|

市场调查报告书

商品编码

1910938

欧洲收缩弹力套筒标籤市场:市场份额分析、行业趋势、统计数据和成长预测(2026-2031 年)Europe Shrink And Stretch Sleeve Label - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

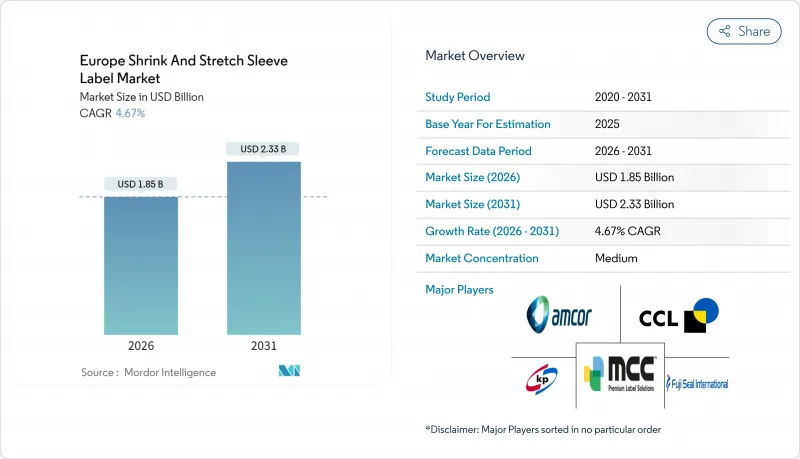

2025年欧洲收缩和弹力套筒标籤市值为17.7亿美元,预计到2031年将达到23.3亿美元,高于2026年的18.5亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 4.67%。

高端消费品的持续需求、日益严格的回收法规以及对聚烯加工生产线的快速投资,共同支撑着这一稳步增长的趋势。饮料品牌正在重新设计包装套,以符合押金退款规定,同时又不影响视觉效果;个人护理公司则在拓展360度全景影像技术,以证明其高价位产品的合理性。加工商对符合欧盟分类测试标准的基材的需求,加速了聚乙烯材料的替代品。日益激烈的竞争,加上石化产业的整合以及树脂成本的上涨,迫使中型加工商要么扩大生产规模,要么退出市场。在线连续数位印刷技术的应用,实现了经济高效的小批量生产,使品牌所有者能够进行本地化宣传活动,并降低库存风险。

欧洲收缩弹力套筒标籤市场趋势与洞察

对提升商店吸引力的需求日益增长

随着零售货架空间日益精简,视觉竞争也愈发激烈。品牌商纷纷采用全包覆式包装,将标准容器转变为360度全方位广告载具。精酿饮料品牌利用限量图案来提升单品利润率,而大众市场汽水品牌则在不影响灌装线速度的前提下,轮换使用季节性图案。西欧消费者持续青睐高端美学设计,并会重复购买,这使得全包覆式包装在价格上优于感压标籤。随着零售商不断拓展自有品牌产品线,全国性品牌正致力于打造差异化装饰,以避免产品同质化。预计欧洲整体包装产业规模将从2024年的1,530亿欧元成长至2029年的1,860亿欧元,这显示高端包装形式仍有成长空间。

需要防篡改保护

欧盟药品安全监管法规强制要求使用可见的安全功能,而收缩膜因其撕开后会留下可见的破损而备受青睐。营养保健品生产商正在采用微缩文字和变色油墨,以便在销售点进行包装认证。预计从2024年起,假冒仿冒品产品问题将急剧上升,促使超级市场越来越重视防窜改功能,即使是高阶果汁也不例外。政府检查人员也倾向于使用能够在低温运输审核期间立即发现篡改痕迹的收缩膜。电子商务的蓬勃发展进一步推动了对此类产品的需求,因为它创造了更多可能被篡改包装的接触点。

欧盟塑胶包装废弃物指令收紧

塑胶包装废弃物指令 (PPWR) 引入了可回收设计清单,使得许多传统的套筒结构一夜之间失效。加工企业必须在 2027 年前承担生产线检查、实验室测试和第三方认证的费用,并逐年承担不断上涨的生产者延伸责任 (EPR) 费用。品牌所有者正利用这项法规作为筹码重新谈判价格,在投资高峰期向供应商施加压力。西欧执法机构已在 2024 年对与包装相关的企业处以 700 万欧元的罚款,凸显了短期合规风险。融资紧张的中小企业正在推迟升级改造,并面临被市场淘汰的风险。

细分市场分析

由于热缩套管能够适应复杂的瓶型,并整合防篡改功能于饮料生产线中,预计到2025年,其在欧洲收缩和弹力套筒标籤市场规模中将占据68.02%的份额。对于每小时在蒸气隧道中处理5万瓶的高产量碳酸饮料和水品牌而言,热缩套管仍然是首选。然而,日益严格的监管和不断上涨的成本正促使品牌所有者采用拉伸套检测,尤其是在容器设计允许无需加热即可摩擦贴合的情况下。预计到2031年,拉伸套管在欧洲收缩和弹力套筒标籤市场将以5.61%的复合年增长率成长,因为易剥离性将成为合规性的关键差异化因素。

为了分散风险,加工商现在使用双功能热缩机,可以根据客户的特定要求在树脂收缩和拉伸捲材之间切换。这种新的平衡也使低密度聚乙烯(LDPE)基材受益,只需对烘箱进行少量调整,即可同时使用这两种技术。个人护理领域率先采用拉伸的企业与收缩型热缩材料相比,实现了4%的材料节约,有助于抵消树脂价格上涨的影响。对穿孔技术的投资进一步增强了热缩生产线的未来适应性,简化了消费后的剥离流程。

其他福利

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 对提升商店吸引力的需求日益增长

- 需要采取防篡改措施

- 过渡到 360° 品牌表面

- 采用可再生聚烯收缩膜

- 在线连续数位印刷集成

- 添加锂金属的油墨可以製造超薄袖套

- 市场限制

- 欧盟塑胶包装废弃物指令收紧

- 原生PET-G和PVC树脂价格上涨

- 多层薄膜回收通路的限制

- 欧盟押金退款计画中的袖标移除瓶颈

- 产业价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方和消费者的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 主要机械製造商

第五章 市场规模与成长预测

- 按类型

- 热缩套管

- 拉伸套

- 其他类型

- 材料

- 聚氯乙烯(PVC)

- 乙二醇改质聚对苯二甲酸乙二醇酯(PET-G)

- 聚乙烯(PE)

- 聚丙烯(PP)

- 其他的

- 透过使用

- 饮料

- 食物

- 个人护理

- 其他的

- 按国家/地区

- 德国

- 法国

- 英国

- 义大利

- 俄罗斯

- 波兰

- 荷兰

- 西班牙

- 其他欧洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Amcor PLC

- CCL Industries Inc.

- Klockner Pentaplast GmbH and Co. KG

- Fuji Seal International Inc.

- Huhtamaki Oyj

- Smurfit WestRock PLC

- Mondi PLC

- Multi-Color Corporation

- Sleevezone Ltd.

- Folienprint Risse Etiketten GmbH

- Oerlemans Plastics BV

- Decomatic SA

- Polifilm Extrusion GmbH

- Maca Srl

- Sleever International Company

- Derprosa Films SLU

- DOW Chemical Company

- UPM Raflatac Oy

- Constantia Flexibles Group GmbH

- Avery Dennison Corporation

- Label-Aire Inc.

第七章 市场机会与未来展望

The Europe shrink and stretch sleeve label market was valued at USD 1.77 billion in 2025 and estimated to grow from USD 1.85 billion in 2026 to reach USD 2.33 billion by 2031, at a CAGR of 4.67% during the forecast period (2026-2031).

Sustained demand from premium consumer goods, tightening recyclability rules, and rapid investments in polyolefin converting lines underpin this steady trajectory. Beverage brands are re-engineering sleeves to survive deposit-return schemes without sacrificing visual impact, while personal care players scale 360-degree graphics to justify premium shelf pricing. Material substitution toward polyethylene accelerates as converters seek substrates that pass EU sorting trials. Competitive intensity rises as petrochemical consolidation inflates resin costs, forcing mid-tier converters to choose between capacity upgrades and exit. Inline digital printing unlocks cost-effective short runs that help brand owners localize campaigns and reduce inventory risk.

