|

市场调查报告书

商品编码

1911301

数位纺织印花:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Digital Textile Printing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

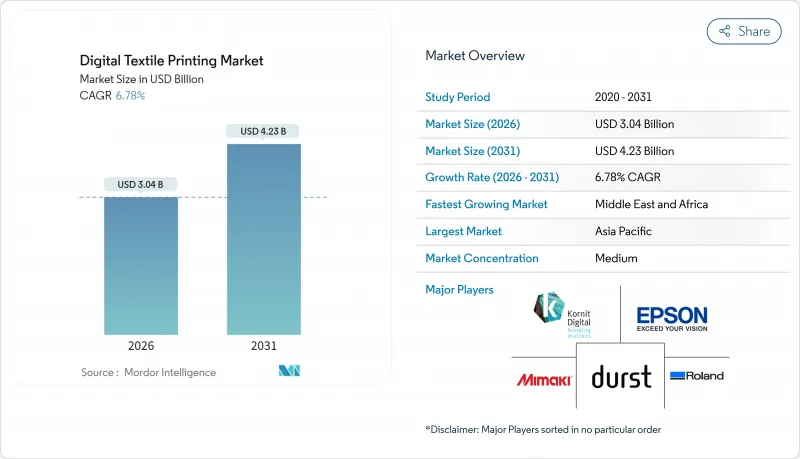

预计到 2026 年,数位纺织品印花市场规模将达到 30.4 亿美元,高于 2025 年的 28.5 亿美元。

预计到 2031 年将达到 42.3 亿美元,2026 年至 2031 年的复合年增长率为 6.78%。

电子商务通路的拓展、监管部门要求减少表面处理工程用水的压力,以及单一途径喷墨技术的快速发展,共同推动了持续增长的需求曲线,其增速超过了传统的模拟印刷。品牌商正将微量库存与按需生产相结合,以降低库存风险。同时,欧盟和加州的合规要求正在加速向低水颜料解决方案的转型。亚太地区凭藉着成熟的供应链和具竞争力的投入成本主导生产,而中东和非洲地区则正经历最快的普及速度,因为各国政府正在逐步摆脱对碳氢化合物的依赖,并投资于出口导向製造业。在竞争方面,硬体专家正将专有墨水、工作流程软体和服务协议相结合,以确保持续的收入并提高客户留存率。

全球数位纺织印花市场趋势与洞察

个性化主导的微型收藏正在蓬勃发展

目前,各大品牌正在试行每週发布新品的胶囊系列,取消最低订购量限制,并在订製服装领域实现高利润率。 Kornit Digital 的 Apollo 平台使 T-Formation 等公司能够提供当日设计发布服务,以满足不断变化的消费者偏好。按需印刷服务商正在整合资源,以应对客製化服饰市场的激增,例如 Printful 和 Printify 于 2024 年合併。库存风险降低、高端价格分布以及设计到上市週期大幅缩短,共同提升了数位纺织印刷市场的生产力。这一趋势也有助于实现循环经济目标,减少库存积压和相关废弃物。因此,设计到上市工作流程的需求仍然是下一阶段市场扩张的核心驱动力。

单一途径列印生产力飞跃

单一途径印表机一次即可完成整个影像的列印,速度比传统的多程系统快 10 到 20 倍。Delta集团第三台 EFI Nozomi 14000 SD 的安装案例表明,各大品牌正在用单程印表机取代类比生产线,并缩短显示图形的前置作业时间。 Mimaki 的 Tiger 600-1800TS(将于 2025 年 2 月在中东和非洲地区上市)在热昇华转印方面也实现了类似的吞吐量提升。机器学习校准确保了工业规模下的色彩稳定性。单一途径技术的广泛应用,在降低平方公尺成本和缩短列印週期的同时,扩大了数位纺织印花市场的潜在基本客群,尤其是在那些每週或每日更新产品是常态的行业。

工业系统的高资本投入

入门级单一途径线价格昂贵,售价在50万至200万美元之间,价格分布许多中小企业望而却步。在资本市场欠发达的地区,资金筹措障碍更为严峻,导致投资回收期更长,设备更新週期更慢。 OEM租赁方案和印刷即服务协议有助于分摊成本,但耗材仍是一笔不小的负担(可能占营运成本的40%至60%)。因此,在订单成本降低和订单到收款週期缩短能够抵消资金壁垒之前,数位纺织印刷市场的发展仍将不均衡。

