|

市场调查报告书

商品编码

1910447

折迭瓦楞纸包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Folding Carton Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

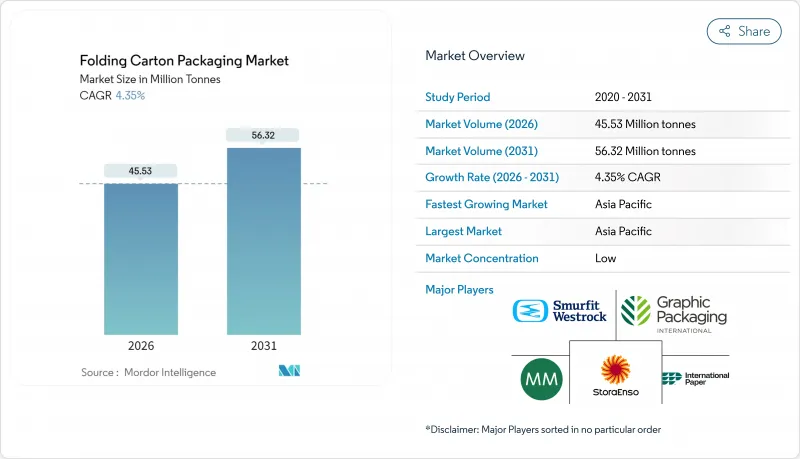

预计折迭纸盒包装市场将从 2025 年的 4,363 万吨增长到 2026 年的 4,553 万吨,到 2031 年将达到 5,632 万吨,2026 年至 2031 年的复合年增长率为 4.35%。

持续的需求源自于更严格的法规促使品牌转向纤维基替代品,以及电子商务的扩张,后者推动了既能保护产品又能满足回收要求的包装形式的发展。消费品(尤其是化妆品和营养补充品)日益高端化,进一步凸显了折迭瓦楞纸包装市场中高视觉效果和高附加价值设计的重要性。欧盟和中国的再生材料含量法规提高了低品质生产商的进入门槛,使一体化造纸厂能够凭藉可追溯的纸板等级获得市场份额。原料价格的波动挤压了非一体化加工商的利润空间,同时加速了再生纤维流的采用,因为再生纤维流具有更可预测的成本结构。

全球折迭瓦楞纸包装市场趋势与洞察

永续性主导,朝向可再生包装转型

为了满足投资者需求和零售商的回收规定,品牌所有者正从塑胶包装转向可再生板包装。斯道拉恩索承诺在2030年实现100%可再生线,这巩固了折迭瓦楞纸包装市场未来多年的需求前景。欧盟的生产者延伸责任制(EPR)成本推高了多材料包装的处置成本,使得纸盒包装在成本效益方面更具优势。饭店和工业领域也正在发生类似的转变,用模塑纤维隔板取代塑胶内衬。大型零售商也积极响应这些目标,优先选择带有再生材料标籤的纤维基包装。这些趋势共同作用,使循环经济成为采购的必要条件,而非只是一种行销选择。

电子商务包装需求快速成长

多通路巨头正在重新设计小包裹工作流程,以降低破损率和运输成本,而折迭纸盒则具有体积效率高的优点,并支援全表面图形印刷。亚马逊2024年10-K报告指出,包装优化是履约的核心支柱,反映了设计改进如何能降低整个网路的成本。在亚太地区,线上食品和美妆领域的快速增长推动了对能够承受长途运输(从第一公里到最后一公里)的防篡改硬质包装的需求。在逆向物流中,纸盒也具有优势,因为它们能够保持完整性,从而降低退货率。随着都市区微型仓配中心的兴起,支持按需拣货的小型折迭纸盒在日用品类别中正获得越来越大的市场份额。

