|

市场调查报告书

商品编码

1910611

医药玻璃包装市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Pharmaceutical Glass Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

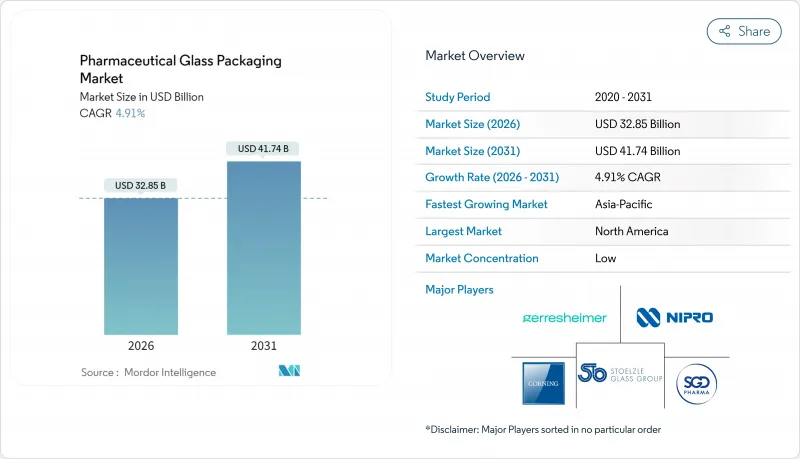

预计医药玻璃容器市场将从 2025 年的 313.1 亿美元成长到 2026 年的 328.5 亿美元,到 2031 年将达到 417.4 亿美元,2026 年至 2031 年的复合年增长率为 4.91%。

这一前景反映出市场正稳步转向更高价值的容器系统,这些系统既能满足严格的无菌性和可萃取物含量限制,又能满足生物製药快速规模化生产、分散式疫苗生产和自行注射日益增长的需求。美国食品药物管理局 (FDA) 和欧洲药品管理局 (EMA) 日益严格的监管持续推动对 I 型硼硅酸玻璃容器的需求。同时,基于人工智慧的检测技术在提高生产效率的同时,也降低了缺陷风险。此外,熔炉现代化改造和回收材料含量的提高,使製造商能够在不影响监管合规性的前提下满足永续性发展要求。因此,儘管面临原材料价格波动和来自先进聚合物日益激烈的竞争等挑战,医药玻璃容器市场仍保持稳定的成长动能。

全球医药玻璃包装市场趋势及展望

不断拓展的生物製药和注射产品线

监管数据显示,2024年FDA核准的55种新药中,将有17种是生物製剂,凸显了生物製剂的持续成长动能。为此,製造商正在加速扩大I型玻璃包装的生产能力,以确保蛋白质稳定性并降低分层风险。 Stevanato集团的销售额飙升至11.04亿欧元,其中38%来自高附加价值解决方案,显示高端包装正在充分利用这一趋势。在肿瘤和自体免疫疗法领域,皮下注射以大容量药筒的日益普及进一步巩固了医药玻璃包装市场在支持以病人为中心的给药方式方面的重要性。基因疗法的持续进步将加深对能够在整个冷冻供应链中保持无菌状态的容器的依赖。这些趋势共同为生物製药提供了结构性利好,推动了2030年后的基准需求。

后疫情时代疫苗填充与包装能力的提升

由于各国政府维持战略疫苗储备,全球管瓶消费量仍居高不下。肖特公司生产的超过10亿剂新冠疫苗管瓶凸显了持续的潜在需求。欧洲药品管理局(EMA)为应对GLP-1促效剂短缺而进行的调整,进一步凸显了建构韧性供应链的努力。在北美,博米奥利製药公司新增的经FDA核准的储存能力提振了需求,推动区域销售额成长47%。印度和东南亚各地的工厂扩建也增加了对当地加工商的供应,从而增强了新兴地区的医药玻璃包装市场。这些投资在支持广泛疫苗接种目标的同时,也缓解了疫情初期订单量波动的影响。

