|

市场调查报告书

商品编码

1934862

汽车半导体记忆体:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Semiconductor Memory For Automotive - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

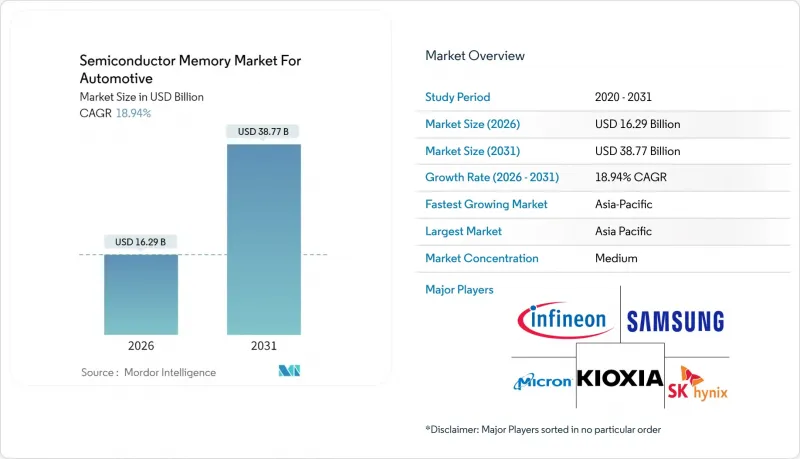

预计汽车半导体记忆体市场将从 2025 年的 137 亿美元成长到 2026 年的 162.9 亿美元,到 2031 年将达到 387.7 亿美元,2026 年至 2031 年的复合年增长率为 18.94%。

这种快速成长是由向软体定义汽车的转变所驱动的,软体定义汽车将数十种电子功能整合到一个集中式运算区域,显着提高了每辆车的记忆体密度和频宽需求。中国、美国和欧盟支持L2+以上等级驾驶辅助系统的监管倡议,正在加速对符合功能安全标准的千兆级工作记忆体的需求。同时,成本优化的3D NAND和即将推出的MRAM选项正在扩大可寻址的应用范围,使汽车製造商能够更有效地平衡性能和组件成本。美国和欧洲供应链本地化的不断推进也促使筹资策略,这提高了对快闪记忆体容量的需求,并为下一代模组建立了持久的更换週期。

汽车半导体记忆体市场趋势与展望

软体定义汽车的兴起

汽车製造商正将车辆转型为行动资料中心,这依赖持续的软体更新和功能部署。特斯拉的硬体4.0透过整合多个LPDDR5堆迭,即时处理12个相机影像和雷达输入,显着提升了记忆体密度。集中式设计将100多个ECU网路整合到几个高效能网域控制器中,将车载DRAM容量从兆位元组扩展到数GB。高阶车型已配备总合内存,预计主流车型到2027年也将达到类似容量。这种升级路径,加上更长的软体维护週期,确保了对高频宽AEC-Q100 1级模组的持续需求。

集中式/分区式EE架构

BMW即将推出的下一代iDrive系统采用分区设计,而非为每个子系统分配独立模组,从而实现了更有效率的记忆体资源分配。这种整合方式消除了冗余,并将组件数量减少了高达30%。然而,每个模组都必须提供更高的吞吐量并承受更大的热负荷。因此,资讯娱乐和ADAS领域正朝着64位元DRAM介面和接近6 Gb/s的更快存取速度发展。一级供应商正透过将记忆体和处理器整合到高密度基板上来应对这一趋势,这一趋势有利于拥有10奈米以下先进技术的供应商。虽然这种架构最初应用于高阶车型,但预计将在四年内渗透到大众市场。

供应链波动

2024年台湾地震暴露了地理位置集中的晶圆厂的脆弱性,扰乱了控制器生产,并将一级记忆体的前置作业时间延长了20週。汽车晶圆需求量占比不到10%,因此在供不应求时,供应商往往会降低汽车晶圆的优先顺序。结果,原始设备製造商(OEM)在韩国和美国之间采取双重采购策略,由于认证週期延长,预计这种做法至少会持续到2026年。出口法规的差异和地缘政治的不确定性可能会使近期经济成长下降100-150个基点。

细分市场分析

工作记忆体将继续保持主导地位,到2025年将占据半导体记忆体市场38.72%的份额,这主要得益于高级驾驶辅助系统(ADAS)和资讯娱乐系统对即时处理的高负载需求。高阶电动车(EV)将配备高达32GB的LPDDR5记忆体用于集中式运算丛集,而预计到2027年,16GB记忆体将成为量产车型的主流配置。虽然韧体容量的代码储存已稳定在8-16GB,但数据储存正以20.02%的复合年增长率快速增长,因为越来越多的车辆收集Terabyte感测器数据用于边缘分析。半导体记忆体市场规模与资料储存密切相关,这将推动对高容量3D NAND元件的长期需求。

工作记忆体领域的发展因分区架构的出现而进一步推动,这些架构实现了安全、驾驶座和动力传动系统系统等领域共用记忆体池的标准化。这种整合要求更高的单模组性能,并促进了宽I/O介面和内建ECC引擎的应用。随着OEM厂商寻求简化认证流程,提供DRAM-NAND双用途组合的供应商可望抓住市场份额机会。正在评估中的HBM-Lite概念如果能够解决散热难题,预计从2028年起投入使用,并可能在半导体记忆体市场开闢新的收入来源。

到2025年,DRAM将占总收入的31.85%,继续在感测器融合和车辆动力学等对延迟要求极高的工作负载领域保持主导地位;而3D NAND将以19.25%的速度增长,这主要得益于每比特成本的下降和AEC-Q100标准的日益普及。读取速度高达4200MB/s的汽车级UFS 4.1快闪记忆体正在成为资料记录器和空中韧体库的标准储存解决方案。

NOR快闪记忆体继续承担启动和恢復任务,但容量限制限制了其年增长。诸如MRAM之类的新兴非挥发性记忆体(NVM)正在故障安全记录和即时启动仪表板等细分领域站稳脚跟。整体趋势清晰可见:DRAM为运算密集型AI模组提供动力,而3D NAND则满足日益增长的持久储存需求,二者相辅相成,构成半导体记忆体市场的核心力量。

汽车半导体记忆体市场报告按技术角色(例如,代码储存、工作记忆体)、记忆体类型(例如,DRAM、 NAND快闪记忆体)、应用(例如,ADAS和自动驾驶、数位驾驶座)、车辆类型(例如,乘用车、轻型商用车)和地区(例如,北美、南美、欧洲)进行细分。市场预测以美元以金额为准。

区域分析

预计到2025年,亚太地区将以37.95%的市占率引领半导体记忆体市场,并以19.88%的复合年增长率扩大领先优势,这主要得益于中国积极的电动车普及目标和韩国强大的製造业基础。中国在亚太全部区域中占相当大的份额,但由于先进製程节点的出口管制措施,中国仍面临持续的挑战。韩国凭藉其垂直整合的主要企业——三星和SK海力士,与全球一级供应商签订了长期合约。同时,日本记忆体代工厂与汽车零件供应商之间的紧密合作,缩短了产品认证前置作业时间。

北美位居第二,这得益于《晶片法案》(CHIPS Act)提供的520亿美元拨款,用于半导体製造业回流,包括在德克萨斯州、亚利桑那州和印第安纳州建设专用汽车生产线。特斯拉的垂直整合模式和底特律的Ultium纯电动车平台是关键因素,推动了国内对1级LPDDR5-X和高循环固态硬碟的需求。加拿大和墨西哥分别透过电池模组组装和经济高效的电子集成,为该地区提供补充,从而增强了三方供应链的韧性。

欧洲正透过价值430亿欧元的《欧洲晶片法案》建构战略自主性,并以德国汽车製造商和记忆体製造商为核心组建了一个联盟,旨在实现部分供应链的本地化。监管机构对ISO 26262和ISO/SAE 21434标准的重视,正在推动对认证记忆体解决方案的需求。同时,中东和非洲地区虽然在绝对销量上落后,但由于阿联酋和南非的电动车製造激励政策,该地区正迅速发展,并有望在本十年末成为半导体记忆体市场的新兴前沿阵地。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 介绍软体定义车辆(SDV)

- 集中式/分区式EE架构

- 整合到微控制器中的特定领域人工智慧加速器

- 二级以上ADAS ECU的记忆体容量增加

- 汽车製造商越来越多地采用空中升级 (OTA) 週期

- 降低汽车用3D NAND的成本

- 市场限制

- 汽车硅供应链的波动性

- 与消费性记忆体价格差异庞大

- 功能安全认证前置作业时间

- 高密度组件的温度控管局限性

- 宏观经济因素如何影响市场

- 产业价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按技术角色

- 程式码储存

- 工作记忆

- 资料储存

- 其他角色(例如启动、日誌记录等)

- 按记忆体类型

- DRAM

- NAND快闪记忆体

- NOR Flash

- MRAM 和新兴的非挥发性记忆体

- 透过使用

- 高级驾驶辅助系统和自动驾驶

- 数位驾驶座

- 动力传动系统

- 底盘和安全装置

- 身体和舒适度

- 按车辆类型

- 搭乘用车

- 轻型商用车

- 大型商用车辆

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 东南亚

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Samsung Electronics Co., Ltd.

- Micron Technology, Inc.

- SK hynix Inc.

- Kioxia Holdings Corporation

- Infineon Technologies AG

- Renesas Electronics Corporation

- NXP Semiconductors NV

- Winbond Electronics Corporation

- Macronix International Co., Ltd.

- GigaDevice Semiconductor Inc.

- Integrated Silicon Solution, Inc.(ISSI)

- Everspin Technologies, Inc.

- Powerchip Technology Corporation

- Transcend Information, Inc.

- Kingston Technology Corporation

- Swissbit AG

- Virtium LLC

- Alliance Memory, Inc.

- AP Memory Technology Corp.

- Semiconductor Manufacturing International Corp.(SMIC)

- Tower Semiconductor Ltd.

- Yangtze Memory Technologies Co.(YMTC)

- Western Digital Corporation

第七章 市场机会与未来展望

The semiconductor memory market for automotive is expected to grow from USD 13.7 billion in 2025 to USD 16.29 billion in 2026 and is forecast to reach USD 38.77 billion by 2031 at 18.94% CAGR over 2026-2031.

The surge is fueled by the shift toward software-defined vehicles, which bundle dozens of electronic functions into centralized compute domains, sharply increasing memory density and bandwidth requirements per car. Regulatory momentum behind Level 2+ driver assistance in China, the United States, and the European Union is accelerating demand for gigabyte-scale working memory that can meet functional-safety standards. Meanwhile, cost-optimized 3D NAND and upcoming MRAM options are expanding the addressable base of applications, letting automakers balance performance and bill-of-materials pressures more effectively. Intensifying supply-chain localization in the United States and Europe is also steering procurement strategies toward multi-sourced, automotive-qualified memory, reducing overreliance on any single region. Finally, premium vehicle programs are pioneering over-the-air software strategies that multiply flash capacity requirements and build a durable replacement cycle for next-generation modules.

Insights and Trends of Semiconductor Memory Market For Automotive

Software-Defined Vehicle Adoption

Automakers are transforming cars into rolling data centers that rely on continuous software updates and feature deployment. Tesla's Hardware 4.0 showcases a significant leap in memory intensity by integrating multiple LPDDR5 stacks, which stream 12 camera feeds and radar inputs in real-time. Centralized designs slash the traditional network of more than 100 ECUs to a handful of high-performance domain controllers, raising installed DRAM from megabyte ranges to multi-gigabyte footprints. Luxury trims are already equipped with 32 GB of total memory, and mainstream models are expected to trend toward similar capacities by 2027. The upgrade path aligns with longer software maintenance cycles, ensuring recurring demand for high-bandwidth, AEC-Q100 Grade 1 modules.

Centralized/Zonal E-E Architecture

BMW's forthcoming iDrive generation demonstrates how zonal designs allocate memory resources efficiently, rather than assigning discrete modules to each subsystem. Consolidation eliminates duplication, reducing part counts by up to 30%. However, each surviving module must deliver higher throughput and withstand heavier thermal loads. The net effect is a shift in demand toward 64-bit-wide DRAM interfaces and faster access speeds, approaching 6 Gb/s, particularly in the infotainment and ADAS domains. Tier-1 suppliers are adapting by co-packaging memory and processors on high-density substrates, a trend that favors vendors with advanced capabilities at the 10 nm node and below. The architecture is rolling out first in premium nameplates but is expected to penetrate mass-market segments within four years.

Supply-Chain Volatility

The 2024 Taiwan earthquake exposed the fragility of geographically concentrated fabs, disrupting controller output and inflating lead times for Grade-1 memory by 20 weeks. Automotive lines, which account for under 10% of total wafer demand, often drop in supplier priority when shortages occur. OEMs are therefore dual-sourcing between South Korea and the United States, but qualification cycles extend this mitigation effort to at least 2026. Divergent export-control regimes and geopolitical uncertainty could shave 100-150 basis points off near-term growth.

Other drivers and restraints analyzed in the detailed report include:

- Domain-Specific AI Accelerators in MCUs

- Growing Memory Content per Level-2+ ADAS ECU

- High Automotive Selling Price (ASP) Premium

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Working memory dominated the semiconductor memory market, accounting for a 38.72% share in 2025, due to the high real-time processing loads in ADAS and infotainment units. Luxury EVs now integrate up to 32 GB of LPDDR5 for centralized compute clusters, while mass-market models are expected to trend toward 16 GB by 2027. Code storage remains stable as firmware footprints plateau around 8-16 GB, while data storage rockets at a 20.02% CAGR as vehicles harvest terabytes of sensor data for edge analytics. The semiconductor memory market size is tied to data storage, reinforcing long-term demand for high-capacity 3D NAND devices.

The outlook for working memory is further buoyed by the arrival of zonal architectures that standardize memory pools shared across safety, cockpit, and powertrain domains. This consolidation demands higher per-module performance, driving a pivot toward wide-I/O interfaces and built-in ECC engines. Suppliers offering dual-purpose DRAM-NAND combinations are poised to capture incremental market share among OEMs seeking to streamline their qualification pipelines. HBM-Lite concepts under evaluation could emerge after 2028 if thermal hurdles are resolved, potentially opening an adjacent revenue stream within the semiconductor memory market.

DRAM delivered 31.85% of 2025 revenue, maintaining its leading position in latency-critical workloads, such as sensor fusion and vehicle dynamics. Simultaneously, 3D NAND is advancing at a 19.25% growth pace, driven by declining cost-per-bit and broader AEC-Q100 coverage. Automotive-grade UFS 4.1 drives, which offer 4,200 MB/s read speeds, are emerging as the default storage solutions for data recorders and over-the-air firmware repositories.

NOR flash continues to fulfill boot and recovery tasks, but density limitations restrict its annual expansion. MRAM and other emerging NVMs are carving niche footholds in fail-safe logging and instant-on dashboards. The overarching dynamic is clear: DRAM feeds compute-intensive AI blocks, while 3D NAND underpins the escalating appetite for persistent storage, forming a complementary duo at the heart of the semiconductor memory market.

The Semiconductor Memory Market for Automotive Report is Segmented by Technology Role (Code Storage, Working Memory, and More), Memory Type (DRAM, NAND Flash, and More), Application (ADAS and Automated Driving, Digital Cockpit, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), and Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led with 37.95% semiconductor memory market share in 2025 and is expected to broaden its lead at a 19.88% CAGR, buoyed by China's aggressive EV penetration targets and South Korea's manufacturing depth. China alone represents a significant share of regional volume but faces continuing headwinds from export-control measures on advanced nodes. South Korea leverages its vertically integrated champions, Samsung and SK Hynix, to secure long-term contracts with global Tier-1s, while Japan's close collaboration between memory fabs and automotive suppliers compresses qualification lead times.

North America ranks second, backed by USD 52 billion CHIPS Act subsidies aimed at reshoring semiconductor output, including dedicated automotive lines in Texas, Arizona, and Indiana. Tesla's vertically integrated model and Detroit's Ultium BEV platform are major off-takers, pushing domestic demand for Grade-1 LPDDR5-X and high-cycle SSDs. Canada and Mexico complement the region through battery-module assembly and cost-efficient electronics integration, respectively, fostering trilateral supply resiliency.

