|

市场调查报告书

商品编码

1934610

汽车金融:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Automotive Financing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

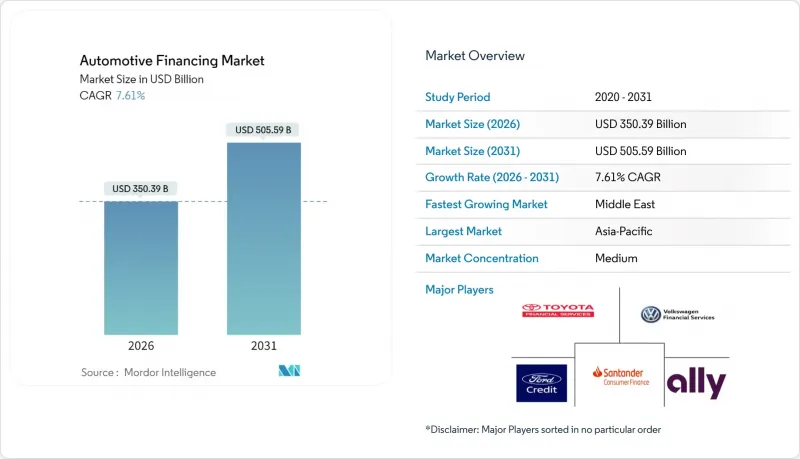

预计汽车金融市场规模将从 2025 年的 3,256.2 亿美元成长到 2026 年的 3,503.9 亿美元,预计到 2031 年将达到 5055.9 亿美元,2026 年至 2031 年的复合年增长率为 7.61%。

二手车贷款目前已占汽车金融市场的53.40%,并以9.2%的快速成长,预计到2030年仍将是主要的成长引擎。儘管基准利率居高不下,但数位借贷平台的激增、消费者对灵活支付方式日益增长的需求以及汽车电气化程度的提高,共同推动了二手车贷款市场的成长势头。 [1] 贷款机构正透过深化分析能力、拓展基于风险的定价模式以及与线上汽车零售平台合作来维持贷款业务的稳定。此外,将融资与增值出行服务(例如订阅套餐和电池租赁)相结合的能力,也正成为银行、汽车製造商金融公司和新兴金融科技参与企业的关键竞争优势。

全球汽车金融市场趋势与洞察

快速发展的线上汽车销售平台推动即时数位贷款

2024年,北美经销商和贷款机构的数位化交易量较去年同期成长显着。消费者现在预期线上购车后10分钟内即可获得贷款即时核准,与2023年常见的1至2天审批时间相比,数字大幅下降。整合利率比较Widgets的引入提高了价格透明度,挤压了那些没有自动定价工具的贷款机构的利润空间。这一趋势也蔓延至欧洲,在欧洲,多贷款机构API的引入使豪华车领域的平均贷款发放时间缩短了48%。在汽车製造商金融领域,将专有的金融计算器嵌入到OEM(原始设备製造商)的电子商务入口网站中,促进了保险和维护合约的交叉销售,提高了附加率和客户终身价值。

二手车交易量的增加催生了新的融资需求。

认证二手车专案正在改变消费者对二手车的认知,使贷款机构能够提供更接近新车的贷款额价值比 (LTV) 和利率。例如,起亚的六年全险认证二手车保固服务使其在美国的二手车销售占比在 2024 年提高了 5 个百分点。在欧洲,供应链中断后库存恢復正常,二手车供应量也随之回升,推动二手车平均贷款额年增 14%。将即时融资服务整合到二手车市场,使消费者能够在到店前锁定利率,从而缩短销售流程,降低贷款放弃率,并提高贷款成交率。

央行升息给净利差带来压力

截至2025年5月,美国政策利率徘徊在4.25%至4.5%的区间。不断上升的资金筹措成本挤压了贷款利差,导致银行2024年新增汽车贷款余额下降了3.4%。传统上提供具有竞争力利率的信用合作社缩减了72个月固定利率产品的供应,引导借款人选择更短的还款期限。在製造商奖励的支持下,汽车金融公司承担了部分利率压力以维持展示室客流量,从而扩大了市场份额。在欧洲,欧洲央行升息的滞后影响同样抑制了净利息收入,迫使贷款机构采用分级利率结构,将风险成本转移给信用评等较低的借款人。

