|

市场调查报告书

商品编码

1910549

功率模组封装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Power Module Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

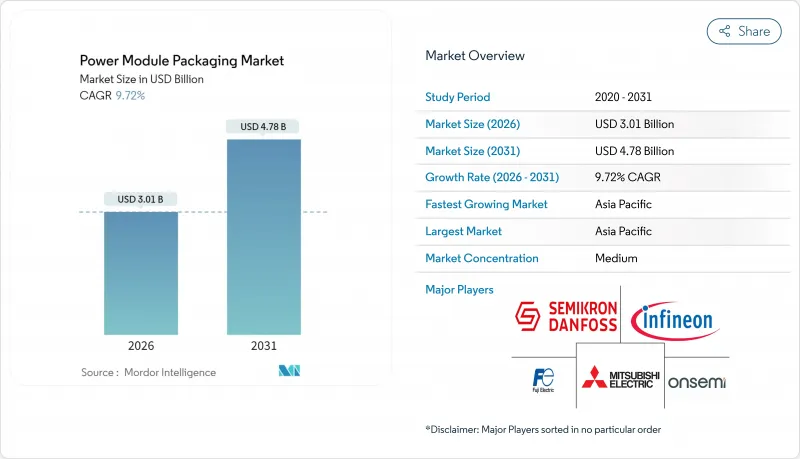

预计到 2026 年,功率模组封装市场规模将达到 30.1 亿美元,高于 2025 年的 27.4 亿美元。预计到 2031 年,该市场规模将达到 47.8 亿美元,2026 年至 2031 年的复合年增长率为 9.72%。

随着宽能带隙半导体从利基市场走向主流市场,电动车采用800V架构,以及工业马达驱动装置优先考虑能源效率,市场需求正在加速成长。能够实现低热阻、高电流密度以及在200°C以上高温下可靠运行的封装创新正成为关键的竞争优势,尤其是在汽车製造商寻求小型化而不牺牲使用寿命可靠性的情况下。地域多角化,特别是马来西亚、印度和印尼的多元化,透过扩大製造地和降低地缘政治风险,进一步推动了市场发展。竞争格局正在发生变化,碳化硅(SiC)和氮化镓(GaN)装置对传统硅解决方案的利润率构成压力,而氮化铝等先进陶瓷基板则透过实现双面冷却设计而不断扩大市场份额。

全球功率模组封装市场趋势与洞察

加速在电动车驱动逆变器中采用碳化硅和氮化镓功率装置

随着汽车製造商优先考虑延长续航里程和提升快速充电能力,碳化硅(SiC)在电池式电动车(BEV)领域正日益普及。特斯拉的初步演示数据显示,与硅基IGBT相比,SiC的续航里程提升了约7%,这一里程碑式的成绩推动了整个行业的广泛应用,儘管SiC装置的成本更高。弗劳恩霍夫研究所改良的直接冷却变频器架构透过取消底板,将效率提升至99.5%,这显示封装技术的进步能够直接转化为动力系统性能的提升。向800V汽车系统的广泛过渡带来了绝缘和局部放电方面的挑战,而这些挑战只有透过先进的基板和低电感互连技术才能解决,从而推动了对高端模组的需求。随着越来越多的原始设备製造商(OEM)推出900V电池组,将SiC晶粒与双面冷却封装相结合的供应商将占据有利地位,确保长期设计应用。

对节能型工业马达驱动装置的需求日益增长

电动马达约占全球工业电力消耗量的70%,专家估计,如果普遍采用变速驱动器,其发电量可抵销数座中型发电厂的发电量。然而,已开发国家仅有15%的三相马达采用了电子调速技术,这意味着巨大的潜力尚未充分开发。在冷暖气空调(HVAC)等变负载应用中,基于碳化硅(SiC)的驱动模组可实现15%至40%的节能,因为在这些应用中,压缩机很少满载运作。第七代车规级IGBT技术提高了允许的结温,从而可以使用更小的散热器和更紧凑的机柜设计,进而降低安装成本。政府的能源效率法规和不断上涨的电费持续推动高性能封装技术的发展,以确保产品在20年的工业运作週期内保持可靠性。

先进包装设备需要高资本投资

根据SEMI的预测,300毫米晶圆厂的产能正在成长,其中一部分产能将分配给雷射切割和混合键合线等先进封装设备。宽能带隙装置需要烧结炉能够处理超过250°C的温度,且拾放精度需达到±3μm以内,这提高了新製造商的进入门槛。电动车电池工厂也面临类似的资本投资负担,显示资本密集度是整个电气化价值链上的系统性障碍。资金筹措壁垒在缺乏成熟半导体产业丛集的地区尤为突出,这延缓了南亚和拉丁美洲的多元化发展目标,并限制了这些地区近期的产能扩张。

