|

市场调查报告书

商品编码

1910638

肉类包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Meat Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

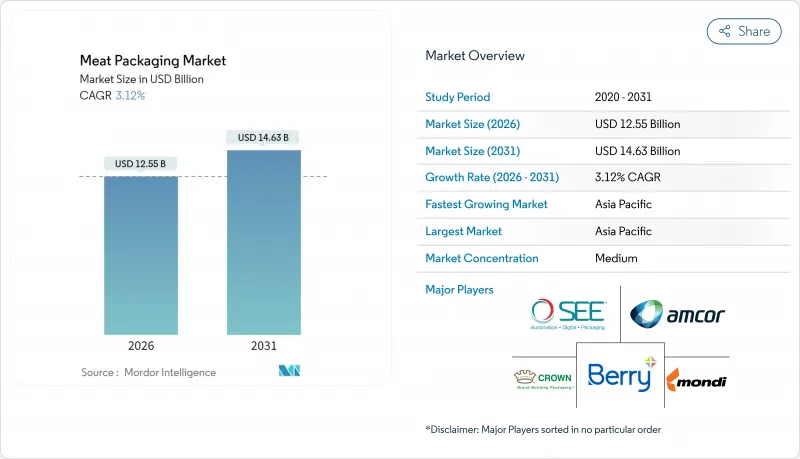

预计到2026年,肉类包装市场规模将达到125.5亿美元,高于2025年的121.7亿美元。预计到2031年,该市场规模将达到146.3亿美元,2026年至2031年的复合年增长率为3.12%。

这一增长反映了消费者对便捷肉品产品的稳定需求、低温运输物流的日益普及以及全球食品安全和永续性法规的不断加强。随着零售商追求更长的保质期和更好的视觉吸引力,柔软性塑胶、调节气体包装和高阻隔单一材料正成为包装规格的主流选择。亚太地区销售量最大,而线上杂货和食材自煮包通路的成长速度最快。塑胶废弃物法规、原材料价格波动以及替代蛋白的兴起正在抑制利润空间,促使生产商致力于可再生薄膜、自动化和智慧包装技术。

全球肉类包装市场趋势与洞察

对方便即食肉品的需求

预计2016年至2022年间,消费者对增值肉品的接受度将从37%增长至67%,这促使加工商采用即食包装,以保持肉製品的色泽和质地,同时最大程度地减少商店处理。泰森鲜肉推出了通用即食包装计划,旨在利用先进的阻隔薄膜简化分销流程并延长保质期。时间紧迫的都市区消费者愿意为方便快速烹饪的包装支付更高的价格。已调理食品的成长推动了对高压加工(HPP)和调气包装(MAP)系统的需求,这些系统能够更好地保留肉製品的风味和营养成分。这些趋势正在推动成熟城市和新兴城市肉类包装市场的持续成长。

有组织的零售和低温运输物流的扩张

预计到2023年,中国便利商店销售额将达到4,248亿元人民币,年增10.8%,其中生鲜食品是成长的主要驱动力。像Etsushi Robot这样的新兴企业正在推出能够在低至-30°C的温度下运作的自主堆高机,从而提高冷冻配送中心的效率。预计到2035年,商用冷冻设备投资将达到562亿美元,这推动了对能够承受低温压力并最大限度地减少氧气渗入的包装的需求。零售商要求采用标准化包装形式以加速货架补货速度,促使加工商开发适用于大规模生产线的软包装袋和热成型托盘。这些趋势巩固了有组织零售作为肉类包装市场长期成长要素。

抗菌/奈米复合膜

抗菌奈米复合材料可直接抑制肉类表面的微生物生长,从而延长保质期并减少对防腐剂的依赖。采用天然萃取物配製的水凝胶载体已被证明能有效降低细菌数量,同时确保食品安全。目前,北美和欧洲的试验生产线正在扩大生产规模,以实现商业化。将这些薄膜与透明的气调包装(MAP)盖结合使用,可产生协同效应,既能提供有效的保护,又能保证产品的可视性,这在冷藏柜中至关重要。

细分市场分析

截至2025年,柔软性塑胶因其能够贴合不规则形状且具有优异的印刷性能,占据了肉类包装市场41.32%的份额。可生物降解薄膜虽然仍属于小众市场,但随着监管机构鼓励使用可堆肥或可回收解决方案,其复合年增长率(CAGR)已达6.85%。金属罐和铝箔仍然是高檔腻子和需要消毒的长效产品必不可少的包装材料。抗菌奈米复合材料层正应用于柔性薄膜中,除了提供阻隔性能外,还能有效抑制细菌滋生。树脂和涂层技术的不断创新使加工商能够在保持抗穿刺性的同时降低薄膜厚度,从而保持柔性包装的成本竞争力。

由PET或PP製成的硬质托盘适用于对承载能力要求较高的切片产品,但其较高的材料重量带来了永续性的挑战。发泡托盘正逐渐被透明的一体式PET托盘所取代,后者更便于回收分拣。金属托盘因其优异的气密性仍用于出口咸牛肉和午餐肉,但其重量和成本限制了其市场成长。总体而言,随着品牌在永续性和展示需求之间寻求平衡,柔性包装解决方案将继续主导肉类包装市场。

到2025年,新鲜和冷冻产品将占肉类包装市场规模的53.25%,这主要得益于超级市场对外观精美、防漏且能维持多日保质期的托盘和外包装的需求。随着新兴国家低温运输网路的扩展,市场成长势头强劲。从熟食切片到常温肉干,即食产品线正以5.32%的复合年增长率增长,这主要受便捷生活方式的推动。这些产品需要具备高阻氧和防潮阻隔性、可微波加热的密封包装以及便于消费者开启的设计,从而推动了易撕盖和份量控制技术的创新。

加工肉品市场份额保持稳定,但日益增长的健康趋势正促使消费者转向更瘦的肉类和植物性替代品。包装方面的改进包括可重复密封的拉炼和真空紧缩包装,这些措施能够改善肉的质地并最大限度地减少空气滞留。在各个品类中,消费者对智慧劣化风险指标的需求不断增长,这有助于在陈列架上进行产品区分,并增强消费者对肉品包装市场的信心。

区域分析

到2025年,亚太地区将占据全球肉类包装市场33.40%的份额,主要得益于中国每年约1亿吨的肉类消费量以及零售业的现代化。到2031年,该地区4.56%的复合年增长率反映了从北京到班加罗尔的都市化以及对低温运输枢纽的投资。中国牛肉线上购买比例超过44%,显示专为宅配网路设计的电商相容包装正在迅速普及。印度超级市场正在扩大冷冻食品区,从而拓展了气调包装(MAP)和真空紧缩包装(VSP)解决方案的应用范围。东南亚的便利商店连锁也纷纷效仿,采用能承受潮湿气候的标准化包装袋。

北美地区人均肉类消费量高,零售基础建设成熟,是推动肉品市场成长的主要动力。技术应用也促进了成长,包括区块链追踪系统、抗菌薄膜和自动化包装机。监管改革促使单一材料阻隔薄膜开始试验应用,尤其是在加拿大的大型连锁超市。欧洲在循环经济相容性方面处于主导,鼓励加工商转向可再生PE/PP结构和纸纤维混合材料。能够同时满足氧气阻隔性和可再生目标的包装公司正在获得欧盟食品杂货商的优先供应商地位。

在南美洲,巴西等出口导向加工商对能够承受远洋运输的耐用包装需求稳定成长。阻隔性包装袋、压花真空袋和坚固的瓦楞纸包装正逐渐成为标准配置。中东和非洲的普及程度不一,海湾地区的零售商指定使用气调包装(MAP)的高檔牛排,而许多非洲市场仍依赖肉品铺纸。儘管低温运输短缺限制了其普及,但基础设施投资和快速的商业试点预计将推动其逐步推广。这些区域趋势正在为全球肉类包装市场创造多层次的成长路径。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 便利性和对即食肉品的需求

- 有组织的零售和低温运输物流的扩张

- 延长保存期限及食品安全法规

- 向高阻隔单材料永续性过渡

- 使用抗菌/奈米复合薄膜(不太常用)

- 基于区块链的可追溯性和防篡改格式(低调)

- 市场限制

- 塑胶废弃物法规和可回收性挑战

- 聚合物和金属原料价格波动

- 一次性包装税和生产者延伸责任(EPR)费用

- 由于替代蛋白质的成长(关注度降低),红肉需求下降

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 疫情影响分析与恢復分析

第五章 市场规模与成长预测

- 依材料类型

- 塑胶

- 软包装袋

- 包包

- 薄膜和包装

- 其他灵活

- 硬质托盘和容器

- 其他(硬质容器)

