|

市场调查报告书

商品编码

1934586

阻隔材料:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Barrier Material - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

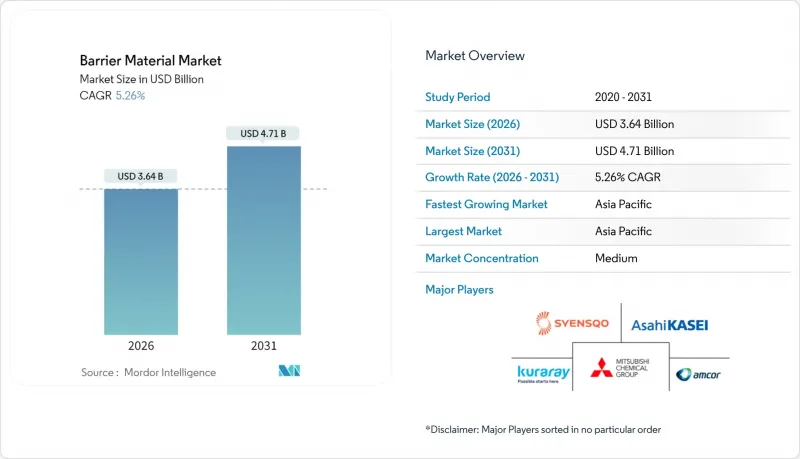

预计阻隔材料市场将从 2025 年的 34.6 亿美元成长到 2026 年的 36.4 亿美元,到 2031 年将达到 47.1 亿美元,2026 年至 2031 年的复合年增长率为 5.26%。

为延长食品保质期,市场对多层薄膜的需求不断增长;亚太地区药品产能迅速扩张;以及监管机构加速逐步淘汰 PFAS 化学品,这些都是推动市场成长的关键因素。品牌所有者对循环经济目标的承诺,促使他们投资于可回收的聚烯结构;而电子商务的快速发展,则鼓励加工商开发更坚固、更耐穿刺的包装形式,以确保在更长的供应链中保持阻隔性能。同时,铝、乙烯和丙烯等原料供应趋紧,导致供应合约中成本转嫁条款增多,并促使主要树脂生产商进行垂直整合。竞争优势正从绝对阻隔性能转向在环境影响更小、检验规性文件符合多个司法管辖区要求的前提下,提供同等保护。

全球阻隔材料市场趋势与洞察

包装食品的保质期要求

旨在减缓微生物生长和脂质氧化的氧气和水蒸气阻隔膜对于高水分烘焙食品、乳製品和蒸馏食品至关重要。采用香叶醇等植物来源活性成分配製的抗菌阻隔板可将麵包和酥皮点心的保质期延长5至10天,同时将迁移量控制在符合全球食品接触基准值的范围内。调节气体包装袋的氧气透过率低于0.1 cc/m²/天,有助于减少冷藏肉品中防腐剂的使用。韩国研究人员开发了一种可食用的几丁聚醣-没食子酸涂层,该涂层在不影响外观的前提下,增加了紫外线防护和抗菌性能,开闢了一个高端市场,其价格比标准包装材料高出20%至30%。延长保存期限与全球减少食物废弃物的目标直接相关,使阻隔材料市场成为联合国永续发展目标(SDG)12的关键驱动力。

亚太地区药品泡壳需求

日本的《药品接触材料正面表列》(将于2025年6月生效)规定,吸湿性原料原料药的透湿性必须低于0.05 g/m²/天,这将加速高品质PVDC和泡壳复合材料的应用。中国的GB 4806.7-2023和GB 43352-2023标准规定了低迁移限值,有利于拥有可靠分析数据和检验的无尘室薄膜的供应商。印度的药品出口正以每年超过15%的速度成长,迫使泡罩包装供应商同时满足美国FDA、欧洲药品管理局(EMA)和日本药品和医疗设备管理局(PMDA)的要求。这些趋势正促使全球加工商将薄膜生产在地化到亚太地区,从而增强区域供应安全并缩短前置作业时间。先进的阻隔结构也为生物相似药製剂提供了支持,这类製剂需要氧气含量低于1 ppm以维持蛋白质在运输过程中的稳定性。

铝环境法规

欧盟正考虑对铝包装征收每公斤0.80欧元的包装税,以反映其相比聚合物替代品更高的碳排放强度。这项政策预计将抑制软包装食品中铝箔的使用。品牌拥有者的生命週期评估模型显示,与具有功能涂层的单层聚乙烯(PE)结构相比,铝层会使包装的二氧化碳排放增加高达300%,这迫使即使是先前已确立性能标准的金属化薄膜也需要重新设计。虽然铝箔在超高湿度药品包装中仍然不可替代,但对低碳冶炼製程和无缝回收途径的探索正在加速进行。使用惰性阳极的电解测试表明,到2025年,每吨铝的二氧化碳当量排放量将减少7吨,但实用化仍需五年时间。同时,儘管材料成本高昂,但在聚对苯二甲酸乙二醇酯(PET)上沉淀氧化铝或二氧化硅涂层的多层结构正在获得市场份额,并重塑高端糖果甜点和咖啡产品的包装选择标准。

细分市场分析

由于其卓越的水蒸气和氧气阻隔性能,PVDC在2025年仍将保持44.60%的阻隔材料市场份额,这对于对湿度敏感的药品和高端加工肉品至关重要。面对环境监管机构对含氯聚合物日益严格的审查所带来的结构性挑战,加工商正在加速推进不含PVDC的结构试点,同时保持氧气阻隔性能(<0.1 cc/m²/天)。 EVOH具有结晶质乙烯嵌段结构,由于其高透明度和优异的干态氧气阻隔性能,且保持完全的相容性,因此展现出显着的增长势头,年复合增长率高达5.62%。

铝箔在泡壳包装盖和杀菌袋仍然发挥着至关重要的作用,这些包装对水蒸气透过率的要求低于0.001 g/m²/天。然而,碳排放税政策和铝箔价格的波动正促使品牌商寻求更环保的替代方案,转向PET基二氧化硅沉淀技术。聚萘二甲酸乙二醇酯(PEN)在高温应用和电子微胶囊化领域占据了一定的市场需求,在这些领域,尺寸稳定性比成本更为重要。研究方向包括氧化石墨烯涂层,这种涂层在奈米级厚度下可将氧气透过率降低99%,预计在卷轴式涂覆均匀性提高后,将于2028年起实现商业化应用。

阻隔材料报告按类型(铝、乙烯 - 乙烯醇共聚物 (EVOH)、Polyethylene Naphthalate甲酸乙二醇酯 (PEN)、聚偏二氯乙烯 (PVDC) 及其他)、用户行业(食品饮料、製药、农业、化妆品、汽车及其他)和地区(亚太、北美、欧洲、南美、中东和非洲)终端进行细分。市场预测以美元 (USD) 为以金额为准。

区域分析

亚太地区预计到2025年将占总收入的41.10%,这反映了该地区无与伦比的生产规模和监管协调,目前已与严格的美国和欧盟标准接轨。中国将于2024年实施GB 4806.7标准,将总迁移限值收紧至10 mg/dm²或以下,这促进了符合《药品法》第三类标准的高纯度EVOH树脂和PVDC-PVDC复合薄膜的快速认证。日本的正面表列将于2025年6月生效,这将推动日本国内加工商采用能够涂覆仅30 nm厚二氧化硅层的等离子涂层设备,从而在保持完全透明的同时,实现与铝箔相当的阻隔性。随着学名药核准加快,印度的泡壳包装出口预计将继续保持两位数的成长。对国内共挤出产能的投资正在推动成长,以降低运输延误和外汇风险。

在北美,电子商务的兴起以及加州《有毒物质减量法案》(其中包括对全氟烷基和多氟烷基物质 (PFAS) 的禁用)等日益严格的法规,推动了市场对防刺穿包装袋的需求。随着品牌商为应对生产者延伸责任制 (EPR) 的成本,采用单一材料聚乙烯 (PE) 包装袋的重新设计工作已在进行中。

