|

市场调查报告书

商品编码

1910884

矿用自动卸货卡车:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Mining Dump Truck - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

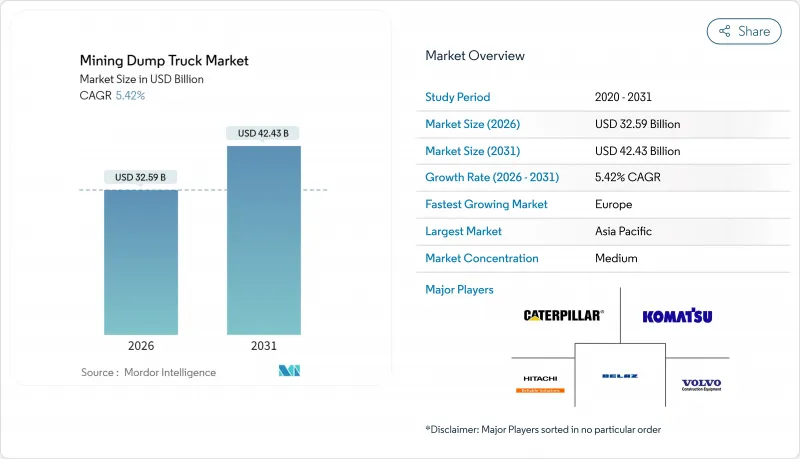

2025 年全球矿用自动卸货卡车市场价值为 309.1 亿美元,预计从 2026 年的 325.9 亿美元成长到 2031 年的 424.3 亿美元,在预测期(2026-2031 年)内复合年增长率为 5.42%。

自动驾驶技术的投资不断增加、向电池电动驱动的转型以及更严格的第五阶段和第五阶段排放标准的实施,是推动需求成长的三大支柱。亚太地区继续占据主导地位,这主要得益于中国、印度和印尼露天采矿产量的不断增长;而欧洲则凭藉排放气体法规推动的车队更新换代,实现了最快的增长。设备製造商正致力于开发整合式数位平台,以提高有效载荷公里效率并降低油耗。与每吨成本挂钩的租赁模式和从采矿到精炼的优化工具正在降低资本门槛,使中型生产商也能获得最新技术。以日本小松公司收购GHH集团为代表的併购活动,标誌着市场正朝着提供全系列地下和地面设备的方向发展,凸显了市场竞争模式从价格主导转变为服务型解决方案的方向。

全球矿用自动卸货卡车市场趋势及展望

更严格的第四阶段和第五阶段排放气体标准推动车辆更新换代

欧盟工业排放指令旨在减少非道路引擎的颗粒物排放,而加州的第五阶段排放标准则将类似的排放标准扩展到美国矿场。对老旧卡车进行改造成本高昂,因此全面升级更具成本效益。力拓等业者正在加装双燃料和混合动力系统,以满足充电网路成熟前的过渡性规定。随着处罚措施的临近,合规期限的缩短正在推动清洁技术卡车的近期订单成长。旨在减少排放并提高生产效率的车辆更新换代正在直接影响矿用自动卸货卡车市场。

透过自动驾驶展示提高装载公里生产率

力拓集团皮尔巴拉地区的23座矿场已投入运作超过700套日本小松公司AHS(自动化运输系统),该系统显着提高了单车生产率并降低了维护成本。全天候运作消除了操作员疲劳的限制,并大幅降低了事故率。卡特彼勒的「运输指令」系统可根据即时矿石品位分配自动卸货卡车执行铲运任务,从而缩短等待时间并提高冶炼厂的处理能力。高产量矿山可在两年内收回实施成本,自动化正从试点阶段走向主流。安全性、运转率和单位成本的提升,已使自动化成为新竞标文件中的强制性要求。

初始投资额高,投资回收期长

一辆超重型卡车需要300万至600万美元的初始投资,包括燃料、轮胎和维护费用,以及未来10年1500万至2000万美元的维护费用。光是轮胎一项就需要每年投入大量资金。虽然改用纯电动卡车需要额外的充电器和储能设备成本,但节能带来的效益可将投资回收期缩短至4至6年。财务状况较弱的小型矿业公司往往会推迟升级,从而限制了早期采用率。目前,贷款额成本占矿场总营运成本的15%至20%,因此资金的可用性是决定矿用自动卸货卡车市场成长轨迹的关键因素。