细分市场分析

到2025年,卷对卷印刷将占据数位纺织品印刷市场64.92%的份额,这主要得益于其在服装、软指示牌和家用纺织品领域的适用性。列印头和在线连续夹具技术的不断改进,使其每平方公尺成本保持竞争力,从而确保了其在大批量订单中的可持续优势。同时,单一途径线平台正以10.22%的复合年增长率快速成长,即使是小批量生产也能提供工业级的生产效率,使品牌能够在一条生产线上完成样品製作和批量生产。结合模拟底涂和数位面涂的混合配置,使加工商能够最大限度地延长运作,并根据图案的复杂程度灵活选择网版印刷或喷墨印刷。

透过采用直喷服装印刷技术(即加工商共用单次走纸头),数位纺织印花市场受益于设备冗余和库存的减少。 EFI、Mimaki 和 Kornit Digital 等公司正在将色彩管理、维护分析和工作流程自动化整合到各自的生态系统中,从而降低转换成本。对于那些正在淘汰旧式网版的企业而言,模组化改装提供了一条迁移路径,既能降低资本投资风险,又不会延缓数位转型。

到2025年,分散型油墨将占据数位纺织品印花市场41.88%的份额,其在聚酯基材上的主导地位将巩固其市场地位。同时,热昇华油墨预计将以9.12%的复合年增长率成为增长最快的油墨,这得益于其能够以最少的后处理工艺附着在织物上,尤其适用于那些对色彩鲜艳持久性有较高要求的应用,例如运动服、宣传旗帜和背光显示屏。随着无水工艺和一步式后整理技术满足日益严格的环保法规,颜料型油墨套装也越来越受欢迎。 OEM厂商采用杜邦Artistri® PN1000系列等油墨,标誌着业界正从活性染料转向更环保、适用于多种基材的油墨。

在棉织物占主导地位的地区,活性油墨占据主导地位,因为深层色彩渗透和耐洗牢度至关重要;而酸性油墨则非常适合丝绸和羊毛,从而支撑起高端市场。油墨创新主要集中在降低固化温度和延长喷嘴开放时间上,这些因素直接影响数位纺织印花市场的运作效益。

区域分析

到2025年,亚太地区将占全球出货量的42.10%,这主要得益于中国779亿美元的纱线和布料出口额,以及印度积极的政策支持,包括七个总理纺织工业园区(PM MITRA parks),并提供22亿美元的激励措施。儘管能源和环境法规日益严格,但低廉的工资水平、密集的供应商丛集和完善的港口网络,使得该地区的泊位成本保持竞争力。区域OEM伙伴关係正在将单一途径列印设备引入垂直整合的工厂,降低了小众品牌进入数位纺织印花市场的门槛。

预计到2031年,中东和非洲地区将以10.75%的复合年增长率实现最高成长,这主要得益于各国政府的多元化措施。阿联酋和沙乌地阿拉伯正充分利用自由贸易区的优惠政策,而埃及(最低月薪为103美元)则与土耳其生产商合作,扩大对美国的供应。摩洛哥和衣索比亚的工业园区等基础设施计划正在吸引外国直接投资,使该地区成为亚洲采购之外一个灵活且免税的选择。

在欧洲,基于环境、社会和管治标准(ESPR)的环境相容性备受重视,工厂越来越多地采用节水颜料製程并添加再生纤维。品牌商正采取策略,将微胶囊生产集中在附近地区,以缩短交货时间,这符合成熟消费者群体对透明度和永续性的需求。自2020年以来,北美地区的製造业回流復苏以每年2.8%的速度成长,例如Chaumot Infinite等公司投资800万美元,用于改造从针织到后整理的一体化生产线。南美地区的成长保持稳定,但受到物流挑战和宏观经济波动的限制,儘管拥有原材料采购优势,但在数位纺织印花市场份额的扩张能力仍然有限。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 个性化主导的微型收藏蓬勃发展

- 单一途径列印,生产力突飞猛进

- 电子商务中的按需印刷履约

- 遵守节水法规的义务

- 近岸外包协助打造更具韧性的供应链

- 服装用永续颜料的进展

- 市场限制

- 工业系统的高资本投入

- 油墨与织物相容性挑战

- 颜色牢度品质保证方面的瓶颈

- PFAS相关颜料的监管风险

- 供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 宏观经济影响分析

第五章 市场规模与成长预测

- 透过印刷方法

- 卷对卷印刷

- 直接成衣印花(DTG)