欧洲在循环经济政策方面进展最为迅速,其《塑胶包装和回收利用条例》(PPWR)草案规定,到2030年,可回收设计是进入市场的先决条件。德国和法国正在试行软包装薄膜的押金返还制度。南美洲和中东及非洲虽然规模较小,但对收入成长表现出强烈的韧性,尤其是在强化食品和非处方药领域,这些产品需要能够抵御热带气候和配送中断的阻隔性包装。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 包装食品的保质期要求

- 亚太地区对药品泡壳包装的需求

- 电子商务主导的多层柔性包装

- 可再生聚烯阻隔涂层

- 不含 PFAS 的油脂隔离层法规

- 市场限制

- 原料成本波动

- 铝环境法规

- 多层薄膜回收问题

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 按类型

- 铝

- 乙烯 - 乙烯醇(EVOH)

- Polyethylene Naphthalate(PEN)

- 聚偏二氯乙烯(PVDC)

- 其他类型

- 按最终用户行业划分

- 食品/饮料

- 製药

- 农业

- 化妆品

- 车

- 其他的

- 按地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- ASEAN

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- 3M

- Amcor plc

- Arkema

- Asahi Kasei Corporation

- Coexpan

- Huhtamaki Oyj

- KURARAY CO., LTD.

- KUREHA CORPORATION

- Mitsubishi Chemical Group Corporation

- Mondi

- Sealed Air

- Syensqo

- TEIJIN LIMITED

- TOPPAN Inc.

- UFlex Limited

第七章 市场机会与未来展望

The Barrier Material market is expected to grow from USD 3.46 billion in 2025 to USD 3.64 billion in 2026 and is forecast to reach USD 4.71 billion by 2031 at 5.26% CAGR over 2026-2031.

Rising demand for multilayer films that extend food shelf life, rapid pharmaceutical capacity additions in Asia-Pacific, and accelerated regulatory moves away from PFAS chemicals are the principal forces shaping growth. Brand-owner commitments to circular-economy goals are steering investments toward recyclable polyolefin structures, while the e-commerce boom pushes converters to engineer tougher, puncture-resistant formats that preserve barrier integrity through longer supply chains. Concurrently, tightening raw-material supply balances for aluminum, ethylene and propylene are elevating cost-pass-through clauses in supply contracts, creating incentives for vertical integration among large resin producers. Competitive differentiation is shifting from absolute barrier performance to the ability to achieve comparable protection with lower environmental footprints and validated compliance dossiers across multiple jurisdictions.

Global Barrier Material Market Trends and Insights

Packaged-Food Shelf-Life Requirements

High-moisture bakery, dairy, and ready-meal categories rely on oxygen- and water-vapor-tight films engineered to slow microbial growth and lipid oxidation. Antimicrobial barrier plates infused with plant-based actives such as geraniol have demonstrated 5-10-day shelf-life extensions for breads and pastries, while maintaining migration levels below global food-contact thresholds. Modified-atmosphere pouches incorporating high-clarity EVOH achieve oxygen-transmission rates below 0.1 cc/m2/day, reducing the need for preservatives in chilled meats. Edible chitosan-gallic acid coatings developed by Korean researchers add UV protection and antimicrobial performance without altering appearance, opening premium niches that command 20-30% price uplifts over commodity packaging. Shelf-life extension aligns directly with global food-waste-reduction targets and positions the barrier material market as a central enabler of United Nations Sustainable Development Goal 12.

Pharmaceutical Blister Demand in APAC

Japan's Positive List for pharmaceutical contact materials, effective June 2025, mandates moisture-transmission rates below 0.05 g/m2/day for hygroscopic actives, accelerating adoption of premium PVDC and EVOH laminates. China's GB 4806.7-2023 and GB 43352-2023 standards embed low-migration limits that favor suppliers with robust analytical data and validated clean-room films. India's pharmaceutical exports are rising more than 15% annually, compelling blister suppliers to certify compliance with U.S. FDA, EMA and PMDA requirements simultaneously. These dynamics push global converters to localize film production in Asia-Pacific, strengthening regional supply security and shortening lead times. Advanced barrier structures also support biosimilar formulations, which require oxygen levels below 1 ppm to maintain protein stability during distribution.

Environmental Limits on Aluminum

The EU is evaluating an EUR 0.80/kg packaging tax on aluminum to reflect its high carbon intensity relative to polymer alternatives, a policy expected to curb thin-foil usage in snack-food flexibles. Brand-owner life-cycle assessment models show aluminum layers boosting package CO2 emissions by up to 300% versus mono-PE structures with functional coatings, prompting reformulation even where metallized films previously set performance benchmarks. Although foil remains irreplaceable in ultra-high-humidity pharmaceutical packs, the search for low-carbon smelting processes and latch-seamless recycling pathways has intensified. Pilot electrolysis cells using inert anodes demonstrated 7 tons CO2-equivalent savings per ton of aluminum in 2025, yet scale-up remains five years away. In the interim, multi-layer structures featuring evaporated aluminum oxide or silica coatings on PET are capturing share despite higher material costs, reshaping material selection criteria for premium confectionery and coffee formats.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce-Driven Multilayer Flexible Packaging

- Recyclable Polyolefin Barrier Coatings

- Recycling Challenges for Multilayers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PVDC retained a commanding 44.60% barrier material market share in 2025, owing to unmatched water-vapor and oxygen impermeability critical for moisture-sensitive pharmaceuticals and premium processed meats. The segment is confronting structural headwinds as environmental agencies scrutinize chlorine-containing polymers, incentivizing converters to pilot PVDC-free structures that still match sub-0.1 cc/m2/day oxygen-barrier thresholds. EVOH stands out, posting a 5.62% CAGR, because its crystalline ethylene blocks yield high clarity and exceptional dry-state oxygen protection while remaining fully compatible.

Aluminum foil sustains relevance in blister lidding and retort pouches where water-vapor-transmission rates must reside below 0.001 g/m2/day; however, carbon-tax scenarios and foil price volatility are nudging brand owners toward silica-oriented deposition on PET as a lower-footprint substitute. PEN addresses high-temperature and electronics micro-encapsulation uses, capturing niche demand where dimensional stability outweighs cost sensitivity. Research and devlopment pipelines include graphene-oxide coatings capable of achieving 99% reduction in oxygen permeation at nanoscale thicknesses, projected to reach commercial scale post-2028 once roll-to-roll coating uniformity improves.

The Barrier Material Report is Segmented by Type (Aluminum, Ethylene Vinyl Alcohol (EVOH), Polyethylene Naphthalate (PEN), Polyvinylidene Chloride (PVDC), and Other Types), End-User Industry (Food and Beverage, Pharmaceutical, Agriculture, Cosmetics, Automotive, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific contributed 41.10%, to 2025 revenue, reflecting unmatched manufacturing scale and regulatory harmonization that now mirrors stringent U.S. and EU standards. China's 2024 rollout of GB 4806.7 tightened total-migration limits to less than or equal to 10 mg/dm2, catalyzing the rapid qualification of high-purity EVOH resins and PVDC-PVDC duplex films certified under Type III pharmacopoeia requirements. Japan's June 2025 Positive List has propelled domestic converters to install plasma-coating units capable of applying only 30 nm thick silica layers, achieving aluminum-foil-like barriers while remaining fully transparent. India's blister-pack exports continue double-digit expansion as generic drug approvals accelerate, prompting investments in in-country co-extrusion capacity to sidestep shipping delays and currency risk.

North America is buoyed by e-commerce-triggered demand for puncture-resistant pouches and legislative action, such as California's toxin-reduction acts that eliminate PFAS usage. Brand responsiveness to Extended Producer Responsibility (EPR) fees is already visible in reformulations toward mono-material PE pouches.

Europe is advancing fastest on circular-economy mandates, with PPWR draft language stipulating design-for-recycling as a prerequisite for market access by 2030; Germany and France are piloting deposit-return schemes for flexible films. South America and the Middle East and Africa, while smaller, exhibit high elasticity to income growth, particularly for fortified foods and over-the-counter medicines, which require barrier formats resistant to tropical climates and distribution gaps.

