|

市场调查报告书

商品编码

1910681

节能玻璃:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Energy-efficient Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

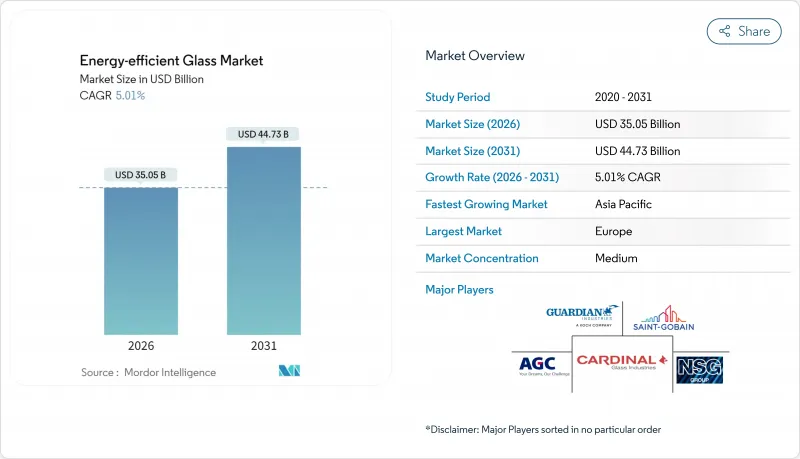

预计到 2026 年,节能玻璃市场价值将达到 350.5 亿美元,高于 2025 年的 333.8 亿美元。

预计到 2031 年,该产业规模将达到 447.3 亿美元,2026 年至 2031 年的复合年增长率为 5.01%。

这一增长主要得益于建筑能效标准的不断提高、绿色建筑认证的推广以及汽车行业向低辐射(Low-E低辐射镀膜玻璃)玻璃的转型,后者能够延长电动车的续航里程。真空绝热玻璃维修技术的进步、欧盟碳边境调节机制以及多层前置作业时间涂层技术的运用,使得产品差异化得以维持,并在原材料价格波动的情况下保障了利润率。拥有磁控溅镀设备的製造商由于设备交付週期长达三年,因此仍保持定价权。同时,玻璃製造商与太阳能技术创新者之间的合作,透过实现符合净零排放目标的建筑一体化太阳能建筑幕墙,正在开闢新的收入来源。

全球节能玻璃市场趋势与洞察

全球建筑节能标准日益收紧

最新的《国际节能规范》(IECC) 将窗户的允许U值降低了高达17%,迫使建筑师转向低辐射(Low-E)三层玻璃和真空玻璃解决方案。加州2025年第24号法规标准将垂直窗户的U值限制在0.47,因此先进的软镀膜玻璃技术对于达到此标准至关重要。加拿大2030年净零建筑目标将固定窗的U值设定为0.27,加速了三层玻璃的需求。这些标准打破了以往公认的性能-成本权衡,使得规格决策可以优先考虑性能而非前期成本。随着亚太地区各大城市一系列法规的更新,拥有多层银镀膜技术的供应商优势日益凸显。中期合规期限也为高性能产品提供了稳定的订单基础。

扩大绿建筑认证(LEED、BREEAM)

此认证架构以透明的方式评估建筑围护结构的能源效率和碳含量。 LEED v4.1认证积分依赖环境产品声明(EPD),鼓励製造商量化其碳足迹。美国绿建筑委员会(USGBC)估计,到2030年,净零排放资产需要投入35兆美元,其中大部分将用于降低营运成本的建筑幕墙。像伦敦获得BREEAM认证的水晶大厦这样的杰出地标建筑,其U值接近1.0 W/m²K,这表明先进的玻璃幕墙不仅能获得认证积分,还能转化为租金溢价。开发商现在更注重整体拥有成本而非表面材料价格,这推动了对低辐射产品的需求。

与传统浮法玻璃的初始成本比较

高价值涂层和双层玻璃的价格比标准浮法玻璃高出 40% 至 80%,这限制了其在对成本敏感的行业的应用。三层玻璃的价格比双层玻璃高出 15% 至 25%,而隔热玻璃 (VIG) 的价格则高出 200% 至 300%,主要针对高规格的商业计划。新兴市场优先考虑降低资本成本而非提升性能,减缓了短期销售成长。然而,不断上涨的公用事业费率和碳定价机制的实施正在缩短投资回收期,并降低市场接受度。公用事业收费公共和优惠融资进一步降低了成本壁垒,尤其对于面向能源贫困家庭的维修计画而言更是如此。

