|

市场调查报告书

商品编码

1910603

工具机:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Machine Tools - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

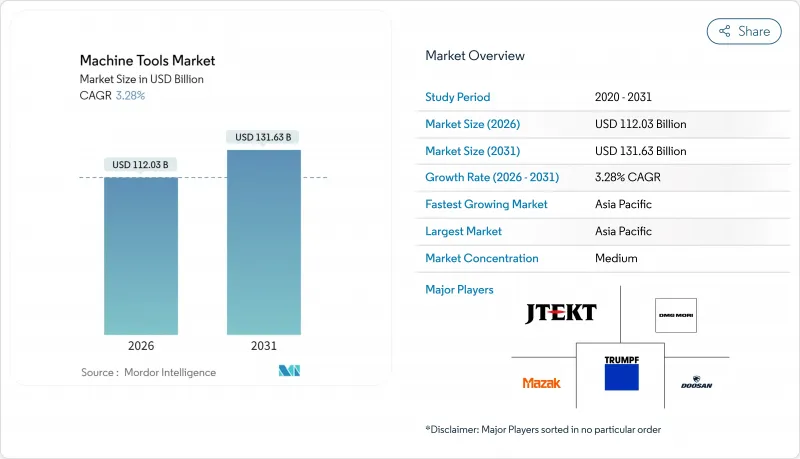

预计到 2026 年,工具机市场规模将达到 1,120.3 亿美元,高于 2025 年的 1,084.7 亿美元。预计到 2031 年,该市场规模将达到 1,316.3 亿美元,2026 年至 2031 年的复合年增长率为 3.28%。

这项扩张的背景是供应链重组、贸易规则趋严以及半导体晶圆厂投资创纪录,所有这些都需要超精密加工能力。 ASML 的高数值孔径 EUV 系统(每台售价超过 4 亿美元)就是一个典型的例子,它展现了下一代微影术技术如何提升奈米级金属切削和精加工性能的标准。汽车电气化和航太领域的现代化正在推动对多轴加工中心的需求,而工业 4.0计划也越来越多地采用人工智慧驱动的数控控制设备,以实现进给速度和刀具路径的自我优化。虽然亚洲占据了新增产能的大部分,但由于美国的回流激励政策和欧洲关税的不确定性,未来的需求正在转向更分散的工厂。儘管直销仍然是全球分销的主导方式,但电子商务平台正在加快中价位数控机床和替换刀具的采购週期。

全球工具机市场趋势与洞察

电气化的快速发展推动了精密电动动力传动系统加工。

电动汽车马达工厂需要微米等级的公差,通常将自动化定子插入和髮夹式绕线製程与五轴加工中心结合,因此无需二次表面处理工程。采埃孚的目标是到2030年实现其电动车传动系统70%的自动化,而中国供应商预计到2034年将年产超过1.2亿台马达。通用汽车和梅赛德斯-奔驰都已实现电机壳体的自主生产,并优先选择在切割铝硅合金时不会产生振动的工具机。为了抑制微米级几何误差引起的电磁噪声,对进程内测量、切削油管理和封闭回路型补偿的需求日益增长。

随着半导体製造厂的扩张,对超精密设备的需求日益增长。

预计到2027年,全球300毫米晶圆厂投资将达到1,370亿美元,其中美洲地区的投资预计将在三年内翻倍。 ASML的多吨级投影光学元件需要钻石车削和气浮研磨系统,以确保在一公尺行程内形状误差小于50奈米。台积电投资1,650亿美元的亚利桑那州工厂就是一个很好的例子,它展现了国家半导体计画如何创造对超精密加工工厂的本地需求,这些工厂能够将重型零件留在本州进行组装。洁净室相容性、静压滑轨和无污染润滑现在已成为服务于此细分市场的设备製造商的标准配置。

