|

市场调查报告书

商品编码

1911377

视讯车载资讯服务:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Video Telematics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

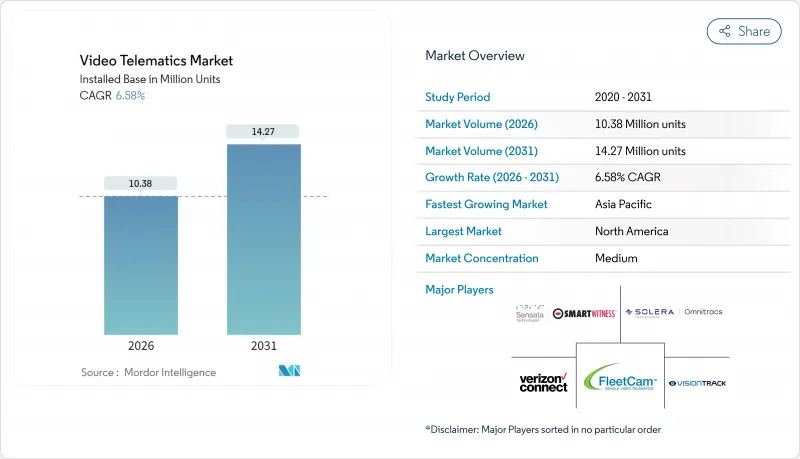

视讯远端资讯处理市场预计将从 2025 年的 974 万美元成长到 2026 年的 1,038 万美元,预计到 2031 年将达到 1,427 万美元,2026 年至 2031 年的复合年增长率为 6.58%。

欧洲对高级驾驶辅助系统 (ADAS) 和驾驶员监控系统的强制法规、人工智慧硬体成本的下降以及保险公司不断增加的奖励,正在加速商用车队采用这些系统。北美市场的成长仍然主要由保险业主导,保险公司将保费折扣与视频检验的驾驶行为挂钩;而亚洲市场的需求则得益于快速的电气化和智慧城市建设。整合 GPS、诊断和人工智慧影像的平台正在取代分散的系统,成为主流。这种整合趋势正在推动从一次性硬体销售转变为与云端分析相关的订阅收入模式。 Powerfleet 收购 Fleet Complete 等策略性收购表明,将影像、数据和车队管理整合到单一平台上的竞争日益激烈。

全球视讯远端资讯处理市场趋势与洞察

驾驶员监控和ADAS数据记录的监管要求

欧盟于2024年7月实施了GSR2法规,强制要求在新车认证中纳入智慧速度辅助系统、自动紧急煞车系统和驾驶疲劳侦测功能。联合国欧洲经济委员会(UNECE)发布的类似框架正在推动亚洲和美洲的监管协调。保险公司现在要求提供影像检验的ADAS资料以进行责任认定,这使得行车记录器从可选工具转变为强制性合规设备。持续发出驾驶分心警报的需求正促使车队采用与远端资讯处理仪錶板整合的多摄影机系统。随着区域部署的扩展,提供现成合规软体套件的供应商正在获得先发优势。这种连锁反应也延伸到售后改装领域,因为混合车龄的车队必须对老旧车辆进行改装,以满足与托运人和物流仲介的合约条款。

扩大整合影像解决方案在车队远端资讯处理的应用

过去,车队管理人员需要透过单独的合约来协调位置追踪、维护计划和影像安全管理。如今,整合式影像远端资讯处理平台只需一份订阅即可提供这些功能,将速度、位置和影像证据关联起来,从而简化工作流程并减少误报。 GPS 资料检验紧急制动,摄影机可以识别驾驶员分心的情况,从而提高驾驶员的接受度并提供即时安全指导。预测性维护也从中受益,因为 AI影像可以侦测加速车辆磨损的驾驶行为,并结合感测器诊断。 OEM 嵌入式远端资讯处理系统(预计 2023 年售出的新车中有 75% 将成为标配)将进一步推动系统集成,因为支援摄影机的线束简化了安装。云端部署正逐渐成为主流,无需本地伺服器即可为混合车队提供可扩展的分析。