细分市场分析

到2025年,软镀膜产品将占节能玻璃市场61.82%的份额,并在2031年之前以5.51%的复合年增长率成长。这主要得益于其低于0.04的超低发射率以及与多层玻璃结构的兼容性。随着建筑规范对窗户U值(热传导係数)的要求日益严格,与软镀膜产品相关的节能玻璃市场规模预计将稳定扩大。先进的多层银层压技术可在不牺牲可见光透过率的情况下优化太阳热增益,从而满足寻求自然采光的办公大楼和追求室内舒适度的电动车製造商的需求。硬镀膜热解玻璃仍然适用于单层店面和对能源效率要求不高的场所,在这些场所,其耐久性和抗刮擦性优于热性能要求。供应商正在采用封闭式阴极阵列来减少边缘雾度并降低产量比率损失,并不断提高大型灯具的溅射均匀性。

汽车需求的激增进一步巩固了软涂层技术的优势。高阶电动车品牌如今已将低辐射挡风玻璃列为出厂标配,而ISO 9050等法规结构也已在全球统一了性能指标,缩短了认证週期。然而,溅射生产线的短缺限制了供应,加速了企业併购和签订长期供应协议以确保配额。领先的浮法银製造商正利用垂直整合来控制其银供应链并最大限度地降低成本波动。如果资本投资落后于需求,高选择性涂层的现货溢价可能会在整个预测期内持续存在。

这份节能玻璃报告按涂层类型(硬涂层、热解涂层、软涂层、磁控溅镀)、玻璃结构类型(单层、双层、三层)、终端用户产业(建筑、汽车、太阳能板及其他终端用户产业)和地区(亚太、北美、欧洲、南美、中东和非洲)进行细分。市场预测以美元计价。

区域分析

到2025年,欧洲在节能玻璃市场仍将占据34.21%的份额,这主要得益于欧盟《建筑能源性能指令》(EPBD),该指令要求新建建筑达到近零能耗标准。德国和英国透过修订L部分法规推动了相关规范的製定,而法国的RE2020指令则优先考虑生产过程中的碳排放,从而带动了对采用电炉生产的低碳浮法玻璃的需求。

亚太地区到2031年将以5.76%的复合年增长率达到最高增速,其中中国新建设量就占全球近一半。主要城市严格的建筑规范要求使用三层玻璃,而印度的智慧城市计画则大力推广绿建筑认证,特别注重建筑外围护结构的能源效率。

北美地区在《美国通货膨胀控制法案》和加拿大「净零排放蓝图」的税额扣抵推动下,实现了稳定成长。加州第24号法规和美国东北部城市的建筑性能标准是维修计划的基础。南美、中东和非洲虽然规模较小,但战略地位重要,这些地区能源价格上涨以及极端气候下的冷却需求推动了对太阳能控制玻璃的需求。然而,当地的生产能力仍无法满足需求。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 全球建筑节能标准日益收紧

- 绿建筑认证(LEED、BREEAM)数量增加

- 电动车原始设备製造商对低辐射(Low-E)玻璃的需求

- 快速维修采用真空绝热玻璃(VIG)

- 欧盟CBAM为低碳平板玻璃供应链提供优惠待遇

- 市场限制

- 与传统浮法玻璃相比,初始成本较高

- 碱灰和能源价格的波动会影响利润率。

- 全球磁控溅镀膜设备产能有限

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 按涂层类型

- 硬涂层(热解)

- 软涂层(磁控溅镀)

- 按玻璃类型

- 单身的

- 双倍的

- 三倍

- 按最终用户行业划分

- 建筑/施工

- 车

- 太阳能板

- 其他终端用户产业(工业等)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Abrisa Technologies

- AGC Inc.

- CARDINAL GLASS INDUSTRIES, INC

- Central Glass Co., Ltd.

- Corning Incorporated

- Fuyao Group

- Guardian Industries Holdings

- Morley Glass & Glazing Ltd

- Nippon Sheet Glass Co., Ltd

- Saint-Gobain

- SCHOTT

- Sisecam

- TuffX Glass

- Vitro

- Xinyi Glass Holdings Limited

第七章 市场机会与未来展望

Energy-efficient Glass market size in 2026 is estimated at USD 35.05 billion, growing from 2025 value of USD 33.38 billion with 2031 projections showing USD 44.73 billion, growing at 5.01% CAGR over 2026-2031.

Growth flows from stricter building-energy codes, green-building certifications, and the automotive shift to low-E glazing that extends electric-vehicle range. Technological gains in vacuum-insulated glass retrofits, the EU Carbon Border Adjustment Mechanism, and multi-layer silver coatings sustain product differentiation while protecting margins despite raw-material volatility. Producers with magnetron-sputter capacity enjoy pricing power as equipment lead times stretch up to three years. Simultaneously, collaborations between glassmakers and photovoltaic innovators unlock building-integrated solar facades that satisfy net-zero goals and open new revenue pools.

