|

市场调查报告书

商品编码

1910505

NAND快闪记忆体:市场占有率分析、产业趋势与统计资料、成长预测(2026-2031年)NAND Flash Memory - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

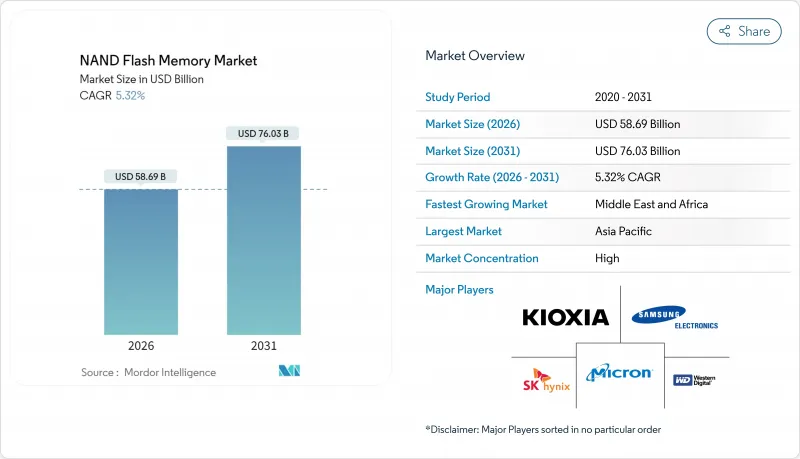

据估计,2026年NAND快闪记忆体体市场规模将达到586.9亿美元,高于2025年的557.3亿美元。预计到2031年,该市场规模将达到760.3亿美元,2026年至2031年的复合年增长率为5.32%。

这项稳定成长的驱动力来自超大规模资料中心在人工智慧训练丛集的资本投入、客户端PC和游戏主机向固态储存的转变,以及垂直堆迭式3D架构带来的每位元成本持续下降的趋势。同时,各国为促进半导体製造在地化而推出的奖励,尤其是在美国和沙乌地阿拉伯,正在增强区域供应链的韧性。突破300层以上的技术进步以及PCIe 5.0的普及,正在缩短企业级和消费级固态硬碟的更换週期。 5G部署和大量物联网终端的整合进一步扩大了潜在需求,使NAND快闪记忆体体市场有望保持持续的个位数温和成长。

全球NAND快闪记忆体体市场趋势与洞察

资料中心对人工智慧/机器学习储存的需求快速成长

超大规模营运商正在重新设计储存层级,将NVMe SSD池部署在靠近GPU丛集的位置,从而为搜寻密集型生成工作负载提供每秒数GB的吞吐量。西部资料预测,到2029年,仅5G终端的NAND快闪记忆体累积需求就将达到Petabyte,这凸显了闪存在弥合记忆体和冷资料储存效能差距方面的重要作用。采购蓝图越来越重视30TB至100TB的企业级硬碟,三星将于2024年发表的128TB BM1743 SSD就反映了这一转变。由此产生的拉动效应正在加速层级创新和控制器级压缩技术的发展,从而保持NAND快闪记忆体市场的成长动能。

5G和大规模物联网设备采用

独立组网5G的引入将推动边缘分析、智慧工厂、联网汽车和智慧电网等应用场景的发展,使本地非挥发性储存成为即时决策引擎的关键。西部数据的一份白皮书预测,随着工业模组容量超过8GB,NOR快闪记忆体将向NAND快闪记忆体过渡。半导体蓝图目前优先考虑扩展温度范围的QLC晶粒和符合车规标准的NVMe设计,从而将NAND快闪记忆体市场扩展至运输和基础设施领域。

高密度电池的耐久极限

QLC 的 1000-3000 次程式设计/擦除循环次数阈值对于日誌密集型资料库而言仍然不足,迫使用户过度配置,从而抵消了其成本优势。 Hackaday 指出,由于 300 层堆迭结构中电子陷阱的加速劣化,其物理极限正逐渐接近。虽然先进的纠错和损耗均衡演算法可以缓解劣化,但 PLC 和 Crosspoint 等替代储存技术仍在开发中,在它们的耐久性得到验证之前,它们很可能仍会限制某些NAND快闪记忆体市场的发展。

细分市场分析

由于TLC闪存在耐用性和成本方面实现了卓越的平衡,其在NAND快闪记忆体快闪记忆体市场占据了63.58%的份额。同时,QLC快闪记忆体正以6.35%的复合年增长率加速成长,超大规模资料中心业者中心在人工智慧资料湖领域展现出8-16倍的密度优势,预计到2031年,QLC闪存在NAND快闪记忆体快闪记忆体市场的整体份额将进一步提升。三星的280层QLC原型展示了16TB单面M.2固态硬碟的发展蓝图,该硬碟既能满足推理丛集的处理容量要求,又能减少机架面积。控制器级SLC快取技术和片上ECC技术缩小了与TLC快闪记忆体相比的延迟差距,从而促进了各种工作负载(例如视讯点播库和备份储存库)的迁移。 TLC闪存在写入密集型ERP和OLTP环境中依然保持优势,其超过10,000次的循环寿命确保了可预测的服务品质。

在消费级笔记型电脑领域,TLC卓越的功耗特性将维持其市场份额,但QLC每位元成本的持续下降已对中阶产品构成压力。美光第六代QLC相比第一代产品,读取延迟降低了34%,从而缩小了两者之间的效能差距。随着韧体定义的耐久性指标日趋成熟,OEM厂商将推出分级产品线,高容量产品采用QLC,而高阶产品则继续沿用先进的TLC製程。这种相互制约的趋势将使两种技术在预测期内继续主导NAND快闪记忆体快闪记忆体市场。

从平面堆迭到垂直堆迭的过渡已接近完成,预计到2025年,3D NAND将占据NAND快闪记忆体市场86.85%的份额。层数方面的技术突破,例如SK海力士的商用321层TLC和三星的400层V-NAND,显示到本十年末,500层大关必将被突破。其经济合理性显而易见:垂直扩展可以在不缩小单元尺寸的情况下提高容量,从而规避光刻技术的限制。 2D NAND将继续在航太和国防模组等细分领域占有一席之地,在这些领域,超低写入延迟比容量更为重要。

增加层数会加剧布线电阻和单元间干扰。为了克服这个问题,铠侠(Kioxia)的CMOS键结阵列策略隔离了外围电路,从而提高了超堆迭结构的I/O效率和产量比率。三星正在探索用于奶油界面闸极的氧化铪铁电也旨在实现类似的目标:在堆迭高度增加时保持阈值电压裕度。

NAND快闪记忆体报告依类型(SLC(单层单元)、MLC(多层单元)、TLC(三层单元)、QLC(四层单元))、结构(2D(平面)NAND、3D NAND)、介面(SATA、PCIe/NVMe、UFS/eMMC)、应用程式(智慧型手机、固态硬碟(PC、主机)主机、企业区和游戏中心进行固态硬碟)。市场预测以美元计价。

区域分析

亚太地区在韩国垂直整合巨头和中国庞大的设备组装基地的支持下,预计到2025年将占全球收入的55.40%。三星第九代V-NAND(286层)的量产以及SK海力士321层TLC生产线的推出,凸显了该地区的技术优势。总部位于北京的国内领导企业长江储存(YMTC)不顾出口限制,正大力推动232层QLC製程的研发,这显示其国内产能的扩张将使亚太地区继续保持其在NAND快闪记忆体快闪记忆体市场的主导地位。

北美在营收方面保持第二的位置,这主要得益于云端领域的资本投资需求。 《晶片与科学法案》为美光公司1,250亿美元的国内巨型晶圆厂建设计画资金筹措,预计到2035年,该计画将提升美国在先进记忆体领域的自给自足能力。加拿大贡献了控制器IP设计人才,而墨西哥则根据美墨加协定(USMCA)扩大了模组级组装,从而增强了全部区域的供应链多元化。

由于储存晶圆产能的限制,欧洲的市占率仍维持在个位数中段。然而,德国和法国的汽车及工业OEM厂商对车规级NVMe模组的需求强劲。诸如欧洲绿色交易等永续性指令正在推动对节能型PCIe 5.0固态硬碟的需求,这类硬碟能够降低机架能耗密度。欧洲晶圆厂正致力于利用新一代3D NAND製程(读取消费量低于3pJ/bit)来抢占这一市场。

中东和非洲地区以8.21%的复合年增长率呈现最高成长率。沙乌地阿拉伯的「2030愿景」正在推动利雅德週边晶圆后端一体化产业链的建设,而阿布达比政府投资机构则正寻求透过与一家控制器专家成立合资企业来建立区域供应链。丰富的可再生能源和极具吸引力的税收政策正在吸引封装合作伙伴,为在地化生产奠定基础,从而推动海湾合作委员会(GCC)资料中心NAND快闪记忆体快闪记忆体市场的渗透。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 资料中心对人工智慧/机器学习储存的需求快速成长

- 5G和大规模物联网设备采用

- PC/主机硬碟到固态硬碟的迁移

- 将业务策略转向成本效益高的QLC固态硬碟

- 国内本土NAND製造计划

- CXL 运算储存采用情况

- 市场限制

- 高密度电池的耐久极限

- 价格週期性和资本投资负担

- 由于出口限制,设备供不应求

- 高层工厂的永续性审查

- 产业供应链分析

- 监管环境

- 技术展望

- 宏观经济因素的影响

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按类型

- SLC(单层单元)

- MLC(多层细胞)

- TLC(三层板)

- QLC(四层池)

- 按结构

- 二维(平面)NAND

- 3D NAND

- 透过介面

- SATA

- PCIe/NVMe

- UFS/eMMC

- 透过使用

- 智慧型手机

- 固态硬碟(适用于PC和主机)

- 企业/资料中心固态硬碟

- 记忆卡和USB

- 工业和汽车电子

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 东南亚

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Samsung Electronics Co., Ltd.

- SK hynix Inc.

- KIOXIA Holdings Corporation

- Western Digital Corporation

- Micron Technology, Inc.

- Nanya Technology Corporation

- Powerchip Technology Corporation

- Winbond Electronics Corporation

- Macronix International Co., Ltd.

- Silicon Motion Technology Corp.

- Phison Electronics Corp.

- Kingston Technology Company, Inc.

- ADATA Technology Co., Ltd.

- Transcend Information, Inc.

- GigaDevice Semiconductor Inc.

- SK Group(Solid-State Storage division)

- PNY Technologies, Inc.

- Team Group Inc.

- Longsys Electronics Co., Ltd.

- Smart Modular Technologies, Inc.

第七章 市场机会与未来展望

NAND flash memory market size in 2026 is estimated at USD 58.69 billion, growing from 2025 value of USD 55.73 billion with 2031 projections showing USD 76.03 billion, growing at 5.32% CAGR over 2026-2031.

This steady expansion is powered by hyperscale data-center capital spending on artificial-intelligence training clusters, the transition of client PCs and game consoles to solid-state storage, and vertically-scaled 3D architectures that keep cost-per-bit on a declining path. At the same time, national incentives to localize semiconductor fabrication, especially in the United States and Saudi Arabia, are strengthening regional supply resilience. Layer-count breakthroughs above 300 layers and PCIe 5.0 adoption are shortening replacement cycles for both enterprise and consumer SSDs. The confluence of 5G rollouts and massive IoT endpoints further widens addressable demand, positioning the NAND flash memory market for durable mid-single-digit growth horizons.