细分市场分析

预计二手车在汽车金融市场中的份额将继续扩大,到2025年将占整个市场的53.10%,复合年增长率(CAGR)为9.02%,超过整体市场成长率。认证二手专案正在使保固服务普及化,让贷款机构将准新车视为低风险抵押品。数位化市场规模的进一步扩大,贷款Widgets整合到主要入口网站后,申请到核准的转换率提高了30%以上。因此,预计到2031年,二手车市场规模将超过2,917亿美元。

不断上涨的购车成本令一些优质借款人对购买新车望而却步。 2025年初,新车的平均月供已达742美元。为了因应价格上涨,经销商纷纷提案长期融资和租赁方案。然而,股权(即资产价值低于贷款余额)的置换车辆比例不断增加,使得残值计算变得更加复杂。儘管新车通路仍占据46.90%的市场份额,但成长放缓迫使贷款机构调整风险调整后的定价策略,并考虑捆绑保险产品,以在二手内燃机汽车(ICE)市场二手的情况下保障车辆的转售价值。

到2025年,银行将占据汽车金融市场46.05%的份额,但随着汽车製造商(OEM)旗下金融子公司的崛起,其主导地位正在下降。预计2026年至2031年,汽车製造商金融业务将以8.02%的复合年增长率成长,这主要得益于购车流程的整合以及优惠年利率的促销活动。光是大众汽车金融服务公司预计在2024年就将签署1,030万份新契约,使其市场渗透率提升至34.1%。信用合作社在汽车金融市场的份额预计将维持在20.10%左右,这主要得益于会员忠诚度和二手车贷款的优惠价格。

非银行金融公司占剩余的15.05%,它们利用另类资料触达信用记录不佳的客户。与分店银行相比,低成本的数位化模式可将贷款发放成本降低高达40%,而内建的金融API则使电商平台能够快速推出自有品牌的汽车贷款服务,从而推动业务量成长。对于传统银行而言,成本收入比仍将受到密切关注,而诸如承保自动化、简化文件工作流程以及与专业金融科技公司合作等战略倡议,对于其在更广泛的汽车金融行业中保持竞争力至关重要。

区域分析

亚太地区仍将是最具影响力的地区,到2025年将占据全球汽车金融市场41.00%的份额。中国电动车的蓬勃发展(预计到2024年将占新车销售的近一半)以及印度在FAME计画下推出的500亿美元电动车融资蓝图,确保了信贷需求的持续成长。数位化优先的信用评估、即时信用数据以及基于人工智慧的诈欺防范措施,使得先前缺乏正式信用记录的借款人也能获得贷款。随着政府对报废车辆的诱因不断扩大,贷款规模也变得更加稳健。例如,中国在推出10%的补贴计画仅六个月后,汽车更换购买量就成长了14%。

到2024年第四季,汽车贷款余额将达到1.66兆美元,拖欠率将达2.96%。贷款机构正在收紧信贷标准、提高首付比例,并投资预测分析以防止贷款损失。同时,美国汽车金融市场正受益于创新的金融科技合作,这些合作缩短了资金筹措週期,并将销售点融资服务扩展到了线上市场。专属贷款机构正在将远端维护合约与预测性服务提醒捆绑在一起,以保护抵押品价值并提高转售价值。

中东是成长最快的地区,预计到2031年将以10.29%的复合年增长率成长。沙乌地阿拉伯的银行信贷在2025年3月达到8,272亿美元,其符合伊斯兰教法的汽车贷款组合也持续以两位数的速度成长。政府的经济多元化政策优先发展交通出行,推动了对个人贷款和经营租赁产品的需求。数位化正在加速,沿岸地区35%的新车融资申请目前都是透过行动优先平台完成的。该地区的汽车金融业也受惠于其年轻的人口结构,海湾合作委员会成员国超过55%的公民年龄在35岁以下。灵活的订阅模式深受这群人青睐,正在改变产品设计。