- 单一途径线

- 混合式(类比+数位)

- 其他印刷方法

- 按墨水类型

- 昇华

- 颜料

- 反应性

- 酸

- 分散式

- 透过使用

- 服饰和服饰

- 家用纺织品

- 技术纺织品

- 展示品和标誌

- 按平台

- 棉布

- 聚酯纤维

- 丝绸

- 尼龙

- 混合

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 义大利

- 英国

- 法国

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲和纽西兰

- 亚太其他地区

- 中东和非洲

- 中东

- 土耳其

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 中东

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Kornit Digital

- Seiko Epson Corporation

- Mimaki Engineering

- Durst Group

- Electronics For Imaging

- D.Gen Inc.

- Aeoon Technologies

- Roland DG

- Ricoh Company

- ColorJet

- ATP Color

- SPGPrints

- HP Inc.

- Brother International

- Mutoh Industries

- MS Printing Solutions

- Kyocera Corp.

- FujiFilm Dimatix

- ROQ International

- Shenzhen Homer

第七章 市场机会与未来展望

Digital textile printing market size in 2026 is estimated at USD 3.04 billion, growing from 2025 value of USD 2.85 billion with 2031 projections showing USD 4.23 billion, growing at 6.78% CAGR over 2026-2031.

Expanding e-commerce channels, regulatory pressure to reduce water use in finishing operations, and rapid progress in single-pass inkjet technology together create a durable demand curve that outperforms legacy analog printing. Brands now blend micro-collections with on-demand manufacturing to cut inventory risk, while compliance mandates in the European Union and California accelerate the shift toward low-water pigment solutions. Asia-Pacific dominates production because of established supply chains and competitive input costs, yet Middle East and Africa records the fastest adoption as governments diversify away from hydrocarbons and invest in export-oriented manufacturing. On the competitive front, hardware specialists combine proprietary inks, workflow software, and service contracts to lock in recurring revenue and deepen client stickiness.

Global Digital Textile Printing Market Trends and Insights

Personalisation-led micro-collections boom

Labels now pilot capsule lines in weekly drops, eliminating minimum order quantities and monetising higher margins on customised apparel. Kornit Digital's Apollo platform enables companies such as T-Formation to release same-day designs that meet shifting consumer tastes. Print-on-demand players consolidate capacity-as seen in the 2024 Printful/Printify merger-to serve this surge in bespoke garments. Lower inventory risk, premium price points, and dramatically shorter design-to-shelf cycles collectively lift throughput across the digital textile printing market. The trend also supports circular economy objectives by reducing surplus stock and related waste. Demand for design-to-garment workflows therefore remains a central accelerator for the next phase of market expansion.

Single-pass inkjet productivity leap

Single-pass printers lay down an entire image in one motion, reaching speeds 10-20 times faster than classic multi-pass systems. Delta Group's third EFI Nozomi 14000 SD installation underscores how brands replace analog lines to cut lead times for display graphics. Mimaki's Tiger600-1800TS, launched in February 2025 for MEA users, offers similar gains in dye-sublimation throughput. Machine-learning-driven calibration ensures colour consistency at industrial scale. As cost per square metre falls in parallel with cycle times, single-pass adoption widens the addressable base for the digital textile printing market, especially where weekly or daily product refreshes are the norm.

High capex for industrial systems

Entry-level single-pass lines cost USD 500,000-USD 2 million, placing them beyond the reach of many SMEs. Financing barriers are more acute in regions with under-developed capital markets, extending payback horizons and slowing equipment refresh cycles. Leasing programmes and print-as-a-service contracts from OEMs help amortise costs, yet the burden of consumables-which can equal 40-60% of operating expenditure-remains. The digital textile printing market therefore advances unevenly until capital hurdles are offset by lower per-unit costs and quicker order-to-cash timelines.

Other drivers and restraints analyzed in the detailed report include:

- E-commerce print-on-demand fulfilment

- Water-saving compliance mandates

- PFAS-linked pigment regulatory risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Roll-to-Roll systems delivered 64.92% of the digital textile printing market size in 2025, supported by their compatibility with high-volume apparel, soft-signage, and home-textile runs. Continued improvements in printheads and inline fixation keep cost per square metre attractive, ensuring enduring relevance for bulk orders. Concurrently, Single-Pass Line platforms are scaling fastest at a 10.22% CAGR, bringing industrial throughput to low-run jobs and enabling brands to merge sampling and mass production on one line. Hybrid configurations that marry analog under-bases with digital overprints now help converters maximise uptime while flexibly deploying screens or inkjets to match artwork complexity.

