|

市场调查报告书

商品编码

1910433

证据管理:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Evidence Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

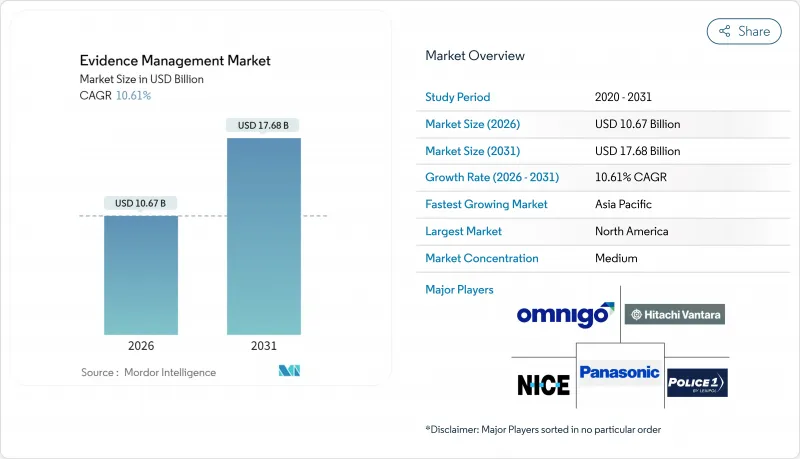

预计证据管理市场将从 2025 年的 96.5 亿美元成长到 2026 年的 106.7 亿美元,并预计到 2031 年将达到 176.8 亿美元,2026 年至 2031 年的复合年增长率为 10.61%。

这种快速扩张反映了各机构正从基本的本地储存转向以云为先、人工智慧驱动的生态系统,用于收集、分类和分析呈指数级增长的多媒体证据。云端部署已支援 63.63% 的工作流程,并且由于其订阅定价、自动扩展和符合 FedRAMP/CJIS 标准等优势,其发展速度持续超越本地解决方案,从而降低了资本成本和采购摩擦。同时,联邦和州政府大力推行的津贴项目,例如司法援助局 (Bureau of Justice Assistance) 的 4 亿美元执法记录仪基金,正鼓励小规模的部门采用集成摄像头和软体包,这些软体包包含证据链、脸部辨识和语音转文本功能。虽然硬体仍然是最大的收入来源,但随着越来越多的机构寻求供应商在整合人工智慧分析、冷资料储存分层和法庭演示模组方面的专业知识,专业服务和託管服务已成为成长最快的类别。同时,智慧城市监控网路、5G回程传输和边缘运算节点每月都在向市政证据库输送Petabyte的影像资料。这迫使管理人员从孤立的记录储存室转向整合的、跨机构的储存库,以便能够近乎即时地识别武器、车辆和车牌。

全球证据管理市场趋势与洞察

全球犯罪率上升推动了对数位证据的需求。

由于暴力犯罪和网路诈骗案件数量居高不下,检察官要求提供无可辩驳的数位证据,以提高定罪的确定性。巡逻警员每月产生40至60小时的影像数据,是2020年基准值的四倍。这迫使檔案管理部门放弃DVD存檔,转而使用扩充性的云端库,自动为每个影片片段建立索引。已在其证据管理平台中整合转录功能的部门,可以搜寻数百Terabyte的影像资料中的关键字,从而将取证过程缩短数週。随着都市区部署车牌盘式分析仪和声学枪声探测感测器,元资料流正流入同一个储存库,增强了情境察觉,并缩短了起诉时间。如果没有这些人工智慧辅助的中心,证据积压可能会损害公共信任和法庭诉讼的效率。

警务机构中执法记录器和车载摄影机的普及

目前全球已有超过2万个执法机构使用执法记录仪,而像加拿大皇家骑警2024年全国性计画这样的大规模部署,更凸显了这项技术的普及应用。每位警员每次执勤会产生8-12GB的数据,这些数据会在设备连接底座时自动上传,无需手动檔案传输。现代证据管理软体会对传输中的影像进行加密,分配防篡改杂凑值,并将每个视讯片段与一个CAD(电脑辅助调度)案件编号关联起来,从而创建从现场到法庭的审核。供应商越来越多地将无限量的Tier 1存储空间与基于人工智能的信息抑制功能捆绑销售,以此锁定客户签订多年合同,同时确保可预测的运营成本。此外,透过整合行车记录器和无人机(UAV)影像,多感测器影像整合技术使负责人能够追踪嫌疑人从街头到巷道直至被捕的整个过程,为陪审团提供完整的案情叙述,从而提高定罪率。