先进数控系统需要高额资本投入和较长的投资回收期。

根据亚特兰大联邦储备银行的一项调查,80%的製造商在做出资本支出决策前会考虑利率因素,而2025年基准利率上调进一步加剧了这一趋势。一套顶级的五轴加工单元安装成本可能超过300万美元,对于中等产量、按订单订单的工厂而言,投资回收期可能超过五年。设备即服务(EaaS)合约正逐渐成为过渡解决方案,但许多财务长仍然担心软体升级导致旧款控制器过时,从而带来残值风险。

细分市场分析

预计到2026年,多轴工具机市场规模将达到262.9亿美元,到2031年将以6.88%的复合年增长率成长。铣床仍是最大的收入来源,到2025年将维持28.05%的市占率。目前,成长主要集中在用于在一次装夹操作中完成复杂壳体精加工的五轴联动平台。汽车製造商正在采用多轴机床,以减少占地面积和搬运成本,并用电动驱动壳体单元取代内燃机缸体生产线。航太製造商正在部署高扭力倾斜主轴机床来加工钛合金翼梁,同时在1.2公尺长度上保持0.015毫米的平面度精度。工具车间操作员仍然依赖三轴膝式铣床,但配备数位显示器和探针功能的改造套件正在帮助他们在维护工作中保持竞争力。

随着人工智慧引导的参数嚮导降低薄不銹钢板的废品率,雷射切割系统的需求正在回升。电火花加工 (EDM) 在模腔加工领域仍占有一席之地,尤其适用于铣床难以经济高效加工的、需要小半径角落的加工。结合定向能量沉积和精铣的混合型工具机正逐渐进入原型实验室,其缩短的加工週期优势超过了设备成本。等离子切割和水刀切割平台在重工业领域得到应用,这两种技术都开始整合封闭回路型高度控制,以确保变形钢板的切割品质。

到2025年,CNC平台将占总营收的68.55%,复合年增长率达6.08%,巩固在工具机市场的核心地位。新兴控制器采用GPU加速演算法,可将STEP檔案直接转换为最佳化的刀具路径,显着缩短小批量零件的程式时间。中国第一自动化已筹集约1亿元人民币用于自主生产伺服驱动器和PLC堆栈,展现了其降低对海外韧体依赖风险的战略倡议。儘管小规模工厂和职业训练学校仍在使用传统的手动机床,甚至在购买新工具机时也不配备控制设备,但越来越多的厂商开始选择伺服相容的机架,以便日后进行升级改造。一种先进的混合迭层切割系统结合了雷射金属迭层和五轴加工技术,无需移除航太支架的支撑结构。

数位双胞胎技术能够模拟刀具挠曲和热膨胀,从而实现离线检验,防止原型製作阶段发生碰撞。 ChatCNC™外挂程式可自动辨识长方体形状,并自动产生从粗加工到精加工的加工流程,即使是经验不足的程式设计人员也能达到与专家媲美的加工週期。预测性维护平台可在严重故障发生前侦测主轴异常,使其在操作员监管极少的无人操作环境中特别实用。

本工具机市场报告按产品类型(金属切削刀具、金属成形刀具等)、技术类型(传统工具机、数控工具机等)、终端用户产业类型(汽车、航太与国防等)、销售管道类型(直销等)和地区类型(北美、亚太、欧洲等)进行细分。报告提供了上述所有细分市场的市场规模和预测(以金额为准)。

区域分析

亚太地区持续主导策略转型,北美地区持续回流製造业,欧洲则在逆境中不断创新。预计到2026年,亚太地区将占全球营收的45.10%,年复合成长率达6.05%。这主要得益于各国政府将激励措施重点放在电动车、航太和半导体产业丛集。中国正在将其小规模工厂升级为高端CNC单元工厂,以抵消美国对中端机械征收25%关税的影响。印度的生产挂钩激励计画正在吸引资金流入300毫米晶圆厂和国防飞机机身製造领域,为精密水平和垂直加工中心创造订单。日本正利用其数十年的运动控制技术,出口可在多班次运作週期内保持亚微米级重复精度的超精密研磨。与此同时,韩国电子巨头正在投资折迭式智慧型手机铰链板和相机模组的加工能力。越南和泰国等东南亚国协正从采用「中国+1」采购模式的OEM製造商那里获得市场份额,这种模式强调地域风险分散。