- 软包装袋

- 金属

- 铝

- 钢

- 其他金属

- 塑胶

- 依肉类种类

- 新鲜/冷冻

- 加工产品

- 即食

- 透过包装技术

- 调气包装(MAP)

- 真空紧缩包装(VSP)

- 主动/智慧包装

- 可食用和可生物降解的薄膜

- 透过最终用户管道

- 零售(超级市场/大卖场)

- 餐饮服务业/Horeca

- 线上杂货和食材自煮包

- 肉类加工/包装

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 中东

- 以色列

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势与发展

- 市占率分析

- 公司简介

- Amcor plc

- Sealed Air Corporation

- Berry Global Group Inc.

- Mondi plc

- Crown Holdings Inc.

- Coveris Management GmbH

- Winpak Ltd.

- Smurfit Kappa Group plc

- Viscofan SA

- Sonoco Products Company

- Huhtamaki Oyj

- DS Smith plc

- WestRock Company

- Graphic Packaging Holding Company

- Tetra Pak International SA

- Klockner Pentaplast GmbH

- Constantia Flexibles GmbH

- Cascades Inc.

- Innovia Films Ltd.

- LINPAC Packaging Ltd.

第七章 市场机会与未来展望

Meat packaging market size in 2026 is estimated at USD 12.55 billion, growing from 2025 value of USD 12.17 billion with 2031 projections showing USD 14.63 billion, growing at 3.12% CAGR over 2026-2031.

Growth reflects steady demand for convenience meat formats, widening adoption of cold-chain logistics, and tightening global food-safety and sustainability rules. Flexible plastics, modified-atmosphere formats, and high-barrier mono-materials dominate specifications as retailers push longer shelf life and stronger visual appeal. Asia-Pacific drives the largest volumes, while online grocery and meal-kit channels record the fastest incremental gains. Plastic-waste regulation, raw-material volatility, and the rise of alternative proteins temper margin outlooks, encouraging producers to pursue recyclable films, automation, and smart-packaging innovations.

Global Meat Packaging Market Trends and Insights

Demand for Convenience and Ready-to-Eat Meat Products

Consumer adoption of value-added meat rose from 37% to 67% between 2016 and 2022, pushing processors toward case-ready formats that minimise in-store handling while preserving colour and texture. Tyson Fresh Meats launched its Universal Case Ready Program to streamline distribution and extend shelf life via advanced barrier films. Urban shoppers, pressed for time, accept premium price points for packs enabling rapid meal preparation. Growth in fresh-prepared foods accelerates demand for high-pressure processing and modified-atmosphere systems that safeguard taste and nutrients. These dynamics reinforce sustained volume gains for the meat packaging market in both mature and emerging cities.

Expansion of Organized Retail and Cold-Chain Logistics

Convenience-store sales in China climbed to CNY 424.8 billion in 2023, up 10.8% year on year, with fresh foods steering the rise. Start-ups such as Yueshi Robot are deploying autonomous forklifts operating at -30 °C, lifting efficiency in frozen distribution nodes. Broader commercial-refrigeration investment, projected to reach USD 56.2 billion by 2035, requires packaging that resists low-temperature stress while keeping oxygen ingress minimal. Retailers also demand standardised shapes to speed shelf replenishment, steering converters toward flexible pouches and thermoformed trays adapted for high-volume lines. These trends cement organised retail as a long-run catalyst for the meat packaging market.

Adoption of Antimicrobial/Nanocomposite Films

Antimicrobial nanocomposites inhibit microbial growth directly on the meat surface, extending shelf life and lowering reliance on preservatives. Hydrogel carriers infused with natural extracts show efficacy in lowering bacterial counts while remaining food-safe. Pilot lines in North America and Europe are scaling production for commercial launch. Synergies arise when such films are paired with transparent MAP lids, offering both active protection and product visibility critical for refrigerated cases.

Other drivers and restraints analyzed in the detailed report include:

- Shelf-Life Extension and Food-Safety Regulations

- Sustainability-Led Shift to High-Barrier Mono-Materials

- Blockchain-Enabled Traceability and Tamper-Evident Formats

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flexible plastics held 41.32% of the meat packaging market in 2025, propelled by conformance to irregular cuts and excellent printability. Biodegradable films, though still niche, record a 6.85% CAGR as regulators favour compostable or recyclable solutions. Metal cans and foil remain vital for premium pate and long-life products requiring sterilisation. Antimicrobial nanocomposite layers are entering flexible webs, offering active bacterial suppression alongside barrier performance. Continuous resin and coating innovation allows converters to downgrade gauge while maintaining puncture resistance, keeping flexible packs cost-competitive.