细分市场分析

截至2025年,刚性后自动卸货卡车将占据矿用自动卸货卡车市场48.70%的份额,这反映了效用在煤炭、铁矿石和采石场等广泛应用领域的实用性。目前规模较小的自动驾驶矿用自卸车细分市场预计将以11.05%的复合年增长率成长,这主要得益于澳洲、智利和加拿大矿场向24小时无人营运模式的转型。到2030年代初,在车辆运转率提高和维护成本降低的推动下,自动驾驶矿用自动卸货卡车市场规模预计将与刚性后卸式自卸车的收入规模相媲美。

生产效率的提升得益于日本小松公司AHS和卡特彼勒Command等系统,这些系统能够自动执行运输循环调度、轮胎监测和碰撞规避等操作。为了最大限度地发挥这些优势,营运商正致力于部署高频宽的全厂网路和远端营运中心。刚性侧卸式和铰接式自卸车仍将是窄脉矿床和软土作业领域的利基市场,在这些领域,机动性比负载容量更为重要。儘管基础设施成本较高,但自动驾驶的回报非常可观,因此越来越多的新竞标文件中将其列为标准配置,这进一步推动了矿自动卸货卡车市场向自动化方向发展。

凭藉成熟的供应链和高能量密度,内燃柴油引擎在2025年占据了矿用自动卸货卡车市场68.73%的份额。随着碳定价的推进,电池电动替代车型正以9.88%的复合年增长率快速成长,预计到2031年将对矿用自动卸货卡车市场规模做出重大贡献。

早期电气化应用将集中在年运作时间超过4000小时的铜矿和金矿,这些矿山的总拥有成本低于柴油车。徐工与Fort Esk签订的价值12亿美元的240吨电池卡车合约表明,一旦经济效益得到验证,大型矿业公司将如何扩大订单规模。混合动力汽车和氢燃料电池汽车将填补过渡期的空白,在无需深度放电充电网路的情况下逐步降低燃料成本。欧盟和加州的监管期限将起到推动作用,确保电动和混合动力汽车的普及继续成为矿用自动卸货卡车市场结构性驱动力。

区域分析

到2025年,亚太地区将占据矿用自动卸货卡车市场57.76%的份额,这主要得益于中国强大的装备製造业生态系统、印度煤炭产量的不断增长以及印尼对电池金属需求的持续扩大。徐工和三一等本土品牌正利用其规模和地理优势赢得订单,而澳洲则主导全球自动驾驶车队的普及,为其他地区树立了最佳实践典范。

到2031年,欧洲将以6.26%的复合年增长率达到最高成长。第五阶段排放法规的实施将推动柴油车快速淘汰,而碳信用货币化将提高电池动力卡车的盈利。瑞典和芬兰的矿业公司正引领着全面电动化的发展,其中Boliden的目标是到2030年实现碳中和卡车,这充分体现了该地区对电动化的坚定承诺。

北美地区的替换需求稳定成长,尤其是在内华达州的金矿区和亚利桑那州的铜矿基地,这些地区在矿场到冶炼厂软体的采用率方面处于领先地位。南美洲,以智利和秘鲁为首,正在扩大其超重型车辆的车队规模,以控製成本。同时,中东和非洲地区正在涌现新的管道开发机会,但电力基础设施的滞后限制了这些地区矿自动卸货卡车市场的短期成长。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 更严格的第四阶段和第五阶段排放气体标准推动车辆更新换代

- 自主运输技术展现出更高的载货公里生产力

- 扩大亚太地区露天矿场生产

- 矿山到冶炼厂的最佳化/将负载容量资料与冶炼厂吞吐量关联起来

- 采用以吨租赁模式降低超大型卡车的资本投资

- 电池电动自动卸货卡车卡车排碳权货币化

- 市场限制

- 初始投资额高,投资回收期长

- 商品价格波动延缓了新矿场的开发

- 偏远地区电网容量不足延缓了电气化。

- 容量超过 500 kWh 的锂离子电池组供应链风险

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模及成长预测(价值(美元)及销售量(单位))

- 按卡车类型

- 刚性后自动卸货卡车

- 刚性侧自动卸货卡车

- 铰接式自动卸货卡车

- 底自动卸货卡车/腹自动卸货卡车

- 自动自动卸货卡车(相容AHS系统)

- 透过燃料/推进方式

- 内燃机(柴油引擎)

- 油电混合(柴油-电力)

- 电池式电动车

- 氢燃料电池

- 按负载容量

- 少于150公吨

- 150-200公吨

- 201至330公吨

- 超过330公吨

- 透过使用

- 露天金属矿开采

- 煤炭和褐煤开采

- 采石场和骨材

- 重大基础建设

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 智利

- 南美洲其他地区

- 欧洲

- 德国

- 英国

- 法国

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 澳洲

- 印尼

- 亚太其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 埃及

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Caterpillar Inc.