欧洲的法规环境正在改变。英国最高法院对未揭露佣金做法的审查可能会改变经销商和租赁公司之间的经济关係,从而缩小利率差。电池租赁专案正在兴起,该专案将高价值电池组的所有权与车辆的所有权分离,有助于金融机构降低残值风险。斯堪地那维亚国家采用与融资合约挂钩的按收费付费保险,显示远端资讯处理数据可以作为风险调整定价的基础。

在南美洲和非洲,政策利率上升和货币波动正在抑制消费者的购买意愿,而基于人工智慧的替代信用评分系统则正在开拓新的借款人群体。在撒哈拉以南非洲,由于分店分行稀少,行动支付的普及正在加速贷款偿还。随着全球金融机构向这些地区扩张,它们正与当地的小额信贷机构和电信业者钱包服务商合作,建立混合融资结构,将风险分散到多个出资方。在汽车金融市场,面向叫车驾驶人的轻资产订阅车队预计将会普及,这将有助于建立正式的信用记录,从而为未来的个人购车提供支援。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 北美线上汽车销售平台的快速成长推动了对即时数位贷款的需求

- 欧洲二手车交易量的成长和认证二手车专案的推出,带动了新的贷款业务量。

- 亚太地区电动汽车租赁和订阅模式的快速成长将推动专属融资服务的普及。

- 政府的报废奖励和绿色金融补贴促进了中国和欧盟的汽车贷款发放。

- OEM直接融资公司「先买后付」和灵活的尾款支付产品在新兴市场的扩张

- 另类数据和基于人工智慧的信用评分系统正在帮助南美洲的次级贷款借款人。

- 市场限制

- 2023年起,央行升息将对汽车贷款机构的净利差构成压力。

- 美国次级汽车贷款违约率上升正在限制银行的信贷风险接受度。

- 印度和巴西的汽车贷款价值比(LTV)上限限制了贷款规模。

- 在电动车转型过程中,内燃机(ICE)的折旧风险削弱了残值假设。

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按类型

- 新车

- 二手车

- 按来源类型

- 专属原厂金融方案

- 银行

- 信用社

- 非银行金融机构

- 按车辆类型

- 搭乘用车

- 商用车辆

- 透过贷款产品

- 贷款

- 租

- 气球式付款

- 订阅

- 按地区

- 北美洲

- 我们

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 印尼

- 越南

- 菲律宾

- 澳洲

- 纽西兰

- 亚太其他地区

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 埃及

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Bank of America Corp.

- Ally Financial Inc.

- Hitachi Capital Corp.

- HDFC Bank Ltd.

- Bank of China

- Capital One Financial Corp.

- Wells Fargo & Co.

- Toyota Financial Services

- BNP Paribas SA

- Volkswagen Financial Services AG

- Mercedes-Benz Financial Services

- Standard Bank Group

- Mahindra Finance Ltd.

- Santander Consumer Finance

- General Motors Financial Company, Inc.

- Ford Motor Credit Co.

- Mitsubishi UFJ Lease & Finance Ltd.

- DBS Bank Ltd.

- Hyundai Capital Ltd.

第七章 市场机会与未来展望

The Automotive Finance market is expected to grow from USD 325.62 billion in 2025 to USD 350.39 billion in 2026 and is forecast to reach USD 505.59 billion by 2031 at 7.61% CAGR over 2026-2031.

Used-car financing, which already commands 53.40% of the automotive financing market, is growing at a rapid 9.2% pace and is set to remain the key growth engine through 2030. Digital origination platforms, heightened consumer appetite for flexible payment structures, and the continued electrification of vehicle fleets are together sustaining momentum even while benchmark rates remain elevated.[1]Lenders are responding by deepening analytics capabilities, widening risk-based pricing, and partnering with online auto-retail marketplaces to keep credit flowing. The ability to combine financing with value-added mobility services, such as subscription packages and battery leasing, is also becoming a decisive competitive lever for banks, OEM captives, and fintech entrants alike.

Global Automotive Financing Market Trends and Insights

Surging Online Auto-Retail Platforms Driving Instant Digital Financing

Digitized contracting volumes among dealers and lenders in North America surged year-on-year in 2024. Consumers now expect real-time credit approvals delivered inside a 10-minute online purchase journey, a dramatic acceleration from the 1-2-day turnaround common in 2023. Integrated rate-shopping widgets have heightened price transparency, squeezing margins for lenders that lack automated pricing tools. The trend is spreading to Europe, where multi-lender APIs have cut average time-to-funding by 48% in premium segments. For captive finance arms, embedding proprietary finance calculators inside OEM e-commerce portals is improving cross-selling of insurance and maintenance contracts, thereby lifting attachment rates and customer lifetime value.

Rising Used-Car Transactions Creating New Lending Volume

Certified pre-owned programs are reshaping consumer perceptions of second-hand vehicles, enabling lenders to offer loan-to-value ratios and rates closer to those on new cars. Kia's six-year bumper-to-bumper CPO warranty, for example, bolstered used-car penetration in the marque's U.S. portfolio by five percentage points in 2024. In Europe, inventory normalization after supply-chain shocks has restored late-model availability, pushing the average financed ticket size for used vehicles up 14% year-on-year. As used-car marketplaces integrate instant finance offers, origination conversion improves because consumers can lock rates before visiting a dealership, thereby shortening the sales funnel and reducing loan abandonment rates.

Central-Bank Rate Hikes Compressing Net-Interest Margins

Policy rates in the United States remain in a 4.25-4.5% corridor as of May 2025. The higher funding cost has squeezed lender spreads; new-auto loan balances at banks fell 3.4% in 2024. Credit unions, traditionally rate-competitive, cut long-term fixed offers for 72-month terms, nudging borrowers toward shorter tenors. Captive finance entities, cushioned by manufacturer incentives, absorbed part of the rate pressure to sustain showroom traffic, explaining their share gains. In Europe, the lagged pass-through of European Central Bank hikes is similarly dampening net-interest income, forcing originators to introduce tiered-rate structures that pass risk costs to lower-quality borrowers.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Growth of EV Leasing & Subscription Models Catalyzing Finance Penetration

- Government Scrappage Incentives & Green-Finance Subsidies

- Rising Delinquency Rates Constraining Credit Appetite

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The used-vehicle slice of the automotive financing market generated 53.10% of the automotive financing market in 2025 and will continue to widen its lead because its 9.02% CAGR exceeds overall market growth. Certified pre-owned programs have mainstreamed warranty coverage, letting lenders treat near-new units more like prime-risk collateral. Digital marketplaces further amplify scale: integrated loan widgets on leading portals lift application-to-approval conversion by more than 30%. As a result, the automotive financing market size for the used-segment is projected to top USD 291.7 billion by 2031.

Affordability headwinds are steering some prime borrowers away from new vehicles; average new-car payments hit USD 742 early in 2025. To mitigate sticker shock, dealers are pitching longer-term loans and leasing packages. However, the proportion of negative-equity trade-ins is rising, complicating residual-value mathematics. Although the new-vehicle channel retains 46.90% share, its slower growth will compel lenders to refine risk-adjusted pricing and to consider bundled insurance products that protect resale values in a softening ICE resale environment.

Banks generated 46.05% of the automotive financing market size in 2025, yet captive finance arms are eroding that lead. Captives are forecast to post an 8.02% CAGR from 2026 to 2031 as they leverage purchase-journey integration and subsidized APR promotions. Volkswagen Financial Services alone wrote 10.3 million new contracts in 2024, boosting penetration to 34.1%. The automotive financing market share of credit unions hovers near 20.10%, helped by member loyalty and competitive pricing on used-vehicle loans.

Non-bank financial companies contribute the balance 15.05%, using alternative data to expand into thin-file demographics. Their low-overhead digital models cut origination expense by up to 40% versus branch-centric banks. Embedded-finance APIs also allow e-commerce players to launch branded auto-loan offerings rapidly, driving incremental volume. For traditional banks, cost-to-income ratios will remain under scrutiny, setting a strategic imperative to automate underwriting, streamline document workflows and partner with fintech specialists to stay relevant in the broader automotive finance industry.