原生纸浆价格与供应波动

2024年5月,纸浆现货价格生产者物价指数(PPI)飙升至219.835,对依赖短期合约的加工商造成了沉重打击。工厂在维护週期中的停产进一步加剧了供应紧张,迫使加工商在负担价格飙升或将成本转嫁给下游之间做出选择。大型一体化企业透过在箱板纸机和纸板机之间分配纤维来抵消价格波动,而独立现货买家则面临营运资金的消耗。由此产生的成本结构差异正在推动併购,小规模业者也正在寻求改善其资产负债表。避险策略的应用日益增多,但由于零售商减少库存,需求的不确定性正在削弱其有效性。

细分市场分析

到2025年,医疗保健和製药业将占折迭纸盒包装市场17.34%的份额,预计到2031年将以6.71%的复合年增长率增长,主要受人口老龄化和生物製药上市的推动。虽然防篡改条纹和序列化视窗是符合美国联邦法规21 CFR Part 211的要求,但这些功能可以轻鬆整合到折迭纸盒中,无需增加多层结构的复杂性。食品和饮料行业将占折迭纸盒包装市场33.18%的份额,这主要得益于调理食品的普及和饮料多包装的兴起,后者充分利用了冷藏涂层纸板的优势。与此同时,个人护理行业正在利用优质光泽清漆在竞争激烈的专卖店货架上脱颖而出。

临床试验活动的增加推动了对适用于数位印刷的小批量包装的需求,从而减少了配方变更期间包装的过时。拥有A级无尘室设施的纸盒加工商具备优于大宗商品製造商的污染控制和审核准备能力,即使原料成本上涨,也能维持价格溢价。在大众食品市场,采用轻质刨花板製成的定量包装谷物和零食托盘满足了基本需求,并缓解了週期性需求波动。

折迭纸盒包装市场报告按终端用户行业(食品饮料、家居用品、个人护理及化妆品、医疗製药、烟草、电器五金)、基材类型(未漂白纸板等)、印刷技术(胶印、数位印刷等)和地区(北美、欧洲等)进行细分。市场预测以吨为单位。

区域分析

亚太地区将继续保持其主导地位,预计到2025年将占据折迭纸盒包装市场38.42%的份额。受中国、印度和印尼全通路零售模式的深入发展所推动,亚太地区预计将持续维持6.82%的复合年增长率。中国加工商正在升级其机械设备,以满足国内电子产品出口商设定的严格抗破强度标准。政府推出的生物降解法规也加速了无PFAS涂层的应用。在日本,便利商店食材自煮包套装的流行带动了对冷冻库冷冻纸板的需求,进而促进了对优质瓦楞纸板的需求。同时,韩国的回收评级系统正在推动纤维包装材料的标准化,并鼓励引入高产量脱墨生产线。

在北美,成长将主要由面向消费者的订阅品牌推动,这些品牌需要印有鲜艳图案的小批量纸盒。国际纸业以99亿美元收购DS Smith,建立了跨境加工网络,缩短了运输距离,并增强了应对力。加拿大禁止使用难以回收的塑料,促使冷冻食品和乳製品重新采用纸板套。墨西哥电子产品组装业务的近岸外包,推高了对防静电纸盒内衬的需求,进而推动了美国造纸厂原生牛皮纸的进口。

欧洲持续致力于创新,其《包装及包装废弃物法规》规定,到2028年必须全面回收,并于2026年8月前淘汰含氟阻隔材料。德国、法国和英国正率先开发将金属效果与水性油墨结合的数位装饰生产线,在追求高端视觉效果的同时,也兼顾了环保法规的要求。儘管东欧加工商已获得欧盟资金用于升级瓦楞纸板设备,但由于纸板在商店的良好表现,它仍然是糖果甜点出口的首选材料。新的监管政策正在推动对新一代涂布设备的资本投资,并促使软包装薄膜用户重新考虑使用纤维替代品来生产保质期更长的产品。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 迈向永续性和可回收包装

- 电子商务包装需求快速成长

- 优质化及货架醒目印刷的需求

- 全球塑胶减量法规

- 数位印刷技术可以实现小批量精准印刷。

- 食材自煮包和即食调理食品订阅服务的激增

- 市场限制

- 原生纸浆价格与供应波动

- 软包装袋替换

- 阻隔性纸盒的回收有限

- 不含 PFAS 涂料的合规成本

- 产业价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 地缘政治影响分析

第五章 市场规模与成长预测

- 按最终用户行业划分

- 食品/饮料

- 家用

- 个人护理和化妆品

- 医疗和药品

- 烟草

- 电气和五金

- 依材料类型

- 固态漂白板(SBB)

- 涂布未漂白牛皮纸板(CUK)

- 白线刨花板

- 折迭纸盒

- 透过印刷技术

- 胶印

- 数位(喷墨/静电复印)

- 柔版印刷

- 凹版印刷

- 其他印刷技术

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲和纽西兰

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Smurfit Westrock plc

- Graphic Packaging International LLC

- Mayr-Melnhof Karton AG

- DS Smith plc

- International Paper Company

- Stora Enso Oyj

- Georgia-Pacific LLC

- Mondi plc

- Huhtamaki Oyj

- Seaboard Folding Box Co. Inc.(Vidya Brands)

- American Carton Company

- All Packaging Company

- Edelmann GmbH

- CCL Healthcare(CCL Industries Inc.)

- Rengo Co., Ltd.

- Sonoco Products Company

- Autajon Group

- Southern Champion Tray

第七章 市场机会与未来展望

The folding carton packaging market is expected to grow from 43.63 million tonnes in 2025 to 45.53 million tonnes in 2026 and is forecast to reach 56.32 million tonnes by 2031 at 4.35% CAGR over 2026-2031.

Sustained demand emerges from stricter legislation that steers brands toward fiber-based substitutes and from e-commerce expansion, which rewards protective formats that also meet recycling mandates. Accelerating premiumization in consumer goods, especially cosmetics and nutraceuticals, magnifies the folding carton packaging market's focus on high-graphic, value-added designs. Recycled-content regulations in the European Union and China raise barriers for low-quality producers, enabling integrated mills to capture share with traceable paperboard grades. Raw-material price volatility narrows margins for non-integrated converters, yet it simultaneously accelerates adoption of recycled fiber streams that deliver more predictable cost structures.

Global Folding Carton Packaging Market Trends and Insights

Sustainability-led Shift to Recyclable Packaging

Brand owners are migrating from plastic toward recyclable board to satisfy investor directives and retail take-back rules. Stora Enso's pledge for 100% recyclable lines by 2030 anchors multi-year volume visibility for the folding carton packaging market. Extended Producer Responsibility fees in the EU raise disposal costs on mixed-material packs, tilting the cost-benefit equation in favor of cartons. The hospitality and industrial sectors echo the shift by swapping plastic inserts for molded fiber partitions. Large retailers align with these targets by preferring fiber-based formats that declare recycled-content percentages on-pack. Together, the moves embed circularity as a procurement prerequisite rather than a marketing option.

E-commerce Packaging Demand Boom

Multichannel giants are redesigning parcel workflows to cut damage rates and freight costs, and folding cartons excel at cube efficiency while supporting full-surface graphics. Amazon's 2024 10-K cites packaging optimization as a core fulfillment pillar, reflecting how design tweaks cascade into network savings. Asia Pacific's surging online grocery and beauty segments amplify demand for tamper-evident, rigid solutions that survive long "first-mile-to-last-mile" journeys. Reverse logistics also favors cartons because integrity retention lowers the percentage of unsaleable returns. As micro-fulfillment hubs proliferate in urban centers, small-format folding cartons that accommodate on-demand picking cycles gain share across household staples.

Virgin Pulp Price and Supply Volatility

Pulp spot prices touched a Producer Price Index level of 219.835 in May 2024, exposing converters that rely on short-term contracts. Mill shutdowns during maintenance cycles tighten supply further, forcing converters to either absorb spikes or pass costs downstream. Integrated majors offset swings by diverting fiber between containerboard and cartonboard machines, yet spot-buying independents face working-capital drains. The resulting spread in cost structures accelerates M&A as sub-scale players seek balance-sheet relief. Hedge-instrument adoption rises, but the effectiveness is diluted by demand unpredictability linked to retail destocking.