细分市场分析

到2025年,基板将占总收入的27.85%,这巩固了其在热控制和电隔离方面的核心地位。晶片贴装预计将成为成长最快的组件,复合年增长率将达到10.96%,因为银烧结和瞬态液相键合技术使得晶片能够在200°C以上温度下运行,而无需使用铅基合金。基板正逐渐被直接基板冷却方法所取代,这种方法缩短了热路径;而陶瓷封装能够降低结温12 K,其应用也日益广泛,尤其是在高功率风力发电转换器领域。

采用铜夹的先进平面互连技术消除了焊线的可靠性缺陷,提高了电流密度,并减少了电动车驱动逆变器的封装面积。导热界面材料演变为奈米结构碳网络,其理论电阻值接近 0.1 mm²K/W,从而延长了高循环应力下的使用寿命。由于原始设备製造商 (OEM) 要求对散热层迭性能承担单一责任,因此能够垂直整合基板压制、金属化和烧结贴装服务的供应商正在赢得合约。这种综合办法在低功耗消费性电子领域日益增长的商品化压力下,保护了供应商的利润空间。

在功率模组封装市场,IGBT模组凭藉着成熟的生产线和1,200V以下应用领域的有利成本优势,预计到2025年将维持36.88%的市场份额。然而,SiC模组到2031年将以10.52%的复合年增长率成长,其在电动车动力系统和快速充电器中具有更高的开关速度和显着降低的导通损耗。 GaN模组的成长主要得益于市场对高频通讯整流器日益增长的需求,而英飞凌对GaN Systems的收购将进一步巩固其竞争地位。

在对成本要求较高的家电和消费电源领域,Si-MOSFET模组依然具有吸引力;而在高压直流输电线路和感应加热等应用中,闸流体继续发挥重要作用,因为在这些应用中,可靠性比开关速度更为重要。预计在十年内,向200mm SiC晶圆的过渡将使其在成本上与硅晶圆相媲美。然而,汽车级SiC晶圆的产量比率仍是其大规模生产的一大障碍。因此,对于宽能带隙半导体晶圆厂而言,能够提供先进侦测能力并实现零ppm缺陷目标的封装公司至关重要。

区域分析

预计到2025年,亚太地区将占全球支出的48.35%,年复合成长率达11.37%,主要得益于中国OSAT生态系统受益于人工智慧伺服器和电动车的强劲成长动能。印度100亿美元的奖励计画以及美光在古吉拉突邦投资8.25亿美元建设晶圆厂,都显示印度政府正积极采取措施,力争在2027年前大幅提升后端产能。马来西亚则受惠于英特尔70亿美元的封装扩张计画以及美光在槟城的投资,正努力将自身打造成为一个能够有效缓解台海风险的互补型产业中心。

北美《晶片技术创新法案》(CHIPS Act)累计527亿美元,优先发展先进封装技术,以加强国内供应链。安姆科(Amcor)位于亚利桑那州、投资20亿美元的工厂计划于2026年运作,届时将生产人工智慧加速器模组。随着晶圆厂对关键设备的本地外包半导体测试与测试(OSAT)机构进行认证,预计区域市场份额将逐步成长。欧洲正致力于实现汽车碳化硅(SiC)供应链的自给自足,沃尔夫斯皮德(Wolfspeed)在德国投资30亿美元,建造一条符合原始设备製造商(OEM)电气化目标的外延片和模组生产线。欧洲版的《晶片技术创新法案》旨在协调各国的支持措施,但其资金规模仍低于美国,鼓励企业加强跨境合作。

中东和非洲地区正迎来基于吉瓦级太阳能和发电工程的蓬勃发展,新业务机会日益增加。併网逆变器对这些项目至关重要,海湾国家的主权财富基金正透过与经验丰富的组件製造商成立合资企业,建构本地组装系统。凭藉丰富的可再生能源资源,该地区正为未来的氢能出口奠定基础。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 加速采用碳化硅和氮化镓功率元件于电动车牵引逆变器

- 对节能型工业马达驱动装置的需求日益增长

- 与可再生能源相关的高功率逆变器的扩展

- 对电动车车载充电器小型化的需求

- 引入双面冷却基板可降低热阻

- 亚洲的本土化政策加强了国内包装供应链。

- 市场限制

- 先进包装设备需要高资本投资

- 一级OSAT厂商市场整合导致利润率承压

- 新型无铅晶片黏接材料在200°C以上温度下的可靠性问题

- 高导热陶瓷(AlN、Si3N4)供应瓶颈

- 产业价值链分析

- 监管环境

- 技术展望

- 宏观经济因素如何影响市场

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代产品和服务的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按组件

- 基板

- 底板

- 模具连接

- 基板安装

- 封装

- 互连

- 其他部件

- 按功率设备类型

- IGBT模组

- Si-MOSFET模组

- SiC模组

- 氮化镓模组

- 闸流体和其他模组

- 按功率范围

- <600 V

- 600-1200 V

- 1200-1700 V

- >1700 V

- 最终用户

- 车

- 产业

- 可再生能源

- 家用电子电器

- 资料中心和电信

- 铁路和交通运输

- 航太/国防

- 其他最终用户

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Infineon Technologies AG

- Mitsubishi Electric Corporation(Powerex Inc.)

- Fuji Electric Co. Ltd

- Semikron-Danfoss GmbH & Co. KG

- Hitachi Ltd(Power Electronics Systems)

- STMicroelectronics NV

- Amkor Technology Inc.

- ON Semiconductor Corporation

- Wolfspeed Inc.

- ROHM Semiconductor

- Texas Instruments Inc.

- Littelfuse Inc.(IXYS)

- Microchip Technology Inc.

- Nexperia BV

- Vishay Intertechnology Inc.

- Dynex Semiconductor Ltd

- Danfoss Silicon Power GmbH

- Power Integrations Inc.

- SanRex Corporation

- Alpha & Omega Semiconductor Ltd

- Kyocera Corporation

- Heraeus Electronics GmbH

- TT Electronics plc

- Advanced Power Electronics Corp.

- Shanghai Electric Power Semiconductor Device Co. Ltd

- Cissoid SA

- Celestica Inc.

第七章 市场机会与未来展望

Power Module Packaging market size in 2026 is estimated at USD 3.01 billion, growing from 2025 value of USD 2.74 billion with 2031 projections showing USD 4.78 billion, growing at 9.72% CAGR over 2026-2031.

Demand is accelerating as wide-bandgap semiconductors transition from a niche to a mainstream market, electric vehicles adopt 800V architectures, and industrial motor drives prioritize energy efficiency improvements. Packaging innovation that delivers lower thermal resistance, higher current density, and reliable operation beyond 200°C has become a decisive competitive advantage, especially as automotive OEMs demand smaller footprints without compromising lifetime reliability. Regional diversification, most notably in Malaysia, India, and Indonesia, adds further impetus by expanding the manufacturing footprint and reducing geopolitical risk. Competitive dynamics are shifting as SiC and GaN devices place legacy silicon solutions under margin pressure, while advanced ceramic substrates, such as aluminum nitride, capture market share by enabling double-sided cooling designs.

Global Power Module Packaging Market Trends and Insights

Accelerating Adoption of SiC and GaN Power Devices in EV Traction Inverters

SiC penetration in battery electric vehicles is increasing as OEMs prioritize range extension and fast-charge capability. Early field data from Tesla demonstrated roughly 7% range gain over silicon IGBT alternatives, a benchmark that triggered broad industry replication despite SiC's higher device cost. Fraunhofer's Enhanced Direct-cooling Inverter architecture increased efficiency to 99.5% by eliminating baseplates, demonstrating how packaging advances directly translate into drivetrain gains. Widespread migration to 800V vehicle systems raises insulation and partial discharge challenges that only advanced substrates and low-inductance interconnects can address, thereby boosting premium module demand. As more OEMs unveil 900-V battery packs, suppliers that marry SiC dies with double-sided-cooling packaging are positioned to secure long-term design wins.

Growing Demand for Energy-Efficient Industrial Motor Drives

Electric motors account for approximately 70% of global industrial power consumption, and experts estimate that the universal deployment of variable-speed drives could offset the equivalent output of several mid-sized power stations. Yet only 15% of three-phase motors in developed economies employ electronic speed control, leaving vast untapped potential. SiC-based drive modules deliver 15-40% energy savings across variable-load applications such as HVAC, where compressors seldom operate at full load. Generation 7 automotive-grade IGBT technology increases the permissible junction temperature, enabling smaller heatsinks and more compact cabinet designs, which in turn lower installation costs. Governments' efficiency mandates and rising electricity prices provide a durable tailwind for high-performance packaging that can guarantee reliability over 20-year industrial duty cycles.