隐私和资料保护合规障碍

GDPR法规要求获得明确同意、建立删除权工作流程以及对生物识别资料进行安全匿名化,这迫使车队营运商实施复杂的资料管治结构。跨境营运进一步增加了储存的复杂性,并提高了基础设施成本,因为某些司法管辖区限制了承包位置。隐私义务可能与建议持续记录的安全法规相衝突,而地理围栏遮蔽和即时人脸模糊处理会增加处理开销。能够提供一站式合规工具包的供应商价格较高,而小规模的供应商则难以获得必要的开发资金。跨多个地区的持续监管审查导致合规目标不断变化,需要持续的软体更新和法律咨询。

细分市场分析

2025年,整合系统将占据视讯远端资讯处理市场57.10%的份额,年复合成长率达7.89%,这主要得益于安全、维护和路线管理平台整合度的持续提高。将远端资讯处理资料与影像证据结合,能够提高侦测精度,增强导航效果,并减少警报疲劳。 OEM伙伴关係透过工厂预载带摄影机的线束,加速了整合系统的普及,减少了后期改装工作。同时,对于成本受限、需要基本录影功能但缺乏全面整合远端资讯处理系统的营运商而言,独立摄影机仍然是可行的选择。

普及势头推动了订阅经济模式的转变,这种模式与软体附加功能而非硬体利润率挂钩。嵌入式连线支援空中下载 (OTA) 更新,无需更换装置即可解锁新的分析功能。因此,整合用户的终身价值超过了单次摄影机销售的价值,这促使供应商将服务捆绑销售。併购活动也促使远端资讯处理公司收购专注影像的公司,以弥补自身能力缺口并确保持续收入。

根据诉讼辩护和保险折扣带来的既定投资回报率 (ROI),到 2025 年,重型卡车将占据视讯远端资讯处理市场 35.92% 的份额。监管机构强制要求为驾驶员遵守驾驶时间规定 (HOS) 而安装整合式电子记录设备 (ELD) 的摄像头,这正在巩固其在长途运输车队中的应用。随着城市推行以乘客安全为优先的「零愿景」目标,公车产业也稳步采用该技术。轻型商用车行业预计将实现温和成长,因为电子商务配送公司正在采用影像引导来减少拥挤城市道路上的轻微碰撞事故。

乘用车市场将以7.29%的复合年增长率实现最快成长,这主要得益于租赁公司将车辆损坏免赔额与即时驾驶员行为监控挂钩。基于使用量的保险试点计画正在引入摄影机进行遥测检验和诈欺防范,以提高消费者接受度。儘管价格敏感,但智慧型手机连接的摄影机适配器降低了准入门槛,使个人保险投保人无需永久安装即可体验视讯功能。随着整合硬体优势的显现,这将为未来进一步提升销售整合硬体铺平道路。

区域分析

北美在2025年仍维持38.30%的市场份额,这主要得益于成熟的远距资讯处理环境和保险公司的积极参与。保险公司鼓励小规模货运公司采用摄影机,并将安全驾驶表现与保费降低挂钩。更清晰的数据使用法规正在简化摄影机的普及过程,而5G网路在高流量路段的部署则实现了即时影片传输和近乎瞬时的理赔处理。竞争压力正从车队规模转向进阶分析,机器学习能够辨识事故发生前的预测性风险模式。

自GSR2实施以来,欧洲的普及速度加快,因为合规期限迫使车队管理公司安装驾驶员监控设备。同时,严格的GDPR法规强化了健全隐私保护的重要性,从而催生了对提供平台内匿名化和安全资料管道的营运商的需求。整合解决方案的成功源自于营运商对既满足安全法规要求又能优化营运的单一控制面板的渴望。对清洁运输走廊投资的不断增长,也使得人们更加关注用于检验绿色货运认证中环保驾驶性能的技术。

亚太地区将以7.38%的复合年增长率(CAGR)实现最快增长,直至2031年,这主要得益于大规模的电气化奖励和雄心勃勃的智慧城市计划。中国的电动物流车队需要对电池状态、充电模式和驾驶行为进行全面监控,从而推动了对电动车特性量身打造的影像分析技术的需求。印度强制要求校车和公共交通车辆进行位置跟踪,也同样扩大了潜在市场。区域供应链生产的低成本硬体进一步降低了进入门槛,使中小企业能够摆脱传统设施的限制,直接迈向云端分析时代。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 车队远端资讯处理整合影像解决方案的普及应用日益广泛