COP/COC聚合物注射器的快速普及

格雷斯海默公司的ClearJect聚合物注射器具有抗衝击性和黏合剂的特性,使其适用于自行注射疗法。肖特製药公司的Toppack Freeze产品针对需要极低温耐久性的mRNA药物,展现了聚合物的多功能性。由于人们担心家庭环境中易碎玻璃容器的安全问题,聚合物在高价值细分市场的应用正在加速。虽然玻璃仍是传统注射剂的主要包装,但聚合物在黏稠生物製药和大容量自动注射器领域正不断扩大市场份额。预计这种竞争将在中期内略微抑制医药玻璃包装市场的发展。

细分市场分析

预计到2025年,管瓶将维持34.78%的收入成长,主要得益于其在疫苗、冷冻干燥生技药品和临床批次产品的柔软性。稳定的需求使得SGD Pharma能够在五家工厂每天生产超过800万管瓶,确保全球供应的连续性。随着库存调整的结束和肿瘤药物研发管线补充商业库存,管瓶的医药玻璃包装市场预计将会扩张。预灌封注射器和药筒的成长速度最快,复合年增长率达7.15%,这主要得益于皮下注射生技药品和GLP-1受体拮抗剂等偏好即用型製剂的产品的需求。 BD最新推出的8毫米针头可适用于高黏度製剂,从而消除了推广应用的一大障碍。虽然瓶装产品在口服混悬液和儿童电解质领域保持稳定的需求,但安瓿瓶则满足了耐热麻醉剂的特定需求。由于复杂疗法的兴起,双腔系统等特殊规格的市场也不断扩大。人工智慧侦测持续减少所有产品的浪费,从而保护了医药玻璃包装市场的利润率。

随着医疗保健模式向以患者为中心的方向转变,製药公司正将便利性、依从性和减少就诊次数作为首要考虑因素。注射笔可实现多剂量,而自动注射器则可在无需专业人员监督的情况下确保精准给药。为了保持竞争力,管瓶生产商正在采用模组化填充生产线,提供混合批次填充方案,在透明瓶和琥珀色瓶之间快速切换,以最大限度地减少停机时间。能够减少颗粒生成并促进硅化的涂层技术正在不断提升玻璃的性能极限。因此,医药玻璃包装市场的差异化程度日益提高,每个产品类型都在法规应对力、加工性能和总体拥有成本等多个方面展开竞争。

由于其优异的耐化学性和在全球药典中的广泛应用,硼硅酸盐玻璃(I型)预计到2025年将占市场份额的54.71%。随着高浓度生物製药和抗体药物复合体(ADC)对惰性表面的需求日益增长,其市场主导地位将持续维持。新型配方,例如几乎消除了分层风险的无硼「Valor」玻璃,有望进一步扩大I型玻璃容器的医药玻璃包装市场。同时,经过处理的II型钠钙玻璃凭藉其表面涂层技术和在弱酸性注射剂领域的广泛应用,在低成本方面实现了性能与预算的良好平衡,预计将实现6.59%的复合年增长率。 Gerresheimer最新的II型产品线为中等浓度的治疗药物提供了更多选择,在这些药物领域,使用昂贵的硼硅酸玻璃并不划算。

III型玻璃仍广泛用于口服液、止咳糖浆和滴瓶等产品中,在这些产品中,pH中性比水解应力更为重要。同时,琥珀色玻璃则用于保护光降解药物和眼科抗病毒药物的一系列产品。随着大药厂设定范围3排放目标,回收成分的使用量正不断增加。 SGD Pharma目前已在部分产品线中添加了20%的消费后玻璃屑(玻璃粉),且未违反相关法规。在预测期内,永续性评估将强化采购决策,生命週期分析将成为医药玻璃包装市场中所有类型玻璃的综合价值提案。

区域分析

2025年,北美地区将占公司总收入的38.42%,主要得益于活跃的研发开发平臺、强劲的创业融资以及严格的合规文化。肖特製药在北卡罗来纳州投资3.71亿美元,计划到2030年将美国本土即用型注射器(RTU)的产量提高三倍,这将进一步巩固其在该地区主导地位。联邦政府对先进製造业的诱因也正在加速传统熔炉向电混合动力炉的转型,从而符合碳减排目标。对GLP-1疗法和肿瘤生技药品的强劲需求,促使主要加工厂实行多班制生产,降低了传统学名药生产波动带来的风险。

