|

市场调查报告书

商品编码

1937274

农业拖拉机:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)Agricultural Tractors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

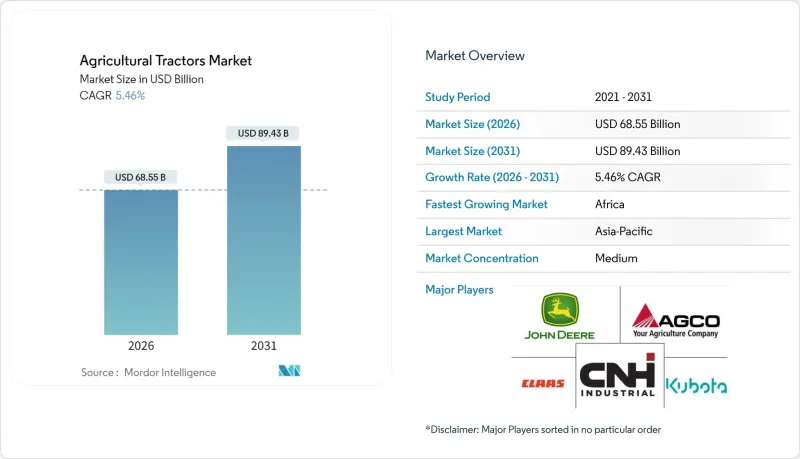

预计农业拖拉机市场将从 2025 年的 650 亿美元成长到 2026 年的 685.5 亿美元,到 2031 年将达到 894.3 亿美元,2026 年至 2031 年的复合年增长率为 5.46%。

目前成长得益于新兴经济体持续的机械化进程、已开发地区精密农业的快速转型以及电动和自动驾驶拖拉机平台的早期商业化。亚太地区保持最强劲的成长势头,印度的大规模补贴计画和中国的农业现代化建设推动了更新换代需求。同时,非洲的成长速度最快,这主要得益于CAADP 2.0设定的最低机械化目标和优惠融资政策。 40-100马力等级的拖拉机为中型农场提供了最佳的动力成本比,而两轮驱动配置则因其购置成本低、易于维护而继续占据主导地位。多用途拖拉机可满足从犁地到物料搬运等各种农业应用需求。然而,随着大型粮食公司试点无人驾驶系统以应对劳动力短缺并优化田间作业,自动驾驶拖拉机正经历爆发式增长。儘管全球供应商整合程度仍然较为温和,但区域品牌凭藉成本优化的产品线和本地化的分销网络继续蓬勃发展。 Tier 4 F 引擎的供应链波动和利率上升影响经销商的楼层平面图融资,这在短期内构成不利因素,但精密农业改造需求和电气化倡议将继续推动长期成长动能。

全球农业拖拉机市场趋势与洞察

印度和巴西的补贴续期

印度已将「农民信用卡计画」下的补贴贷款机制延长至2029财年,并拨款1.68兆卢比(约202亿美元)用于农业机械化。其中,拖拉机约占贷款额的15%。巴西的「加强家庭农业国家计画」提供3%利率的贷款,以减轻40至100马力拖拉机的购买负担。预计从2022年起,人事费用将上涨40%至60%,因此,对于5公顷及以上的农场而言,引进拖拉机已变得经济可行,这将加速农业拖拉机市场的扩张。

60马力以下作业拖拉机的电气化

功率低于60马力的电动拖拉机在果园和温室中越来越受欢迎,因为零排放可以降低排放成本并符合当地法规。芬特(Fendt)的e100 Vario电动拖拉机运作长达6小时,欧盟的「绿色新政」为购买电动农业机械提供高达40%的补贴。加州空气资源委员会也强制要求公用事业车辆在2030年前达到零排放标准,为电气化提供监管支援。虽然电池组的成本目前仍为每千瓦时400至600美元,但国际能源总署(IEA)预测,到2030年,电池成本将下降40%,届时价格将与传统燃油动力拖拉机持平。