High Capex Requirements for Advanced Packaging Equipment

SEMI forecasts that 300 mm fab equipment will increase with a rising slice earmarked for advanced packaging gear such as laser dicing and hybrid-bonding lines. Wide-bandgap devices require sintering ovens capable of profiles exceeding 250 °C and pick-and-place accuracy within +-3 µm, which raises the barrier to entry for newcomers. EV battery plants face parallel capex burdens, illustrating how capital intensity is a systemic hurdle across electrification value chains. Financing obstacles are felt most acutely in regions that lack mature semiconductor clusters, slowing diversification goals and tempering near-term capacity additions in South Asia and Latin America.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Renewable-Energy-Linked High-Power Inverters

- Miniaturisation Mandate from On-Board Chargers in E-Mobility Fleets

- Margin Squeeze Caused by Market Consolidation Among Tier-1 OSATs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Substrates captured 27.85% of 2025 revenue, underscoring their pivotal role in controlling heat and electrical isolation. Die attach is projected to post an 10.96% CAGR, the fastest component trajectory, as silver sintering and transient-liquid-phase bonding enable operation beyond 200 °C without the use of lead-based alloys. Baseplates are steadily displaced by direct-substrate-cooling schemes that collapse thermal paths, while ceramic encapsulants that pare junction temperature by 12 K widen their footprint, especially in high-power wind converters.

Advanced planar interconnects using copper clips eliminate wire-bond reliability weak points and enhance current density, thereby reducing package footprints within EV traction inverters. Thermal interface materials are evolving toward nano-structured carbon networks, nearing the theoretical resistance of 0.1 mm2K/W, which extends mission life under high-cycle stress. Suppliers that vertically integrate substrate pressing, metallization, and sintered attach services are winning contracts as OEMs demand single-source responsibility for thermal stack-up performance. The holistic approach safeguards supplier margins even as commoditization pressures intensify in lower-power consumer segments.

IGBT modules retained 36.88% of the 2025 value within the power module packaging market, buoyed by entrenched manufacturing lines and favorable cost curves for <=1200 V applications. Yet SiC modules will grow at a 10.52% CAGR through 2031, unlocking superior switching speeds and slashing conduction losses in EV drivetrains and fast chargers. GaN modules are witnessing growth in high-frequency telecom rectifier demand, with Infineon's acquisition of GaN Systems amplifying its competitive firepower.

Si-MOSFET modules remain attractive for cost-sensitive appliance and consumer power supplies, while thyristors retain relevance in HVDC links and induction heating, where ruggedness takes precedence over switching speed. The transition to 200 mm SiC wafers promises cost parity with silicon within the decade; however, automotive-grade SiC yields remain the gating factor for volume ramp. Packaging houses offering deep inspection competence and zero-ppm defect targets are, therefore, essential allies to wide-bandgap fab owners.

The Power Module Packaging Market Report is Segmented by Components (Substrate, Baseplate, Die Attach, and More), Power Device Type (IGBT Modules, Si-MOSFET Modules, and More), Power Range (< 600 V, 600 - 1200 V, 1200 - 1700 V, and More), End-User (Automotive, Industrial, and More), and Geography (North America, South America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

The Asia-Pacific region led with 48.35% of 2025 spending and is expected to compound at a 11.37% CAGR as China's OSAT ecosystem benefits from AI server and EV momentum. India's USD 10 billion incentive scheme and Micron's USD 825 million Gujarat plant underscore a policy drive that will add meaningful backend capacity by 2027. Malaysia is bolstered by Intel's USD 7 billion packaging expansion and Micron's investment in Penang, positioning the country as a complementary hub that can mitigate Taiwan Strait risk.

North America's CHIPS Act earmarks USD 52.7 billion and prioritizes advanced packaging to shore up domestic supply; Amkor's USD 2 billion Arizona site will handle AI accelerator modules when it comes online in 2026. Regional share is poised to rise modestly as fabs qualify local OSATs for critical installations. Europe focuses on automotive SiC supply-chain sovereignty, with Wolfspeed planning USD 3 billion for a German epi-wafer and module line that dovetails with OEM electrification targets. The European Chips Act aims to harmonize national incentives, yet it still lags behind U.S. funding levels, prompting companies to enhance cross-border collaboration.

The Middle East and Africa present emerging greenfield opportunities anchored in gigawatt-scale solar and wind projects that require grid-forming inverters. Gulf sovereign funds are exploring joint ventures with experienced module makers to establish local assembly, leveraging abundant renewable energy to power future hydrogen exports.

- Infineon Technologies AG

- Mitsubishi Electric Corporation (Powerex Inc.)

