|

市场调查报告书

商品编码

1934668

非洲农业拖拉机机械:市场份额分析、行业趋势与统计、成长预测(2026-2031 年)Africa Agricultural Tractor Machinery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

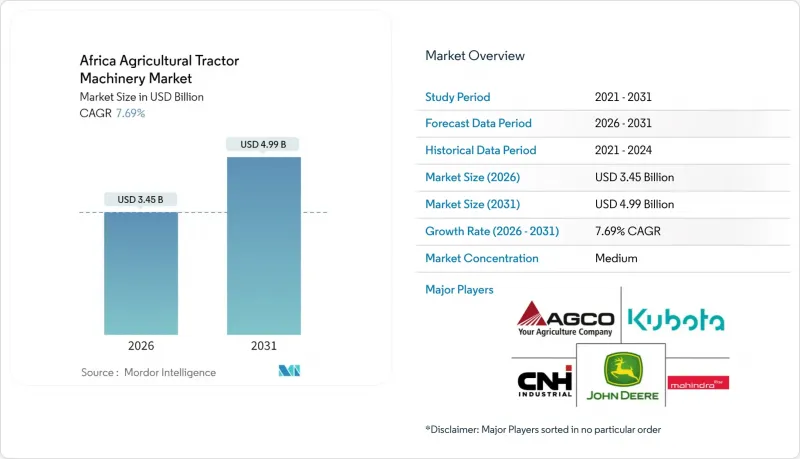

预计非洲农业拖拉机机械市场将从 2025 年的 32 亿美元成长到 2026 年的 34.5 亿美元,预计到 2031 年将达到 49.9 亿美元,2026 年至 2031 年的复合年增长率为 7.69%。

这一增长反映了透过有针对性的补贴、不断发展的数位化就业平台以及气候智慧型农机设备的兴起,弥合日益扩大的机械化差距,使得拖拉机在非洲多样化的生产系统中成为必不可少的工具。在各国政府继续提供该地货币信贷的同时,捐助者支持的计划正在创造对精准喷药机、播种机和配备GPS的节油节料拖拉机的新需求。儘管面临货币贬值和海关延误等结构性阻力,但计量收费的经营模式,加上低成本的全散件组装(CKD),正开始缓解长期以来阻碍机械化普及的价格障碍。同时,大型商业农场的马力需求不断增长,导致产品组合出现两极分化,从小规模的90马力以下机型到面向出口型农场的450马力机型,不一而足。原始设备製造商(OEM)正透过本地组装、车队融资方案和售后服务中心来应对这一需求,从而增强品牌忠诚度,并提高整个非洲大陆的运转率。

非洲农业拖拉机机械市场趋势与洞察

政府机械化补贴和拖拉机贷款计划

泛非地区的赠款计画和优惠信贷机制正在迅速降低拖拉机购买门槛,刺激整个非洲农业拖拉机市场的需求。自2015年以来,尼日利亚的「锚定借款人计画」已向耕种530万公顷土地的480万农民提供了1.12兆奈拉(约15亿美元)的资金。农业信贷担保计画基金为75%的贷款提供担保,降低了贷款机构的风险。肯亚2024/25财政年度预算也加强了类似力度,为农业部门拨款683亿肯亚先令(约合5.2亿美元)。这笔资金用于支持农业企业家营运的拖拉机车队,以及分发230台牛奶冷却器以整合酪农价值链。目前,肯亚的平均拖拉机普及率仍为每公顷0.27马力,而亚洲的平均水平为每公顷1.5马力,这表明透过机械化实现成长仍有很大的空间。儘管18%至30%的高名目利率限制了信贷获取,但该地货币金融产品的增加和部分风险担保的引入正在改善农村地区的信贷获取状况。这些措施对于支持非洲农业拖拉机机械市场预期的成长轨迹至关重要。

非洲大规模商业农业的扩张

农业集约化正在推动市场对更高功率的机型和更先进的农机设备的需求。埃及的沙漠农业计划通常由企业控股,耕地面积达7500至9000英亩(约3000至3600公顷),采用中心枢轴式灌溉和机械化收割,需要配备GPS导航系统的120至450马力拖拉机。机构投资者已在全球农场收购中投入450亿美元,其中一些投资瞄准了非洲的大型农场,因为规模经济效益足以支撑高性能设备的投入使用。新兴的排碳权计画鼓励犁地和覆盖作物种植,进一步加速了机械化进程,因为大型农场需要精确追踪投入使用情况和产量,以创造额外的收入来源。因此,非洲农用拖拉机市场对具备先进远端资讯处理功能的高阶机型的需求正在逐步增长,从而推高了平均售价。鑑于私募股权、退休基金和主权财富基金等投资者制定了长达数十年的土地开发计划,这一趋势具有长期性,并且不太容易受到週期性商品价格波动的影响。

CKD试剂盒关税高昂且海关手续复杂

儘管组装拖拉机的名目关税较低,但由于单证障碍、港口拥塞和检验制度不一致等问题,非洲市场的实际泊位成本比发票价格高出25%。在奈及利亚,CKD货物的清关週期长达60至90天,导致当地组装的流动资金被冻结。肯亚蒙巴萨港也面临类似的积压问题,滞期费推高了整体成本。儘管《非洲大陆自由贸易协定》(AfCFTA)承诺协调贸易流程,但其执行情况仍不均衡,海关单证的数位化也尚处于起步阶段。在清关时间恢復正常之前,製造商将面临漫长的现金週转週期,这不仅会加剧库存规划的难度,还会阻碍新企业进入非洲农业拖拉机市场。

细分市场分析

截至2025年,犁地机械在非洲农业拖拉机市场收入份额中占比30.68%,这主要得益于旋耕机、耕耘机和耙等农机具对耕作设备的需求,这些设备用于整地,以准备零散的农田。尚比亚每公顷19-28美元、津巴布韦每公顷51-69美元的机械化服务合约价格,也印证了犁地作业的持续需求。然而,在马拉威和尚比亚的部分地区,畜力耕作仍占耕作总量的57%,显示尚未完全过渡到以拖拉机为基础的耕作系统。保护性农业计画正在推广犁地农业,但由于专用播种机成本高且需要额外的杂草管理专业知识,因此免耕技术的普及程度有限。儘管在预测期内,该细分市场的相对份额可能会被精准农业工具蚕食,但随着粮食产量的增长,其绝对销售量预计仍将保持增长。

喷雾器是成长最快的产品线,预计到2031年将以9.67%的复合年增长率成长,重塑非洲农业拖拉机机械市场格局。中东和非洲地区到2024年将登记95万台喷雾器,其中尼日利亚和南非合计将达到34万台。目前,曳引机式喷雾器占全球需求的34%至38%,取代了手动背负式喷雾器,提高了喷洒均匀性,同时减少了人工工时。太阳能喷雾器可在无电网农场实现零排放作业,但电池成本和充电基础设施的缺乏阻碍了其主流应用。精准化学、可变流量喷嘴和物联网感测器也正在被广泛采用,这与援助机构呼吁发展气候智慧型农业的概念相符。由于仍有51%的非洲农民共用或租赁喷雾器,租赁池和数位化预订平台将继续在推动喷雾器的进一步普及方面发挥关键作用。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 政府机械化补贴和拖拉机贷款计划

- 非洲大规模商业农业的扩张

- 计量型拖拉机租赁数位平台的普及

- 气候智慧型农业计画推动了对精准农业设备的需求。

- 扩大可再生能源驱动的自动驾驶拖拉机的应用

- 中非工业园区实现低成本CKD拖拉机组装

- 市场限制

- CKD试剂盒进口关税高昂,海关手续复杂

- 售后服务网路分散,限制了机器的运作

- 货币贬值导致进口零件成本上升

- 土地所有权的不确定性阻碍了长期机械投资。

- 监管环境

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依产品类型

- 犁地机械

- 犁

- 光环

- 耕耘机

- 其他设备

- 种植机械

- 播种机

- 播种机

- 撒布器

- 其他播种机

- 喷雾器

- 干草和饲料机械

- 收割者和护髮素

- 打包机

- 其他干草和饲料机械

- 其他类型

- 犁地机械

- 按地区

- 奈及利亚

- 南非

- 肯亚

- 其他非洲地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Deere and Company

- CNH Industrial

- AGCO Corporation

- Mahindra and Mahindra

- Kubota Corporation

- Tractors and Farm Equipment Ltd(Amalgamations Group)

- Yanmar Holdings Co., Ltd.

- International Tractors Ltd-Sonalika

- CLAAS KGaA mbH

- Weichai Lovol Intelligent Agriculture(Weichai Group)

- LS Mtron Ltd(LS Group)

- SDF Group-Same Deutz-Fahr

- Tumosan Motor ve Traktor Sanayi AS

- Dongfeng Agricultural Machinery Group

- Zetor Tractors as(HTC Holding)

第七章 市场机会与未来展望

The Africa agricultural tractor machinery market is expected to grow from USD 3.20 billion in 2025 to USD 3.45 billion in 2026 and is forecast to reach USD 4.99 billion by 2031 at 7.69% CAGR over 2026-2031.

This expansion reflects widening mechanization gaps being closed through targeted subsidies, growing digital hiring platforms, and the rise of climate-smart implements that make tractors indispensable across a variety of African production systems. Governments continue to anchor credit lines in local currencies, while donor-backed projects create new demand for precision sprayers, planters, and GPS-enabled tractors capable of conserving fuel and inputs. Despite structural headwinds such as currency depreciation and customs delays, pay-per-use business models combined with lower-cost CKD (Completely Knocked Down) assembly have begun easing the affordability barrier that long constrained mechanization adoption. Large-scale commercial farms are simultaneously pushing horsepower requirements higher, creating a bifurcated product mix that ranges from sub-90 horsepower units for smallholders to 450 horsepower machines for export-oriented estates. Original equipment manufacturers are responding with localized assembly, fleet-financing packages, and after-sales service hubs that tighten brand loyalty while improving uptime across the continent.

Africa Agricultural Tractor Machinery Market Trends and Insights

Government Mechanization Subsidies and Tractor Financing Schemes

Pan-African subsidy programs and concessional credit lines have rapidly lowered purchase barriers for tractor ownership, stimulating demand across the Africa agricultural tractor machinery market. Nigeria's Anchor Borrowers' Programme disbursed ₦1.12 trillion (USD 1.5 billion) to 4.8 million farmers cultivating 5.3 million hectares since 2015, while the Agricultural Credit Guarantee Scheme Fund covers 75% of loan defaults, mitigating lender risk. Kenya reinforced a similar approach in its 2024/25 budget, allocating KES 68.3 billion (USD 520 million) for agriculture, including tractor fleets operated by agripreneurs and the distribution of 230 milk coolers that integrate dairy value chains. Average tractor density remains just 0.27 horsepower per hectare versus 1.5 horsepower per hectare in Asia, underscoring the scope for mechanization gains. Although high nominal interest rates between 18% and 30% limit credit uptake, the growing presence of local-currency instruments and partial-risk guarantees is easing access in rural areas. These programs thereby underpin the projected growth trajectory of the Africa agricultural tractor machinery market.

Expansion of Large-Scale Commercial Farming Across Africa

Consolidation of farmland is shifting demand toward larger horsepower models and sophisticated implements. Egypt's desert agriculture projects operate corporate holdings of 7,500 to 9,000 acres, using center-pivot irrigation and machine harvesting that call for GPS-guided 120-450 horsepower units. Institutional capital has already deployed USD 45 billion into global farm acquisitions, a portion of which targets African estates where scale efficiencies justify premium equipment. Emerging carbon-credit programs that reward no-till and cover crops further accelerate mechanization, because large farms must track input use and yields precisely to earn additional revenue streams. As a result, the Africa agricultural tractor machinery market is witnessing a gradual tilt toward high-end models with advanced telematics, boosting average selling prices. The trend is long-term in nature and resilient to cyclical commodity swings, given the multi-decade land-development horizons of private equity, pension funds, and sovereign wealth investors.

High Import Tariffs and Complex Customs Procedures for CKD Kits

Despite low nominal tariffs on assembled tractors, documentation hurdles, port congestion, and varied inspection regimes keep effective landed costs up to 25% above invoice prices in several African markets. Nigeria's clearance cycle stretches 60-90 days for CKD consignments, immobilizing working capital for local assemblers. Kenya's Mombasa port faces similar backlogs, with demurrage charges increasing total costs. While AfCFTA promises to harmonize trade processes, implementation remains uneven, and the digitization of customs paperwork is still in early stages. Until clearance times normalize, manufacturers face elongated cash conversion cycles that weigh on inventory planning and deter new entrants in the Africa agricultural tractor machinery market.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of Pay-Per-Use Tractor Hiring Digital Platforms

- Climate-Smart Agriculture Programs Driving Demand for Precision Implements

- Fragmented After-Sales Service Networks Limiting Machinery Uptime

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The plowing and cultivating category held a 30.68% revenue share of the Africa agricultural tractor machinery market in 2025, driven by rotovators, cultivators, and harrows that prepare fragmented plots for planting. Contract mechanization services priced between USD 19-28 per hectare in Zambia and USD 51-69 per hectare in Zimbabwe underline the persistent need for tillage operations. Nonetheless, animal draft power still covers up to 57% of tillage in parts of Malawi and Zambia, indicating that full transition to tractor-based systems is incomplete. Conservation agriculture programs promote no-till practices, but uptake remains limited because specialized planters are expensive and weed management requires additional knowledge. Over the forecast horizon, the segment is likely to cede relative share to precision implements, yet absolute volumes will still grow on the back of rising food output.

Sprayers form the fastest-growing product line, advancing at a 9.67% CAGR through 2031 and reshaping the Africa agricultural tractor machinery market. The Middle East and Africa region registered 0.95 million sprayer units in 2024, with Nigeria and South Africa jointly accounting for 0.34 million. Tractor-mounted configurations now capture 34-38% of global demand, replacing manual knapsack units and cutting labor hours while improving coverage uniformity. Solar-powered sprayers offer emissions-free operation for off-grid farms, although battery costs and charging gaps postpone mainstream adoption. Precision chemistry, variable-rate nozzles, and IoT sensors are also entering the field, aligning with donor mandates for climate-smart agriculture. Given that 51% of African farmers still share or rent sprayers, leasing pools and digital booking platforms will remain pivotal in unlocking further penetration.

The Africa Agricultural Tractor Machinery Market Report is Segmented by Product Type ( Plowing and Cultivating Machinery, Planting Machinery, Sprayers, Haying and Forage Machinery, and Other Types) and by Geography (Nigeria, South Africa, Kenya, and Rest of Africa). The Report Offers the Market Size and Forecasts in Terms of Value (USD).

List of Companies Covered in this Report:

- Deere and Company

- CNH Industrial

- AGCO Corporation

- Mahindra and Mahindra

- Kubota Corporation

- Tractors and Farm Equipment Ltd (Amalgamations Group)

- Yanmar Holdings Co., Ltd.

- International Tractors Ltd -Sonalika

- CLAAS KGaA mbH

- Weichai Lovol Intelligent Agriculture (Weichai Group)

- LS Mtron Ltd (LS Group)

- SDF Group - Same Deutz-Fahr

- Tumosan Motor ve Traktor Sanayi A.S.