在严格的法规环境和早期永续性指令的支持下,欧洲保持着均衡成长。新的欧盟包装和包装废弃物法规2025/40豁免了关键的医药玻璃的部分回收配额,同时品牌所有者也自愿承诺整合碎玻璃,以实现其公司的净零排放目标。对后管瓶和药筒的生产能力。然而,能源成本仍然是一项竞争挑战,除非绿色电力价格稳定下来,否则一些製造商将被迫把生产转移到成本较低的地区。

亚太地区以7.72%的复合年增长率成为成长最快的地区,这主要得益于中国和印度製造业的扩张。预计到2023年,两国生物製药市场规模将达到6,506亿元人民币,2029年将增加一倍。政府的奖励策略推动了高端玻璃製品的进口,同时,国内製造商也正在加速熔炉的重组。跨国合约研发生产企业(CDMO)正在新加坡和韩国建立灌装包装工厂,将区域标准提升至美国和欧盟水平,并扩大了医药玻璃包装的潜在市场。东南亚的疫苗研究机构正在利用优惠资金建造灌装包装生产线,进一步刺激了管瓶的需求。

儘管南美洲和中东及非洲在绝对数量上落后,但当地的学名药生产商正透过扩建工厂来减少对进口的依赖,从而获得发展动力。巴西国家卫生监督局 (ANVISA) 的严格监管促使药品包装升级,海湾国家也正大力投资医疗保健领域,将其作为经济多元化计画的一部分。值得注意的是,区域性的碱灰和液化石油气 (LPG) 能源供应链正在缓解人们对炉用燃料的担忧,一些成长型市场正在发展成为医药玻璃包装市场出口导向生产的二级枢纽。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 不断拓展的生物製药和注射产品线

- 新冠疫情后扩大疫苗填充及包装产能

- 过渡到即用型(RTU)管瓶和注射器

- 高附加价值硼硅酸玻璃(I型)的需求不断增长

- 製药业的永续性要求推动了玻璃的可回收性。

- 利用人工智慧驱动的在线连续品管降低玻璃缺陷率(被低估了)

- 市场限制

- COP/COC聚合物注射器的快速普及

- 碱灰和能源价格波动推高玻璃成本

- 对高活性药物剥落和破损的担忧

- 区域容器玻璃熔炉产能短缺(往往被低估)

- 供应链分析

- 监理展望

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 副产品

- 瓶子

- 管瓶

- 安瓿

- 药筒和预填充式注射器

- 其他产品

- 按玻璃类型

- I型硼硼硅酸玻璃

- II 型处理钠石灰

- 第三型钠石灰

- 其他玻璃类型

- 按药物形式

- 注射

- 口服液

- 眼科/鼻科

- 按主题

- 最终用户

- 製药创新公司

- 学名药和合约生产商

- 生技公司

- 配药药房

- 动物医药

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲和纽西兰

- 亚太其他地区

- 中东和非洲

- 中东

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 埃及

- 其他非洲地区

- 中东

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Gerresheimer AG

- Schott AG

- SGD Pharma

- Stevanato Group

- Corning Inc.

- Nipro Corp.

- West Pharmaceutical Services

- Bormioli Pharma

- Owens-Illinois(Ardagh Glass Pharma)

- Stolzle Glass Group

- Beatson Clark

- Shandong Medicinal Glass

- Arab Pharmaceutical Glass

- Piramal Glass

- Sisecam Group

- Baxter BioPharma Solutions

- Kindeva Drug Delivery

- Origin Pharma Packaging

- DWK Life Sciences

- GerroMed(under-reported niche)

第七章 市场机会与未来展望

The pharmaceutical glass packaging market is expected to grow from USD 31.31 billion in 2025 to USD 32.85 billion in 2026 and is forecast to reach USD 41.74 billion by 2031 at 4.91% CAGR over 2026-2031.

This outlook reflects a steady pivot toward high-value container systems that can meet rigorous sterility and leachables limits while supporting rapid biologics scale-up, decentralized vaccine production and growing self-injection preferences. Tightened guidelines from the FDA and the European Medicines Agency continue to elevate demand for Type I borosilicate formats, while AI-enabled inspection unlocks higher throughput with lower defect risk. At the same time, furnace modernization and greater recycled content help producers manage sustainability mandates without compromising regulatory compliance. As a result, the pharmaceutical glass packaging market continues to offer reliable growth opportunities, tempered only by raw-material cost swings and rising competition from advanced polymers.

Global Pharmaceutical Glass Packaging Market Trends and Insights

Expansion of Biologics and Injectable Drugs Pipeline

Regulatory data show 17 biologics approvals among 55 new FDA drugs in 2024, underscoring sustained biologics momentum. Manufacturers therefore accelerate Type I capacity upgrades that ensure protein stability and mitigate delamination risk. A revenue jump to EUR 1,104 million at Stevanato Group, with 38% from high-value solutions, highlights how premium containers capture this wave. Oncology and autoimmune therapies increasingly favor large-volume cartridges that enable subcutaneous dosing, reinforcing the critical role of the pharmaceutical glass packaging market in supporting patient-centric delivery. Continued gene-therapy breakthroughs will deepen reliance on containers that maintain sterility across frozen supply chains. Together these trends give biologics a structural tailwind that raises baseline demand well beyond 2030.

Mounting Vaccine Fill-Finish Capacity Post-COVID

Global vial consumption remains elevated as governments keep strategic vaccine reserves. SCHOTT produced enough vials for more than 1 billion COVID-19 doses, illustrating the sustained baseline. EMA coordination to ease GLP-1 agonist shortages further spotlights the drive for resilient supply chains. North American demand strengthened when Bormioli Pharma lifted regional sales 47% after adding FDA-approved storage capacity. Facility expansions across India and Southeast Asia also push incremental volume to local converters, reinforcing the pharmaceutical glass packaging market across emerging hubs. These investments support broad immunization goals while smoothing order volatility seen during the initial pandemic surge.

Rapid Adoption of COP/COC Polymer Syringes

ClearJect polymer syringes from Gerresheimer deliver break-resistant, glue-free formats that appeal to self-injection therapies. SCHOTT Pharma's TOPPAC Freeze targets mRNA drugs that need deep-cold durability, underscoring polymer versatility. Patient safety concerns for fragile glass in at-home settings accelerate polymer acceptance in high-value niches. While glass maintains dominance for conventional injectables, polymers now capture incremental share in viscous biologics and high-volume autoinjectors. This competitive encroachment creates a modest drag on the pharmaceutical glass packaging market over the medium term.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Ready-to-Use (RTU) Vials and Syringes

- Rising Demand for High-Value Borosilicate Type I Glass

- Volatile Soda-Ash and Energy Prices Inflating Glass Cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Vials retained 34.78% revenue in 2025 as their flexibility spans vaccines, lyophilized biologics and clinical batches. Steady demand lets SGD Pharma run more than 8 million vials daily across five plants, safeguarding global supply continuity. The pharmaceutical glass packaging market size for vials is projected to grow as destocking subsides and oncology pipelines refill commercial inventories. Prefillable syringes and cartridges expand fastest at a 7.15% CAGR, propelled by subcutaneous biologics and GLP-1 antagonists that favor ready-to-inject formats. BD's latest eight-millimeter needles address higher viscosity formulations, removing one adoption hurdle. Bottles hold steady in oral suspensions and pediatric electrolytes, whereas ampoules preserve niche demand for heat-stable anesthetics. Specialty formats, including dual-chamber systems, rise alongside complex combination therapies. Across products, AI inspection continues to trim scrap rates, protecting margins within the pharmaceutical glass packaging market.

The shift toward patient-centric care pushes drug developers to prioritize convenience, adherence and reduced clinic visits. Cartridge-based pens accommodate multi-dose regimes, while autoinjectors ensure accurate dose delivery without professional oversight. Vial makers lean on modular filling lines to remain competitive, offering hybrid batches that switch between clear and amber containers with minimal downtime. Coating technologies that reduce particle generation and ease siliconization broaden the performance envelope for glass. Consequently, every product category now competes on a mix of regulatory robustness, machinability and total cost of ownership, heightening differentiation within the pharmaceutical glass packaging market.

Type I borosilicate captured 54.71% revenue in 2025 thanks to sterling chemical resistance and global pharmacopeia acceptance. Its dominance will persist as high-concentration biologics and antibody-drug conjugates demand inert surfaces. The pharmaceutical glass packaging market size for Type I containers benefits further from new compositions like boron-free Valor that virtually eliminate delamination risk. Treated Type II soda-lime glass, however, posts a 6.59% CAGR as surface coatings extend suitability to mildly acidic injectables at lower cost, offering an attractive balance between performance and budget. Gerresheimer's latest Type II lines broaden options for mid-tier therapies that cannot justify premium borosilicate pricing.