电动车型电池组成本高成本

电动拖拉机的普及面临巨大的阻力:电池组成本是汽车电池组的两到三倍,儘管环保法规日益严格,但市场渗透率仍然有限。农用锂离子电池组的成本在每千瓦时400至600美元之间,大约是轻型车辆电池成本的三倍。即使考虑到较低的营运成本和政府奖励,电动拖拉机五年内的总拥有成本也比同等柴油拖拉机高出20%至40%。在农业应用中,拖拉机通常在多尘、高振动的环境中运作,并且充电週期不规律,这会加速电池的劣化。电池有效容量每年下降15%至25%,进一步降低了商业化农业生产的经济效益。

细分市场分析

截至2025年,40-100马力等级的农用拖拉机将占据42.94%的市场。这是因为该级别拖拉机在各种农业作业中,从田间作物耕作到物料搬运,都能提供最佳的动力成本比。该级别拖拉机的优势在于其多功能性,能够胜任多种农业任务,使农民能够全年使用而非季节性使用,从而证明其较高的初始投资是值得的。 40马力以下等级的拖拉机主要供应给新兴市场的特种作物种植者、葡萄园经营者和小规模农户,在这些市场中,紧凑的尺寸和操控性比单纯的动力需求更为重要,因此该级别拖拉机仍能保持一定的市场份额。

高功率(200马力以上)拖拉机市场正以7.49%的复合年增长率增长,这主要得益于大型农场寻求与各种农具更高的兼容性以及减少每英亩运作以最大限度地提高田间作业效率。 101-200马力拖拉机市场则受到供应链限制的影响,导致Tier 4 Final发动机的供应受到影响,但精密农业的改进正在推动对支持变量施肥和自动驾驶系统的ISOBUS车型的需求。

到2025年,两轮驱动(2WD)拖拉机将占据农业拖拉机市场71.80%的份额,这主要得益于其较低的购置成本和更便捷的维护。一台典型的40-100马力两轮驱动拖拉机比四轮驱动(4WD)拖拉机便宜8000-15000美元,这在价格敏感型经济体中是一笔不小的差价。随着保护性耕作和延长湿地作物种植期,对牵引力的需求不断增长,预计四轮驱动拖拉机的需求将以每年7.62%的速度增长。

四轮驱动系统的普及反映了农业生产方式的转变,这种转变将田间作业效率和土壤保护置于设备初始成本之上。现代四轮驱动拖拉机配备了电子牵引力管理系统,能够根据打滑检测自动接合前轮驱动,从而在保持牵引性能的同时优化燃油效率。美国和欧盟土壤保护计画的监管影响正在推动四轮驱动技术的普及,这些措施透过减少土壤压实和提高湿地条件下的田间通行能力,在保持生产力水平的同时,支持永续农业实践。

区域分析

亚太地区以38.60%的市占率领先全球农用拖拉机市场,主要得益于印度的机械化进程、中国的农业现代化计画以及日本对精密农业的推广应用。印度对35马力以下拖拉机的25%至50%的购买补贴政策支撑了该地区的需求;中国则大力推广中型拖拉机,目标是到2030年实现75%的机械化率,高于2024年的52%。日本在自主系统技术领域的领先地位使其成为全球机器人设备部署的试验场。

非洲是成长最快的地区。该地区的农业拖拉机市场预计将以每年7.62%的速度成长,政府采购和优惠融资正在协助实现《综合农业发展计画2.0》(CAADP 2.0)下40%的机械化率目标。奈及利亚计划在2024年进口8,500台拖拉机(比前一年增长15%),而肯亚和加纳已获得一笔总额达4.8亿美元的多边信贷,用于资助一个联合农业机械池。

北美地区的农机替换需求已趋于成熟。在玉米带地区,大马力拖拉机的采购占据主导地位,因为平均面积达600公顷的农场需要作业范围更广、劳动生产力更高的农具。虽然美国占据了该地区的大部分市场份额,但加拿大正在投资用于酪农和温室种植的电动小型拖拉机。欧洲也紧跟其后,在第五阶段排放法规和欧洲绿色交易(到2030年将农业排放减少25%)的推动下,加速了专业应用领域从柴油拖拉机向电动拖拉机的转型。德国和法国是四轮驱动和自动驾驶平台的早期采用者,预计到2025年,两国将占欧洲出货量的42%。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 印度和巴西的补贴续期