The Automotive Financing Market Report is Segmented by Type (New Vehicle and Used Vehicle), Source Type (OEM Captive Finance, Banks, and More), Vehicle Type (Passenger Cars and Commercial Vehicles), Financing Product (Loan, Lease, and More), and Geography (North America, South America, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained a 41.00% share of the automotive financing market in 2025 and remains the most influential region. China's EV boom, with EVs capturing nearly half of new-car sales in 2024, coupled with India's USD 50 billion EV-finance roadmap under the FAME scheme, ensures prolonged credit-demand growth. Digital-first underwriting, real-time bureau data, and AI-based fraud controls enable lenders to serve borrowers who previously lacked formal credit files. As governments expand scrappage incentives, loan volume elasticity is rising; a 10% rebate in China triggered a 14% jump in financed replacement purchases in just six months.

Auto-loan balances climbed to USD 1.66 trillion by Q4 2024, even as delinquency transitions reached 2.96%. Lenders are tightening credit tiers, boosting down-payment requests, and investing in predictive analytics to pre-empt charge-offs. The automotive financing market size in the United States nonetheless benefits from innovative fintech collaborations that shorten funding cycles and extend point-of-sale loan offers into online marketplaces. Captive lenders are bundling tele-maintenance subscriptions that send predictive service reminders, protecting collateral, and improving resale values.

The Middle East is the fastest-growing territory, projected to advance at a 10.29% CAGR to 2031. Saudi banking credit reached USD 827.2 billion in March 2025, with Shariah-compliant auto-loan portfolios expanding in double digits. Government diversification agendas prioritize mobility, sparking demand for both personal loans and operating-lease products. Digitalization levels are accelerating; mobile-first platforms now account for 35% of new auto applications in the Gulf. The automotive finance industry in the region also benefits from a young demographic, more than 55% of GCC citizens are under 35, whose preference for flexible subscription models is reshaping product design.

Europe region's regulatory environment is evolving; the UK Supreme Court's review of undisclosed commission practices could alter dealer-lender economics, potentially lowering rate spreads. Battery-lease programs that detach ownership of high-value packs from the vehicle are emerging, helping finance providers de-risk residual-value exposure. Scandinavia's embrace of pay-per-kilometre insurance tied to finance contracts illustrates how telematics data can underpin risk-adjusted pricing.

South America and Africa elevated policy rates and currency volatility pose affordability challenges, yet AI-driven alternative credit scoring is unlocking new borrower pools. Mobile money integration accelerates loan payments in sub-Saharan Africa, where branch infrastructure remains thin. For global lenders, entering these regions often requires partnering with local microfinance institutions or telco wallets, creating blended-finance structures that dilute risk across multiple capital providers. The automotive financing market is expected to see wider adoption of asset-light subscription fleets for ride-hail drivers, fostering formal credit histories that can support future personal-vehicle purchases.

- Bank of America Corp.

- Ally Financial Inc.

- Hitachi Capital Corp.

- HDFC Bank Ltd.

- Bank of China

- Capital One Financial Corp.

- Wells Fargo & Co.

- Toyota Financial Services

- BNP Paribas SA

- Volkswagen Financial Services AG

- Mercedes-Benz Financial Services

- Standard Bank Group

- Mahindra Finance Ltd.

- Santander Consumer Finance

- General Motors Financial Company, Inc.

- Ford Motor Credit Co.

- Mitsubishi UFJ Lease & Finance Ltd.

- DBS Bank Ltd.