Type III glass remains common for oral liquids, cough syrups and dropper bottles where pH neutrality dominates over hydrolytic stress. Meanwhile, colored amber variants shield photolabile drugs and line extensions of ophthalmic antivirals. Recycled content climbs as large pharma institutes Scope 3 emission targets; SGD Pharma now offers 20% post-consumer cullet in selected ranges without compromising regulatory compliance. Over the forecast horizon, sustainability scoring will intensify procurement decisions, making life-cycle analysis an embedded value proposition across all glass types of the pharmaceutical glass packaging market.

The Pharmaceutical Glass Packaging Market Report is Segmented by Product (Bottles, Vials, Ampoules, and More), Glass Type (Type I Borosilicate, Type II Treated Soda-Lime, and More), Drug Formulation (Injectables, Oral Liquids, Ophthalmic/Nasal, Topical), End-User (Pharma Innovator Companies, Generic and CMOs, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 38.42% of 2025 revenue, fueled by intense R&D pipelines, strong venture funding and strict compliance culture. SCHOTT Pharma's USD 371 million investment in North Carolina is slated to triple domestic output of RTU syringes by 2030, further cementing regional leadership. Federal incentives for advanced manufacturing also speed furnace rebuilds into electric hybrids, aligning with carbon-reduction targets. Robust demand for GLP-1 therapeutics and oncology biologics sustains multi-shift operations at major converters, guarding against volume swings in legacy generics.

Europe maintains balanced growth, underpinned by its stringent regulatory environment and early sustainability mandates. The new EU Packaging and Packaging Waste Regulation 2025/40 exempts critical pharma glass from some recycling quotas, yet brand owners voluntarily pledge to integrate cullet to meet corporate net-zero goals. Political support for strategic drug reserves post-COVID fosters local vial and cartridge capacity. However, energy costs remain a competitive thorn, pushing some producers to relocate capacity to lower-cost regions unless green power tariffs stabilize.

Asia-Pacific records the fastest 7.72% CAGR, powered by manufacturing scale-ups in China and India where the 2023 biopharma market stood at 650.6 billion yuan and is forecast to double by 2029. Government stimulus packages encourage high-end glass imports even as domestic players ramp furnace rebuilds. Multinational CDMOs establish fill-finish sites in Singapore and South Korea, raising regional specifications to US and EU levels and enlarging the addressable pharmaceutical glass packaging market. Southeast Asian vaccine institutes leverage concessional funding to build fill-finish lines, further lifting vial demand.

South America and the Middle East & Africa trail in absolute numbers but gain momentum as local generics houses expand facility footprints to cut import reliance. Brazil's stringent ANVISA rules compel packaging upgrades, and Gulf states pursue health-care investment drives as part of economic diversification plans. Importantly, regional arteries for soda ash and LPG energy ease furnace-fuel concerns, positioning select emerging markets as secondary hubs for export-oriented production within the pharmaceutical glass packaging market.

- Gerresheimer AG

- Schott AG

- SGD Pharma

- Stevanato Group

- Corning Inc.

- Nipro Corp.

- West Pharmaceutical Services

- Bormioli Pharma

- Owens-Illinois (Ardagh Glass Pharma)

- Stolzle Glass Group

- Beatson Clark

- Shandong Medicinal Glass

- Arab Pharmaceutical Glass

- Piramal Glass

- Sisecam Group

- Baxter BioPharma Solutions

- Kindeva Drug Delivery

- Origin Pharma Packaging

- DWK Life Sciences

- GerroMed (under-reported niche)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of biologics and injectable drugs pipeline

- 4.2.2 Mounting vaccine fill-finish capacity post-COVID

- 4.2.3 Shift to ready-to-use (RTU) vials and syringes

- 4.2.4 Rising demand for high-value borosilicate Type-I glass

- 4.2.5 Pharma sustainability mandates boosting glass recyclability

- 4.2.6 AI-enabled inline QC reducing glass defect rates (under-reported)

- 4.3 Market Restraints

- 4.3.1 Rapid adoption of COP/COC polymer syringes

- 4.3.2 Volatile soda-ash and energy prices inflating glass cost

- 4.3.3 Delamination and breakage concerns in ultra-potent drugs

- 4.3.4 Regional container-glass furnace capacity shortages (under-reported)

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product

- 5.1.1 Bottles

- 5.1.2 Vials

- 5.1.3 Ampoules

- 5.1.4 Cartridges and Prefillable Syringes

- 5.1.5 Other Product

- 5.2 By Glass Type

- 5.2.1 Type I Borosilicate

- 5.2.2 Type II Treated Soda-Lime

- 5.2.3 Type III Soda-Lime

- 5.2.4 Other Glass Type

- 5.3 By Drug Formulation

- 5.3.1 Injectables

- 5.3.2 Oral Liquids

- 5.3.3 Ophthalmic / Nasal

- 5.3.4 Topical

- 5.4 By End-User

- 5.4.1 Pharma Innovator Companies

- 5.4.2 Generic and CMOs

- 5.4.3 Biotech Firms

- 5.4.4 Compounding Pharmacies

- 5.4.5 Veterinary Pharma

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 United Arab Emirates

- 5.5.4.1.2 Saudi Arabia

- 5.5.4.1.3 Turkey

- 5.5.4.1.4 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Nigeria

- 5.5.4.2.3 Egypt

- 5.5.4.2.4 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, and others)

- 6.4.1 Gerresheimer AG

- 6.4.2 Schott AG

- 6.4.3 SGD Pharma

- 6.4.4 Stevanato Group

- 6.4.5 Corning Inc.

- 6.4.6 Nipro Corp.

- 6.4.7 West Pharmaceutical Services

- 6.4.8 Bormioli Pharma

- 6.4.9 Owens-Illinois (Ardagh Glass Pharma)

- 6.4.10 Stolzle Glass Group

- 6.4.11 Beatson Clark

- 6.4.12 Shandong Medicinal Glass

- 6.4.13 Arab Pharmaceutical Glass

- 6.4.14 Piramal Glass

- 6.4.15 Sisecam Group

- 6.4.16 Baxter BioPharma Solutions

- 6.4.17 Kindeva Drug Delivery

- 6.4.18 Origin Pharma Packaging

- 6.4.19 DWK Life Sciences

- 6.4.20 GerroMed (under-reported niche)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

2026年全球医药玻璃器皿市场报告2026年全球低硼硅酸玻璃瓶市场报告

2026年全球医药玻璃器皿市场报告2026年全球低硼硅酸玻璃瓶市场报告 全球医药玻璃包装市场-产业规模、份额、趋势、机会及预测:依产品、药品类型、地区及竞争格局划分,2021-2031年

全球医药玻璃包装市场-产业规模、份额、趋势、机会及预测:依产品、药品类型、地区及竞争格局划分,2021-2031年 医药管瓶和安瓿市占率分析、产业趋势与统计、成长预测(2026-2031)

医药管瓶和安瓿市占率分析、产业趋势与统计、成长预测(2026-2031) 医药玻璃容器市场规模、份额及成长分析(按材料、产品、药物类型及地区划分)-2026-2033年产业预测

医药玻璃容器市场规模、份额及成长分析(按材料、产品、药物类型及地区划分)-2026-2033年产业预测 全球医药玻璃市场-市场占有率及排名、总收入及需求预测(2025-2031年)2025年全球医用玻璃疫苗瓶市场报告

全球医药玻璃市场-市场占有率及排名、总收入及需求预测(2025-2031年)2025年全球医用玻璃疫苗瓶市场报告 全球药用管瓶市场:市场规模(按数量、分销类型、瓶盖尺寸和地区划分)、未来预测

全球药用管瓶市场:市场规模(按数量、分销类型、瓶盖尺寸和地区划分)、未来预测 2032 年药用管瓶和安瓿瓶市场预测:按产品、材料、产能、应用、最终用户和地区进行的全球分析

2032 年药用管瓶和安瓿瓶市场预测:按产品、材料、产能、应用、最终用户和地区进行的全球分析 硼硅酸管瓶市场报告:2031 年趋势、预测与竞争分析

硼硅酸管瓶市场报告:2031 年趋势、预测与竞争分析