- 中型马力拖拉机的精密农业改装蓬勃发展

- 实用型拖拉机(60马力以下)的电气化

- 美国玉米带地区替换需求不断成长

- 非洲 CAADP 2.0 下的机械化任务

- 全球粮食巨头的自动驾驶试验计画

- 市场限制

- 电动车电池组成本高成本

- 撒哈拉以南非洲银行流动性紧缩

- 动力传动系统(Tier 4 F 引擎)供应链的波动性

- 利率上升影响经销商库存资金筹措

- 监管环境

- 技术展望

- 波特五力分析

- 买方的议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 透过输出

- 不到40马力

- 40-100马力

- 101-200马力

- 超过200马力

- 按驱动类型

- 两轮驱动

- 四轮驱动

- 按引擎类型

- 柴油引擎

- 电

- 杂交种

- 按拖拉机类型

- 公用事业

- 田间作物

- 果园和葡萄园

- 自主

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 德国

- 法国

- 俄罗斯

- 英国

- 义大利

- 其他欧洲

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 中东

- 沙乌地阿拉伯

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Deere and Company

- CNH Industrial

- AGCO Corporation

- Kubota Corporation

- Mahindra and Mahindra

- CLAAS KGaA

- SDF Group

- Yanmar Holdings Co., Ltd.

- Argo Tractors SpA

- Weichai Lovol Intelligent Agricultural Technology CO., LTD

- LS Mtron Ltd

- Kioti Tractor(Daedong Corporation)

- International Tractors Limited

第七章 市场机会与未来展望

The agricultural tractors market is expected to grow from USD 65 billion in 2025 to USD 68.55 billion in 2026 and is forecast to reach USD 89.43 billion by 2031 at 5.46% CAGR over 2026-2031.

Current growth is underpinned by continuing mechanization in emerging economies, rapid precision-agriculture retrofit activity in developed regions, and early commercialization of electric and autonomous tractor platforms. Asia-Pacific sustains the strongest regional momentum, as expansive subsidy programs in India and China's farm-modernization push stimulate replacement demand, while Africa posts the fastest growth as CAADP 2.0 sets minimum mechanization targets and unlocks concessional financing. The 40-100 HP segment reflects optimal power-to-cost ratios for mid-scale farming operations, while 2-wheel drive configurations maintain dominance due to lower acquisition costs and maintenance simplicity. Utility tractors serve diverse agricultural applications from tillage to material handling. However, autonomous tractors are experiencing explosive growth as grain majors pilot driverless systems to address labor shortages and optimize field operations. Consolidation among global vendors remains moderate; yet regional brands continue to grow through focused cost-optimized product lines and locally aligned distribution. Supply chain volatility in Tier 4 F engines and rising interest rates affecting dealer floor-plan financing present near-term headwinds, yet precision agriculture retrofit demand and electrification initiatives continue driving long-term growth momentum.

Global Agricultural Tractors Market Trends and Insights

Subsidy Renewals in India and Brazil

India extended subsidized credit lines under the Kisan Credit Card scheme to fiscal 2029, allocating INR 1.68 trillion (USD 20.2 billion) for farm mechanization, with tractors capturing roughly 15% of disbursements . Brazil's Programa Nacional de Fortalecimento da Agricultura Familiar offers 3% interest financing, improving affordability for 40-100 HP models . As manual labor costs have risen 40-60% since 2022, tractors have become financially viable for holdings above 5 ha, accelerating agricultural tractor market adoption.

Electrification of Utility Tractors below 60 HP

Electric tractors under 60 HP gain traction in orchards and greenhouses where zero-tailpipe emissions reduce ventilation costs and meet local regulations. Fendt's e100 Vario delivers up to six operating hours, the European Union's Green Deal provides up to 40% purchase subsidies for electric agricultural equipment, and California's Air Resources Board mandates zero-emission standards for utility vehicles by 2030, creating regulatory tailwinds for electrification initiatives. Battery packs still cost USD 400-600 per kWh, yet the International Energy Agency projects a 40% cost decline by 2030, bringing parity within reach .

High battery pack cost for electric models

Electric tractor adoption faces significant headwinds from battery pack costs that remain 2-3 times higher than automotive applications, limiting market penetration despite growing environmental regulations. Agricultural lithium-ion packs cost USD 400-600 per kWh, roughly triple light-duty automotive levels. The total cost of ownership for electric tractors exceeds diesel equivalents by 20-40% over five-year periods, even accounting for lower operating costs and government incentives. Battery degradation in agricultural applications, where tractors operate in dusty, high-vibration conditions with irregular charging cycles, reduces effective capacity by 15-25% annually, further impacting economic viability for commercial farming operations.

Other drivers and restraints analyzed in the detailed report include:

- Rising Replacement Demand in the U.S. Corn Belt

- Precision-ag Retrofit Boom in Mid-Horsepower Fleet

- Bank liquidity crunch in Sub-Saharan credit lines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 40-100 HP segment captured 42.94% of the agricultural tractors market share in 2025, reflecting optimal power-to-cost ratios for diverse farming operations from row-crop cultivation to material handling applications. This segment benefits from versatility across multiple agricultural tasks, enabling farmers to justify higher capital investments through year-round utilization rather than seasonal deployment. The sub-40 HP category maintains its share by primarily serving specialty crops, vineyard operations, and smallholder agriculture in emerging markets where compact size and maneuverability outweigh raw power requirements.

High-horsepower segments above 200 HP demonstrate 7.49% CAGR growth, driven by large-scale farming operations seeking to maximize field efficiency through wider implement compatibility and reduced operating hours per acre.The 101-200 HP segment faces headwinds from supply chain constraints affecting Tier 4 Final engines, yet precision agriculture retrofits are driving demand for ISOBUS-compatible models that support variable-rate application and autonomous guidance systems.

Two-wheel configurations delivered a 71.80% share of the agricultural tractor market size in 2025, favored for lower acquisition cost and simpler upkeep. The typical 40-100 HP 2WD tractor is USD 8,000-15,000 cheaper than its 4WD counterpart, an important gap in price-sensitive economies. Four-wheel drive demand is projected to expand 7.62% annually as conservation tillage and wetter planting windows raise traction needs.

The shift toward 4WD systems reflects changing farming practices that prioritize field efficiency and soil conservation over initial equipment costs. Modern 4WD tractors incorporate electronic traction management systems that automatically engage front-wheel assist based on slip detection, optimizing fuel efficiency while maintaining traction advantages. Regulatory influence from soil conservation programs in the United States and European Union encourages 4WD adoption through reduced soil compaction and improved field trafficability during wet conditions, supporting sustainable farming practices while maintaining productivity levels.

The Agricultural Tractors Market Report is Segmented by Power Output (less Than 40 HP, and More), by Drive Type ( 2-Wheel Drive, and 4-Wheel Drive ), by Engine Type (Diesel and More), by Tractor Type (Utility, Row-Crop and More), and by Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Report Offers Market Size and Forecasts in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominates the global agricultural tractors market with a 38.60% share, driven by India's mechanization initiatives, China's agricultural modernization programs, and Japan's precision agriculture adoption. India anchors regional demand through 25-50% purchase subsidies on tractors below 35 HP, while China seeks 75% mechanization by 2030 versus 52% in 2024, spurring mid-range tractor uptake. Japan's technology leadership in autonomous systems positions the country as a testing ground for the global rollout of robotized equipment.

Africa is the fastest-growing region. The agricultural tractors market in Africa is projected to advance 7.62% annually, with government procurement and concessionary financing targeting 40% mechanization under CAADP 2.0. Nigeria imported 8,500 tractors in 2024, a 15% rise year on year, while Kenya and Ghana collectively secured USD 480 million in multilateral credit lines to fund cooperative machinery pools

North America exhibits mature replacement dynamics. High-horsepower purchases dominate in the Corn Belt as farms averaging 600 ha seek wider implements and labor productivity gains. The United States accounts for the majority share of regional value, while Canada invests in electric compact units for dairy and greenhouse operations. Europe follows, driven by Stage V emissions compliance and the European Green Deal target to cut agricultural emissions 25% by 2030, accelerating the diesel-to-electric transition in specialty applications. Germany and France remain early adopters of 4WD and autosteer platforms and jointly represent 42% of European shipments in 2025.

- Deere and Company

- CNH Industrial

- AGCO Corporation

- Kubota Corporation

- Mahindra and Mahindra

- CLAAS KGaA

- SDF Group

- Yanmar Holdings Co., Ltd.

- Argo Tractors S.p.A.

- Weichai Lovol Intelligent Agricultural Technology CO., LTD

- LS Mtron Ltd

- Kioti Tractor (Daedong Corporation)

- International Tractors Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Subsidy Renewals in India and Brazil

- 4.2.2 Precision-ag Retrofit Boom among Mid-Horsepower Tractors

- 4.2.3 Electrification of Utility Tractors (<60 HP)

- 4.2.4 Rising Replacement Demand in U.S. Corn Belt

- 4.2.5 Mandated Mechanization under Africa's CAADP 2.0

- 4.2.6 Autonomous Pilot Programs by Global Grain Majors

- 4.3 Market Restraints

- 4.3.1 High Battery Pack Cost for Electric Models

- 4.3.2 Bank Liquidity Crunch in Sub-Saharan Credit Lines

- 4.3.3 Supply-chain Volatility in Powertrains (Tier 4 F engines)

- 4.3.4 Rising Interest Rates Affecting Dealer Floorplan Financing

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Power Output

- 5.1.1 Less than 40 HP

- 5.1.2 40-100 HP

- 5.1.3 101-200 HP

- 5.1.4 More than 200 HP

- 5.2 By Drive Type

- 5.2.1 2-Wheel Drive

- 5.2.2 4-Wheel Drive

- 5.3 By Engine Type

- 5.3.1 Diesel

- 5.3.2 Electric

- 5.3.3 Hybrid

- 5.4 By Tractor Type

- 5.4.1 Utility

- 5.4.2 Row-Crop

- 5.4.3 Orchard and Vineyard

- 5.4.4 Autonomous

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 Russia

- 5.5.3.4 United Kingdom

- 5.5.3.5 Italy

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 Turkey

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Deere and Company

- 6.4.2 CNH Industrial

- 6.4.3 AGCO Corporation

- 6.4.4 Kubota Corporation

- 6.4.5 Mahindra and Mahindra

- 6.4.6 CLAAS KGaA

- 6.4.7 SDF Group

- 6.4.8 Yanmar Holdings Co., Ltd.

- 6.4.9 Argo Tractors S.p.A.

- 6.4.10 Weichai Lovol Intelligent Agricultural Technology CO., LTD

- 6.4.11 LS Mtron Ltd

- 6.4.12 Kioti Tractor (Daedong Corporation)

- 6.4.13 International Tractors Limited

7 Market Opportunities and Future Outlook

农业拖拉机市场:按功率范围、拖拉机类型、燃料类型、应用和最终用户划分 - 全球市场预测(2026-2032 年)

农业拖拉机市场:按功率范围、拖拉机类型、燃料类型、应用和最终用户划分 - 全球市场预测(2026-2032 年) 2026年全球小型农用拖拉机市场报告2026年全球农业拖拉机租赁市场报告电动农用拖拉机市场:2026-2032年全球市场预测(按推进方式、驱动系统、运作小时数、自主等级、功率输出、作物类型、应用、最终用户和销售管道)农业拖拉机市场:按发动机功率、产品类型、拖拉机类型、应用和销售管道,全球预测,2026-2032年

2026年全球小型农用拖拉机市场报告2026年全球农业拖拉机租赁市场报告电动农用拖拉机市场:2026-2032年全球市场预测(按推进方式、驱动系统、运作小时数、自主等级、功率输出、作物类型、应用、最终用户和销售管道)农业拖拉机市场:按发动机功率、产品类型、拖拉机类型、应用和销售管道,全球预测,2026-2032年 农业拖拉机市场规模、份额、成长及全球产业分析:按类型、应用和地区划分-2026-2034年洞察与预测

农业拖拉机市场规模、份额、成长及全球产业分析:按类型、应用和地区划分-2026-2034年洞察与预测 非洲农业拖拉机机械:市场份额分析、行业趋势与统计、成长预测(2026-2031 年)全球农业拖拉机市场规模、份额、趋势和成长分析报告(2026-2034年)2026年全球农业导航与转向系统市场报告2026年全球农业拖拉机市场报告

非洲农业拖拉机机械:市场份额分析、行业趋势与统计、成长预测(2026-2031 年)全球农业拖拉机市场规模、份额、趋势和成长分析报告(2026-2034年)2026年全球农业导航与转向系统市场报告2026年全球农业拖拉机市场报告