- Hyundai Capital Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Online Auto-Retail Platforms Driving Demand for Instant Digital Financing in North America

- 4.2.2 Rising Used-Car Transactions and Certified Pre-Owned Programs in Europe Creating New Lending Volume

- 4.2.3 Rapid Growth of EV Leasing and Subscription Models in Asia-Pacific Catalyzing Captive Finance Penetration

- 4.2.4 Government Scrappage Incentives and Green-Finance Subsidies Accelerating Auto Loan Originations in China and EU

- 4.2.5 OEM Captives Expanding Buy-Now-Pay-Later and Flexible Balloon Payment Products in Emerging Markets

- 4.2.6 Alternative Data and AI-Based Credit Scoring Opening Sub-prime Borrower Segments in South America

- 4.3 Market Restraints

- 4.3.1 Central-Bank Rate Hikes Compressing Net Interest Margins for Auto Lenders Since 2023

- 4.3.2 Rising Delinquency Rates in U.S. Sub-prime Auto Segment Constraining Banks' Credit Appetite

- 4.3.3 Regulatory Caps on Vehicle Loan-to-Value Ratios in India and Brazil Limiting Financing Volumes

- 4.3.4 Depreciation Risk of ICE Vehicles Undermining Residual Value Assumptions amid EV Shift

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 New Vehicle

- 5.1.2 Used Vehicle

- 5.2 By Source Type

- 5.2.1 OEM Captive Finance

- 5.2.2 Banks

- 5.2.3 Credit Unions

- 5.2.4 Non-Bank Financial Institutions

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.4 By Financing Product

- 5.4.1 Loan

- 5.4.2 Lease

- 5.4.3 Balloon Payment

- 5.4.4 Subscription

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Indonesia

- 5.5.4.6 Vietnam

- 5.5.4.7 Philippines

- 5.5.4.8 Australia

- 5.5.4.9 New Zealand

- 5.5.4.10 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Bank of America Corp.

- 6.4.2 Ally Financial Inc.

- 6.4.3 Hitachi Capital Corp.

- 6.4.4 HDFC Bank Ltd.

- 6.4.5 Bank of China

- 6.4.6 Capital One Financial Corp.

- 6.4.7 Wells Fargo & Co.

- 6.4.8 Toyota Financial Services

- 6.4.9 BNP Paribas SA

- 6.4.10 Volkswagen Financial Services AG

- 6.4.11 Mercedes-Benz Financial Services

- 6.4.12 Standard Bank Group

- 6.4.13 Mahindra Finance Ltd.

- 6.4.14 Santander Consumer Finance

- 6.4.15 General Motors Financial Company, Inc.

- 6.4.16 Ford Motor Credit Co.

- 6.4.17 Mitsubishi UFJ Lease & Finance Ltd.

- 6.4.18 DBS Bank Ltd.

- 6.4.19 Hyundai Capital Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

汽车金融市场:2026-2032年全球市场预测(依客户类型、贷款形式、信用评级、车辆类型及销售管道)

汽车金融市场:2026-2032年全球市场预测(依客户类型、贷款形式、信用评级、车辆类型及销售管道) 汽车金融市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测人工智慧驱动的残值预测市场:策略洞察与预测(2026-2031)汽车里程融资市场:策略性洞察与预测(2026-2031 年)租赁,2035:未来出行金融

汽车金融市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测人工智慧驱动的残值预测市场:策略洞察与预测(2026-2031)汽车里程融资市场:策略性洞察与预测(2026-2031 年)租赁,2035:未来出行金融 美国汽车贷款:市场份额分析、行业趋势和统计数据以及成长预测(2026-2031 年)全球汽车租赁服务市场规模、份额、趋势和成长分析报告(2026-2034)

美国汽车贷款:市场份额分析、行业趋势和统计数据以及成长预测(2026-2031 年)全球汽车租赁服务市场规模、份额、趋势和成长分析报告(2026-2034) 汽车金融市场规模、份额和成长分析(按提供者类型、车辆类型、金融类型和地区划分)-2026-2033年产业预测

汽车金融市场规模、份额和成长分析(按提供者类型、车辆类型、金融类型和地区划分)-2026-2033年产业预测 汽车金融市场规模、份额和成长分析(按车龄、用途、分销管道、应用和地区划分)-2026-2033年产业预测

汽车金融市场规模、份额和成长分析(按车龄、用途、分销管道、应用和地区划分)-2026-2033年产业预测 汽车金融平台市场预测至2032年:按类型、贷款类型、车辆类型、最终用户和地区分類的全球分析

汽车金融平台市场预测至2032年:按类型、贷款类型、车辆类型、最终用户和地区分類的全球分析