- 驾驶员监控和ADAS数据记录的监管要求

- 降低摄影机/边缘人工智慧成本

- 商用车辆安全合规性日益受到重视

- 从按使用量计费的保险过渡到影像检验理赔

- 道路图像资料货币化与智慧城市合作

- 市场限制

- 隐私和资料保护合规障碍

- 中小企业车队面临高昂的硬体和安装成本

- 高清和 4K 串流媒体的频宽和储存负载

- 视讯分析互通性缺乏开放标准

- 产业价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 投资分析

第五章 市场规模及成长预测(单位)

- 按类型

- 整合系统

- 独立系统

- 按车辆类型

- 大型卡车

- 公车和长途客车

- 轻型商用车(LCV)

- 搭乘用车

- 按部署模式

- 基于云端的

- 本地部署/混合部署

- 按组件

- 硬体(相机、DVR/NVR、感测器)

- 软体和分析

- 服务(安装、订阅、支援)

- 按地区

- 北美洲

- 南美洲

- 欧洲

- 亚太地区

- 中东和非洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 供应商市场占有率和定位

- Global Vendor Share

- North America Vendor Ranking

- Europe Vendor Ranking

- 公司简介

- SmartWitness(Sensata Technologies)

- Verizon Connect(Verizon Communications Inc.)

- Omnitracs(Solera Holdings Inc.)

- FleetCam(Pty)Ltd

- VisionTrack Ltd

- Lytx Inc.

- Nauto Inc.

- SureCam(Europe)Limited

- LightMetrics Inc.

- NetraDyne Inc.

- Geotab Inc.

- ATandT Inc.

- Fleet Complete Inc.

- Samsara Inc.

- Octo Group SpA

- Motive Technologies Inc.

- One Step GPS LLC

- MiX Telematics Ltd

- Trimble Transportation(Trimble Inc.)

- Streamax Technology Co. Ltd

- Howen Technologies Co. Ltd

- Micronet Ltd

- PFK Electronics(Pty)Ltd

- Blackvue(Pittasoft Co. Ltd)

- Garmin Ltd

- Zonar Systems Inc.

- Azuga Holdings Inc.

第七章 市场机会与未来展望

The video telematics market is expected to grow from USD 9.74 million in 2025 to USD 10.38 million in 2026 and is forecast to reach USD 14.27 million by 2031 at 6.58% CAGR over 2026-2031.

Mandated ADAS and driver-monitoring regulations in Europe, falling edge-AI hardware costs, and rising insurance incentives are accelerating adoption across commercial fleets. North American growth remains insurance-driven as carriers link premium discounts to video-verified driving behavior, while Asian demand rides on rapid electrification and smart-city programs. Integrated platforms that merge GPS, diagnostics, and AI video move to the forefront as fleets replace disparate systems, and the same convergence fuels a shift from one-time hardware sales toward subscription revenues tied to cloud analytics. Strategic acquisitions such as Powerfleet's purchase of Fleet Complete underscore the competitive race to bundle video, data, and fleet management within a single stack.

Global Video Telematics Market Trends and Insights

Regulatory mandates for driver-monitoring and ADAS data logging

The European Union enforced GSR2 in July 2024, requiring intelligent speed assist, autonomous emergency braking, and driver drowsiness detection in new vehicle approvals. Similar frameworks issued by the UN Economic Commission for Europe are prompting alignment in Asia and the Americas. Insurers now demand video-verified ADAS data to confirm liability, converting dashcams from discretionary tools into compliance necessities. The requirement for continuous driver-distraction warnings pushes fleets toward multi-camera installations that integrate with telematics dashboards. As regional rollouts widen, vendors that deliver off-the-shelf compliance packages gain a first-mover advantage. The cascading effect extends to aftermarket retrofits because mixed-age fleets must retrofit older vehicles to meet contract terms with shippers and logistics brokers.

Increasing adoption of fleet telematics-integrated video solutions

Fleet managers once balanced separate contracts for location tracking, maintenance scheduling, and video safety. Integrated video telematics platforms now bundle these functions under a single subscription, streamlining workflows and reducing false alerts by correlating speed, location, and video evidence. When GPS data validates harsh-brake events and cameras confirm distraction, driver acceptance rates improve and safety coaching becomes real time. Predictive maintenance also benefits, as AI video detects driver behavior that accelerates vehicle wear and combines it with sensor diagnostics. OEM-embedded telematics, standard on 75% of new cars sold in 2023, further propels system integration because camera-ready wiring harnesses simplify installation. Cloud deployment dominates, letting mixed fleets scale analytics without on-premise servers.