- 3M

- Amcor plc

- Arkema

- Asahi Kasei Corporation

- Coexpan

- Huhtamaki Oyj

- KURARAY CO., LTD.

- KUREHA CORPORATION

- Mitsubishi Chemical Group Corporation

- Mondi

- Sealed Air

- Syensqo

- TEIJIN LIMITED

- TOPPAN Inc.

- UFlex Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Packaged-Food Shelf-Life Requirements

- 4.2.2 Pharmaceutical Blister Demand in APAC

- 4.2.3 E-Commerce-Driven Multilayer Flexible Packaging

- 4.2.4 Recyclable Polyolefin Barrier Coatings

- 4.2.5 PFAS-Free Grease Barrier Regulations

- 4.3 Market Restraints

- 4.3.1 Raw-Material Cost Volatility

- 4.3.2 Environmental Limits on Aluminum

- 4.3.3 Recycling Challenges for Multilayers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Aluminum

- 5.1.2 Ethylene Vinyl Alcohol (EVOH)

- 5.1.3 Polyethylene Naphthalate (PEN)

- 5.1.4 Polyvinylidene Chloride (PVDC)

- 5.1.5 Other Types

- 5.2 By End-user Industry

- 5.2.1 Food and Beverage

- 5.2.2 Pharmaceutical

- 5.2.3 Agriculture

- 5.2.4 Cosmetics

- 5.2.5 Automotive

- 5.2.6 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 3M

- 6.4.2 Amcor plc

- 6.4.3 Arkema

- 6.4.4 Asahi Kasei Corporation

- 6.4.5 Coexpan

- 6.4.6 Huhtamaki Oyj

- 6.4.7 KURARAY CO., LTD.

- 6.4.8 KUREHA CORPORATION

- 6.4.9 Mitsubishi Chemical Group Corporation

- 6.4.10 Mondi

- 6.4.11 Sealed Air

- 6.4.12 Syensqo

- 6.4.13 TEIJIN LIMITED

- 6.4.14 TOPPAN Inc.

- 6.4.15 UFlex Limited

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

永续包装涂料和阻隔材料市场预测至2034年—按材料类型、基材、技术、应用、最终用户和地区分類的全球分析

永续包装涂料和阻隔材料市场预测至2034年—按材料类型、基材、技术、应用、最终用户和地区分類的全球分析 阻隔材料市场:依材料种类、应用、技术及最终用途产业划分-2026-2032年全球市场预测静电屏蔽瓦楞纸板市场:依材料、终端用途产业及销售管道,全球预测(2026-2032年)

阻隔材料市场:依材料种类、应用、技术及最终用途产业划分-2026-2032年全球市场预测静电屏蔽瓦楞纸板市场:依材料、终端用途产业及销售管道,全球预测(2026-2032年) 捲烟衬垫市场-全球产业规模、份额、趋势、机会、预测:材料类型、涂层类型、最终用途、地区和竞争格局划分,2021-2031年全球原生纤维防油纸市场(按纸张类型、处理方式、纸张重量、应用和销售管道划分)预测(2026-2032年)全球氧气阻隔健康食品包装市场(依材料、包装类型、形状、阻隔性能及最终用途划分)-2026-2032年预测多层共挤薄膜市场(按材料、产品类型和应用划分)—全球预测,2026-2032年全球先进阻隔材料技术市场预测(至2032年):依产品类型、材料、技术、应用、最终用户及地区划分

捲烟衬垫市场-全球产业规模、份额、趋势、机会、预测:材料类型、涂层类型、最终用途、地区和竞争格局划分,2021-2031年全球原生纤维防油纸市场(按纸张类型、处理方式、纸张重量、应用和销售管道划分)预测(2026-2032年)全球氧气阻隔健康食品包装市场(依材料、包装类型、形状、阻隔性能及最终用途划分)-2026-2032年预测多层共挤薄膜市场(按材料、产品类型和应用划分)—全球预测,2026-2032年全球先进阻隔材料技术市场预测(至2032年):依产品类型、材料、技术、应用、最终用户及地区划分 阻隔材料市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

阻隔材料市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 全球阻隔材料市场

全球阻隔材料市场