- Dongfeng Agricultural Machinery Group

- Zetor Tractors a.s. (HTC Holding)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government mechanization subsidies and tractor financing schemes

- 4.2.2 Expansion of large-scale commercial farming across Africa

- 4.2.3 Proliferation of pay-per-use tractor hiring digital platforms

- 4.2.4 Climate-smart agriculture programs driving demand for precision implements

- 4.2.5 Rising adoption of renewable-powered autonomous tractors

- 4.2.6 China-Africa industrial parks enabling low-cost CKD tractor assembly

- 4.3 Market Restraints

- 4.3.1 High import tariffs and complex customs procedures for CKD kits

- 4.3.2 Fragmented after-sales service networks limiting machinery uptime

- 4.3.3 Currency depreciation increasing the cost of imported components

- 4.3.4 Land tenure uncertainties discouraging long-term machinery investment

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Plowing and Cultivating Machinery

- 5.1.1.1 Plows

- 5.1.1.2 Harrows

- 5.1.1.3 Rotovators and Cultivators

- 5.1.1.4 Other Equipment

- 5.1.2 Planting Machinery

- 5.1.2.1 Seed Drills

- 5.1.2.2 Planters

- 5.1.2.3 Spreaders

- 5.1.2.4 Other Planting Machinery

- 5.1.3 Sprayers

- 5.1.4 Haying and Forage Machinery

- 5.1.4.1 Mowers and Conditioners

- 5.1.4.2 Balers

- 5.1.4.3 Other Haying and Forage Machinery

- 5.1.5 Other Types

- 5.1.1 Plowing and Cultivating Machinery

- 5.2 By Geography

- 5.2.1 Nigeria

- 5.2.2 South Africa

- 5.2.3 Kenya

- 5.2.4 Rest of Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Deere and Company

- 6.4.2 CNH Industrial

- 6.4.3 AGCO Corporation

- 6.4.4 Mahindra and Mahindra

- 6.4.5 Kubota Corporation

- 6.4.6 Tractors and Farm Equipment Ltd (Amalgamations Group)

- 6.4.7 Yanmar Holdings Co., Ltd.

- 6.4.8 International Tractors Ltd -Sonalika

- 6.4.9 CLAAS KGaA mbH

- 6.4.10 Weichai Lovol Intelligent Agriculture (Weichai Group)

- 6.4.11 LS Mtron Ltd (LS Group)

- 6.4.12 SDF Group - Same Deutz-Fahr

- 6.4.13 Tumosan Motor ve Traktor Sanayi A.S.

- 6.4.14 Dongfeng Agricultural Machinery Group

- 6.4.15 Zetor Tractors a.s. (HTC Holding)

7 Market Opportunities and Future Outlook

农业拖拉机市场:按功率范围、拖拉机类型、燃料类型、应用和最终用户划分 - 全球市场预测(2026-2032 年)

农业拖拉机市场:按功率范围、拖拉机类型、燃料类型、应用和最终用户划分 - 全球市场预测(2026-2032 年) 2026年全球小型农用拖拉机市场报告2026年全球农业拖拉机租赁市场报告电动农用拖拉机市场:2026-2032年全球市场预测(按推进方式、驱动系统、运作小时数、自主等级、功率输出、作物类型、应用、最终用户和销售管道)农业拖拉机市场:按发动机功率、产品类型、拖拉机类型、应用和销售管道,全球预测,2026-2032年

2026年全球小型农用拖拉机市场报告2026年全球农业拖拉机租赁市场报告电动农用拖拉机市场:2026-2032年全球市场预测(按推进方式、驱动系统、运作小时数、自主等级、功率输出、作物类型、应用、最终用户和销售管道)农业拖拉机市场:按发动机功率、产品类型、拖拉机类型、应用和销售管道,全球预测,2026-2032年 农业拖拉机市场规模、份额、成长及全球产业分析:按类型、应用和地区划分-2026-2034年洞察与预测

农业拖拉机市场规模、份额、成长及全球产业分析:按类型、应用和地区划分-2026-2034年洞察与预测 农业拖拉机:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)全球农业拖拉机市场规模、份额、趋势和成长分析报告(2026-2034年)2026年全球农业导航与转向系统市场报告2026年全球农业拖拉机市场报告

农业拖拉机:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)全球农业拖拉机市场规模、份额、趋势和成长分析报告(2026-2034年)2026年全球农业导航与转向系统市场报告2026年全球农业拖拉机市场报告