Privacy and data-protection compliance hurdles

GDPR rules require explicit consent for biometric data, right-to-erasure workflows, and secure anonymization, forcing fleets to deploy complex data-governance architectures. Cross-border operations further complicate storage because certain jurisdictions restrict cloud locations, raising infrastructure costs. Privacy obligations can clash with safety mandates that favor always-on recording, leading to geofenced masking and real-time face blurring that add processing overhead. Vendors able to deliver turnkey compliance toolkits gain a pricing premium, while smaller providers struggle to fund the necessary development. Ongoing legislative reviews in multiple regions keep compliance targets moving, prompting continuous software updates and legal consultations.

Other drivers and restraints analyzed in the detailed report include:

- Falling camera and edge-AI costs

- Growing safety-compliance focus among commercial fleets

- High hardware and installation costs for SMB fleets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Integrated systems controlled 57.10% of the video telematics market in 2025 and are expanding at an 7.89% CAGR as fleets consolidate platforms for safety, maintenance, and routing. The coupling of telematics data with video evidence increases detection accuracy, improving coaching while reducing alert fatigue. OEM partnerships accelerate uptake by factory-installing camera-ready harnesses that cut retrofitting labor. In contrast, standalone cameras persist among cost-constrained operators that need basic recording but lack resources for full telematics integration.

Deployment momentum favors subscription economics tied to software add-ons rather than hardware margins. Embedded connectivity supports over-the-air updates that unlock new analytics without swapping devices. As a result, the lifetime value of an integrated subscriber outpaces a one-off camera sale, motivating vendors to bundle services. M&A activity shows telematics firms buying vision specialists to close capability gaps and secure recurring revenues.

Heavy trucks captured 35.92% of the video telematics market share in 2025, anchored by well-established ROI through litigation defense and premium discounts. Regulatory bodies mandate ELD-integrated cameras for hours-of-service compliance, cementing penetration in long-haul fleets. Buses maintain steady uptake as municipalities adopt Vision Zero targets that prioritize passenger safety. Light commercial vehicles experience moderate growth as e-commerce couriers adopt video coaching to reduce fender-benders in dense urban routes.

Passenger cars post the steepest rise at a 7.29% CAGR, propelled by rental and leasing companies that tie damage-waiver fees to real-time driver behavior monitoring. Usage-based insurance pilots embed cameras to validate telemetry and curb fraud, broadening consumer exposure. Despite price sensitivity, smartphone-linked camera dongles lower barriers, allowing personal-line policyholders to trial video without permanent installations, priming a future upsell path to integrated hardware as benefits become evident.

The Video Telematics Market Report is Segmented by Type (Integrated Systems, and Stand-Alone Systems), Vehicle Type (Heavy Trucks, Buses and Coaches, Light Commercial Vehicles, and Passenger Cars), Deployment Model (Cloud-Based, and On-premises/Hybrid), Component (Hardware [Cameras, and More}, Software and Analytics, and Services [Installation, and More]), and Geography. The Market Forecasts are Provided in Terms of Value (Units).

Geography Analysis

North America retained 38.30% share in 2025 on the back of mature telematics ecosystems and strong insurer engagement. Carriers link premium savings to documented safe driving, encouraging even small haulers to add cameras. Regulatory clarity on data usage streamlines rollouts, and 5G coverage in high-traffic corridors allows real-time video transfer for near-instant claims processing. Competitive pressure now pivots away from installation counts toward advanced analytics, where machine learning identifies predictive risk patterns before incidents occur.

Europe shows brisk uptake following GSR2, as compliance deadlines leave fleets little choice but to install driver-monitoring hardware. The strict GDPR regime simultaneously elevates the importance of robust privacy safeguards, rewarding providers with in-platform anonymization and secure data pipelines. Integrated solutions prosper because operators prefer single dashboards that satisfy both safety mandates and business optimization imperatives. Increasing investment in clean transport corridors places further emphasis on technology that validates eco-driving credentials for green freight certification.

