Forecasts are Provided in Terms of Volume (Units).

Geography Analysis

Asia-Pacific led with 39.54% of the pouch packaging market share in 2025 and is forecast to record a 6.74% CAGR to 2031. China's rapid shift toward packaged foods, propelled by organized retail and stringent food-safety laws, keeps demand buoyant. India's modern trade expansion drives volume gains, while South Korea's K-Beauty ecosystem exports flexible cosmetic packs worldwide. Regional converters benefit from proximity to virgin resin suppliers and cost-competitive labor, reinforcing localized supply chains even as multinational brand owners demand global harmonization of pack specifications.

North America exhibits a mature demand profile focused on premiumization and e-commerce readiness. Lightweight designs translate into shipping cost savings under dimensional-weight tariffs, pushing retailers toward house-brand pouch adoption. Europe's regulatory drive toward recyclability accelerates mono-material rollouts, positioning flexible packs ahead of rigid glass and multilayer cartons on lifecycle metrics. Scandinavian markets pilot deposit schemes for flexible films, providing data for broader EU implementation.

South America and the Middle East, and Africa collectively offer emerging upside. Brazil's dairy sector adopts spouted pouches for yogurt drinks, citing cold-chain energy savings. Gulf Cooperation Council nations import pouch-packed ready meals that withstand desert logistics, and African megacities rely on small-sachet formats for affordable daily necessities. Infrastructure hurdles remain, yet demographic momentum and rising disposable incomes will progressively close the gap with developed regions.

- Amcor plc

- Mondi plc

- ProAmpac Intermediate, Inc.

- Constantia Flexibles Group GmbH

- Huhtamaki Oyj

- Sealed Air Corporation

- Sonoco Products Company

- Coveris Management GmbH

- Bischof + Klein SE and Co. KG

- FlexPak Services, LLC

- Goglio SpA

- Scholle IPN Corporation

- Gualapack SpA

- Aluflexpack AG

- Flair Flexible Packaging Corporation

- Hood Packaging Corporation

- Toppan Printing Co., Ltd.

- Winpak Ltd.

- Glenroy, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for cost-effective packaging and brand differentiation

- 4.2.2 Surge in convenience and ready-to-eat food consumption

- 4.2.3 Sustainability-driven shift toward lightweight flexible packs

- 4.2.4 Acceleration of e-commerce and direct-to-consumer logistics

- 4.2.5 Expansion of spouted pouches in industrial bulk applications

- 4.2.6 High-barrier mono-material film breakthroughs enabling recyclability

- 4.3 Market Restraints

- 4.3.1 Escalating environmental and recycling challenges

- 4.3.2 Volatility in plastic-resin feedstock prices

- 4.3.3 Competition from emerging fiber-based flexible formats

- 4.3.4 Supply constraints for bio-based high-barrier resins

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 The Impact of Macroeconomic Factors on the Market

- 4.9 Recycling and Sustainability Landscape

5 MARKET SIZE AND GROWTH FORECASTS(VALUE)

- 5.1 By Material

- 5.1.1 Plastics

- 5.1.1.1 Polyethylene (PE)

- 5.1.1.2 Polypropylene (PP)

- 5.1.1.3 Polyethylene Terephthalate (PET)

- 5.1.1.4 Polyvinyl Chloride resin (PVC)

- 5.1.1.5 Other Plastics

- 5.1.2 Paper

- 5.1.3 Aluminum Foil

- 5.1.4 Bio-degradable/Compostable

- 5.1.1 Plastics

- 5.2 By Product Type

- 5.2.1 Flat (Pillow and Side-Seal)

- 5.2.2 Stand-Up

- 5.2.3 Spouted

- 5.2.4 Retort

- 5.2.5 Aseptic

- 5.2.6 Stick-Pack / Sachet

- 5.2.7 Rollstock / Premade Pouch

- 5.3 By Closure Type

- 5.3.1 Zipper

- 5.3.2 Spout and Cap

- 5.3.3 Tear-Notch

- 5.3.4 Slider

- 5.3.5 Other Closure Type

- 5.4 By End-User Industry

- 5.4.1 Food

- 5.4.1.1 Candy and Confectionery

- 5.4.1.2 Frozen Foods

- 5.4.1.3 Fresh Produce

- 5.4.1.4 Dairy Products

- 5.4.1.5 Dry Foods and Cereals

- 5.4.1.6 Meat, Poultry and Seafood

- 5.4.1.7 Pet Food

- 5.4.1.8 Other Foods (Sauces, Condiments, Spreads)

- 5.4.2 Beverage

- 5.4.2.1 Alcoholic

- 5.4.2.2 Non-Alcoholic

- 5.4.3 Medical and Pharmaceutical

- 5.4.4 Personal Care and Cosmetics

- 5.4.5 Home Care and Household

- 5.4.6 Other End-User Industry

- 5.4.1 Food

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Kenya

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 Mondi plc

- 6.4.3 ProAmpac Intermediate, Inc.

- 6.4.4 Constantia Flexibles Group GmbH

- 6.4.5 Huhtamaki Oyj

- 6.4.6 Sealed Air Corporation

- 6.4.7 Sonoco Products Company

- 6.4.8 Coveris Management GmbH

- 6.4.9 Bischof + Klein SE and Co. KG

- 6.4.10 FlexPak Services, LLC

- 6.4.11 Goglio SpA

- 6.4.12 Scholle IPN Corporation

- 6.4.13 Gualapack SpA

- 6.4.14 Aluflexpack AG

- 6.4.15 Flair Flexible Packaging Corporation

- 6.4.16 Hood Packaging Corporation

- 6.4.17 Toppan Printing Co., Ltd.

- 6.4.18 Winpak Ltd.

- 6.4.19 Glenroy, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment