|

市场调查报告书

商品编码

1934819

德国容器玻璃:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Germany Container Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

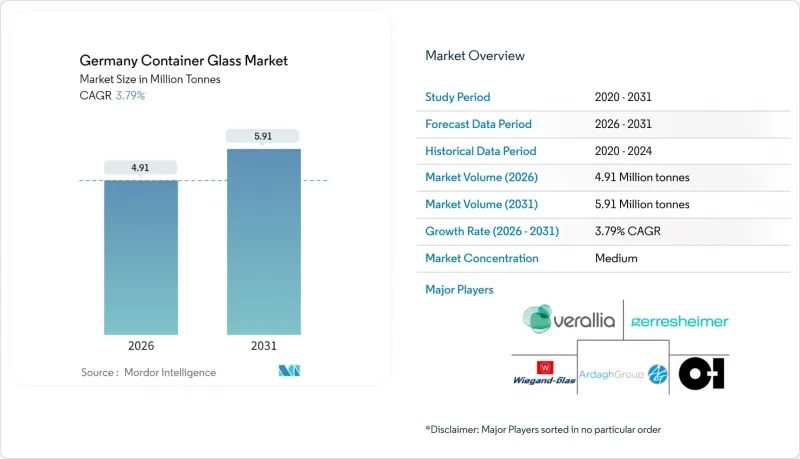

德国容器玻璃市场预计将从 2025 年的 473 万吨成长到 2026 年的 491 万吨,到 2031 年达到 591 万吨,2026 年至 2031 年的复合年增长率为 3.79%。

儘管能源价格上涨和啤酒销售量多年下滑将对短期成长构成挑战,但轻质玻璃创新、混合熔炉的普及以及政府的循环经济策略将支撑市场的中期成长。高端饮料生产商正在定制能够提升品牌形象并减少碳足迹的瓶子,而製药灌装商则正在向符合欧盟GMP附录1标准的无菌即用型容器转型。国家设定的25%再生材料含量和80%玻璃回收率目标,使玻璃容器比塑胶容器更具优势。塑胶生产商目前面临最低再生材料含量基准值(ihk.de)。领先的製造商正采取双管齐下的策略来应对,即精简产能并投资低碳技术,预计这将提高生产效率并降低每吨排放。在德国玻璃容器市场中,那些能够获得可再生能源和混合熔融技术的参与企业,预计将占据高价值医药、化妆品和高端酒类应用领域不断增长的需求的大部分份额。

德国容器玻璃市场趋势与展望

德国对可再生包装的需求不断增长

2025年1月通过的《国家循环经济战略》规定,战略性原料需求的25%必须回收,并在2030年至2040年间将人均城市垃圾减少10%至20%。这个框架使得玻璃容器凭藉其无限的可回收性和稳定的质量,展现出优于聚合物替代品的优势。目前,约30万个公共玻璃回收点已实现超过80%的玻璃回收率,为生产商提供稳定的玻璃屑供应,并使每吨熔融玻璃的熔炉能源需求降低高达30%。该策略还包括一个数位产品护照,用于记录回收成分,从而为高玻璃屑含量的瓶子提供差异化竞争优势。对于希望遵守即将推出的一次性塑胶回收成分规定的品牌而言,玻璃提供了一条实现包装永续性目标的清晰路径,从而推动了德国玻璃容器市场的需求成长。

製药业的蓬勃发展推动了对高品质玻璃的需求。

肖特製药预计2024年销售额将达到9.57亿欧元(10.8亿美元),以外汇汇率计算成长12%。高价值注射器和即用型(RTU)容器目前占销售额的55%。生物製药生产集中在德国,以及新型GLP-1疗法的推出,推动了对低碱、低颗粒玻璃容器的需求,这些容器能够承受冷冻干燥并保持药物稳定性。由肖特製药、格雷斯海默和斯特瓦纳托集团组成的「RTU联盟」正在通过RTU规格的标准化,提高药品填充线的效率并降低污染风险,从而进一步扩大高品质硼硅酸和铝硅酸盐玻璃的潜在市场。预计这些趋势将推动对能够获得USP(660)和欧盟药典I型认证,并提供快速换型和无菌供给能力的製造商的需求成长。

能源成本上涨推高了玻璃生产成本。

从2024年到2025年,工业用电价格将维持在每兆瓦时40欧元(43.2美元)左右,约为危机前水准的四倍。同时,儘管政府提供了临时补贴,但天然气价格的急剧上涨仍然推高了熔炼成本。由于1600摄氏度的熔炼过程占熔炉营业成本的70-75%,不断上涨的电价正在侵蚀盈利,并加剧投资预算的压力。正如阿达格公司的NextGen系列产品所展示的那样,混合熔炉可以将二氧化碳排放减少高达64%,但它们仍然依赖价格具有竞争力的再生能源。在透过电网脱碳和降低工业用电价格使投入成本稳定下来之前,德国容器玻璃市场的产能扩张将落后于潜在需求。

细分市场分析

到2025年,饮料业仍将占据德国包装玻璃市场51.60%的份额(相当于2,440千吨),这反映了啤酒和葡萄酒强劲的灌装消费文化。然而,2025年1月至5月,啤酒出货量下降6.8%至3,410万百升,为啤酒产业重组以来的最低水准。这导致瓶装需求下降,并促使啤酒厂进行精简。与标准啤酒瓶相关的德国玻璃容器市场预计到2030年将以较低的个位数复合年增长率萎缩。同时,烈酒、精酿啤酒和非酒精麦芽饮料透过采用客製化的轻质玻璃来部分抵消这一下滑,这些玻璃价格较高。服务这些细分市场的製造商可以透过提供快速的模具週转时间和低二氧化碳玻璃认证来维持其利润率。

到2025年,医药应用将占德国玻璃容器市场规模的约10.40%,预计将以超过5.05%的复合年增长率增长,超过饮料行业,这主要得益于生物製药、GLP-1注射剂和mRNA疫苗需求的增长。欧盟附件一的严格规定推动了管瓶和注射器(RTU)的无菌性和生产线效率,从而推高了平均售价并降低了玻璃屑等级的要求。化妆品和个人护理行业虽然规模小规模(仅占8.10%),但预计将以5.12%的复合年增长率成为增长最快的行业,这主要得益于高端护肤品牌从塑胶瓶转向玻璃瓶,以提供奢华的开启体验。食品瓶保持稳定的个位数市场份额,这主要得益于消费者认为玻璃材质惰性且可重复使用。然而,其成长率与整体食品市场大致持平。

德国容器玻璃市场报告按最终用途(饮料[酒精饮料(啤酒、葡萄酒、烈酒和其他酒精饮料)]、非酒精饮料[果汁、碳酸饮料、乳製品饮料和其他非酒精饮料]、食品、化妆品和个人护理用品、药品和香水]和颜色(绿色、琥珀色、水白色等)分析市场。市场预测以吨为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 德国对可再生包装的需求不断增长

- 医药产业的蓬勃发展推动了高品质玻璃包装的需求。

- 高端饮品带动了对订製瓶装饮料的需求。

- 循环经济政策强化了玻璃回收系统

- 永续性目标推动轻质玻璃领域的创新

- 产业整合重组货柜玻璃产能

- 市场限制

- 能源成本上涨推高了玻璃生产成本。

- 来自PET和进口玻璃包装的竞争

- 监理合规对中小型生产者构成障碍

- 工厂倒闭导致本地供应减少

- PESTEL 分析

- 产业价值链分析

- 德国容器玻璃熔炉的产能和位置

- 工厂选址及投产

- 生产能力

- 炉型

- 所产玻璃的颜色

- 货柜玻璃进出口资料-涵盖主要进出口目的地

- 进口量及进口额(2021-2024 年)

- 出口量和出口额(2021-2024 年)

- 波特五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 原料分析

- 玻璃包装的回收趋势

- 玻璃包装需求与供给分析

第五章 市场规模与成长预测

- 最终用户

- 饮料

- 酒精饮料

- 啤酒

- 葡萄酒

- 烈酒

- 其他酒精饮料(苹果酒和其他发酵饮料)

- 非酒精性

- 果汁

- 碳酸软性饮料(CSD)

- 乳製品饮料

- 其他非酒精饮料

- 酒精饮料

- 食品(果酱、果冻、橘子酱、蜂蜜、香肠和调味品、食用油、腌菜)

- 化妆品和个人护理

- 药品(不含管瓶和安瓿瓶)