Other drivers and restraints analyzed in the detailed report include:

- Premiumization and Shelf-Impact Printing Needs

- Global Plastic-Reduction Regulations

- Substitution by Flexible Pouches

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Healthcare and Pharmaceuticals claimed 17.34% of the folding carton packaging market in 2025 and are poised to climb at a 6.71% CAGR to 2031 on the back of aging demographics and biologic drug launches. Compliance with 21 CFR Part 211 demands tamper-evidence striplines and serialization windows, features readily integrated into folding cartons without adding multilayer complexity. The Food and Beverages category, holding 33.18% of the folding carton packaging market share, sustains volumes through ready-meal adoption and beverage multipacks that benefit from refrigerator-grade coated boards. Meanwhile, Personal Care leans on premium gloss varnishes to anchor shelf differentiation in crowded specialty stores.

Growing clinical trial activity triggers short-run packs that suit digital printing, cutting obsolescence when formulations shift. Carton converters with Class A cleanroom sites out-compete commodity players on contamination control and audit readiness, enabling price premiums even as input costs rise. For mass-market foods, portion-controlled cereal and snack trays rely on lightweight chipboard, underpinning baseline volume and cushioning overall demand swings driven by economic cycles.

The Folding Carton Packaging Market Report is Segmented by End-User Industry (Food and Beverages, Household, Personal Care and Cosmetics, Healthcare and Pharmaceuticals, Tobacco, and Electrical and Hardware), Material Type (Solid Bleached Board, and More), Printing Technology (Offset Lithography, Digital, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Volume (Tonnes).

Geography Analysis

Asia Pacific maintains clear leadership with 38.42% of the folding carton packaging market share in 2025 and is advancing at a 6.82% CAGR as omni-channel retail deepens in China, India, and Indonesia. Chinese converters upscale machinery to meet domestic electronics exporters' stringent burst-strength targets, and government mandates on biodegradability accelerate the adoption of PFAS-free coatings. Japanese premium carton demand rises as convenience-store meal kits proliferate and require freezer-grade board. Meanwhile, South Korea's recyclability grading scheme further standardizes fiber packaging inputs and incentivizes high-yield deinking lines.

North America sustains growth through direct-to-consumer subscription brands that need small-batch cartons with vibrant graphics. International Paper's USD 9.9 billion DS Smith acquisition provides coast-to-coast converting nodes, trimming freight miles, and enhancing responsiveness to regional CPG demand surges. Canadian bans on difficult-to-recycle plastics redirect frozen entrees and dairy products back into cartonboard sleeves. Mexico's near-shoring of electronics assembly escalates demand for ESD-safe carton inserts, pulling imports of virgin Kraft liner from United States mills.

Europe remains innovation-centric, with the Packaging and Packaging Waste Regulation forcing full recyclability by 2028 and eliminating fluorinated barriers by August 2026. Germany, France, and the United Kingdom pioneer digital embellishment lines that marry metallic effects with water-based inks, aligning luxury visual targets with environmental mandates. Eastern European converters secure EU funding to update corrugators, yet cartonboard remains the format of choice for confectionery exports due to its higher shelf impact. The new regulatory certainty galvanizes CapEx in next-generation coating kitchens, nudging flexible-film users to reconsider fiber alternatives for long-shelf-life SKUs.

- Smurfit Westrock plc

- Graphic Packaging International LLC

- Mayr-Melnhof Karton AG

- DS Smith plc

- International Paper Company

- Stora Enso Oyj

- Georgia-Pacific LLC

- Mondi plc

- Huhtamaki Oyj

- Seaboard Folding Box Co. Inc. (Vidya Brands)

- American Carton Company

- All Packaging Company

- Edelmann GmbH

- CCL Healthcare (CCL Industries Inc.)

- Rengo Co., Ltd.