- Komatsu Ltd.

- Hitachi Construction Machinery Co., Ltd.

- Liebherr Group

- BelAZ

- Volvo Construction Equipment

- SANY Heavy Industry Co., Ltd.

- Epiroc AB

- Sandvik AB

- HD Hyundai Infracore Co., Ltd.

- Xuzhou Construction Machinery Group Co., Ltd.

- Bell Equipment

- Shaanxi Tonly Heavy Industries Co., Ltd.

- Ashok Leyland Limited

- Guangxi LiuGong Machinery Co., Ltd.

- Daimler Truck AG

第七章 市场机会与未来展望

The global mining dump truck market was valued at USD 30.91 billion in 2025 and estimated to grow from USD 32.59 billion in 2026 to reach USD 42.43 billion by 2031, at a CAGR of 5.42% during the forecast period (2026-2031).

Surging investments in autonomous haulage, the switch to battery-electric propulsion, and stricter Stage V and Tier 5 rules are the three pillars pushing demand higher. Asia-Pacific keeps a commanding lead because surface mines in China, India, and Indonesia scale output, while Europe registers the quickest gains on the back of emission-related fleet renewal. Equipment makers focus on integrated digital platforms that raise payload-kilometer productivity and trim fuel burn. Leasing models tied to cost-per-ton and mine-to-mill optimization tools lower capital hurdles and make the latest technology accessible to mid-tier producers. M&A activity, highlighted by Komatsu's purchase of GHH Group, signals a turn toward full-line underground and surface offerings and underscores the shift from price-led competition toward service-rich solutions.

Global Mining Dump Truck Market Trends and Insights

Tightening Tier-4 and Stage-V Emission Norms Drive Fleet Renewal

The EU Industrial Emissions Directive cuts particulate output from off-road engines, while California's Tier 5 package extends similar thresholds to mines in the United States . Retrofitting older trucks has high costs per unit, tilting the cost-benefit equation toward full replacement. Operators such as Rio Tinto add dual-fuel and hybrid systems to meet interim rules as charging networks mature. With penalties looming ahead, the compliance timetable tightens purchasing cycles and lifts near-term order books for clean-tech trucks. The replacement wave directly feeds the mining dump truck market as fleets look to pair emission cuts with productivity upgrades.

Autonomous Haulage Proven to Raise Payload-km Productivity

Komatsu's AHS has over 700 units running across 23 mines, and Rio Tinto's Pilbara network reports extra productivity and lower maintenance per truck . Around-the-clock operation removes operator fatigue constraints and cuts incident rates significantly. Caterpillar's Command for Hauling allocates trucks to shovel assignments based on real-time ore grade, shrinking idle time, and improving mill throughput. High-volume mines recoup conversion costs within two years, propelling autonomous functionality from pilot stage to mainstream specification. Gains in safety, utilization, and unit cost cement autonomy as a non-negotiable feature in new tender documents.

High Upfront Capex and Long Payback Cycles

An ultra-class truck demands USD 3-6 million in capital and USD 15-20 million over a decade once fuel, tires, and maintenance are folded in. Tires alone can incur high investments annually. Battery-electric conversions tack on significant cost for chargers and storage but promise energy savings, stretching payback to 4-6 years. Smaller miners with thin balance sheets often defer upgrades, limiting early adoption rates. Financing now measures 15-20% of total mine operating cost, making capital availability a decisive factor in the mining dump truck market's growth slope.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Surface-Mine Output in Asia-Pacific

- Mine-to-Mill Optimization Linking Payload Data to Mill Throughput

- Commodity-Price Volatility Delaying Green-Field Mines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rigid rear-dump trucks commanded 48.70% of the mining dump truck market share in 2025, reflecting their broad utility across coal, iron ore, and quarry operations. The autonomous sub-segment, while smaller today, is scaling at an 11.05% CAGR as sites in Australia, Chile, and Canada convert fleets to 24-hour driverless operation. The mining dump truck market size for autonomous fleets is projected to match rigid rear-dump revenue by the early 2030s, driven by higher truck utilization and lower maintenance.

Productivity benefits stem from systems such as Komatsu AHS and Caterpillar Command that automate haul cycle dispatch, tire monitoring, and collision avoidance. Operators commit to high-bandwidth sitewide networks and remote-operation centers to unlock these gains. Rigid side-dump and articulated formats remain niche, serving narrow-vein or soft-ground applications where maneuverability overrides payload. Despite infrastructure costs, the payback for autonomy proves compelling enough that new tender documents increasingly specify the feature as standard, further tilting the mining dump truck market toward automated options.

Internal-combustion diesel units held 68.73% of the mining dump truck market share in 2025, supported by mature supply chains and high energy density. Battery-electric alternatives are expanding at a 9.88% CAGR and are forecast to account for a notable contribution to the mining dump truck market size by 2031 as carbon pricing lifts.

Early electric deployments focus on copper and gold pits where high utilization surpasses 4,000 hours annually, pushing total cost of ownership below that of diesel. XCMG's USD 1.2 billion agreement with Fortescue for 240-t battery trucks illustrates how major miners scale orders once economics prove viable. Hybrid and hydrogen pathways fill the transition gap, offering incremental fuel savings without deep-cycle charging networks. Regulatory deadlines in the EU and California act as forcing functions, ensuring electric and hybrid penetration remains a structural, rather than cyclical, driver of the mining dump truck market.

The Global Mining Dump Truck Market Report is Segmented by Truck Type (Rigid Rear-Dump, Rigid Side-Dump, and More), Fuel/Propulsion Type (Internal-Combustion (Diesel), Hybrid (Diesel-Electric), and More), Payload Capacity (Below 150 Metric Tons, 150-200 Metric Tons, and More), Application (Open-Pit Metal Mining, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific held 57.76% of the mining dump truck market share in 2025, anchored by China's equipment manufacturing ecosystem, India's rising coal output, and Indonesia's battery-metal growth. Domestic brands such as XCMG and Sany exploit scale and proximity to win contracts, while Australia leads global deployment of autonomous fleets, shaping best practices taken up elsewhere.

Europe records the highest 6.26% CAGR to 2031 as Stage V timelines compel rapid diesel replacement and carbon-credit monetization sweetens returns on battery trucks. Miners in Sweden and Finland pioneer full battery-electric pathways; Boliden targets carbon-neutral trucks by 2030, signaling deep regional commitment.

North America shows steady replacement demand, especially in Nevada gold and Arizona copper hubs, and ranks first in mine-to-mill software adoption. South America, centered on Chile and Peru, scales ultra-class fleets to protect cost curves, while the Middle East and Africa unlock greenfield pipeline potential but lag on grid infrastructure, tempering short-term mining dump truck market growth in those regions.

- Caterpillar Inc.

- Komatsu Ltd.

- Hitachi Construction Machinery Co., Ltd.

- Liebherr Group

- BelAZ

- Volvo Construction Equipment

- SANY Heavy Industry Co., Ltd.

- Epiroc AB

- Sandvik AB

- HD Hyundai Infracore Co., Ltd.

- Xuzhou Construction Machinery Group Co., Ltd.

- Bell Equipment

- Shaanxi Tonly Heavy Industries Co., Ltd.

- Ashok Leyland Limited

- Guangxi LiuGong Machinery Co., Ltd.