Europe Shrink And Stretch Sleeve Label Market Trends and Insights

Demand to Increase On-Shelf Appeal

Retail shelf space rationalization intensifies visual competition, prompting brand owners to adopt full-body sleeves that convert an ordinary container into a 360-degree billboard. Craft beverage lines exploit limited-edition graphics to boost unit margins, while mass-market soda brands rotate seasonal artwork without disrupting fill-line speeds. Western European consumers continue to reward premium aesthetics with repeat purchases, helping sleeves defend pricing versus pressure-sensitive labels. As retailers expand private-label ranges, national brands double down on differentiated decoration to avoid commoditization. The broader European packaging sector's value climb from EUR 153 billion in 2024 to EUR 186 billion by 2029 signals headroom for upscale formats.

Need for Tamper-Evident Protection

EU pharmacovigilance rules mandate overt security features, making shrink sleeves attractive because removal leaves visible damage. Nutraceutical producers embed micro-text and color-shift inks to authenticate packages at point of sale. Counterfeit concern has risen sharply since 2024, pushing supermarkets to favor tamper-proof formats even for premium juices. Government inspectors also prefer sleeves that signal breach instantly during cold-chain audits. Growing e-commerce adds another touch-point where packages can be compromised, further raising demand.

Stricter EU Plastics-Packaging Waste Directives

PPWR introduces design-for-recycling checklists that invalidate many legacy sleeve constructions overnight. Converters must finance line trials, laboratory tests, and third-party certifications before 2027 while absorbing EPR fees that escalate annually. Brand owners use the legislation to renegotiate pricing, squeezing suppliers during investment peaks. Western European enforcement agencies already issued EUR 7 million in packaging fines during 2024, underscoring near-term compliance risk.Cash-strapped SMEs defer upgrades, risking market exit.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward 360° Branding Surfaces

- Adoption of Recyclable Polyolefin Shrink Films

- Limited Recycling Streams for Multilayer Films

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Heat shrink sleeves represented 68.02% of the Europe shrink and stretch sleeve label market size in 2025 thanks to proven conformity around intricate bottle contours and integrated tamper-evidence on beverage lines. They remain the go-to choice for high-volume soda and water brands that run containers through steam tunnels at 50,000 bottles per hour. Yet regulatory and cost headwinds encourage brand owners to trial stretch sleeves, especially where container designs allow friction application without heat. The Europe shrink and stretch sleeve label market expects stretch formats to post a 5.61% CAGR through 2031 as removal ease becomes a compliance differentiator.

Converters hedging risk now operate dual-capability applicators, shifting between resin shrink ratios and stretch roll stocks to match customer specifications. The new equilibrium also benefits low-density polyethylene substrates that accommodate both technologies with minor oven adjustments. Early stretch adopters in personal care report 4% material savings versus shrink alternatives, helping offset resin inflation. Investment in perforation technology further future-proofs heat shrink lines by simplifying post-consumer detachment.

The Europe Shrink and Stretch Sleeve Label Market Report is Segmented by Type (Heat Shrink Sleeve, Stretch Sleeve, and More), Material (PVC, PET-G, PE, PP, and More), Application (Beverage, Food, Personal Care, and More), and Geography (Germany, France, United Kingdom, Italy, Russia, Poland, Netherlands, Spain, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Amcor PLC

- CCL Industries Inc.

- Klockner Pentaplast GmbH and Co. KG

- Fuji Seal International Inc.

- Huhtamaki Oyj

- Smurfit WestRock PLC

- Mondi PLC

- Multi-Color Corporation

- Sleevezone Ltd.

- Folienprint Risse Etiketten GmbH

- Oerlemans Plastics B.V.

- Decomatic S.A.

- Polifilm Extrusion GmbH

- Maca S.r.l.

- Sleever International Company

- Derprosa Films S.L.U.