Global NAND Flash Memory Market Trends and Insights

Data-center AI/ML storage surge

Hyperscale operators are redesigning storage hierarchies so that NVMe SSD pools sit closer to GPU clusters, sustaining multi-gigabyte-per-second throughput for retrieval-augmented generation workloads. Western Digital estimates cumulative demand of 19,000 petabytes of NAND by 2029 for 5G-enabled endpoints alone, underscoring flash's role in bridging memory and cold-storage performance gaps. Procurement roadmaps increasingly favor 30 TB to 100 TB enterprise drives, a shift visible in Samsung's 128 TB BM1743 SSD showcased in 2024. The resulting pull-through effect accelerates layer-count innovation and controller-level compression techniques that sustain the NAND flash memory market momentum.

5G and massive-IoT device proliferation

Standalone 5G deployments unlock edge analytics use cases, smart factories, connected cars, and smart grids that mandate local non-volatile storage for real-time decision engines. Western Digital's white paper anticipates a NOR-to-NAND crossover within industrial modules as capacities climb above 8 GB. Semiconductor roadmaps now prioritize extended-temperature QLC die and automotive-qualified NVMe designs, broadening the NAND flash memory market footprint across transportation and infrastructure domains.

Endurance limits of high-density cells

QLC's 1,000-3,000 program/erase thresholds remain insufficient for log-heavy databases, forcing over-provisioning that erodes cost benefits. Hackaday notes the physics ceiling approaching as electron-trap wear accelerates in 300-layer stacks. Although advanced error-correction and wear-leveling algorithms offset degradation, alternate memories such as PLC or cross-point remain on the horizon, tempering portions of the NAND flash memory market until longevity is proven.

Other drivers and restraints analyzed in the detailed report include:

- PC/Console transition from HDD to SSD

- Enterprise pivot to cost-efficient QLC SSDs

- Pricing cyclicality and cap-ex burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The NAND flash memory market size for TLC devices held a 63.58% market share with the strength of balanced endurance and cost. QLC, however, is accelerating at 6.35% CAGR as hyperscalers validate its 8-16X density advantage for AI data-lakes, which lifts the overall NAND flash memory market share allocated to QLC by 2031. Samsung's 280-layer QLC prototype signals a roadmap to 16 TB single-sided M.2 drives, shrinking rack footprints while meeting throughput rules for inference clusters. Controller-level SLC-cache techniques and on-die ECC are narrowing the latency gap with TLC, encouraging broader workloads such as VOD libraries and backup repositories to migrate. TLC will retain primacy in write-intensive ERP and OLTP environments where its 10,000-plus cycle rating secures predictable quality-of-service.

In consumer notebooks, TLC's favorable power profile sustains its install base, but falling QLC cost-per-bit is already pressuring mid-range SKUs. Micron's sixth-gen QLC exhibits 34% lower read latency than first-gen samples, eroding the perceived performance divide. As firmware-defined endurance mitigation matures, OEMs will likely introduce tiered offerings where high-capacity SKUs employ QLC, while premium lines continue on advanced TLC nodes. This interplay keeps both technologies central to the NAND flash memory market over the forecast horizon.

The shift from planar to vertical stacking is virtually complete: 3D NAND commanded 86.85% of the NAND flash memory market share in 2025. Layer-count breakthroughs, SK Hynix's commercial 321-layer TLC and Samsung's 400-plus-layer V-NAND, signal confident scaling beyond the 500-layer watermark before decade-end. The economic logic is clear; vertical scaling adds capacity without shrinking cell size, sidestepping lithography constraints. 2D NAND survives in niche aerospace and defense modules where ultra-low-latency writes outweigh capacity.

Layer additions do stress interconnect resistance and cell-to-cell interference. To overcome this, Kioxia's CMOS-bonded-array strategy decouples peripheral circuits, boosting I/O efficiency and improving yield in ultra-tall stacks. Samsung's exploration of hafnia ferroelectrics for creamy-interface gates pursues a similar aim: maintain threshold-voltage margins even as stack height extends.