- 香水

- 饮料

- 按颜色

- 绿色的

- 琥珀色

- 无色透明

- 其他颜色

第六章 竞争情势

- 市场集中度

- 策略趋势与发展

- 公司市占率分析(基于当前产能)

- 公司简介

- Ardagh Glass GmbH

- Systempack Manufaktur GmbH

- HEINZ-GLAS GmbH & Co. KGaA

- Schott AG

- Saint-Gobain Oberland AG(Verallia Deutschland AG)

- Rixius AG

- OI Germany GmbH & Co KG

- Gerresheimer AG

- Wiegand-Glas GmbH

- Noelle+von Campe GmbH & Co. KG

- SGD Pharma Germany GmbH

- Glashutte Freital GmbH

- KP Glas GmbH & Co. KG

- Verallia Deutschland AG

- Glashutte Eisch GmbH

第七章 市场机会与未来展望

The Germany Container Glass Market is expected to grow from 4.73 million tonnes in 2025 to 4.91 million tonnes in 2026 and is forecast to reach 5.91 million tonnes by 2031 at 3.79% CAGR over 2026-2031.

The market's medium-term momentum is underpinned by lightweight glass innovation, hybrid furnace deployment, and the government's circular economy strategy, despite the impact of energy prices and a multi-year decline in beer volumes on near-term growth. Premium beverage owners are specifying customized bottles that reinforce brand identity while reducing their carbon footprint, and pharmaceutical fillers are shifting toward sterile, ready-to-use containers that meet EU Good Manufacturing Practice Annex 1 guidelines. National targets for 25% recycled raw material use and 80% glass collection rates position container glass favorably against plastic, whose producers now face minimum recycled-content thresholds ihk.de. Scale manufacturers are responding with capacity rationalization and investments in low-carbon technology, a dual strategy that is expected to boost productivity and reduce per-ton emissions. Germany container glass market participants able to secure renewable power and deploy hybrid melting technology are forecast to capture the bulk of incremental demand from high-value pharmaceutical, cosmetics, and premium spirits applications.

Germany Container Glass Market Trends and Insights

Increasing Demand for Recyclable Packaging in Germany

The National Circular Economy Strategy, adopted in January 2025, mandates that 25% of strategic raw material demand be met through recycling and that per capita municipal waste decline by 10-20% by 2030-2040. This framework elevates container glass, whose infinite recyclability and stable quality outperform polymer substitutes. Roughly 300,000 public glass-collection points already deliver glass return rates above 80%, providing producers with a dependable cullet stream and reducing furnace energy demand by up to 30% per ton of glass melted. Digital product passports planned under the strategy will document the recycled content, creating competitive differentiation for bottles containing high levels of cullet. Brands seeking to comply with forthcoming single-use plastic recycled-content mandates find glass to be a straightforward path to achieving packaging sustainability targets, thereby bolstering demand for Germany's container glass market.

Growing Pharmaceutical Sector Accelerates High-Quality Glass Demand

SCHOTT Pharma recorded EUR 957 million (USD 1.08 billion) in revenue for 2024, representing a 12% constant-currency increase. High-value syringes and ready-to-use (RTU) containers now account for 55% of turnover. Germany's concentration of biologics production and the introduction of new GLP-1 therapies are driving demand for low-alkali, low-particle glass formats that can withstand lyophilization and maintain drug stability. The "Alliance for RTU" formed by SCHOTT Pharma, Gerresheimer, and Stevanato Group is standardizing RTU specifications to streamline pharma filling lines and reduce contamination risk, further expanding the addressable market for premium borosilicate and aluminosilicate glass. These trends channel incremental volume to producers that can certify USP (660) and EU Pharmacopoeia Type I compliance while offering rapid changeover and sterile supply capabilities.

Rising Energy Costs Elevate Glass Production Expenses

Industrial electricity hovered near EUR 40 (USD 43.2) per MWh in 2024-2025, roughly four times pre-crisis levels, while natural-gas price spikes raised total melt costs despite temporary government subsidies. Because melting at 1,600 °C accounts for 70-75% of furnace operating cost, elevated power prices erode profitability and compress investment budgets. Hybrid furnaces can reduce CO2 by up to 64%, as demonstrated by Ardagh's NextGen line, yet still rely on competitively priced renewable electricity. Until grid decarbonization and industrial power-price relief stabilize input costs, Germany's container glass market capacity growth will lag potential demand.