Rigid trays, often PET or PP, serve sliced products where stackability matters, but face sustainability scrutiny for their higher material mass. Foam trays are losing ground to clear mono-PET variants that ease recyclability sorting. Metal options endure in export-grade corned beef and luncheon meat thanks to superior hermetic integrity, yet their growth is limited by weight and cost. Overall, flexible solutions will keep leading the meat packaging market as brands balance sustainability with merchandising demands.

Fresh and frozen products generated 53.25% of the meat packaging market size in 2025, backed by supermarket demand for visually appealing, leak-proof trays and overwraps that endure multi-day shelf life. Growth remains healthy as cold-chain coverage widens in emerging economies. Ready-to-eat lines, from deli slices to shelf-stable jerky, grow at 5.32% CAGR as lifestyles favour convenience. These formats need high-oxygen and moisture barriers, microwave-safe seals, and consumer-friendly openings, spurring innovation in peelable lidding and portion control.

Processed meats enjoy steady share, though health trends shift some volume toward leaner cuts and plant alternatives. Packaging upgrades focus on resealable zippers and vacuum skin formats that highlight texture while minimising air pockets. Across categories, demand converges toward smart indicators that display spoilage risk, reinforcing differentiation in crowded cases and boosting shopper confidence in the meat packaging market.

The Meat Packaging Market Report is Segmented by Material Type (Plastic, Metal), Meat Type (Fresh and Frozen, Processed, Ready-To-Eat), Packaging Technology (Modified Atmosphere Packaging (MAP), Vacuum Skin Packaging, and More ), End-User Channel (Retail, Foodservice, Online Grocery, Meat Processors), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 33.40% of the meat packaging market size in 2025, underpinned by China's near-100 million-ton meat consumption and vigorous retail modernisation. Regional CAGR of 4.56% through 2031 reflects urbanisation and investment in cold-chain nodes from Beijing to Bangalore. China's online beef purchases surpassed 44% share, signalling rapid uptake of e-commerce friendly packs designed for parcel networks. Indian supermarkets multiply freezer aisles, widening the addressable base for MAP and VSP solutions. Southeast Asian convenience chains follow suit, embracing standardised pouch formats that withstand humid climates.

North America combines high per-capita meat intake with mature retail infrastructure. Growth stems from technology adoption: blockchain tracing, antimicrobial films, and automation-ready baggers. Regulatory reviews spur trials of monomaterial barrier films, especially in Canada's major chains. Europe leads in circular-economy compliance, pushing converters toward recyclable PE/PP structures and paper-fibre hybrids. Packaging firms that meet both oxygen-barrier and recyclability targets unlock preferred supplier status with EU grocers.

South America sees steady demand from Brazil's export-oriented processors that need robust packs for transoceanic shipping. High-barrier pouches, embossed vacuum bags, and strong corrugated outers are standard. Middle East & Africa exhibit uneven penetration; Gulf retailers specify premium MAP steaks, while many African markets still rely on butcher paper. Cold-chain gaps limit adoption but infrastructure investments and quick-commerce pilots point to gradual uptake. Together, these geographic dynamics foster multi-speed growth paths that expand the global meat packaging market.

- Amcor plc

- Sealed Air Corporation

- Berry Global Group Inc.

- Mondi plc

- Crown Holdings Inc.

- Coveris Management GmbH

- Winpak Ltd.

- Smurfit Kappa Group plc

- Viscofan S.A.

- Sonoco Products Company

- Huhtamaki Oyj

- DS Smith plc

- WestRock Company

- Graphic Packaging Holding Company

- Tetra Pak International S.A.

- Klockner Pentaplast GmbH

- Constantia Flexibles GmbH

- Cascades Inc.

- Innovia Films Ltd.