- Fuji Electric Co. Ltd

- Semikron-Danfoss GmbH & Co. KG

- Hitachi Ltd (Power Electronics Systems)

- STMicroelectronics N.V.

- Amkor Technology Inc.

- ON Semiconductor Corporation

- Wolfspeed Inc.

- ROHM Semiconductor

- Texas Instruments Inc.

- Littelfuse Inc. (IXYS)

- Microchip Technology Inc.

- Nexperia B.V.

- Vishay Intertechnology Inc.

- Dynex Semiconductor Ltd

- Danfoss Silicon Power GmbH

- Power Integrations Inc.

- SanRex Corporation

- Alpha & Omega Semiconductor Ltd

- Kyocera Corporation

- Heraeus Electronics GmbH

- TT Electronics plc

- Advanced Power Electronics Corp.

- Shanghai Electric Power Semiconductor Device Co. Ltd

- Cissoid SA

- Celestica Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating adoption of SiC and GaN power devices in EV traction inverters

- 4.2.2 Growing demand for energy-efficient industrial motor drives

- 4.2.3 Expansion of renewable-energy-linked high-power inverters

- 4.2.4 Miniaturisation mandate from on-board chargers in e-mobility fleets

- 4.2.5 Emergence of double-sided-cooling substrates lowering thermal resistance

- 4.2.6 Localisation policies in Asia boosting domestic packaging supply chains

- 4.3 Market Restraints

- 4.3.1 High capex requirements for advanced packaging equipment

- 4.3.2 Margin squeeze caused by market consolidation among Tier-1 OSATs

- 4.3.3 Reliability concerns over new lead-free die-attach materials > 200 °C

- 4.3.4 Supply bottlenecks for high-thermal-conductivity ceramics (AlN, Si3N4)

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitute Products and Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Components

- 5.1.1 Substrate

- 5.1.2 Baseplate

- 5.1.3 Die Attach

- 5.1.4 Substrate Attach

- 5.1.5 Encapsulations

- 5.1.6 Interconnections

- 5.1.7 Other Components

- 5.2 By Power Device Type

- 5.2.1 IGBT Modules

- 5.2.2 Si-MOSFET Modules

- 5.2.3 SiC Modules

- 5.2.4 GaN Modules

- 5.2.5 Thyristor and Other Modules

- 5.3 By Power Range

- 5.3.1 < 600 V

- 5.3.2 600 - 1200 V

- 5.3.3 1200 - 1700 V

- 5.3.4 > 1700 V

- 5.4 By End-user

- 5.4.1 Automotive

- 5.4.2 Industrial

- 5.4.3 Renewable Energy

- 5.4.4 Consumer Electronics

- 5.4.5 Data Centres and Telecom

- 5.4.6 Rail and Transportation

- 5.4.7 Aerospace and Defence

- 5.4.8 Other End-users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Infineon Technologies AG

- 6.4.2 Mitsubishi Electric Corporation (Powerex Inc.)

- 6.4.3 Fuji Electric Co. Ltd

- 6.4.4 Semikron-Danfoss GmbH & Co. KG

- 6.4.5 Hitachi Ltd (Power Electronics Systems)

- 6.4.6 STMicroelectronics N.V.

- 6.4.7 Amkor Technology Inc.

- 6.4.8 ON Semiconductor Corporation

- 6.4.9 Wolfspeed Inc.

- 6.4.10 ROHM Semiconductor

- 6.4.11 Texas Instruments Inc.

- 6.4.12 Littelfuse Inc. (IXYS)

- 6.4.13 Microchip Technology Inc.

- 6.4.14 Nexperia B.V.

- 6.4.15 Vishay Intertechnology Inc.

- 6.4.16 Dynex Semiconductor Ltd

- 6.4.17 Danfoss Silicon Power GmbH

- 6.4.18 Power Integrations Inc.

- 6.4.19 SanRex Corporation

- 6.4.20 Alpha & Omega Semiconductor Ltd

- 6.4.21 Kyocera Corporation

- 6.4.22 Heraeus Electronics GmbH

- 6.4.23 TT Electronics plc

- 6.4.24 Advanced Power Electronics Corp.

- 6.4.25 Shanghai Electric Power Semiconductor Device Co. Ltd

- 6.4.26 Cissoid SA

- 6.4.27 Celestica Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

功率模组封装市场-2025-2030年预测

功率模组封装市场-2025-2030年预测 汽车电源模组封装:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)

汽车电源模组封装:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年) 功率模组封装市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

功率模组封装市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测