长期云端冷资料储存高成本

刑事司法资讯系统 (CJIS) 要求警察部门将凶杀案影像保存数十年,这迅速累积成每月每 GB 0.08 至 0.12 美元的成本。一个中型警察机构每年存檔 5PB 的数据,仅储存一项每年就要花费超过 50 万美元。混合分层储存(热储存用于正在处理的案件,宽储存用于已结案件)可以降低成本,但搜寻费用和审核要求使预算编制变得复杂。供应商则以固定费率的「无限保留」方案作为应对,将机构锁定在专有格式中,阻碍了迁移。因此,地方政府财务主管在核准多年期云端合约之前,要求提供严格的总成本模型,这减缓了证据管理市场的整体发展。

细分市场分析

预计到2025年,云端工作流程将占据证据管理市场62.95%的份额,并在2031年之前以12.03%的复合年增长率成长。这一优势得益于云端的快速部署、按需收费和整合式人工智慧工具包,而这些在本地环境中难以实现。运输安全局在全国部署用于储存机场影像的云端储存库,体现了联邦政府对第三方基础设施的信任。各机构利用全球内容分发网路(CDN)在几秒钟内将关键影像串流传输给检察官,消除了传输延迟。同时,混合模式满足了那些担心传票回应延迟的团队的需求,将最新的影像在本地,并将夜间存檔同步到云端。云的弹性边缘节点甚至可以实现摄影机内分析,在拍摄后几秒钟内标记武器,并成为多机构联合工作组事实上的骨干网路。

在那些对资料主权法律和低延迟自主运作至关重要的环境中(例如拥有现有资料中心的大型都市警察部门),本地部门仍将继续。然而,即使在这些环境中,也出现了一种日益增长的趋势,即在重大事件期间增加云端爆发容量,以避免资本支出激增。供应商已经意识到这种转变,并在将功能移植到本地客户端之前,优先发布云端更新,从而强化了云端作为证据管理市场主要交付模式的良性循环。

到2025年,硬体收入将占总收入的48.17%,这反映了第一代执法记录器正被4K、宽动态范围型号以及配备5G回程传输的坚固型行车记录器所取代。每笔硬体订单通常都捆绑了多年期的SaaS许可,从而确保了可预测的经常性收入。服务业务虽然绝对规模小规模,但其复合年增长率(CAGR)高达11.28%,主要得益于各部门倾向将资料迁移、使用者培训和策略配置等工作外包给供应商主导的团队。这一趋势与分配给服务业务的证据管理市场规模相符,预计到2031年,该市场规模将超过44.7亿美元。

软体收入将紧跟着硬体发展步伐,随着各机构津贴减少并转向证据分析、转录和法庭准备方案,软体收入将加速成长。跨平台SDK鼓励第三方开发者建立编辑功能、车牌辨识和证据归檔仪表板,从而提高生态系统的普及率。随着时间的推移,差异化价值不再在于摄影机本身,而是能够减少70%审查工作的AI模型,而软硬体一体化方案也将成为首选的采购方案。

区域分析

预计到2025年,北美将创造37.1亿美元的市场规模(占全球证据管理市场份额的38.48%),这得益于完善的执法记录仪强制佩戴政策和慷慨的拨款,这些拨款缓衝了采购週期。 18,000个地方政府部门之间的跨机构合作推动了持续的升级需求,各州立法机构也持续推进平台互通性,为符合CJIS和NIJ指南的软体升级提供新的资金。供应商通常会先在美国主要大都会圈的警察部门试行推广语音翻译和自动警员匿名模糊处理等研发能力,然后再推广到海外。