北美正受惠于旨在重组战略製造业的回流政策。在美国,由于航太火箭结构以大型直立式车床的产能扩张,区域工具製造商的订单成长了11.9%,创下2001年以来的最高水准。墨西哥的订单成长了9.1%,主要得益于近岸汽车组装,新莱昂州政府支持的工业园区实现了24小时内核准。加拿大正从采矿业和低碳能源计划中获得工具机订单,但技术纯熟劳工短缺阻碍了整体成长势头,这也是整个北美大陆通用的限制因素。

在欧洲,不断上涨的电价和汇率波动给利润率带来了压力,但该行业在高精度五轴加工中心和雷射金属沉积系统领域仍然占据主导地位。德国製造商正透过专注于售后服务合约和业务重组(包括48小时主轴更换保证计划)来应对国内订单疲软。儘管销售额下降了9%,TRUMPF仍维持着光束源效率的领先地位,并将在2025年投资5.3亿欧元研发。北欧企业透过在每台新机器交付时提供碳足迹证书来彰显永续性的领先地位,这项倡议正日益成为公共部门竞标的强制性要求。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 电气化推动精密动力传动系统总成加工

- 工业4.0的普及推动了对智慧数控平台的需求。

- 高速多轴加工工具对于轻质合金和复合材料的广泛应用至关重要。

- 随着半导体製造厂的扩张,对超高精度设备的需求日益增长。

- 全球老旧(超过20年)工具机的更新週期

- 适用于自动化多品种、小批量生产的灵活加工

- 市场限制

- 特殊钢材和直线运动部件成本飙升

- 先进数控系统需要高额资本投入和较长的投资回收期。

- 全球范围内熟练的数控程式设计人员和操作员短缺。

- 资本转向积层製造技术

- 价值/供应链分析

- 监管展望(主要政府法规和政策)

- 技术概述

- 互联自动化机器

- 先进控制/运动系统

- 数位化和工业4.0

- 利用人工智慧提高金属切削精度

- 金属加工产业概览

- 地缘政治对工具机市场的影响

- 产业吸引力—五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模及成长预测(价值,单位:十亿美元)

- 副产品

- 金属切削工具

- 铣床

- 挖土机

- 车床

- 研磨

- 雷射切割机

- 电火花加工工具机(EDM)

- 水刀切割机

- 电浆切割机

- 多轴加工中心

- 其他(保龄球等)

- 金属成型工具

- 压平机(机械式、液压式、伺服)

- 锻造机

- 折弯机

- 其他(剪切、挤压、轧延等)

- 金属切削工具

- 透过技术

- 传统机器(手动或半自动)

- CNC工具工具机

- 积层製造/混合型机器

- 按最终用户行业划分

- 车

- 航太/国防

- 电气和电子设备

- 工业机械及设备

- 医疗设备

- 造船/海洋

- 精密工程

- 能源与电力

- 金属加工(代工厂等)

- 其他行业(铁路、其他一般製造业等)

- 按销售管道

- 直接销售(OEM 直接面向最终用户)

- 分销商和批发商

- 线上/电子商务

- 其他(系统整合商、活动/展览、翻新/再製造商等)

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 秘鲁

- 其他南美洲

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 比荷卢经济联盟(比利时、荷兰、卢森堡)

- 北欧国家(丹麦、芬兰、冰岛、挪威、瑞典)

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东协(印尼、泰国、菲律宾、马来西亚、越南)

- 亚太其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 卡达

- 科威特

- 土耳其

- 埃及

- 南非

- 奈及利亚

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Yamazaki Mazak Corporation

- DMG MORI Co. Ltd

- TRUMPF Group

- JTEKT Corporation

- Doosan Machine Tools

- Okuma Corporation

- Makino Milling Machine Co. Ltd

- Haas Automation Inc.