- Sonoco Products Company

- Autajon Group

- Southern Champion Tray

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Sustainability-led shift to recyclable packaging

- 4.2.2 E-commerce packaging demand boom

- 4.2.3 Premiumization and shelf-impact printing needs

- 4.2.4 Global plastic-reduction regulations

- 4.2.5 Digital printing enables short-run micro-targeting

- 4.2.6 Meal-kit and ready-meal subscriptions surge

- 4.3 Market Restraints

- 4.3.1 Virgin pulp price and supply volatility

- 4.3.2 Substitution by flexible pouches

- 4.3.3 Limited recycling for barrier cartons

- 4.3.4 PFAS-free coating compliance costs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Geopolitical Impact Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1 By End-user Industry

- 5.1.1 Food and Beverages

- 5.1.2 Household

- 5.1.3 Personal Care and Cosmetics

- 5.1.4 Healthcare and Pharmaceuticals

- 5.1.5 Tobacco

- 5.1.6 Electrical and Hardware

- 5.2 By Material Type

- 5.2.1 Solid Bleached Board (SBB)

- 5.2.2 Coated Unbleached Kraftboard (CUK)

- 5.2.3 White-lined Chipboard

- 5.2.4 Folding Boxboard

- 5.3 By Printing Technology

- 5.3.1 Offset Lithography

- 5.3.2 Digital (Inkjet / Electrophotography)

- 5.3.3 Flexography

- 5.3.4 Gravure

- 5.3.5 Other Printing Technology

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Australia and New Zealand

- 5.4.4.6 Rest of Asia Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Egypt

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Smurfit Westrock plc

- 6.4.2 Graphic Packaging International LLC

- 6.4.3 Mayr-Melnhof Karton AG

- 6.4.4 DS Smith plc

- 6.4.5 International Paper Company

- 6.4.6 Stora Enso Oyj

- 6.4.7 Georgia-Pacific LLC

- 6.4.8 Mondi plc

- 6.4.9 Huhtamaki Oyj

- 6.4.10 Seaboard Folding Box Co. Inc. (Vidya Brands)

- 6.4.11 American Carton Company

- 6.4.12 All Packaging Company

- 6.4.13 Edelmann GmbH

- 6.4.14 CCL Healthcare (CCL Industries Inc.)

- 6.4.15 Rengo Co., Ltd.

- 6.4.16 Sonoco Products Company

- 6.4.17 Autajon Group

- 6.4.18 Southern Champion Tray

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

2025-2029年全球摺迭瓦楞纸包装市场

2025-2029年全球摺迭瓦楞纸包装市场 折迭瓦楞纸箱市场规模、份额及成长分析(按材料类型、订单类型、最终用途产业和地区划分)-2026-2033年产业预测

折迭瓦楞纸箱市场规模、份额及成长分析(按材料类型、订单类型、最终用途产业和地区划分)-2026-2033年产业预测 折迭式纸盒市场:未来预测(2025-2030)

折迭式纸盒市场:未来预测(2025-2030) 全球折迭纸盒市场未来展望(至2030年)

全球折迭纸盒市场未来展望(至2030年) 折迭式纸盒包装市场规模、份额、趋势分析报告:按最终用途、地区和细分市场预测,2025-2030 年

折迭式纸盒包装市场规模、份额、趋势分析报告:按最终用途、地区和细分市场预测,2025-2030 年 印尼纸包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)

印尼纸包装:市场占有率分析、行业趋势和成长预测(2025-2030 年) 折迭式纸盒市场 - 成长、未来展望、竞争分析,2025 年至 2033 年泰国折迭式纸盒包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)全球折迭纸盒包装市场规模:按材料类型、按产品类型、按最终用户、按地区、范围和预测

折迭式纸盒市场 - 成长、未来展望、竞争分析,2025 年至 2033 年泰国折迭式纸盒包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)全球折迭纸盒包装市场规模:按材料类型、按产品类型、按最终用户、按地区、范围和预测 2030 年豪华折迭纸盒市场预测:按盒子类型、材料类型、印刷技术、应用、最终用户和地区进行的全球分析

2030 年豪华折迭纸盒市场预测:按盒子类型、材料类型、印刷技术、应用、最终用户和地区进行的全球分析