亚太地区虽然目前规模较小,但正以11.45%的复合年增长率成为成长最快的地区,这主要得益于印度、中国、新加坡和日本的智慧城市网络,这些网络将数百万个物联网设备连接到集中式系统。各国政府部门和机构都在优先考虑人工智慧驱动的态势分析,公私合作联盟也在资金筹措符合资料主权法规的大规模云端资料中心。日本国家警察厅计划在2026年前为所有巡逻警员配备执法记录仪,这将持续产生硬体和许可证需求。同时,印度的一些地区性城市正在效仿德里和孟买的先行部署模式,从而刺激了下游对多语言转录和法庭回放工具的需求。

在欧洲,跨境资讯框架的建立推动了相关工作的进展,该框架要求成员国采用标准化的证据格式。 GDPR要求供应商整合细粒度的资料保留逻辑和公民删除工作流程,这正在影响其他地区的功能需求。拉丁美洲和中东是新兴市场。都市化和不断增长的公共预算正在推动先导计画结合了无人机拍摄的影像、社群媒体抓取和即时影像分析技术。儘管遍远地区频宽不足,但卫星回程传输和5G固定无线存取正在帮助扩大覆盖范围,使所有司法管辖区都能获得可靠的证据管理市场解决方案,而无需新建资料中心。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 全球犯罪率上升推动了对数位证据的需求。

- 警察机关中执法记录器和车载摄影机的普及

- 政府投入大量资金用于公共科技升级

- 智慧城市产生的多媒体数据爆炸性成长

- 利用人工智慧分析技术消除证据处理延误

- 强制执行机构间资料互通性

- 市场限制

- 长期云端储存和冷资料储存高成本

- 网路安全和资料完整性漏洞

- 司法管辖区内资料主权方面的法律不确定性(UTR)

- 地方警察部门宽频接取有限(UTR)

- 产业价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 透过部署

- 本地部署

- 云

- 按组件

- 硬体

- 执法记录仪

- 车载行车记录仪

- 全市摄影机

- 公共运输影片

- 软体

- 服务(咨询、培训、支援)

- 硬体

- 按证据类型

- 数位证据

- 影片

- 声音的

- 影像

- 文件

- 实物证据元资料

- 数位证据

- 最终用户

- 执法机关

- 运输

- 联邦和国防机构

- 法院和检察官办公室

- 保险公司

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 荷兰

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- NICE Ltd.

- QueTel Corporation

- Lexipol LLC

- Hitachi Vantara Corporation

- Panasonic Holdings Corporation

- Motorola Solutions, Inc.

- Oracle Corporation

- CaseGuard LLC

- COBAN Technologies, Inc.

- Porter Lee Corporation

- Finalcover LLC

- International Business Machines Corporation

- Axon Enterprise, Inc.

- Genetec Inc.

- Digital Ally, Inc.

- Veritone, Inc.

- Tyler Technologies, Inc.

- Safe Fleet Holdco, Inc.

- Reveal Media Ltd.

- Utility Associates, Inc.

- Getac Technology Corporation

- StorMagic Ltd.

第七章 市场机会与未来展望

The Evidence Management market is expected to grow from USD 9.65 billion in 2025 to USD 10.67 billion in 2026 and is forecast to reach USD 17.68 billion by 2031 at 10.61% CAGR over 2026-2031.

This swift expansion reflects agencies' shift from basic on-premise storage toward cloud-first, AI-enabled ecosystems that collect, classify, and analyze rapidly growing volumes of multimedia evidence. Cloud deployment, which already supports 63.63% of total workflows, continues to outpace on-premise alternatives because subscription pricing, auto-scaling, and FedRAMP / CJIS compliance reduce both capital cost and procurement friction. At the same time, aggressive federal and state grant programs, such as the Bureau of Justice Assistance's USD 400 million body-camera fund, are pushing even small departments toward integrated camera-plus-software bundles that guarantee chain-of-custody, facial recognition, and speech-to-text functions out of the box. Hardware still contributes the single largest revenue stream, but professional and managed services are the fastest growing line item as agencies seek vendor expertise to integrate AI analytics, cold-storage tiering, and courtroom presentation modules. In parallel, smart-city surveillance networks, 5G backhaul, and edge compute nodes are injecting petabytes of video into municipal evidence vaults every month, compelling administrators to migrate from siloed record rooms to unified, cross-agency repositories able to flag weapons, vehicles, or license plates in near real time.

Global Evidence Management Market Trends and Insights

Rising Global Crime Rate Boosting Digital-Evidence Demand

Violent-crime and cyber-fraud caseloads remain elevated, prompting prosecutors to demand indisputable digital proof for successful convictions.Patrol officers now generate 40-60 hours of video each month, quadruple the 2020 baseline, forcing records units to abandon DVD archives for elastic cloud libraries that auto-index every clip. Departments adopting Evidence Management market platforms with built-in transcription shave weeks off discovery timelines because detectives can keyword search across hundreds of terabytes of footage. As cities add license-plate readers and acoustic gunshot sensors, metadata streams flood into the same repositories, strengthening situational awareness and speeding time-to-charge. Without these AI-assisted hubs, agencies risk evidence backlogs that undermine public trust and trial efficiency.

Proliferation of Body-Worn and In-Car Cameras Among Police Forces

More than 20,000 agencies worldwide now deploy body cameras, and large rollouts, such as the Royal Canadian Mounted Police's 2024 national program, prove the technology's mainstream status. Each officer produces 8-12 GB of data per shift, which is automatically uploaded once the device docks, eliminating the need for manual file transfer. Modern Evidence Management market software encrypts footage in transit, assigns tamper-proof hashes, and links every clip to CAD incident numbers, creating a cradle-to-courtroom audit trail. Vendors increasingly bundle unlimited tier-one storage and AI redaction, locking customers into multi-year contracts while guaranteeing predictable operating expense. As dash-cam and UAV footage join the mix, multi-sensor stitching enables analysts to track a suspect from the street to the alley to arrest, providing jurors with a seamless narrative that enhances conviction rates.

High Long-Term Cloud and Cold-Storage Costs

CJIS mandates push departments to retain homicide footage for decades, and at USD 0.08-0.12 per GB per month, expenses climb quickly. A mid-size force archiving 5 PB per year spends more than USD 500,000 annually just on storage. Hybrid tiers mitigate cost, hot buckets for active cases, glacier tiers for closed files, but retrieval fees and audit requirements complicate budgeting. Vendors counter with flat-rate "all you can store" plans yet lock agencies into proprietary formats that hinder migration. Municipal CFOs therefore demand rigorous total-cost models before greenlighting multi-year cloud contracts, slowing the broader Evidence Management market rollout.

Other drivers and restraints analyzed in the detailed report include:

- Government Funding Waves for Public-Safety Technology Upgrades

- AI-Driven Analytics to Clear Evidence Backlogs

- Cyber-Security and Data-Integrity Vulnerabilities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud workflows generated 62.95% of Evidence Management market share in 2025 and are projected to expand at a 12.03% CAGR through 2031. This dominance stems from rapid provisioning, usage-based billing and integrated AI toolkits that on-prem setups rarely match. The Transportation Security Administration's national rollout of a cloud vault for airport footage underlines federal confidence in third-party infrastructure. Agencies tap global CDNs to stream critical clips to prosecutors within seconds, eliminating courier delays. Meanwhile, hybrid models appease teams worried about subpoena latency by caching recent footage in local appliances while syncing archives to the cloud overnight. Cloud's elastic edge nodes even enable in-camera analytics, flagging a weapon just seconds after capture, making it the de-facto backbone for multi-agency task forces.

On-premise deployments persist where sovereign-data statutes or low-latency autonomous operation is critical, such as large metropolitan forces with existing data centers. Yet even those environments increasingly bolt on cloud burst capacity during major events to avoid capital spikes. Vendors, sensing the shift, now release updates cloud-first before porting features to on-prem clients, reinforcing a virtuous cycle that cements the cloud as the primary Evidence Management market delivery model.

Hardware captured 48.17% of 2025 revenues, reflecting continual replacement of first-generation body cameras with 4K, wide-dynamic-range units and rugged dash cams built for 5G backhaul. Each hardware order typically bundles multiyear SaaS licenses, ensuring predictable annuity streams. Services, though smaller in absolute terms, are on pace for an 11.28% CAGR, as departments outsource data migration, user training and policy configuration to vendor-led teams. That trend aligns with the Evidence Management market size allocated to services, which is expected to surpass USD 4.47 billion by 2031.

Software revenue follows hardware footprints yet accelerates once agencies exhaust grant funds and shift to evidence analytics, transcription and courtroom-ready packaging. Cross-platform SDKs invite third-party developers to craft redaction, license-plate recognition and chain-of-custody dashboards, widening ecosystem stickiness. Over time, differentiating value lies not in the camera itself but in AI models that cut review labor by 70%, cementing integrated hardware-plus-software stacks as the preferred procurement package.

The Evidence Management Market Report is Segmented by Deployment (On-Premises and Cloud), Component (Hardware, Software, and Services), Evidence Type (Digital Evidence and Physical Evidence Metadata), End User (Law-Enforcement Agencies, Transportation Agencies, Federal and Defense Agencies, Courts and Prosecutors, and Insurance Companies), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated USD 3.71 billion in 2025, equal to 38.48% of the global Evidence Management market share, and benefits from entrenched body-cam mandates plus rich grant funnels that cushion procurement cycles. Agency collaboration across 18,000 municipal departments drives consistent refresh demand, and state legislatures continue to legislate platform interoperability, funneling new funds into software upgrades that align with CJIS and NIJ guidelines. Vendors often pilot R&D features, speech translation, automatic officer de-identifier blurring, within U.S. metropolitan forces before exporting them.

Asia-Pacific, though smaller today, posts the fastest 11.45% CAGR as smart-city grids in India, China, Singapore and Japan plug millions of IoT lenses into centralized vaults. Regional ministries prioritize AI-enabled situational analytics, and public-private consortia finance large-scale cloud pods to satisfy data-sovereignty rules. Japan's National Police Agency expects to equip every patrol officer with a body camera by 2026, creating an ongoing hardware and license pipeline. Meanwhile, India's tier-2 cities replicate flagship deployments from Delhi and Mumbai, accelerating downstream demand for multilingual transcription and in-courtroom replay tools.

Europe advances on the back of cross-border intelligence frameworks that require standardized evidentiary formats among member states. GDPR compels vendors to embed fine-grained retention logic and citizen-deletion workflows that are now influencing feature requests in other regions. Latin America and the Middle East represent emerging frontiers; urbanization and rising public-safety budgets spur pilot projects that bundle drone video, social-media scraping and real-time video analytics. Despite bandwidth gaps in rural provinces, satellite backhaul and 5G Fixed Wireless Access help extend coverage, ensuring every jurisdiction can now subscribe to a credible Evidence Management market solution without erecting new data centers.

- NICE Ltd.

- QueTel Corporation

- Lexipol LLC

- Hitachi Vantara Corporation

- Panasonic Holdings Corporation

- Motorola Solutions, Inc.

- Oracle Corporation

- CaseGuard LLC

- COBAN Technologies, Inc.

- Porter Lee Corporation

- Finalcover LLC

- International Business Machines Corporation

- Axon Enterprise, Inc.

- Genetec Inc.

- Digital Ally, Inc.

- Veritone, Inc.

- Tyler Technologies, Inc.

- Safe Fleet Holdco, Inc.

- Reveal Media Ltd.

- Utility Associates, Inc.

- Getac Technology Corporation

- StorMagic Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising global crime rate boosting digital-evidence demand

- 4.2.2 Proliferation of body-worn and in-car cameras among police forces

- 4.2.3 Government funding waves for public-safety technology upgrades

- 4.2.4 Explosive growth in multimedia data generated by smart cities

- 4.2.5 AI-driven analytics to clear evidence backlogs

- 4.2.6 Cross-agency data-interoperability mandates

- 4.3 Market Restraints

- 4.3.1 High long-term cloud and cold-storage costs

- 4.3.2 Cyber-security and data-integrity vulnerabilities

- 4.3.3 Legal uncertainty over jurisdictional data sovereignty (UTR)

- 4.3.4 Limited broadband connectivity in rural policing (UTR)