The digital textile printing market benefits when converters adopt direct-to-garment options that share single-pass heads, reducing equipment redundancy and inventory. EFI, Mimaki, and Kornit Digital each package colour management, maintenance analytics, and workflow automation in their ecosystems, raising switching costs. For enterprises still amortising legacy screens, modular retrofits offer a transitional path, mitigating capex risk without stalling digital transition.

Disperse inks captured 41.88% of the digital textile printing market share in 2025, cemented by polyester's reigning material dominance. Sublimation chemistries, however, notch the quickest 9.12% CAGR because sportswear, promotional flags, and backlit displays prize vivid, durable colour that sublimates into fibre with minimal post-treatment. Pigment sets gain favour as waterless workflows and one-step finishing address tightening environmental codes; OEM introductions such as DuPont's Artistri(R) PN1000 series illustrate the pivot from reactive dyes toward greener, cross-substrate options.

Reactive inks hold sway in cotton-heavy regions where deep shade penetration and wash resistance are mission-critical, while acid inks cater to silk and wool, sustaining premium segments. Ink innovation continues to revolve around lowering curing temperatures and improving nozzle open time, factors that directly influence uptime economics in the digital textile printing market.

The Digital Textile Printing Market Report is Segmented by Printing Method (Roll-To-Roll Printing, Direct-To-Garment (DTG), and More), Ink Type (Sublimation, Pigment, Reactive, Acid, Disperse), Application (Garment and Apparel, Home Textiles, Technical Textiles, Display and Signage), Substrate (Cotton, Polyester, Silk, Nylon, Blends), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific controlled 42.10% of global shipments in 2025, anchored by China's USD 77.9 billion yarn and fabric exports and India's aggressive policy packages, including seven PM MITRA parks backed by USD 2.2 billion in incentives. Lower labour rates, dense supplier clusters, and deep port networks keep landed costs competitive even as energy and environmental rules tighten. Regional OEM partnerships funnel single-pass equipment into vertically integrated mills, lowering the adoption barrier for niche brands entering the digital textile printing market.

Middle East & Africa registers the sharpest 10.75% CAGR to 2031 as governments pursue diversification. The UAE and Saudi Arabia leverage free-zone incentives while Egypt teams with Turkish producers to supply US buyers, taking advantage of USD 103 monthly minimum wages. Infrastructure projects such as industrial parks in Morocco and Ethiopia attract foreign direct investment that positions the region as an agile, tariff-hedged alternative to Asian sourcing.

Europe emphasises ecological compliance under the ESPR, prompting mills to adopt water-saving pigment workstreams and recycled fibre blends. Brands near-shore micro-capsule runs to shorten delivery windows, a strategy aligned with the continent's mature consumer base demanding transparency and sustainable credentials. North America's reshoring renaissance advances at 2.8% annual growth since 2020, with players like Shawmut Infinite investing USD 8 million to modernise integrated knit-to-finish lines. South American growth is steady yet hampered by logistics gaps and macro volatility, limiting its share of the digital textile printing market despite favourable raw-material availability.

- Kornit Digital

- Seiko Epson Corporation

- Mimaki Engineering

- Durst Group

- Electronics For Imaging

- D.Gen Inc.

- Aeoon Technologies

- Roland DG

- Ricoh Company

- ColorJet

- ATP Color

- SPGPrints

- HP Inc.

- Brother International

- Mutoh Industries

- MS Printing Solutions

- Kyocera Corp.