Global Energy-efficient Glass Market Trends and Insights

Stricter Global Building-Energy Codes

The latest International Energy Conservation Code trims allowable window U-factors by up to 17%, pushing architects toward low-E triple panes and vacuum solutions. California's 2025 Title 24 limits vertical fenestration U-factors to 0.47, a level achievable only with advanced soft-coat glazing. Canada's path to net-zero-ready buildings by 2030 sets a 0.27 target for fixed windows, accelerating triple-glazing demand. These codes eliminate loopholes that once permitted trade-offs, so performance now outweighs upfront cost during specification. Suppliers with multi-silver stacks find greater leverage as code updates proliferate across Asia-Pacific capitals. Compliance deadlines over the medium term underpin a dependable order pipeline for high-performance units.

Growth in Green-Building Certifications (LEED, BREEAM)

Certification frameworks reward envelope efficiency and embodied-carbon transparency. LEED v4.1 credits hinge on Environmental Product Declarations, nudging fabricators to quantify carbon footprints. The United States Green Building Council estimates USD 35 trillion must flow into net-zero assets by 2030, much of it earmarked for facades that cut operational loads. BREEAM Outstanding landmarks such as London's Crystal achieve U-values near 1.0 W/m2K, highlighting how advanced glazing delivers certification points that translate into rental premiums. Developers now value total cost of ownership over headline material prices, reinforcing demand for low-emissivity products.

High Upfront Cost Versus Conventional Float Glass

Premium coatings and multiple panes lift prices 40-80% above standard float, constraining adoption where first-cost sensitivity dominates. Triple units carry 15-25% mark-ups over double panes, while VIG commands 200-300% premiums, placing it mostly in high-spec commercial projects. Emerging markets often defer performance gains for capital savings, slowing near-term volume. Yet escalating utility tariffs and nascent carbon pricing are shortening payback horizons, easing resistance. Public-sector subsidies and concessional lending further erode the cost barrier, particularly in retrofits targeting energy-poverty households.

Other drivers and restraints analyzed in the detailed report include:

- OEM Demand for Low-E Glazing in EVs

- EU CBAM Favoring Low-Carbon Flat-Glass Supply Chains

- Limited Global Magnetron-Sputter Coating Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soft-coat products held 61.82% share of the energy-efficient glass market in 2025 and are growing at a 5.51% CAGR through 2031, reflecting unmatched emissivity below 0.04 and compatibility with multi-pane assemblies. The energy-efficient glass market size attached to soft-coat offerings is forecast to expand steadily as building codes ratchet down window U-factors. Advanced multi-silver stacks optimize solar heat-gain coefficients without sacrificing visible transmittance, appealing to both office towers seeking daylighting and EV makers requiring cabin comfort. Hard-coat pyrolytic glass remains relevant in monolithic storefronts and regions with modest efficiency requirements where durability and scratch resistance outweigh thermal targets. Suppliers continually refine sputter uniformity across jumbo lites, using closed-field cathode arrays that cut edge haze and reduce yield loss.

A surge in automotive demand further cements soft-coat ascendance. Low-E windshields are now factory-specified by premium EV brands, and regulatory frameworks such as ISO 9050 harmonize performance metrics globally, shortening qualification cycles. However, sputter-line scarcity tempers supply, prompting mergers and long-term offtake agreements that lock in allocations. Tier-one float producers leverage vertical integration to control silver supply chains, minimizing cost spikes. Should capital commitments lag demand, spot premiums for high-selectivity coatings may persist well into the forecast horizon.

The Energy-Efficient Glass Report is Segmented by Coating Type (Hard-Coat Pyrolytic and Soft-Coat Magnetron-Sputtered), Glazing Type (Single, Double, and Triple), End-User Industry (Building and Construction, Automotive, Solar Panel, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe retained 34.21% share of the energy-efficient glass market in 2025 on the back of the EU Energy Performance of Buildings Directive that requires near-zero-energy new builds. Germany and the UK drove specification with updated Part L rules, while France's RE2020 prioritized embodied carbon, steering orders toward low-carbon float made with electric furnaces.

Asia-Pacific posts the briskest 5.76% CAGR through 2031 as China alone accounts for roughly half of global new construction. Stringent Tier-1 city codes now reference triple-pane performance, and India's Smart Cities Mission fosters green-building certifications that spotlight envelope efficiency.

North America records steady gains aided by tax credits under the U.S. Inflation Reduction Act and Canada's net-zero-ready roadmap. Title 24 in California and city-level building-performance standards across the Northeast anchor retrofit pipelines. South America and the Middle East and Africa remain smaller but strategic: rising energy tariffs and extreme-climate cooling needs boost solar-control glazing uptake, though local fabrication capacity still lags demand.

- Abrisa Technologies

- AGC Inc.

- CARDINAL GLASS INDUSTRIES, INC

- Central Glass Co., Ltd.

- Corning Incorporated

- Fuyao Group

- Guardian Industries Holdings

- Morley Glass & Glazing Ltd

- Nippon Sheet Glass Co., Ltd

- Saint-Gobain

- SCHOTT

- ?i?ecam

- TuffX Glass

- Vitro

- Xinyi Glass Holdings Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter global building-energy codes

- 4.2.2 Growth in green-building certifications (LEED, BREEAM)

- 4.2.3 OEM demand for low-E glazing in EVs

- 4.2.4 Rapid retrofit uptake of vacuum-insulated glass (VIG)

- 4.2.5 EU CBAM favouring low-carbon flat-glass supply chains

- 4.3 Market Restraints

- 4.3.1 High upfront cost vs. conventional float glass

- 4.3.2 Volatile soda-ash and energy prices impacting margins

- 4.3.3 Limited global magnetron-sputter coating capacity

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Coating Type

- 5.1.1 Hard-coat (pyrolytic)

- 5.1.2 Soft-coat (magnetron-sputtered)

- 5.2 By Glazing Type

- 5.2.1 Single

- 5.2.2 Double

- 5.2.3 Triple

- 5.3 By End-user Industry

- 5.3.1 Building and Construction

- 5.3.2 Automotive

- 5.3.3 Solar Panel

- 5.3.4 Other End-user Industries (Industrial, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Russia

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Abrisa Technologies

- 6.4.2 AGC Inc.

- 6.4.3 CARDINAL GLASS INDUSTRIES, INC

- 6.4.4 Central Glass Co., Ltd.

- 6.4.5 Corning Incorporated

- 6.4.6 Fuyao Group

- 6.4.7 Guardian Industries Holdings

- 6.4.8 Morley Glass & Glazing Ltd

- 6.4.9 Nippon Sheet Glass Co., Ltd

- 6.4.10 Saint-Gobain

- 6.4.11 SCHOTT

- 6.4.12 ?i?ecam

- 6.4.13 TuffX Glass

- 6.4.14 Vitro

- 6.4.15 Xinyi Glass Holdings Limited

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

节能窗市场:2026-2032 年全球市场预测,依产品、框架材料、应用、最终用户和销售管道细分。

节能窗市场:2026-2032 年全球市场预测,依产品、框架材料、应用、最终用户和销售管道细分。 2026年全球节能窗市场报告2026年全球节能玻璃市场报告

2026年全球节能窗市场报告2026年全球节能玻璃市场报告 节能玻璃市场-全球产业规模、份额、趋势、机会和预测:按玻璃类型、涂层、产业垂直领域、地区和竞争格局划分,2021-2031年节能窗市场-全球产业规模、份额、趋势、机会及预测(按玻璃类型、最终用途产业、组件、应用、地区和竞争格局划分,2021-2031年)

节能玻璃市场-全球产业规模、份额、趋势、机会和预测:按玻璃类型、涂层、产业垂直领域、地区和竞争格局划分,2021-2031年节能窗市场-全球产业规模、份额、趋势、机会及预测(按玻璃类型、最终用途产业、组件、应用、地区和竞争格局划分,2021-2031年) 节能窗市场规模、份额和成长分析(按运行类型、玻璃类型、组件、结构类型、最终用途和地区划分)—产业预测(2026-2033 年)

节能窗市场规模、份额和成长分析(按运行类型、玻璃类型、组件、结构类型、最终用途和地区划分)—产业预测(2026-2033 年) 2032 年节能玻璃市场预测:按涂层类型、嵌装玻璃类型、玻璃类型、功能、最终用户和地区进行的全球分析

2032 年节能玻璃市场预测:按涂层类型、嵌装玻璃类型、玻璃类型、功能、最终用户和地区进行的全球分析 2025 年至 2033 年节能窗户市场报告(按营运类型、玻璃类型、组件、最终用途和地区)

2025 年至 2033 年节能窗户市场报告(按营运类型、玻璃类型、组件、最终用途和地区) 全球节能窗户市场-按类型、应用、地区和预测的市场规模

全球节能窗户市场-按类型、应用、地区和预测的市场规模 商业节能窗户市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

商业节能窗户市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测