- FANUC Corporation

- Hyundai Wia Corp.

- Schuler AG

- Sandvik AB(Seco & Walter)

- GF Machining Solutions

- Fives Group

- GROB-Werke GmbH & Co. KG

- Hermle AG

- EMAG GmbH & Co. KG

- Hardinge Inc.

- HURCO Companies Inc.

- Amada Co. Ltd

第七章 市场机会与未来展望

The Machine Tools Market size in 2026 is estimated at USD 112.03 billion, growing from 2025 value of USD 108.47 billion with 2031 projections showing USD 131.63 billion, growing at 3.28% CAGR over 2026-2031.

This expansion occurs against a backdrop of realigned supply chains, stricter trade rules, and record investment in semiconductor fabs, each of which demands ultra-precision machining capacity. ASML's High-NA EUV systems, which cost more than USD 400 million apiece, exemplify how next-generation lithography is lifting the performance bar for nanometer-level metal cutting and finishing . Electrification in automotive and ongoing aerospace modernization are spurring purchases of multi-axis machining centers, while Industry 4.0 projects increasingly bundle AI-enabled CNC controls that self-optimize feed rates and tool paths. Regional investment patterns show Asia drawing the bulk of new capacity additions, yet reshoring incentives in the United States and tariff uncertainty in Europe are tilting future demand toward more diversified plant footprints. Direct sales still dominate the global distribution mix, but e-commerce portals are accelerating procurement cycles for mid-ticket CNC models and replacement tooling.

Global Machine Tools Market Trends and Insights

Electrification Surge Driving Precision e-Powertrain Machining

Electric-vehicle motor plants are pushing tolerances to micro-scale ranges, often pairing automated stator insertion and hairpin winding with five-axis machining centers that eliminate secondary finishing steps. ZF targets 70% automation for EV drive-train lines by 2030, and Chinese suppliers project annual output exceeding 120 million e-motors by 2034. General Motors and Mercedes-Benz have both insourced e-motor housing production, favouring machines that cut aluminum-silicon alloys without creating pass-off chatter. Demand is intensifying for in-process gauging, coolant management, and closed-loop compensation to suppress electromagnetic noise that would otherwise arise from micron-level form errors.

Semiconductor Fab Expansion Necessitating Ultra-Precision Equipment

Global 300 mm fab spending is forecast to hit USD 137 billion in 2027, with the Americas doubling outlays in three years. ASML's multi-ton projection optics require diamond-turning and air-bearing grinding systems that hold sub-50 nm form error over 1 m travel. TSMC's USD 165 billion Arizona complex exemplifies how sovereign chip programs create local pull for ultraprecision machine shops that can keep heavy components in-state during assembly. Clean-room compatibility, hydrostatic slideways, and contamination-free lubrication schemes are now baseline specifications for equipment makers serving this niche.

High Capex & Lengthy Payback for Advanced CNC Systems

Atlanta Fed surveys reveal that 80% of manufacturers weigh interest rates heavily before committing to capital equipment, a dynamic amplified by prime-rate increases in 2025. A top-tier five-axis cell can exceed USD 3 million installed, pushing breakeven past five years for medium-volume job shops. Equipment-as-a-service contracts are emerging as an interim solution, though many CFOs remain wary of residual value risk once software upgrades render early-generation controllers obsolete.

Other drivers and restraints analyzed in the detailed report include:

- Industry 4.0 Adoption Boosting Demand for Smart CNC Platforms

- Lightweight Alloy & Composite Uptake Requiring High-Speed Multi-Axis Tools

- Surging Specialty Steel & Linear-Motion Component Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The multi-axis segment started 2026 commanding USD 26.29 billion of the machine tools market size and is heading toward a 6.88% CAGR to 2031. Milling machines retain the biggest revenue pool with 28.05% share in 2025, yet growth now concentrates on simultaneous five-axis platforms that finish complex housings in one clamp. Automakers replacing ICE cylinder-block lines with e-drive casing cells embrace multi-axis machines to lower floor-space and handling costs. Aerospace primes add high-torque tilt-spindle centres to mill titanium spars while maintaining 0.015 mm flatness over 1.2 m lengths. Toolroom operators still rely on three-axis knee mills, but retrofit kits with digital readouts and probing keep them competitive for maintenance work.