Other drivers and restraints analyzed in the detailed report include:

- Premium Beverages Drive Customized Bottle Requirements

- Circular Economy Policies Strengthen Glass Recycling Systems

- Competition from PET and Imported Glass Packaging

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Beverages retained 51.60% of the German container glass market share in 2025, equivalent to 2.44 thousand kilotons, reflecting the entrenched traditions of refillable beer and wine. However, from January to May 2025, beer shipments fell 6.8% to 34.1 million hectoliters, marking the lowest post-reunification level, which trimmed bottle demand and prompted brewery rationalization. Germany's container glass market size linked to standard beer bottles is projected to contract at a low single-digit CAGR through 2030. Spirits, craft, and alcohol-free malt drinks partly offset this decline by adopting bespoke lightweight glass that commands premium shelf prices. Producers serving these niches can defend margins by offering rapid mold turnaround and low-CO2 glass certificates.

Pharmaceutical applications accounted for an estimated 10.40% of Germany's container glass market size in 2025, yet are forecast to outpace beverages, expanding at a 5.05% or more CAGR, thanks to the growing demand for biologics, GLP-1 injectables, and mRNA vaccines. Stringent EU Annex 1 rules promote RTU vials and syringes that deliver sterility assurance and line efficiency, thereby lifting average selling prices and reducing the grades of cullet required. Cosmetics and personal care hold only 8.10% volume but post the fastest 5.12% CAGR as premium skin-care brands switch from plastic to glass for a luxury unboxing experience. Food jars maintain a resilient mid-single-digit share, benefiting from consumer perception of glass as inert and reusable, although growth mirrors that of the broader grocery market.

The Germany Container Glass Market Report is Segmented by End-User (Beverages [Alcoholic (Beer, Wine, Spirits, and Other Alcoholic Beverages), Non-Alcoholic (Juices, Carbonated Drinks, Dairy Product Based Drinks, and Other Non-Alcoholic Beverages]), Food, Cosmetics and Personal Care, Pharmaceuticals, and Perfumery), Color (Green, Amber, Flint, and More). The Market Forecasts are Provided in Terms of Volume (Tonnes).

List of Companies Covered in this Report:

- Ardagh Glass GmbH

- Systempack Manufaktur GmbH

- HEINZ-GLAS GmbH & Co. KGaA

- Schott AG

- Saint-Gobain Oberland AG (Verallia Deutschland AG)

- Rixius AG

- O-I Germany GmbH & Co KG

- Gerresheimer AG

- Wiegand-Glas GmbH

- Noelle + von Campe GmbH & Co. KG

- SGD Pharma Germany GmbH

- Glashutte Freital GmbH

- KP Glas GmbH & Co. KG

- Verallia Deutschland AG

- Glashutte Eisch GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Recyclable Packaging in Germany

- 4.2.2 Growing Pharma Sector Boosts High-Quality Glass Packaging

- 4.2.3 Premium Beverages Drive Customized Bottle Requirements

- 4.2.4 Circular Economy Policies Strengthen Glass Recycling Systems

- 4.2.5 Sustainability Targets Accelerate Lightweight Glass Innovation

- 4.2.6 Industry Consolidation Reshapes Container Glass Capacity

- 4.3 Market Restraints

- 4.3.1 Rising Energy Costs Elevate Glass Production Expenses

- 4.3.2 Competition from PET and Imported Glass Packaging

- 4.3.3 Regulatory Compliance Raises Barriers for Small Producers

- 4.3.4 Plant Closures Reduce Local Supply Availability

- 4.4 PESTEL Analysis

- 4.5 Industry Value Chain Analysis

- 4.6 Container Glass Furnace Capacity and Locations in Germany

- 4.6.1 Plant Locations and Year of Commencement

- 4.6.2 Production Capacities

- 4.6.3 Types of Furnaces

- 4.6.4 Color of Glass Produced

- 4.7 Export-Import Data of Container Glass - Covering Key Import and Export Destinations