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 On-premises

- 5.1.2 Cloud

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.1.1 Body-worn Cameras

- 5.2.1.2 Vehicle Dash Cameras

- 5.2.1.3 Citywide Cameras

- 5.2.1.4 Public Transit Video

- 5.2.2 Software

- 5.2.3 Services (Consulting, Training, Support)

- 5.2.1 Hardware

- 5.3 By Evidence Type

- 5.3.1 Digital Evidence

- 5.3.1.1 Video

- 5.3.1.2 Audio

- 5.3.1.3 Image

- 5.3.1.4 Documents

- 5.3.2 Physical Evidence Metadata

- 5.3.1 Digital Evidence

- 5.4 By End User

- 5.4.1 Law-Enforcement Agencies

- 5.4.2 Transportation Agencies

- 5.4.3 Federal and Defense Agencies

- 5.4.4 Courts and Prosecutors

- 5.4.5 Insurance Companies

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Netherlands

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 NICE Ltd.

- 6.4.2 QueTel Corporation

- 6.4.3 Lexipol LLC

- 6.4.4 Hitachi Vantara Corporation

- 6.4.5 Panasonic Holdings Corporation

- 6.4.6 Motorola Solutions, Inc.

- 6.4.7 Oracle Corporation

- 6.4.8 CaseGuard LLC

- 6.4.9 COBAN Technologies, Inc.

- 6.4.10 Porter Lee Corporation

- 6.4.11 Finalcover LLC

- 6.4.12 International Business Machines Corporation

- 6.4.13 Axon Enterprise, Inc.

- 6.4.14 Genetec Inc.

- 6.4.15 Digital Ally, Inc.

- 6.4.16 Veritone, Inc.

- 6.4.17 Tyler Technologies, Inc.

- 6.4.18 Safe Fleet Holdco, Inc.

- 6.4.19 Reveal Media Ltd.

- 6.4.20 Utility Associates, Inc.

- 6.4.21 Getac Technology Corporation

- 6.4.22 StorMagic Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

数位健康证据市场规模、份额和成长分析:按数位健康平台、最终用户和地区划分 - 2026-2033 年产业预测

数位健康证据市场规模、份额和成长分析:按数位健康平台、最终用户和地区划分 - 2026-2033 年产业预测 数位证据管理市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和功能划分

数位证据管理市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和功能划分 全球数位证据管理市场规模、份额、趋势和成长分析报告(2026-2034年)

全球数位证据管理市场规模、份额、趋势和成长分析报告(2026-2034年) 数位证据管理市场-全球产业规模、份额、趋势、机会、预测:按组件、部署类型、应用、地区和竞争格局划分,2021-2031年

数位证据管理市场-全球产业规模、份额、趋势、机会、预测:按组件、部署类型、应用、地区和竞争格局划分,2021-2031年 电子证据管理平台市场按组件、组织规模、部署模式、垂直产业和应用划分-2026-2032年全球预测

电子证据管理平台市场按组件、组织规模、部署模式、垂直产业和应用划分-2026-2032年全球预测 数位证据管理市场规模、份额和成长分析(按组件、软体、部署类型、最终用户和地区划分)—2026-2033年产业预测数位证据管理市场:按组件、部署模式、应用、最终用户、证据类型和组织规模划分 - 全球预测(2025-2032 年)

数位证据管理市场规模、份额和成长分析(按组件、软体、部署类型、最终用户和地区划分)—2026-2033年产业预测数位证据管理市场:按组件、部署模式、应用、最终用户、证据类型和组织规模划分 - 全球预测(2025-2032 年) 数位证据管理市场规模、份额和趋势分析报告(按组件、部署模式、最终用途、地区和细分市场预测,2025 年至 2030 年)

数位证据管理市场规模、份额和趋势分析报告(按组件、部署模式、最终用途、地区和细分市场预测,2025 年至 2030 年) 美国证据管理:市场占有率分析、产业趋势、统计数据、成长预测(2025-2030 年)

美国证据管理:市场占有率分析、产业趋势、统计数据、成长预测(2025-2030 年) 全球数位证据管理市场,2024-2028

全球数位证据管理市场,2024-2028