Demand for laser cutting systems is rebounding as AI-guided parameter wizards reduce scrap rates on thin-gauge stainless. Electrical-discharge machining maintains a niche in tool-and-die cavities that require micro-corner radii which mills cannot reach economically. Hybrid machines that mix directed-energy deposition with finish milling are entering prototype labs where cycle-time savings outweigh equipment cost. Plasma and waterjet platforms serve heavy-fabrication yards; however, both are starting to integrate closed-loop height control to maintain cut quality on warped plates.

CNC platforms represented 68.55% revenue in 2025 and will climb at 6.08% CAGR, solidifying their position at the heart of the machine tools market. Emerging controllers employ GPU-accelerated algorithmsthat translate STEP files directly to optimized toolpaths, slashing programming time for short-run parts. China's First Automation secured nearly RMB 100 million to localize servo drives and PLC stacks, highlighting strategic efforts to de-risk foreign firmware dependencies. Conventional manual machines endure in small workshops and vocational schools, yet new builds are trending toward servo-ready frames even when purchased without controls, anticipating future retrofits. Hybrid additive-subtractive systems occupy the cutting edge, combining laser metal deposition with five-axis milling to eliminate support-structure removal steps in aerospace brackets.

Digital twins now simulate tool deflection and thermal drift, allowing off-machine validation that prevents collision during first-article runs. ChatCNC(TM) plug-ins recognise prismatic features and auto-generate rough-to-finish sequences, enabling less-experienced programmers to achieve veteran-level cycle times. Predictive analytics platforms flag spindle anomalies well before catastrophic failure, an especially valuable feature for lights-out processing where operator oversight is minimal.

The Machine Tools Market Report is Segmented by Product (Metal Cutting Tools, Metal Forming Tools), by Technology (Conventional Machines, CNC Machines, and More), by End-User Industry (Automotive, Aerospace & Defense, and More), by Sales Channel (Direct Sales, and More), and by Geography (North America, Asia-Pacific, Europe, and More). The Report Offers Market Size and Forecasts in Value (USD) for all the Above Segments.

Geography Analysis

Asia-Pacific Leads Amid Strategic Shifts, While North America Reshores and Europe Innovates Through Headwinds. Asia-Pacific entered 2026 with 45.10% of global revenue and a 6.05% CAGR outlook as governments funnel incentives into EV, aerospace, and semiconductor clusters. China is upgrading small-batch workshops into high-end CNC cell factories to offset looming 25% U.S. tariffs on mid-range machinery. India's production-linked incentive program is steering capital toward 300 mm wafer fabs and defence airframe work, generating orders for precision horizontals and vertical machining centres. Japan leverages decades of motion-control know-how to export ultra-precision grinders that hold sub-micron repeatability across multi-shift duty cycles, while South Korea's consumer-electronics conglomerates invest in machining capacity for foldable-phone hinge plates and camera modules. ASEAN nations such as Vietnam and Thailand gain share as OEMs adopt a China-plus-one sourcing model that values geographic risk dispersion.

North America benefits from reshoring policies aimed at rebuilding strategic manufacturing self-reliance. United States consumption reached its highest 11.9% share since 2001 as regional tool builders added capacity for large-format vertical lathes used in space-launch structures. Mexico's 9.1% uptick stems from near-shore vehicle assembly, with state-backed industrial parks in Nuevo Leon offering 24-hour permit approvals. Canada draws machine-tool orders from the mining sector and low-carbon energy projects, though overall momentum is tempered by skilled-labour shortages, a constraint echoed across the entire continent.

Europe faces margin erosion from elevated electricity costs and currency volatility, yet it preserves a commanding lead in high-accuracy five-axis and laser-metal-deposition systems. German builders are responding to soft domestic orders by pushing into after-sales contracts and retrofits, including spindle-exchange programmes that guarantee 48-hour turnaround. TRUMPF invested EUR 530 million in R&D during 2025 to maintain its edge in beam-source efficiency despite a 9% revenue dip. Nordic firms highlight sustainability leadership by offering carbon-footprint certificates with each new machine shipment, a feature increasingly mandated in public-sector tenders.

- Yamazaki Mazak Corporation

- DMG MORI Co. Ltd

- TRUMPF Group

- JTEKT Corporation

- Doosan Machine Tools

- Okuma Corporation

- Makino Milling Machine Co. Ltd

- Haas Automation Inc.

- FANUC Corporation

- Hyundai Wia Corp.

- Schuler AG

- Sandvik AB (Seco & Walter)

- GF Machining Solutions

- Fives Group

- GROB-Werke GmbH & Co. KG

- Hermle AG

- EMAG GmbH & Co. KG

- Hardinge Inc.

- HURCO Companies Inc.

- Amada Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electrification Surge Driving Precision e-Powertrain Machining

- 4.2.2 Industry 4.0 Adoption Boosting Demand for Smart CNC Platforms

- 4.2.3 Lightweight Alloy & Composite Uptake Requiring High-Speed Multi-Axis Tools

- 4.2.4 Semiconductor Fab Expansion Necessitating Ultra-Precision Equipment

- 4.2.5 Global Replacement Cycle of Ageing (>20 yrs) Machine Tool Fleet

- 4.2.6 Automation of High-Mix/Low-Volume Production Via Flexible Machining

- 4.3 Market Restraints

- 4.3.1 Surging Specialty Steel & Linear-Motion Component Costs

- 4.3.2 High Capex & Lengthy Payback for Advanced CNC Systems

- 4.3.3 Worldwide Shortage of Skilled CNC Programmers/Operators

- 4.3.4 Capital Diversion to Additive Manufacturing Technologies

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook (Key Government Regulations & Initiatives)

- 4.6 Technology Snapshot

- 4.6.1 Connected & Automated Machines

- 4.6.2 Advanced Controls / Motion Systems

- 4.6.3 Digitalisation & Industry 4.0

- 4.6.4 AI-Enhanced Metal Cutting Accuracy

- 4.7 Metalworking Industry Snapshot

- 4.8 Impact of Geopolitics on the Machine Tools Market

- 4.9 Industry Attractiveness - Porter's Five Forces

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Product

- 5.1.1 Metal Cutting Tools

- 5.1.1.1 Milling Machines

- 5.1.1.2 Drilling Machines

- 5.1.1.3 Turning (Lathe) Machines

- 5.1.1.4 Grinding Machines

- 5.1.1.5 Laser Cutting Machines

- 5.1.1.6 Electrical Discharge Machines (EDM)

- 5.1.1.7 Waterjet Cutting Machines

- 5.1.1.8 Plasma Cutting Machines

- 5.1.1.9 Multi-Axis Machining Centres

- 5.1.1.10 Others (Boring, etc.)

- 5.1.2 Metal Forming Tools

- 5.1.2.1 Presses (Mechanical, Hydraulic, Servo)

- 5.1.2.2 Forging Machines

- 5.1.2.3 Bending Machines

- 5.1.2.4 Others (Shearing, Extrusion, Rolling, etc.)

- 5.1.1 Metal Cutting Tools

- 5.2 By Technology

- 5.2.1 Conventional Machines (Manually or Semi-Manually)

- 5.2.2 CNC Machines

- 5.2.3 Additive Manufacturing / Hybrid Machines

- 5.3 By End-User Industry

- 5.3.1 Automotive

- 5.3.2 Aerospace & Defence

- 5.3.3 Electrical & Electronics

- 5.3.4 Industrial Machinery & Equipment

- 5.3.5 Medical Devices

- 5.3.6 Shipbuilding & Marine

- 5.3.7 Precision Engineering

- 5.3.8 Energy & Power

- 5.3.9 Metal Fabrication (Job Shops, etc.)

- 5.3.10 Other Industries (Railway, Other General Manufacturing, etc.)

- 5.4 By Sales Channel

- 5.4.1 Direct Sales (OEMs to End Users)

- 5.4.2 Dealers & Distributors

- 5.4.3 Online / E-commerce

- 5.4.4 Others (System Integrators, Events & Exhibitions, Rebuilders & Refurbished, etc.)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Peru

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 Kuwait

- 5.5.5.5 Turkey

- 5.5.5.6 Egypt

- 5.5.5.7 South Africa

- 5.5.5.8 Nigeria

- 5.5.5.9 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 Yamazaki Mazak Corporation

- 6.4.2 DMG MORI Co. Ltd

- 6.4.3 TRUMPF Group

- 6.4.4 JTEKT Corporation

- 6.4.5 Doosan Machine Tools

- 6.4.6 Okuma Corporation

- 6.4.7 Makino Milling Machine Co. Ltd

- 6.4.8 Haas Automation Inc.

- 6.4.9 FANUC Corporation

- 6.4.10 Hyundai Wia Corp.

- 6.4.11 Schuler AG

- 6.4.12 Sandvik AB (Seco & Walter)

- 6.4.13 GF Machining Solutions

- 6.4.14 Fives Group

- 6.4.15 GROB-Werke GmbH & Co. KG

- 6.4.16 Hermle AG

- 6.4.17 EMAG GmbH & Co. KG

- 6.4.18 Hardinge Inc.

- 6.4.19 HURCO Companies Inc.

- 6.4.20 Amada Co. Ltd

7 Market Opportunities & Future Outlook

工具机机光栅尺市场按类型、材料、输出介面、安装方式、解析度、精确度、最终用户、应用和销售管道,全球预测,2026-2032年高精度数位游标卡尺市场:按测量范围、精度、销售管道、产业和最终用户划分,全球预测(2026-2032年)

工具机机光栅尺市场按类型、材料、输出介面、安装方式、解析度、精确度、最终用户、应用和销售管道,全球预测,2026-2032年高精度数位游标卡尺市场:按测量范围、精度、销售管道、产业和最终用户划分,全球预测(2026-2032年) 全球铆接机市场规模、份额、趋势和成长分析报告(2026-2034)

全球铆接机市场规模、份额、趋势和成长分析报告(2026-2034) 2026年全球工具机市场报告可程式智慧控制面板市场(按触控技术、面板尺寸、应用和分销管道划分),全球预测(2026-2032年)

2026年全球工具机市场报告可程式智慧控制面板市场(按触控技术、面板尺寸、应用和分销管道划分),全球预测(2026-2032年) 工具机市场规模、份额及成长分析(按工具机类型、技术、最终用途产业、销售管道和地区划分)-2026-2033年产业预测

工具机市场规模、份额及成长分析(按工具机类型、技术、最终用途产业、销售管道和地区划分)-2026-2033年产业预测 日本工具机市场规模、份额、趋势及预测(依刀具类型、技术类型、最终用途产业及地区划分),2026-2034年

日本工具机市场规模、份额、趋势及预测(依刀具类型、技术类型、最终用途产业及地区划分),2026-2034年 工具机主轴单元市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

工具机主轴单元市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 精密手动工具市场规模、份额及趋势分析报告:按应用、产品、地区和细分市场预测(2025-2033 年)

精密手动工具市场规模、份额及趋势分析报告:按应用、产品、地区和细分市场预测(2025-2033 年) 高效能直线伺服马达及驱动器:全球市占率及排名、总收入及需求预测(2025-2031年)

高效能直线伺服马达及驱动器:全球市占率及排名、总收入及需求预测(2025-2031年)