- LINPAC Packaging Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand for convenience and RTE meat products

- 4.2.2 Expansion of organized retail and cold-chain logistics

- 4.2.3 Shelf-life extension and food?safety regulations

- 4.2.4 Sustainability-led shift to high-barrier mono-materials

- 4.2.5 Adoption of antimicrobial / nanocomposite films (under-radar)

- 4.2.6 Blockchain-enabled traceability and tamper-evident formats (under-radar)

- 4.3 Market Restraints

- 4.3.1 Plastic-waste regulations and recyclability challenges

- 4.3.2 Volatile polymer and metal input prices

- 4.3.3 Single-use-packaging taxes and EPR fees

- 4.3.4 Growth of alternative proteins reducing red-meat demand (under-radar)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pandemic Impact and Recovery Analysis

5 MARKET SIZE and GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Plastic

- 5.1.1.1 Flexible Pouches

- 5.1.1.1.1 Bags

- 5.1.1.1.2 Films and Wraps

- 5.1.1.1.3 Other Flexible

- 5.1.1.2 Rigid Trays and Containers

- 5.1.1.2.1 Other Rigid

- 5.1.1.1 Flexible Pouches

- 5.1.2 Metal

- 5.1.2.1 Aluminium

- 5.1.2.2 Steel

- 5.1.2.3 Other Metals

- 5.1.1 Plastic

- 5.2 By Meat Type

- 5.2.1 Fresh and Frozen

- 5.2.2 Processed

- 5.2.3 Ready-to-Eat

- 5.3 By Packaging Technology

- 5.3.1 Modified Atmosphere Packaging (MAP)

- 5.3.2 Vacuum Skin Packaging (VSP)

- 5.3.3 Active and Intelligent Packaging

- 5.3.4 Edible and Biodegradable Films

- 5.4 By End-user Channel

- 5.4.1 Retail (Supermarkets / Hypermarkets)

- 5.4.2 Food-service / HORECA

- 5.4.3 Online Grocery and Meal-kit

- 5.4.4 Meat Processors / Packers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Developments

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 Sealed Air Corporation

- 6.4.3 Berry Global Group Inc.

- 6.4.4 Mondi plc

- 6.4.5 Crown Holdings Inc.

- 6.4.6 Coveris Management GmbH

- 6.4.7 Winpak Ltd.

- 6.4.8 Smurfit Kappa Group plc

- 6.4.9 Viscofan S.A.

- 6.4.10 Sonoco Products Company

- 6.4.11 Huhtamaki Oyj

- 6.4.12 DS Smith plc

- 6.4.13 WestRock Company

- 6.4.14 Graphic Packaging Holding Company

- 6.4.15 Tetra Pak International S.A.

- 6.4.16 Klockner Pentaplast GmbH

- 6.4.17 Constantia Flexibles GmbH

- 6.4.18 Cascades Inc.

- 6.4.19 Innovia Films Ltd.

- 6.4.20 LINPAC Packaging Ltd.

7 MARKET OPPORTUNITIES and FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

鲜肉包装市场:2026-2032年全球市场预测(按包装类型、材料、肉类类型、应用和最终用户划分)肉类包装市场:2026-2032年全球市场预测(按包装类型、材料、肉类类型、技术、包装组件、最终用户和分销管道划分)

鲜肉包装市场:2026-2032年全球市场预测(按包装类型、材料、肉类类型、应用和最终用户划分)肉类包装市场:2026-2032年全球市场预测(按包装类型、材料、肉类类型、技术、包装组件、最终用户和分销管道划分) 2026-2030年全球肉品包装市场

2026-2030年全球肉品包装市场 家禽包装市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并提供2026-2034年的见解和预测肉类包装市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年

家禽包装市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并提供2026-2034年的见解和预测肉类包装市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年 2026年全球生鲜肉包装市场报告

2026年全球生鲜肉包装市场报告 鲜肉包装市场规模、份额及成长分析(按包装类型、材料、肉类类型、通路、最终用户和地区划分)-2026-2033年产业预测肉类包装器材市场:按机器类型、包装材料、自动化程度、包装技术和最终用途划分-2026-2032年全球预测肉类包装市场-2026-2031年预测

鲜肉包装市场规模、份额及成长分析(按包装类型、材料、肉类类型、通路、最终用户和地区划分)-2026-2033年产业预测肉类包装器材市场:按机器类型、包装材料、自动化程度、包装技术和最终用途划分-2026-2032年全球预测肉类包装市场-2026-2031年预测 肉类包装市场:依材料种类、包装技术、肉类类型及地区划分

肉类包装市场:依材料种类、包装技术、肉类类型及地区划分