The NAND Flash Memory Report is Segmented by Type (SLC (Single-Level Cell), MLC (Multi-Level Cell), TLC (Triple-Level Cell), and QLC (Quad-Level Cell)), Structure (2D (Planar) NAND, and 3D NAND), Interface (SATA, Pcie / NVMe, and UFS / EMMC), Application (Smartphones, Solid-State Drives (PC and Console), Enterprise / Data-Center SSD, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific contributed 55.40% of sales in 2025, anchored by South Korea's vertically-integrated champions and China's colossal device assembly base. Samsung's mass production of 9th-generation V-NAND (286 layers) and SK Hynix's 321-layer TLC line affirm the region's technology lead. Beijing's domestic champion YMTC pushes 232-layer QLC nodes despite export-control constraints, illustrating indigenous capacity expansion that preserves Asia-Pacific's outsized influence on the NAND flash memory market.

North America sits second on revenue league tables, propelled by cloud capital-expenditure intensity. The CHIPS and Science Act bankrolls Micron's USD 125 billion state-side megafab roadmap, lifting U.S. advanced-memory self-sufficiency by 2035. Canada contributes controller-IP design talent, while Mexico scales module-level assembly lines under USMCA provisions, together reinforcing regional supply diversification.

Europe registers mid-single-digit share, constrained by limited memory wafer fabrication. Nonetheless, automotive and industrial OEMs in Germany and France generate robust demand for auto-grade NVMe modules. Sustainability directives such as the European Green Deal pivot buyers toward power-efficient PCIe 5.0 SSDs that lower rack energy density, a niche European fabs aim to capture through next-generation 3D NAND nodes with under-3 pJ/bit read energy footprints.

The Middle East and Africa present the highest growth rate at 8.21% CAGR. Saudi Arabia's Vision 2030 underwrites wafer-to-back-end complexes around Riyadh, while Abu Dhabi's sovereign investors explore joint-ventures with controller specialists to bootstrap a regional supply chain. Ample renewable-energy pipelines and attractive tax regimes draw packaging partners, setting the stage for localized production that boosts the NAND flash memory market penetration across GCC data hubs.

- Samsung Electronics Co., Ltd.

- SK hynix Inc.

- KIOXIA Holdings Corporation

- Western Digital Corporation

- Micron Technology, Inc.

- Nanya Technology Corporation

- Powerchip Technology Corporation

- Winbond Electronics Corporation

- Macronix International Co., Ltd.

- Silicon Motion Technology Corp.

- Phison Electronics Corp.

- Kingston Technology Company, Inc.

- ADATA Technology Co., Ltd.

- Transcend Information, Inc.

- GigaDevice Semiconductor Inc.

- SK Group (Solid-State Storage division)

- PNY Technologies, Inc.

- Team Group Inc.

- Longsys Electronics Co., Ltd.

- Smart Modular Technologies, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Data-center AI/ML storage surge

- 4.2.2 5G and massive-IoT device proliferation

- 4.2.3 PC/Console transition from HDD to SSD

- 4.2.4 Enterprise pivot to cost-efficient QLC SSDs

- 4.2.5 National on-shore NAND fab programs

- 4.2.6 CXL-enabled computational storage adoption

- 4.3 Market Restraints

- 4.3.1 Endurance limits of high-density cells

- 4.3.2 Pricing cyclicality and cap-ex burden

- 4.3.3 Export-control induced equipment bottlenecks

- 4.3.4 Sustainability scrutiny on high-layer fabs

- 4.4 Industry Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 SLC (Single-Level Cell)

- 5.1.2 MLC (Multi-Level Cell)

- 5.1.3 TLC (Triple-Level Cell)

- 5.1.4 QLC (Quad-Level Cell)

- 5.2 By Structure

- 5.2.1 2D (Planar) NAND

- 5.2.2 3D NAND

- 5.3 By Interface

- 5.3.1 SATA

- 5.3.2 PCIe / NVMe

- 5.3.3 UFS / eMMC

- 5.4 By Application

- 5.4.1 Smartphones

- 5.4.2 Solid-State Drives (PC and Console)

- 5.4.3 Enterprise / Data-center SSD

- 5.4.4 Memory Cards and USB Drives

- 5.4.5 Industrial and Automotive Electronics

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 South-East Asia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Samsung Electronics Co., Ltd.