- FujiFilm Dimatix

- ROQ International

- Shenzhen Homer

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Personalisation-led micro-collections boom

- 4.2.2 Single-pass inkjet productivity leap

- 4.2.3 E-commerce print-on-demand fulfilment

- 4.2.4 Water-saving compliance mandates

- 4.2.5 Near-shoring for resilient supply chains

- 4.2.6 On-garment sustainable pigment advances

- 4.3 Market Restraints

- 4.3.1 High capex for industrial systems

- 4.3.2 Ink-fabric compatibility hurdles

- 4.3.3 Colour-fastness QA bottlenecks

- 4.3.4 PFAS-linked pigment regulatory risk

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Macroeconomic Impact Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Printing Method

- 5.1.1 Roll-to-Roll Printing

- 5.1.2 Direct-to-Garment (DTG)

- 5.1.3 Single-Pass Line

- 5.1.4 Hybrid (Analog + Digital)

- 5.1.5 Other Printing Method

- 5.2 By Ink Type

- 5.2.1 Sublimation

- 5.2.2 Pigment

- 5.2.3 Reactive

- 5.2.4 Acid

- 5.2.5 Disperse

- 5.3 By Application

- 5.3.1 Garment and Apparel

- 5.3.2 Home Textiles

- 5.3.3 Technical Textiles

- 5.3.4 Display and Signage

- 5.4 By Substrate

- 5.4.1 Cotton

- 5.4.2 Polyester

- 5.4.3 Silk

- 5.4.4 Nylon

- 5.4.5 Blends

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 Italy

- 5.5.2.3 United Kingdom

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Turkey

- 5.5.4.1.2 Saudi Arabia

- 5.5.4.1.3 United Arab Emirates

- 5.5.4.1.4 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Kornit Digital

- 6.4.2 Seiko Epson Corporation

- 6.4.3 Mimaki Engineering

- 6.4.4 Durst Group

- 6.4.5 Electronics For Imaging

- 6.4.6 D.Gen Inc.

- 6.4.7 Aeoon Technologies

- 6.4.8 Roland DG

- 6.4.9 Ricoh Company

- 6.4.10 ColorJet

- 6.4.11 ATP Color

- 6.4.12 SPGPrints

- 6.4.13 HP Inc.

- 6.4.14 Brother International

- 6.4.15 Mutoh Industries

- 6.4.16 MS Printing Solutions

- 6.4.17 Kyocera Corp.

- 6.4.18 FujiFilm Dimatix

- 6.4.19 ROQ International

- 6.4.20 Shenzhen Homer

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

纺织品印花市场:依印花技术、油墨类型、承印物、产量及应用划分-2026-2032年全球预测

纺织品印花市场:依印花技术、油墨类型、承印物、产量及应用划分-2026-2032年全球预测 日本数位纺织印花市场规模、份额、趋势及预测(按印花方法、承印物类型、油墨类型、应用及地区划分,2026-2034年)

日本数位纺织印花市场规模、份额、趋势及预测(按印花方法、承印物类型、油墨类型、应用及地区划分,2026-2034年) 2026年全球数位纺织印花市场报告

2026年全球数位纺织印花市场报告 全球数位纺织印花机市场:按印花机类型、印花机技术、墨水类型、材料类型、应用、国家和地区划分-产业分析、市场规模、份额及未来预测(2025-2032)大幅面纺织品直喷印表机市场:按墨水类型、印表机技术、印表机幅宽和应用划分 - 全球预测(2026-2032 年)宽幅直喷式织物印表机市场:按列印技术、印表机类型、应用和最终用户划分 - 全球预测(2026-2032 年)按技术、织物材料、墨水类型、最终用户和应用分類的直接织物纺织印表机市场—2026-2032年全球预测

全球数位纺织印花机市场:按印花机类型、印花机技术、墨水类型、材料类型、应用、国家和地区划分-产业分析、市场规模、份额及未来预测(2025-2032)大幅面纺织品直喷印表机市场:按墨水类型、印表机技术、印表机幅宽和应用划分 - 全球预测(2026-2032 年)宽幅直喷式织物印表机市场:按列印技术、印表机类型、应用和最终用户划分 - 全球预测(2026-2032 年)按技术、织物材料、墨水类型、最终用户和应用分類的直接织物纺织印表机市场—2026-2032年全球预测 数位纺织印花市场规模、份额及成长分析(按纺织品、印花製程、油墨类型、操作方式、承印物、应用及地区划分)-产业预测:2026-2033年

数位纺织印花市场规模、份额及成长分析(按纺织品、印花製程、油墨类型、操作方式、承印物、应用及地区划分)-产业预测:2026-2033年 数位纺织印花机市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)

数位纺织印花机市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年) 纺织品印花市场规模、份额和趋势分析报告:按印花技术、应用、地区和细分市场预测(2025-2033 年)

纺织品印花市场规模、份额和趋势分析报告:按印花技术、应用、地区和细分市场预测(2025-2033 年)