Europe is carving strategic autonomy via the EUR 43 billion European Chips Act, with consortia forming around German OEMs and memory makers to localize parts of the supply chain. The regulatory emphasis on ISO 26262 and ISO/SAE 21434 has elevated the demand for certified memory solutions. Meanwhile, the Middle East and Africa trail in absolute volume but are gaining traction through EV manufacturing incentives in the United Arab Emirates and South Africa, signaling an emerging frontier for the semiconductor memory market by the end of the decade.

- Samsung Electronics Co., Ltd.

- Micron Technology, Inc.

- SK hynix Inc.

- Kioxia Holdings Corporation

- Infineon Technologies AG

- Renesas Electronics Corporation

- NXP Semiconductors N.V.

- Winbond Electronics Corporation

- Macronix International Co., Ltd.

- GigaDevice Semiconductor Inc.

- Integrated Silicon Solution, Inc. (ISSI)

- Everspin Technologies, Inc.

- Powerchip Technology Corporation

- Transcend Information, Inc.

- Kingston Technology Corporation

- Swissbit AG

- Virtium LLC

- Alliance Memory, Inc.

- AP Memory Technology Corp.

- Semiconductor Manufacturing International Corp. (SMIC)

- Tower Semiconductor Ltd.

- Yangtze Memory Technologies Co. (YMTC)

- Western Digital Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Software-Defined Vehicle (SDV) adoption

- 4.2.2 Centralized/Zonal E-E Architecture

- 4.2.3 Domain-specific AI accelerators inside MCUs

- 4.2.4 Growing memory content per Level-2+ ADAS ECU

- 4.2.5 Wider OEM use of over-the-air (OTA) update cycles

- 4.2.6 Automotive-qualified 3D NAND cost decline

- 4.3 Market Restraints

- 4.3.1 Volatility in automotive silicon supply chain

- 4.3.2 High ASP gap vs. consumer-grade memory

- 4.3.3 Functional-safety certification lead-times

- 4.3.4 Thermal-management limits in high-density modules

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology Role

- 5.1.1 Code Storage

- 5.1.2 Working Memory

- 5.1.3 Data Storage

- 5.1.4 Other Roles (e.g., Boot, Logs)

- 5.2 By Memory Type

- 5.2.1 DRAM

- 5.2.2 NAND Flash

- 5.2.3 NOR Flash

- 5.2.4 MRAM and Emerging NVM

- 5.3 By Application

- 5.3.1 ADAS and Automated Driving

- 5.3.2 Digital Cockpit

- 5.3.3 Powertrain

- 5.3.4 Chassis and Safety

- 5.3.5 Body and Comfort

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Light Commercial Vehicles

- 5.4.3 Heavy Commercial Vehicles

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 South-East Asia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Samsung Electronics Co., Ltd.

- 6.4.2 Micron Technology, Inc.

- 6.4.3 SK hynix Inc.

- 6.4.4 Kioxia Holdings Corporation

- 6.4.5 Infineon Technologies AG

- 6.4.6 Renesas Electronics Corporation

- 6.4.7 NXP Semiconductors N.V.

- 6.4.8 Winbond Electronics Corporation

- 6.4.9 Macronix International Co., Ltd.

- 6.4.10 GigaDevice Semiconductor Inc.

- 6.4.11 Integrated Silicon Solution, Inc. (ISSI)

- 6.4.12 Everspin Technologies, Inc.

- 6.4.13 Powerchip Technology Corporation

- 6.4.14 Transcend Information, Inc.

- 6.4.15 Kingston Technology Corporation

- 6.4.16 Swissbit AG

- 6.4.17 Virtium LLC

- 6.4.18 Alliance Memory, Inc.

- 6.4.19 AP Memory Technology Corp.

- 6.4.20 Semiconductor Manufacturing International Corp. (SMIC)

- 6.4.21 Tower Semiconductor Ltd.

- 6.4.22 Yangtze Memory Technologies Co. (YMTC)

- 6.4.23 Western Digital Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

汽车储存半导体市场:依记忆体类型、车辆类型、应用、最终用户、国家及地区划分-产业分析、市场规模、市场占有率及2025年至2032年预测

汽车储存半导体市场:依记忆体类型、车辆类型、应用、最终用户、国家及地区划分-产业分析、市场规模、市场占有率及2025年至2032年预测 汽车储存半导体市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)

汽车储存半导体市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)