- Daimler Truck AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightening Tier-4 and Stage-V Emission Norms Drive Fleet Renewal

- 4.2.2 Autonomous Haulage Proven to Raise Payload-km Productivity

- 4.2.3 Expansion of Surface-Mine Output in Asia-Pacific

- 4.2.4 Mine-to-Mill Optimization Linking Payload Data to Mill Throughput

- 4.2.5 Pay-per-Ton Leasing Models for Ultra-Class Trucks Cut Capex

- 4.2.6 Carbon-Credit Monetization for Battery-Electric Dump Trucks

- 4.3 Market Restraints

- 4.3.1 High Upfront Capex and Long Payback Cycles

- 4.3.2 Commodity-Price Volatility Delaying Green-Field Mines

- 4.3.3 Weak Grid Capacity in Remote Sites Slows Electrification

- 4.3.4 Li-ion Supply-Chain Risk for Above 500 kWh Battery Packs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Truck Type

- 5.1.1 Rigid Rear-Dump Trucks

- 5.1.2 Rigid Side-Dump Trucks

- 5.1.3 Articulated Dump Trucks

- 5.1.4 Bottom/Belly Dump Trucks

- 5.1.5 Autonomous Dump Trucks (AHS-ready)

- 5.2 By Fuel/Propulsion Type

- 5.2.1 Internal-Combustion (Diesel)

- 5.2.2 Hybrid (Diesel-Electric)

- 5.2.3 Battery-Electric

- 5.2.4 Hydrogen Fuel-Cell

- 5.3 By Payload Capacity

- 5.3.1 Below 150 metric tons

- 5.3.2 150-200 metric tons

- 5.3.3 201-330 metric tons

- 5.3.4 Above 330 metric tons

- 5.4 By Application

- 5.4.1 Open-pit Metal Mining

- 5.4.2 Coal and Lignite Mining

- 5.4.3 Quarrying and Aggregates

- 5.4.4 Major Infrastructure Construction

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Chile

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Australia

- 5.5.4.4 Indonesia

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Egypt

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Caterpillar Inc.

- 6.4.2 Komatsu Ltd.

- 6.4.3 Hitachi Construction Machinery Co., Ltd.

- 6.4.4 Liebherr Group

- 6.4.5 BelAZ

- 6.4.6 Volvo Construction Equipment

- 6.4.7 SANY Heavy Industry Co., Ltd.

- 6.4.8 Epiroc AB

- 6.4.9 Sandvik AB

- 6.4.10 HD Hyundai Infracore Co., Ltd.

- 6.4.11 Xuzhou Construction Machinery Group Co., Ltd.

- 6.4.12 Bell Equipment

- 6.4.13 Shaanxi Tonly Heavy Industries Co., Ltd.

- 6.4.14 Ashok Leyland Limited

- 6.4.15 Guangxi LiuGong Machinery Co., Ltd.

- 6.4.16 Daimler Truck AG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

铰接式自动卸货卡车市场:依驱动系统、负载容量、应用及销售管道划分-2026-2032年全球市场预测自动卸货卡车市场:按负载容量、推进系统和应用分類的全球预测,2026-2032年自动卸货卡车市场:按车辆类型、负载容量、燃料类型、应用、最终用户和分销管道划分-2026-2032年全球预测

铰接式自动卸货卡车市场:依驱动系统、负载容量、应用及销售管道划分-2026-2032年全球市场预测自动卸货卡车市场:按负载容量、推进系统和应用分類的全球预测,2026-2032年自动卸货卡车市场:按车辆类型、负载容量、燃料类型、应用、最终用户和分销管道划分-2026-2032年全球预测 自卸车车厢市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测

自卸车车厢市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测 2026年全球铰接式自动卸货卡车轮胎市场报告全地形自动卸货卡车市场按有效载荷能力、燃料类型、驱动类型、车辆类型、应用、最终用户和销售管道划分,全球预测,2026-2032年柴油动力铰接式自动卸货卡车市场(按载重能力、引擎功率、变速箱、底盘配置、轮胎类型、应用和销售管道)——全球预测,2026-2032年自动卸货卡车底盘市场按载重能力、传动系统、动力传动系统、车桥配置和应用划分-全球预测,2026-2032年

2026年全球铰接式自动卸货卡车轮胎市场报告全地形自动卸货卡车市场按有效载荷能力、燃料类型、驱动类型、车辆类型、应用、最终用户和销售管道划分,全球预测,2026-2032年柴油动力铰接式自动卸货卡车市场(按载重能力、引擎功率、变速箱、底盘配置、轮胎类型、应用和销售管道)——全球预测,2026-2032年自动卸货卡车底盘市场按载重能力、传动系统、动力传动系统、车桥配置和应用划分-全球预测,2026-2032年 自卸卡车市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

自卸卡车市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 全球电动工程自动卸货卡车市场

全球电动工程自动卸货卡车市场