|

市场调查报告书

商品编码

1910535

机器人流程自动化 (RPA) – 市场占有率分析、产业趋势与统计、成长预测 (2026-2031)Robotic Process Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

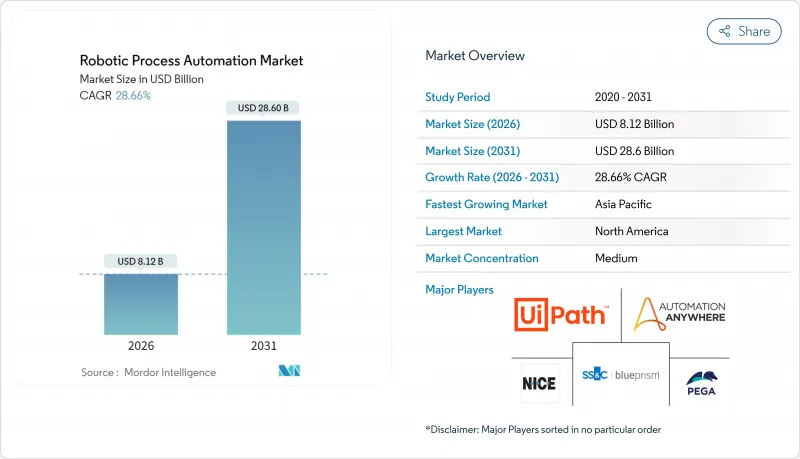

预计到 2025 年,机器人流程自动化 (RPA) 市场价值为 63.1 亿美元,到 2026 年将成长至 81.2 亿美元,到 2031 年将达到 286 亿美元,预测期(2026-2031 年)的复合年增长率为 28.66%。

生成式人工智慧与现有RPA平台的日益融合,正在拓展可自动化任务的范围,使企业能够处理以往需要人工干预的非结构化流程。云端原生部署缩短了引进週期,并将支出转移到营运预算中,也推动了市场扩张。北美地区凭藉着严格的合规要求和成熟的技术生态系统,预计到2024年将占据机器人流程自动化市场39.6%的最大份额。同时,亚太地区在政府支持的自动化项目以及中小企业采用计量收费机器人的推动下,实现了34.5%的最高区域复合年增长率。供应商之间的竞争日益激烈,各公司透过专注于人工智慧的收购和合作,将智慧文件处理、低程式码设计和自主代理功能整合到其平台蓝图中。

全球机器人流程自动化市场趋势与洞察

零售全通路订单履行自动化

为了满足消费者对即时购物的需求,零售商正在实现库存核对、出货协调和退货管理的自动化。 Grupo Exito 在实施了一项企业级 RPA 专案后,将订单处理时间缩短了高达 75%。此专案将电商前端与原有 ERP 资料连接起来。即使在高峰期,电脑视觉模组的整合也能保持 98% 以上的准确率,而人工智慧辅助的需求预测则有助于在供应链波动的情况下管理利润率。因此,无论是在成熟市场还是新兴电商市场,零售商都将自动化视为应对物流中断和劳动力短缺的必要措施。

中小企业采用云端原生RPA平台

计量收费的SaaS模式降低了中小企业的进入门槛。 Jana Small Finance Bank在迁移到UiPath云端服务后,关键流程的处理时间缩短了约70%,而且无需任何本地基础设施。超大规模服务供应商正在将RPA整合到其市场中,使中小企业能够在几天内部署安全的机器人,并仅根据交易量的成长扩展许可证。分析师预测,到2027年,随着公民开发者工具的成熟和产业专用的模板的普及,中小企业将推动超过40%的新机器人部署。

由于使用者介面变更,机器人问题持续存在。

企业和SaaS应用中频繁的介面更新会导致选择器失效,使机器人无法运行,从而导致高达40%的年度自动化预算被用于被动维护。 Tarsus Distribution由于供应商格式变更被迫重新设计其发票工作流程,凸显了其旧版萤幕抓取机器人的脆弱性。儘管新世代平台增加了物件式的选择器和自癒功能,但缺乏变更管理仍然会拖慢扩展计画的步伐,并降低人们对早期专案的信心。

细分市场分析

在机器人流程自动化 (RPA) 市场,受监管产业对本地管理的需求驱动,到 2025 年,本地部署仍将占据主导地位,市场占有率达 53.62%。然而,随着安全认证的普及,云端部署将以 36.95% 的复合年增长率 (CAGR) 实现最高成长,并缩小与本地部署的差距。据 UiPath 称,超过 80% 的新契约来自云端订阅,客户的部署速度比本地部署快 50%。混合模式正变得越来越流行,欧洲银行将敏感的支付工作流程保留在内部,同时利用云端租户进行设计、测试和分析。这种柔软性使企业能够在满足居住要求的同时,保持扩充性。

随着边缘运算技术的成熟,供应商开始提供轻量级执行环境,这些环境可在本地运行,但由云端进行编配。此类架构可降低工厂车间机器人的延迟,同时最大限度地减少伺服器管理开销。因此,许多製造商计划在未来三年内将其非生产机器人迁移到SaaS平台,因为SaaS简化了修补程式管理,并可即时获得AI升级。预计这一转变将推动订阅收入从永久授权收入成长,从而持续扩大机器人流程自动化市场。

到2025年,软体平台将占总营收的51.05%,而服务板块正以34.1%的复合年增长率快速成长,因为各组织逐渐意识到以人为本的变革管理是成功的关键。采用者正越来越多地整合探索、重塑和公民开发者辅导,这些环节合计约占整体转型预算的60%。 SS&C Technologies将Blue Prism软体与咨询服务结合,使其机器人数量增加了两倍,并节省了1亿美元的成本。

对持续改进服务合约的需求也在不断增长,因为持续调整人工智慧模型对于智慧自动化至关重要。供应商现在提供的託管服务是基于服务等级协定 (SLA) 而非单一计划里程碑来保证成果。这种转变进一步扩大了 RPA 服务市场的份额,并凸显了该行业从工具实施向企业级业务模式重塑的演变。

机器人流程自动化市场按部署类型(本地部署/云端部署/SaaS)、解决方案组件(软体/服务)、公司规模(中小企业/大型企业)、技术类型(有人值守RPA/无人值守RPA/智慧RPA/认知RPA)、最终用户产业(金融/保险/证券/IT/电信/医疗保健等)和地区进行细分。市场预测以美元计价。

区域分析

北美地区在2025年仍保持领先地位,市占率达到39.12%,主要得益于早期采用趋势以及政府和金融服务领域严格的合规要求。例如,美国住房与城市发展部等机构正在采用RPA和机器学习相结合的方法来改善福利处理流程。加州机动车辆管理局(DMV)等州级机构则利用机器人来加速数位化驾照发放服务,从而确保在疫情期间业务的持续运作。供应商格局受益于丰富的系统整合能力和熟练的自动化专业人员,这将确保市场持续成长。

亚太地区是成长最快的地区,复合年增长率高达33.6%。日本的RPA(机器人流程自动化)解决方案「Robopat DX」在中小企业中的安装量已超过1700套,这表明在人手不足的市场中,该技术拥有强大的市场基础。印度马尼帕尔医院已实现财务工作流程自动化,以符合不断改进的数位化医疗法规。政府补贴和对本地语言介面的支持预计将进一步推动製造业和外包地区的RPA应用,从而进一步扩大该地区的RPA市场。

欧洲的发展趋势正受到《数位业务韧性法案》的影响,该法案要求银行记录并对其自动化工作流程进行压力测试。金融机构已拨出高达1500万欧元的多年预算,以确保在2025年之前达到合规要求。德国製造商正在推动后勤部门营运的进阶自动化,北欧医疗保健系统则在各地区部署共用的机器人库。混合部署结构(资料储存在本地,但透过云端主机进行管理)正逐渐成为常态,机器人流程自动化市场在欧盟成员国的份额也在稳步增长。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 全通路零售中的订单履行自动化

- 中小企业云端原生RPA平台采用现状

- 基于生成式人工智慧的机器人设计助手

- 超大规模市场的计量收费机器人

- DORA 和 HIPAA 的合规主导自动化

- 全球共用服务中心人才短缺

- 市场限制

- 由于使用者介面变更,机器人问题持续存在。

- 无人机器人的管治与伦理监督

- 从传统RPA套件转换过来成本高昂

- 新兴市场流程标准化程度低

- 产业价值链分析

- 监管环境

- 技术展望

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 宏观经济因素如何影响市场

第五章 市场规模与成长预测

- 透过部署

- 本地部署

- 云/SaaS

- 按解决方案组件

- 软体(平台和许可)

- 服务(实施、卓越中心、支援)

- 按公司规模

- 中小企业

- 大公司

- 依技术类型

- 参加了RPA

- 无人值守的RPA

- 智慧型/认知型RPA

- 按最终用户行业划分

- BFSI

- 资讯科技和电信

- 卫生保健

- 零售与消费品包装 (CPG)

- 製造业

- 其他终端用户产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 新加坡

- 马来西亚

- 澳洲

- 亚太其他地区

- 中东和非洲

- 中东

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- UiPath Inc.

- Automation Anywhere Inc.

- SS&C Blue Prism Ltd.

- NICE Ltd.(Robotic Automation)

- Pegasystems Inc.

- Kofax Inc.

- WorkFusion Inc.

- Kryon Systems Ltd.

- EdgeVerve Systems Ltd.

- AntWorks Pte Ltd.

- Laiye Technology Ltd.

- Cyclone Robotics Co. Ltd.

- AutomationEdge Technologies Inc.

- Datamatics Global Services Ltd.

- Nividous Software Solutions

- Soroco

- Redwood Software Inc.

- Microsoft Corp.(Power Automate)

- Servicetrace GmbH

- Jidoka(Novayre Solutions)

- Fortra LLC(ex-HelpSystems)

- ElectroNeek Robotics Inc.

- Robocorp Technologies Inc.

- Robiquity Ltd.

- Rocketbot SpA

- OpenConnect Systems Inc.

第七章 投资分析

第八章:市场机会与未来趋势

- 评估差距和未满足的需求

The Robotic Process Automation Market was valued at USD 6.31 billion in 2025 and estimated to grow from USD 8.12 billion in 2026 to reach USD 28.6 billion by 2031, at a CAGR of 28.66% during the forecast period (2026-2031).

Increasing integration of generative AI with established RPA platforms widens the range of automatable tasks and lets enterprises address unstructured processes that once required human intervention. Expansion is also fueled by cloud-native deployments that shorten implementation cycles and shift spending to operating budgets. North America held the largest Robotic Process Automation market share at 39.6% in 2024, supported by stringent compliance mandates and mature technology ecosystems, while Asia-Pacific is registering the fastest regional CAGR of 34.5% as governments sponsor automation programs and SMEs adopt pay-as-you-go bots. Vendor competition is intensifying through AI-focused acquisitions and partnerships that bundle intelligent document processing, low-code design, and autonomous agent capabilities into platform roadmaps.

Global Robotic Process Automation Market Trends and Insights

Retail Omni-Channel Order-Fulfilment Automation

Retailers are automating inventory reconciliation, shipment orchestration, and return management to keep pace with real-time consumer expectations. Grupo Exito cut order-processing times by up to 75% after deploying an enterprise-wide RPA program that links e-commerce front ends with legacy ERP data. Integration of computer-vision modules maintains accuracy above 98% during peak seasons, while AI-assisted demand forecasting helps retailers manage margin pressure amid supply-chain volatility. Retailers in both mature and emerging e-commerce markets, therefore, view automation as an essential hedge against logistics disruptions and labor shortages.

SME Adoption of Cloud-Native RPA Platforms

Consumption-based SaaS models are lowering entry barriers for small firms. Jana Small Finance Bank shortened critical process turnaround times by nearly 70% after migrating to UiPath's cloud service, with no on-premise infrastructure required. As hyperscale providers embed RPA into their marketplaces, SMEs can deploy secure bots within days and scale licenses only when transaction volumes rise. Analysts expect SMEs to drive more than 40% of net-new bot deployments by 2027 as citizen-developer tools mature and industry-specific templates proliferate.

Persistent Bot Breakage from UI Changes

Frequent interface updates in enterprise and SaaS apps disrupt selectors and render bots inoperable, consuming up to 40% of annual automation budgets for reactive maintenance. Tarsus Distribution had to redesign invoice workflows when supplier formats shifted, highlighting the fragility of legacy, screen-scraping bots. Newer platforms add object-based selectors and self-healing functions, yet change-management shortcomings continue to delay scaling plans and erode confidence in early-stage programs.

Other drivers and restraints analyzed in the detailed report include:

- Gen-AI-Powered Bot-Design Assistants

- Pay-as-You-Go Bots on Hyperscale Marketplaces

- Governance and Ethical Scrutiny of Unattended Bots

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-premise installations remained dominant at 53.62% of the Robotic Process Automation market in 2025 because heavily regulated sectors required local control. Cloud deployments nevertheless posted the highest 36.95% CAGR and will narrow the gap as security certifications expand. UiPath stated that more than 80% of new bookings stem from cloud subscriptions, and customers achieve rollouts 50% faster than on-premise equivalents. The hybrid pattern is gaining ground as European banks keep sensitive payment workflows in-house while using cloud tenants for design, test, and analytics. This flexibility lets firms satisfy residency mandates without forfeiting elastic capacity.

As edge computing matures, vendors package lightweight run-times that execute locally yet receive orchestration from the cloud. Such architectures reduce latency for factory-floor bots while minimizing server administration overhead. Consequently, many manufacturers plan to migrate their non-production robots to SaaS within three years, citing simplified patching and immediate access to AI upgrades. The resulting shift will continue to boost the Robotic Process Automation market as subscription revenue overtakes perpetual licenses.

Software platforms controlled 51.05% of revenue in 2025, but services are expanding at a 34.1% CAGR as organizations recognize that people-centric change management dictates success. Implementers increasingly bundle discovery, re-engineering, and citizen-developer coaching, representing roughly 60% of total transformation budgets. SS&C Technologies realized USD 100 million in cost savings by pairing Blue Prism software with advisory services that tripled its bot count.

Demand for continuous-improvement retainers is also rising because intelligent automation requires ongoing AI model tuning. Vendors now position managed service offers that guarantee SLA-based outcomes rather than discrete project milestones. This pivot further inflates the Robotic Process Automation market size allocated to services and underscores the sector's progression from tool adoption toward enterprise-wide operating model redesign.

Robotic Process Automation Market is Segmented by Deployment (On-Premise and Cloud/SaaS), Solution Component (Software and Services), Enterprise Size (Small and Medium Enterprises and Large Enterprises), Technology Type (Attended RPA, Unattended RPA, and Intelligent/Cognitive RPA), End-User Industry (BFSI, IT and Telecom, Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained leadership with a 39.12% share in 2025, propelled by early adoption curves and rigorous compliance mandates across government and financial services. Agencies such as the U.S. Department of Housing and Urban Development employ combined RPA and machine-learning approaches to modernize benefit processing. State entities like the California DMV leveraged bots to accelerate digital licensing services, allowing continuity during pandemic disruptions. The vendor landscape benefits from abundant system-integrator capacity and skilled automation professionals, ensuring continuous pipeline growth.

Asia-Pacific is the fastest-growing geography at 33.6% CAGR. Japan's RPA Robopat DX passed 1,700 SME implementations, signaling grassroots demand in a tight labor market. India's Manipal Hospitals automated finance workflows to comply with expanding digital health regulations. Government subsidy schemes and local-language interface support will further widen adoption among manufacturers and outsourcing hubs, magnifying the Robotic Process Automation market in the region.

Europe's trajectory is shaped by the Digital Operational Resilience Act, which compels banks to document and stress-test automated workflows. Institutions have earmarked multi-year budgets reaching EUR 15 million per entity to meet the 2025 compliance deadline. German manufacturers showcase deep back-office automation, while Nordic healthcare systems deploy region-wide shared-bot libraries. Hybrid deployment structures that retain data on-premise yet orchestrate via cloud consoles are becoming the norm, steadily increasing the Robotic Process Automation market presence across European Union member states.

- UiPath Inc.

- Automation Anywhere Inc.

- SS&C Blue Prism Ltd.

- NICE Ltd. (Robotic Automation)

- Pegasystems Inc.

- Kofax Inc.

- WorkFusion Inc.

- Kryon Systems Ltd.

- EdgeVerve Systems Ltd.

- AntWorks Pte Ltd.

- Laiye Technology Ltd.

- Cyclone Robotics Co. Ltd.

- AutomationEdge Technologies Inc.

- Datamatics Global Services Ltd.

- Nividous Software Solutions

- Soroco

- Redwood Software Inc.

- Microsoft Corp. (Power Automate)

- Servicetrace GmbH

- Jidoka (Novayre Solutions)

- Fortra LLC (ex-HelpSystems)

- ElectroNeek Robotics Inc.

- Robocorp Technologies Inc.

- Robiquity Ltd.

- Rocketbot SpA

- OpenConnect Systems Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Retail omni-channel order-fulfilment automation

- 4.2.2 SME adoption of cloud-native RPA platforms

- 4.2.3 Gen-AI powered bot-design assistants

- 4.2.4 Pay-as-you-go bots on hyperscale marketplaces

- 4.2.5 Compliance-driven automation post-DORA and HIPAA

- 4.2.6 Global talent shortages in shared-service centres

- 4.3 Market Restraints

- 4.3.1 Persistent bot breakage from UI changes

- 4.3.2 Governance and ethical scrutiny of unattended bots

- 4.3.3 High switching cost from legacy RPA suites

- 4.3.4 Low process standardisation in emerging markets

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Deployment

- 5.1.1 On-premise

- 5.1.2 Cloud/SaaS

- 5.2 By Solution Component

- 5.2.1 Software (Platforms and Licences)

- 5.2.2 Services (Implementation, CoE, Support)

- 5.3 By Enterprise Size

- 5.3.1 Small and Medium Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By Technology Type

- 5.4.1 Attended RPA

- 5.4.2 Unattended RPA

- 5.4.3 Intelligent/Cognitive RPA

- 5.5 By End-user Industry

- 5.5.1 BFSI

- 5.5.2 IT and Telecom

- 5.5.3 Healthcare

- 5.5.4 Retail and CPG

- 5.5.5 Manufacturing

- 5.5.6 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Singapore

- 5.6.4.6 Malaysia

- 5.6.4.7 Australia

- 5.6.4.8 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 UiPath Inc.

- 6.4.2 Automation Anywhere Inc.

- 6.4.3 SS&C Blue Prism Ltd.

- 6.4.4 NICE Ltd. (Robotic Automation)

- 6.4.5 Pegasystems Inc.

- 6.4.6 Kofax Inc.

- 6.4.7 WorkFusion Inc.

- 6.4.8 Kryon Systems Ltd.

- 6.4.9 EdgeVerve Systems Ltd.

- 6.4.10 AntWorks Pte Ltd.

- 6.4.11 Laiye Technology Ltd.

- 6.4.12 Cyclone Robotics Co. Ltd.

- 6.4.13 AutomationEdge Technologies Inc.

- 6.4.14 Datamatics Global Services Ltd.

- 6.4.15 Nividous Software Solutions

- 6.4.16 Soroco

- 6.4.17 Redwood Software Inc.

- 6.4.18 Microsoft Corp. (Power Automate)

- 6.4.19 Servicetrace GmbH

- 6.4.20 Jidoka (Novayre Solutions)

- 6.4.21 Fortra LLC (ex-HelpSystems)

- 6.4.22 ElectroNeek Robotics Inc.

- 6.4.23 Robocorp Technologies Inc.

- 6.4.24 Robiquity Ltd.

- 6.4.25 Rocketbot SpA

- 6.4.26 OpenConnect Systems Inc.

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 8.1 White-Space and Unmet-Need Assessment

IT机器人自动化市场分析与预测(至2035年):按类型、产品类型、服务、技术、组件、应用、流程、部署类型和最终用户划分机器人流程自动化市场分析及预测(至2035年):依类型、产品类型、服务、技术、元件、应用、部署类型、最终使用者、功能与模式划分

IT机器人自动化市场分析与预测(至2035年):按类型、产品类型、服务、技术、组件、应用、流程、部署类型和最终用户划分机器人流程自动化市场分析及预测(至2035年):依类型、产品类型、服务、技术、元件、应用、部署类型、最终使用者、功能与模式划分 RPA(机器人流程自动化)市场规模、份额和趋势分析报告:按类型、部署、营运、企业规模、最终用途、地区和细分市场预测(2026-2033 年)

RPA(机器人流程自动化)市场规模、份额和趋势分析报告:按类型、部署、营运、企业规模、最终用途、地区和细分市场预测(2026-2033 年) 智慧型手机製造机器人流程自动化市场-全球产业规模、份额、趋势、机会及预测(按机器人类型、组件、公司规模、地区和竞争格局划分,2021-2031年)

智慧型手机製造机器人流程自动化市场-全球产业规模、份额、趋势、机会及预测(按机器人类型、组件、公司规模、地区和竞争格局划分,2021-2031年) 机器人流程自动化(RPA)市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测(2026–2034)金融、保险和房地产行业机器人流程自动化市场-全球产业规模、份额、趋势、机会及预测(按类型、部署方式、组织、应用、地区和竞争格局划分,2021-2031年)

机器人流程自动化(RPA)市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测(2026–2034)金融、保险和房地产行业机器人流程自动化市场-全球产业规模、份额、趋势、机会及预测(按类型、部署方式、组织、应用、地区和竞争格局划分,2021-2031年) 日本机器人流程自动化市场按组件、操作、部署模式、组织规模、最终用户和地区划分,2026-2034 年

日本机器人流程自动化市场按组件、操作、部署模式、组织规模、最终用户和地区划分,2026-2034 年 监管报告自动化市场预测至2032年:按解决方案类型、部署模式、技术、最终用户和地区分類的全球分析认知机器人市场-全球产业规模、份额、趋势、机会和预测,按学习类型、应用、地区和竞争格局划分,2020-2030年预测机器人流程自动化市场-2025-2030年预测

监管报告自动化市场预测至2032年:按解决方案类型、部署模式、技术、最终用户和地区分類的全球分析认知机器人市场-全球产业规模、份额、趋势、机会和预测,按学习类型、应用、地区和竞争格局划分,2020-2030年预测机器人流程自动化市场-2025-2030年预测