- DOW Chemical Company

- UPM Raflatac Oy

- Constantia Flexibles Group GmbH

- Avery Dennison Corporation

- Label-Aire Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand to increase on-shelf appeal

- 4.2.2 Need for tamper-evident protection

- 4.2.3 Shift toward 360° branding surfaces

- 4.2.4 Adoption of recyclable polyolefin shrink films

- 4.2.5 Inline digital printing integration

- 4.2.6 Lithium-metal additive inks enabling ultra-thin sleeves

- 4.3 Market Restraints

- 4.3.1 Stricter EU plastics-packaging waste directives

- 4.3.2 Rising prices of virgin PET-G and PVC resins

- 4.3.3 Limited recycling streams for multi-layer films

- 4.3.4 Sleeve removal bottlenecks in EU deposit-return schemes

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers/Consumers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Major Machine Suppliers

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Heat Shrink Sleeve

- 5.1.2 Stretch Sleeve

- 5.1.3 Other Types

- 5.2 By Material

- 5.2.1 Polyvinyl Chloride (PVC)

- 5.2.2 Polyethylene Terephthalate Glycol-modified (PET-G)

- 5.2.3 Polyethylene (PE)

- 5.2.4 Polypropylene (PP)

- 5.2.5 Other Materials

- 5.3 By Application

- 5.3.1 Beverage

- 5.3.2 Food

- 5.3.3 Personal Care

- 5.3.4 Other Applications

- 5.4 By Country

- 5.4.1 Germany

- 5.4.2 France

- 5.4.3 United Kingdom

- 5.4.4 Italy

- 5.4.5 Russia

- 5.4.6 Poland

- 5.4.7 Netherlands

- 5.4.8 Spain

- 5.4.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor PLC

- 6.4.2 CCL Industries Inc.

- 6.4.3 Klockner Pentaplast GmbH and Co. KG

- 6.4.4 Fuji Seal International Inc.

- 6.4.5 Huhtamaki Oyj

- 6.4.6 Smurfit WestRock PLC

- 6.4.7 Mondi PLC

- 6.4.8 Multi-Color Corporation

- 6.4.9 Sleevezone Ltd.

- 6.4.10 Folienprint Risse Etiketten GmbH

- 6.4.11 Oerlemans Plastics B.V.

- 6.4.12 Decomatic S.A.

- 6.4.13 Polifilm Extrusion GmbH

- 6.4.14 Maca S.r.l.

- 6.4.15 Sleever International Company

- 6.4.16 Derprosa Films S.L.U.

- 6.4.17 DOW Chemical Company

- 6.4.18 UPM Raflatac Oy

- 6.4.19 Constantia Flexibles Group GmbH

- 6.4.20 Avery Dennison Corporation

- 6.4.21 Label-Aire Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

拉伸套和收缩套筒标籤市场:按包装类型、印刷技术、应用和最终用途行业划分-2026-2032年全球市场预测

拉伸套和收缩套筒标籤市场:按包装类型、印刷技术、应用和最终用途行业划分-2026-2032年全球市场预测 热缩套筒标籤市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测

热缩套筒标籤市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测 2026年全球拉伸套和收缩套筒标籤市场报告热缩套筒标籤市场按材料类型、容器类型、印刷技术、厚度范围和应用划分-2026年至2032年全球预测

2026年全球拉伸套和收缩套筒标籤市场报告热缩套筒标籤市场按材料类型、容器类型、印刷技术、厚度范围和应用划分-2026年至2032年全球预测 收缩标籤和弹力套筒标籤:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)

收缩标籤和弹力套筒标籤:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年) 2025-2029年全球收缩套标与弹力套筒标籤套筒标籤市场:2025-2030 年预测笔记型电脑内胆包市场:按材料、尺寸、保护类型、闭合类型、价格分布、分销管道和最终用户 - 2025-2030 年全球预测

2025-2029年全球收缩套标与弹力套筒标籤套筒标籤市场:2025-2030 年预测笔记型电脑内胆包市场:按材料、尺寸、保护类型、闭合类型、价格分布、分销管道和最终用户 - 2025-2030 年全球预测 2025 年至 2033 年套筒标籤市场(按类型、印刷技术、应用、最终用途和地区划分)

2025 年至 2033 年套筒标籤市场(按类型、印刷技术、应用、最终用途和地区划分) 套筒标籤市场:按原料、类型、最终用途行业和地区划分

套筒标籤市场:按原料、类型、最终用途行业和地区划分