- 4.7.1 Import Volume and Value, 2021-2024

- 4.7.2 Export Volume and Value, 2021-2024

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

- 4.9 Raw Material Analysis

- 4.10 Recycling Trends for Glass Packaging

- 4.11 Demand vs Supply Analysis for Glass Packaging

5 MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1 By End-user

- 5.1.1 Beverages

- 5.1.1.1 Alcoholic

- 5.1.1.1.1 Beer

- 5.1.1.1.2 Wine

- 5.1.1.1.3 Spirits

- 5.1.1.1.4 Other Alcoholic Beverages (Cider and Other Fermented Drinks)

- 5.1.1.2 Non-Alcoholic

- 5.1.1.2.1 Juices

- 5.1.1.2.2 Carbonated Drinks (CSDs)

- 5.1.1.2.3 Dairy Product Based Drinks

- 5.1.1.2.4 Other Non-Alcoholic Beverages

- 5.1.1.1 Alcoholic

- 5.1.2 Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles)

- 5.1.3 Cosmetics and Personal Care

- 5.1.4 Pharmaceuticals (excluding Vials and Ampoules)

- 5.1.5 Perfumery

- 5.1.1 Beverages

- 5.2 By Color

- 5.2.1 Green

- 5.2.2 Amber

- 5.2.3 Flint

- 5.2.4 Other Colors

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Developments

- 6.3 Company Market Share Analysis, (Based on Latest Production Capacity)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Ardagh Glass GmbH

- 6.4.2 Systempack Manufaktur GmbH

- 6.4.3 HEINZ-GLAS GmbH & Co. KGaA

- 6.4.4 Schott AG

- 6.4.5 Saint-Gobain Oberland AG (Verallia Deutschland AG)

- 6.4.6 Rixius AG

- 6.4.7 O-I Germany GmbH & Co KG

- 6.4.8 Gerresheimer AG

- 6.4.9 Wiegand-Glas GmbH

- 6.4.10 Noelle + von Campe GmbH & Co. KG

- 6.4.11 SGD Pharma Germany GmbH

- 6.4.12 Glashutte Freital GmbH

- 6.4.13 KP Glas GmbH & Co. KG

- 6.4.14 Verallia Deutschland AG

- 6.4.15 Glashutte Eisch GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

玻璃器皿容器市场:2026-2032年全球市场预测(依产品类型、材料、製造流程、容量范围、容器形状和最终用途划分)玻璃瓶市场:依材质、颜色、容量、应用及通路划分-2026-2032年全球市场预测

玻璃器皿容器市场:2026-2032年全球市场预测(依产品类型、材料、製造流程、容量范围、容器形状和最终用途划分)玻璃瓶市场:依材质、颜色、容量、应用及通路划分-2026-2032年全球市场预测 酒精饮料瓶市场规模、份额和成长分析:按形状、容量、材质、应用和地区划分-2026-2033年产业预测

酒精饮料瓶市场规模、份额和成长分析:按形状、容量、材质、应用和地区划分-2026-2033年产业预测 全球保温瓶市场规模、份额、成长率、按类型和应用分類的全球产业分析、区域趋势以及 2026-2034 年预测。

全球保温瓶市场规模、份额、成长率、按类型和应用分類的全球产业分析、区域趋势以及 2026-2034 年预测。 越南容器玻璃:市场占有率分析、产业趋势与统计、成长预测(2026-2031)2026-2034年全球容器玻璃市场规模、份额、趋势和成长分析报告

越南容器玻璃:市场占有率分析、产业趋势与统计、成长预测(2026-2031)2026-2034年全球容器玻璃市场规模、份额、趋势和成长分析报告 日本玻璃容器市场规模、份额、趋势和预测:按产品、最终用途行业和地区划分,2026-2034年

日本玻璃容器市场规模、份额、趋势和预测:按产品、最终用途行业和地区划分,2026-2034年 2026年全球容器玻璃市场报告2026年全球运动水壶市场报告

2026年全球容器玻璃市场报告2026年全球运动水壶市场报告 容器玻璃市场 - 全球产业规模、份额、趋势、机会及预测(按玻璃类型、容器类型、成型方法、终端用户产业、地区和竞争格局划分,2021-2031年)

容器玻璃市场 - 全球产业规模、份额、趋势、机会及预测(按玻璃类型、容器类型、成型方法、终端用户产业、地区和竞争格局划分,2021-2031年)