- 6.4.2 SK hynix Inc.

- 6.4.3 KIOXIA Holdings Corporation

- 6.4.4 Western Digital Corporation

- 6.4.5 Micron Technology, Inc.

- 6.4.6 Nanya Technology Corporation

- 6.4.7 Powerchip Technology Corporation

- 6.4.8 Winbond Electronics Corporation

- 6.4.9 Macronix International Co., Ltd.

- 6.4.10 Silicon Motion Technology Corp.

- 6.4.11 Phison Electronics Corp.

- 6.4.12 Kingston Technology Company, Inc.

- 6.4.13 ADATA Technology Co., Ltd.

- 6.4.14 Transcend Information, Inc.

- 6.4.15 GigaDevice Semiconductor Inc.

- 6.4.16 SK Group (Solid-State Storage division)

- 6.4.17 PNY Technologies, Inc.

- 6.4.18 Team Group Inc.

- 6.4.19 Longsys Electronics Co., Ltd.

- 6.4.20 Smart Modular Technologies, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

2026年低密度SLC NAND快闪记忆体快闪记忆体全球市场报告

2026年低密度SLC NAND快闪记忆体快闪记忆体全球市场报告 128TB SSD市场按介面类型、外形规格、应用和最终用户分類的全球预测(2026-2032年)

128TB SSD市场按介面类型、外形规格、应用和最终用户分類的全球预测(2026-2032年) 区域闪光灯市场分析及至2035年预测:按类型、产品、服务、技术、组件、应用、部署、最终用户和功能划分

区域闪光灯市场分析及至2035年预测:按类型、产品、服务、技术、组件、应用、部署、最终用户和功能划分 人工智慧重塑记忆体格局:市场收入预计在 2027 年达到峰值

人工智慧重塑记忆体格局:市场收入预计在 2027 年达到峰值 3D NAND 记忆体市场 - 全球产业规模、份额、趋势、机会及预测(按类型、应用、最终用户、地区和竞争格局划分),2021-2031 年NAND快闪记忆体市场 - 全球产业规模、份额、趋势、机会及预测(按类型、应用、产业垂直领域、地区和竞争格局划分,2021-2031年)NAND快闪记忆体主晶片市场(按NAND类型、应用、介面、最终用户、封装类型和密度划分),全球预测,2026-2032年储存加速器市场:依加速器类型、外形尺寸、记忆体技术、部署模式、组织规模、应用领域和最终用户产业划分-2026-2032年全球预测

3D NAND 记忆体市场 - 全球产业规模、份额、趋势、机会及预测(按类型、应用、最终用户、地区和竞争格局划分),2021-2031 年NAND快闪记忆体市场 - 全球产业规模、份额、趋势、机会及预测(按类型、应用、产业垂直领域、地区和竞争格局划分,2021-2031年)NAND快闪记忆体主晶片市场(按NAND类型、应用、介面、最终用户、封装类型和密度划分),全球预测,2026-2032年储存加速器市场:依加速器类型、外形尺寸、记忆体技术、部署模式、组织规模、应用领域和最终用户产业划分-2026-2032年全球预测 NAND快闪记忆体(2026):人工智慧和硬碟短缺推动价格上涨

NAND快闪记忆体(2026):人工智慧和硬碟短缺推动价格上涨 高容量SSD的登场:AI储存·解决方案和NAND快闪记忆体

高容量SSD的登场:AI储存·解决方案和NAND快闪记忆体