Asia Pacific posts the fastest growth at 7.38% CAGR to 2031, fueled by large-scale electrification incentives and ambitious smart-city programs. China's electric logistics fleets require combined monitoring of battery health, charging patterns, and driver behavior, generating incremental demand for video analytics tailored to EV dynamics. India's mandate for vehicle location tracking on school buses and public transport similarly broadens addressable volumes. Cost-efficient hardware produced in regional supply chains further lowers barriers, enabling smaller operators to leapfrog to cloud analytics without legacy equipment constraints.

- SmartWitness (Sensata Technologies)

- Verizon Connect (Verizon Communications Inc.)

- Omnitracs (Solera Holdings Inc.)

- FleetCam (Pty) Ltd

- VisionTrack Ltd

- Lytx Inc.

- Nauto Inc.

- SureCam (Europe) Limited

- LightMetrics Inc.

- NetraDyne Inc.

- Geotab Inc.

- ATandT Inc.

- Fleet Complete Inc.

- Samsara Inc.

- Octo Group SpA

- Motive Technologies Inc.

- One Step GPS LLC

- MiX Telematics Ltd

- Trimble Transportation (Trimble Inc.)

- Streamax Technology Co. Ltd

- Howen Technologies Co. Ltd

- Micronet Ltd

- PFK Electronics (Pty) Ltd

- Blackvue (Pittasoft Co. Ltd)

- Garmin Ltd

- Zonar Systems Inc.

- Azuga Holdings Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing adoption of fleet telematics-integrated video solutions

- 4.2.2 Regulatory mandates for driver-monitoring and ADAS data logging

- 4.2.3 Falling camera/edge-AI costs

- 4.2.4 Growing safety-compliance focus among commercial fleets

- 4.2.5 Usage-based-insurance shift to video-verified claims

- 4.2.6 Road-image data monetisation and smart-city partnerships

- 4.3 Market Restraints

- 4.3.1 Privacy and data-protection compliance hurdles

- 4.3.2 High hardware and installation costs for SMB fleets

- 4.3.3 Bandwidth / storage burdens for HD and 4K streaming

- 4.3.4 Lack of open standards for video-analytics interoperability

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (UNITS)

- 5.1 By Type

- 5.1.1 Integrated Systems

- 5.1.2 Stand-alone Systems

- 5.2 By Vehicle Type

- 5.2.1 Heavy Trucks

- 5.2.2 Buses and Coaches

- 5.2.3 Light Commercial Vehicles (LCV)

- 5.2.4 Passenger Cars

- 5.3 By Deployment Model

- 5.3.1 Cloud-based

- 5.3.2 On-premises / Hybrid

- 5.4 By Component

- 5.4.1 Hardware (Cameras, DVR/NVR, Sensors)

- 5.4.2 Software and Analytics

- 5.4.3 Services (Installation, Subscription, Support)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.2 South America

- 5.5.3 Europe

- 5.5.4 Asia Pacific

- 5.5.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Vendor Market Share and Positioning

- 6.4.1 Global Vendor Share

- 6.4.2 North America Vendor Ranking

- 6.4.3 Europe Vendor Ranking

- 6.5 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.5.1 SmartWitness (Sensata Technologies)

- 6.5.2 Verizon Connect (Verizon Communications Inc.)

- 6.5.3 Omnitracs (Solera Holdings Inc.)

- 6.5.4 FleetCam (Pty) Ltd

- 6.5.5 VisionTrack Ltd

- 6.5.6 Lytx Inc.

- 6.5.7 Nauto Inc.

- 6.5.8 SureCam (Europe) Limited

- 6.5.9 LightMetrics Inc.

- 6.5.10 NetraDyne Inc.

- 6.5.11 Geotab Inc.

- 6.5.12 ATandT Inc.

- 6.5.13 Fleet Complete Inc.

- 6.5.14 Samsara Inc.

- 6.5.15 Octo Group SpA

- 6.5.16 Motive Technologies Inc.

- 6.5.17 One Step GPS LLC

- 6.5.18 MiX Telematics Ltd

- 6.5.19 Trimble Transportation (Trimble Inc.)

- 6.5.20 Streamax Technology Co. Ltd

- 6.5.21 Howen Technologies Co. Ltd

- 6.5.22 Micronet Ltd

- 6.5.23 PFK Electronics (Pty) Ltd

- 6.5.24 Blackvue (Pittasoft Co. Ltd)

- 6.5.25 Garmin Ltd

- 6.5.26 Zonar Systems Inc.

- 6.5.27 Azuga Holdings Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment