|

市场调查报告书

商品编码

1934783

美国校车市占率分析、产业趋势与统计、成长预测(2026-2031)United States School Bus - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

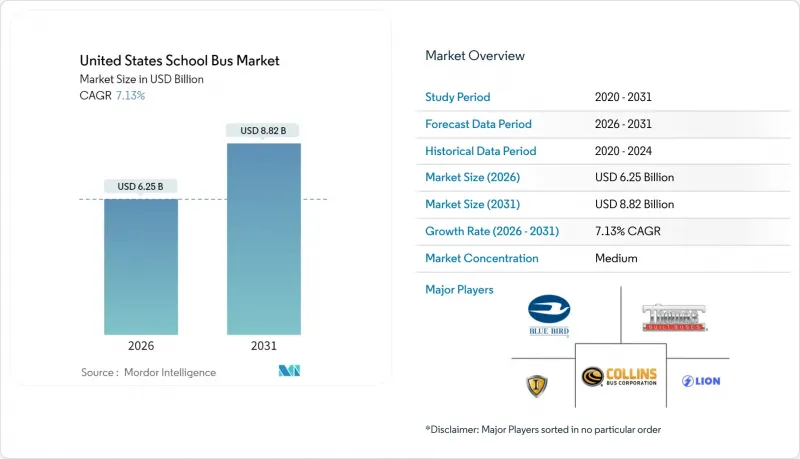

2025年美国校车市场价值58.3亿美元,预计2031年将达到88.2亿美元,高于2026年的62.5亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 7.13%。

随着科技进步,电动校车的出现凸显了保护环境和造福子孙后代的决心。预计向电池式电动车的快速转型以及创新的低氮氧化物排放解决方案将显着加速电动校车的普及。同时,美国国家公路交通安全管理局 (NHTSA) 加强的安全标准以及各州对零排放车辆采购期限的设定,正在加速先前推迟的车辆更新换代决策。业内相关人员正在努力平衡短期挑战(例如底盘短缺、技术人员培训困难以及充电基础设施不完善)与长期机会(例如V2G收入来源和基于站点的微电网,这些都能显着降低总体拥有成本)。

美国校车市场趋势与洞察

美国环保署清洁校车计画的联邦资金激增

美国环保署的清洁校车计画正在改变采购经济格局,该计画为电池电动校车提供高达80%的增量成本补贴,激励学区加快升级换代步伐,超越传统的折旧免税额週期。优先评分机制确保45%的资金流向低收入社区和美洲原住民社区,从而在历来受低税基限制的市场中形成普及丛集。预计在2026年该计画结束前,这波由补贴驱动的需求浪潮将达到高峰,缩短采购时间,并加剧生产名额的竞争。这促使原始设备製造商(OEM)和电池供应商与公共产业合作,简化充电基础设施的部署,同时扩大国内生产能力。

全国老旧的公车车队(车龄超过11年)推动了对新车的需求。

目前,公车的平均车龄已超过11年,远超过联邦交通管理局规定的12年或50万英里的使用年限。这导致大量公车积压,需要在五年内更换。延期维修成本飙升,尤其是在中西部地区,严寒的冬季会加速腐蚀。电动车型的维护成本约为每英里0.40美元,而柴油车型则为0.70美元,因此,更高的购置价格可以透过12年生命週期内更低的维护成本来抵消。拥有最老旧车队的农村地区正在评估电气化基础设施津贴,同时也正在探索使用丙烷或压缩天然气的过渡方案。原始设备製造商(OEM)正在推出模组化电动底盘,这些底盘可以重复利用现有的C型布局,从而缩短当地维修人员的学习曲线。这些车辆的到期日和补助金计画的推出,都支撑了美国校车市场强劲的成长前景。

农村地区充电基础设施不足

农村学区公共充电桩密度低——比都市区低五到十倍——这使得长途路线规划变得复杂。伊利诺州的威廉斯菲尔德学区透过建造校内微电网克服了这项挑战,目前该微电网能够满足其94%的能源需求。然而,大多数农村学区缺乏技术人员和电力公司的合作,无法复製这种模式。 《基础建设投资与就业法案》拨款12.5亿美元用于农村电动车基础建设。然而,由于计划前置作业时间超过了即时的升级週期,资金到位存在时间上的偏差。在3级充电桩普及之前,美国校车市场的电气化进程预计将会放缓,因为柴油和丙烷仍将是重要的替代能源。

细分市场分析

C型(传统型)校车是美国校车市场的核心细分市场,预计到2025年将占美国校车市场78.05%的份额。在学区优先考虑兼顾出行便利性和座位容量的推动下,预计到2031年,C型校车将维持8.05%的复合年增长率。随着升级週期与纯电动校车改装奖励政策的实施期相吻合,美国此类校车的市场规模预计将稳定扩大。汽车製造商正在C型校车平台上整合最新的驾驶辅助系统,同时保持维修人员熟悉的车架尺寸。升级套件包括电子稳定控制系统和360度全景影像系统,这些系统简化了驾驶人培训并降低了保险费用。

同时,90人座D型公车的现代化改造也在进行中,以适应综合线路的需求。托马斯·布伊特公司(Thomas Built)的Saf-T-Liner EFX2于2025年3月发布,其车身结构经过加强,可有效防止侧翻,并配备了车道偏离预警系统,征兆公交行业正朝着公共交通安全标准转型。随着各区域整合公车场站并延长线路,预计D型公车的需求将超过历史平均水平,但产能限制可能会在短期内导致交货延迟。小型A型和B型公车则服务于特殊需求人口的出行和狭窄的都市区线路。虽然就销量而言,A型和B型公车仍属于小众市场,但个人化教育计画的普及正在推动其成长,尤其是在清晨接送学生的高峰时段,这进一步刺激了对更安静的电动车的需求。

截至2025年,内燃机将占美国校车市场88.40%的份额,但随着联邦政府拨款加速推广纯电动校车,预计这一份额将会下降。美国校车市场规模预计将快速成长,到2031年复合年增长率将达到37.09%。在冬季耐久性和燃料供应仍然是首要考虑因素的偏远地区,柴油车仍然占据主导地位。然而,随着环保法规日益严格,汽车製造商正在推出低氮氧化物排放引擎和怠速降低系统,以维持柴油车的市场竞争力。

电动巴士发展势头强劲,尤其是在那些实施排放排放采购政策和电力需量反应奖励的州。混合动力传动系统虽然占据着小规模但具有战略意义的细分市场,为学区提供了一种过渡方案,既能节省20-30%的燃料,又能缓解里程焦虑。丙烷和压缩天然气(CNG)车型则有助于在臭氧超标地区达到标准,这些地区的低采购价格和现有的燃料供应基础设施正在推动其普及。这种多样化的动力系统组合解释了为什么美国校车市场在不断发展的同时日益成熟。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 美国环保署清洁校车计画的联邦资金激增

- 老旧(超过11年)国家铁路车辆的更换需求增加

- 严格的汽车安全标准加速了车辆更新换代。

- 未达标县对低氮氧化物「其他燃料」的需求

- 学区可以从车辆到电网(V2G)中获得收入

- 结合车厂微电网和太阳能发电,降低电力总拥有成本(TCO)

- 市场限制

- 农村地区充电基础设施不足

- 儘管有奖励,电动公车的初始成本仍然很高。

- 高压维修工程师短缺

- 中型底盘供应瓶颈

- 价值/供应链分析

- 监理情势与资金筹措环境

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模及成长预测(金额:美元 / 数量:单位)

- 依设计类型

- A 型(剖面图)

- B型

- C型(常规)

- D 型(交通工具风格)

- 依动力传动系统类型

- 内燃机(IC引擎)

- 混合动力汽车和电动车

- 依所有权类型

- 辖区车辆

- 承包商车队

- 按座位数

- 不到30个座位

- 30至60个座位

- 60个或更多座位

第六章 竞争情势

- 市场集中度

- 策略倡议和联盟

- 市占率分析

- 公司简介

- Blue Bird Corporation

- Daimler Truck North America LLC(Thomas Built)

- Navistar Inc.(IC Bus)

- Collins Bus Corporation

- Lion Electric Company

- GreenPower Motor Company Inc.

- Micro Bird Inc.(Girardin)

- BYD Motors USA

- Van-Con, Inc.

- Starcraft Bus

- Trans Tech Bus

第七章 市场机会与未来展望

The United States school bus market was valued at USD 5.83 billion in 2025 and estimated to grow from USD 6.25 billion in 2026 to reach USD 8.82 billion by 2031, at a CAGR of 7.13% during the forecast period (2026-2031).

With technological advancements, the emergence of electric school buses on roads underscores a dedication to environmental care and the future of younger generations. The swift transition towards battery-electric vehicles and innovative low-NOx solutions is poised to boost the adoption of electric school buses significantly. Simultaneously, stricter NHTSA safety mandates and state-level zero-emission purchase deadlines are advancing replacement decisions that might otherwise have been deferred. Industry participants are therefore balancing near-term chassis shortages, technician training gaps, and uneven charging infrastructure with longer-term opportunities such as vehicle-to-grid revenue streams and depot-based micro-grids that materially reduce total cost of ownership.

United States School Bus Market Trends and Insights

Federal Funding Surge via EPA Clean School Bus Program

The EPA Clean School Bus Program has altered procurement economics by offsetting up to 80% of incremental costs for battery-electric models, prompting districts to accelerate replacement schedules beyond normal depreciation cycles. Priority scoring directs 45% of funds to low-income and tribal communities, creating adoption clusters in markets that have historically faced limitations due to low tax bases. This wave of subsidized demand is expected to peak before the program sunsets in 2026, compressing procurement windows and intensifying competition for production slots. OEMs and battery suppliers are therefore expanding domestic capacity while forging utility partnerships to streamline charging deployments.

Aging National Fleet (Above 11 yrs) Pushing Replacement Demand

Average bus age now exceeds 11 years, well beyond the Federal Transit Administration's 12-year or 500,000-mile guidance, creating a backlog of sigiifcnat amount of buses units that must be cycled out within five years. Deferred maintenance costs are escalating, particularly in the Midwest, where harsh winters accelerate corrosion. Electric models cost roughly USD 0.40 per mile to maintain versus USD 0.70 for diesel, allowing life-cycle savings to offset higher purchase prices over 12 years . Rural systems with the oldest fleets are exploring propane or CNG bridges while evaluating grants for electrification infrastructure. OEMs are responding with modular electrified chassis that reuse existing Type C layouts, shortening the learning curve for district mechanics. This alignment of end-of-life timing and incentive availability underpins the robust growth outlook for the United States school bus market.

Sparse Rural Charging Infrastructure

Rural districts face a five-to-ten-fold deficit in public charging density compared with urban areas, complicating route planning for long daily runs. While Illinois' Williamsfield Schools overcame the hurdle via a campus microgrid that now meets 94% of energy needs, most rural systems lack the technical staff or utility partnerships to replicate the model. The Infrastructure Investment and Jobs Act allocated USD 1.25 billion for rural EV infrastructure. However, project lead times exceed immediate replacement cycles, resulting in timing misalignments. Until Level 3 chargers become more widely available, diesel and propane will remain important fallback options, tempering overall electrification momentum in the United States school bus market.

Other drivers and restraints analyzed in the detailed report include:

- Stringent On-Board Safety Mandates Accelerating Fleet Renewal

- Low-NOx "Other Fuels" Demand in Non-Attainment Counties

- High Upfront Cost Of E-Buses Despite Incentives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Type C (conventional) buses anchored the United States school bus market in 2025 with 78.05% share, and the segment is expected to deliver an 8.05% CAGR through 2031 as districts favor its blend of maneuverability and seating capacity. The United States school bus market size for this design is therefore poised to rise steadily as replacement cycles align with incentive windows that subsidize battery-electric retrofits. OEMs are fortifying Type C platforms with updated driver-assistance suites, while maintaining frame dimensions familiar to maintenance staff. Upgrade packages include electronic stability control and 360-degree camera systems that simplify driver training and reduce insurance premiums.

A parallel modernization wave is unfolding in Type D transit-style configurations, which cater to consolidated routes requiring 90-passenger capacity. Thomas Built's Saf-T-Liner EFX2 launch in March 2025 added rollover-enhanced body structures and lane-departure warnings, signaling an industry shift toward mass-transit safety norms. As districts consolidate depots and extend route lengths, Type D demand is projected to outpace historical averages, though limited production slots may constrain near-term deliveries. At the smaller end, Type A and B buses serve special-needs transport and tight urban corridors. While they remain niche in unit volume, a surge in individualized education programs is boosting growth prospects, especially for electric variants that can operate quietly during early-morning pickup windows.

Internal-combustion engines captured 88.40% of the United States School Bus Market size in 2025, yet the segment's share is forecast to shrink as battery-electric deployments accelerate under federal funding schemes. The United States school bus market size for electric models is set to climb rapidly, given their 37.09% CAGR through 2031. Diesel retains an edge in remote geographies where winter resilience and fuel availability remain paramount. Nevertheless, OEMs are integrating lower-NOx engines and idle-reduction systems to extend diesel relevance amid environmental scrutiny.

Electric momentum is particularly strong in states with zero-emission purchase mandates and utility demand-response incentives. Hybrid powertrains occupy a small but strategic niche, offering districts a transitional pathway that mitigates range anxiety while providing fuel savings of 20-30%. Propane and CNG models underpin compliance in ozone-non-attainment counties, their adoption bolstered by lower acquisition prices and familiar fueling infrastructure. Collectively, this diverse propulsion mix underlines why the United States school bus market remains simultaneously mature and transformative.

The United States School Bus Market Report is Segmented by Design Type (Type A (Cut-Away), Type B, and More), Powertrain Type (Internal Combustion Engine, Hybrid, and Electric), Ownership Model (District-Owned Fleets and Contractor-Owned Fleets), and Seating Capacity (Less Than 30 Seats, 30-60 Seats, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- Blue Bird Corporation

- Daimler Truck North America LLC (Thomas Built)

- Navistar Inc. (IC Bus)

- Collins Bus Corporation

- Lion Electric Company

- GreenPower Motor Company Inc.

- Micro Bird Inc. (Girardin)

- BYD Motors USA

- Van-Con, Inc.

- Starcraft Bus

- Trans Tech Bus

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Federal Funding Surge via EPA Clean School Bus Program

- 4.2.2 Aging National Fleet (Above 11 yrs) Pushing Replacement Demand

- 4.2.3 Stringent On-board Safety Mandates Accelerating Fleet Renewal

- 4.2.4 Low-NOx "Other Fuels" Demand in Non-attainment Counties

- 4.2.5 Vehicle-to-grid (V2G) Revenue Potential for School Districts

- 4.2.6 Depot Micro-grid and Solar Pairing Lowers Electric TCO

- 4.3 Market Restraints

- 4.3.1 Sparse Rural Charging Infrastructure

- 4.3.2 High Upfront Cost Of E-Buses Despite Incentives

- 4.3.3 Scarcity Of High-Voltage Maintenance Technicians

- 4.3.4 Medium-Duty Chassis Supply Bottlenecks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory & Funding Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD and Volume in Units)

- 5.1 By Design Type

- 5.1.1 Type A (Cut-away)

- 5.1.2 Type B

- 5.1.3 Type C (Conventional)

- 5.1.4 Type D (Transit-Style)

- 5.2 By Powertrain Type

- 5.2.1 Internal Combustion Engine (IC Engine)

- 5.2.2 Hybrid and Electric

- 5.3 By Ownership Model

- 5.3.1 District-Owned Fleets

- 5.3.2 Contractor-Owned Fleets

- 5.4 By Seating Capacity

- 5.4.1 Less than 30 Seats

- 5.4.2 30-60 Seats

- 5.4.3 Above 60 Seats

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves & Partnerships

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Blue Bird Corporation

- 6.4.2 Daimler Truck North America LLC (Thomas Built)

- 6.4.3 Navistar Inc. (IC Bus)

- 6.4.4 Collins Bus Corporation

- 6.4.5 Lion Electric Company

- 6.4.6 GreenPower Motor Company Inc.

- 6.4.7 Micro Bird Inc. (Girardin)

- 6.4.8 BYD Motors USA

- 6.4.9 Van-Con, Inc.

- 6.4.10 Starcraft Bus

- 6.4.11 Trans Tech Bus

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment