|

市场调查报告书

商品编码

1934886

美洲感测器市场:市场份额分析、产业趋势与统计、成长预测(2026-2031 年)Americas Sensor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

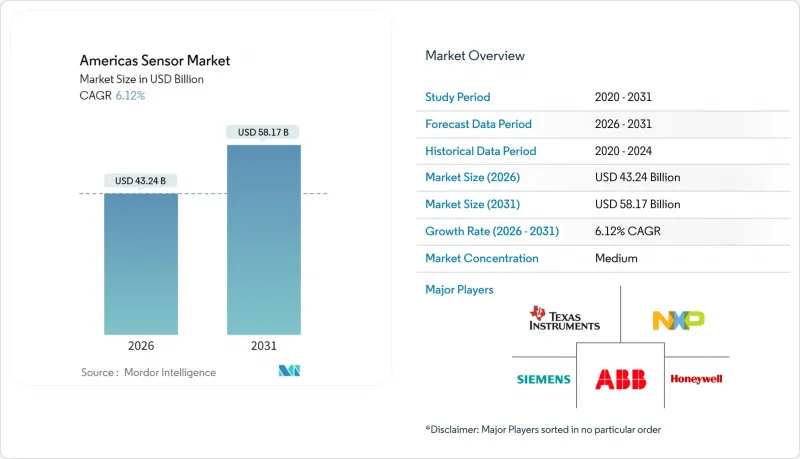

预计美洲感测器市场将从 2025 年的 407.5 亿美元成长到 2026 年的 432.4 亿美元,到 2031 年将达到 581.7 亿美元,2026 年至 2031 年的复合年增长率为 6.12%。

量子导航系统、低功耗边缘人工智慧处理以及微机电系统(MEMS)小型化正在融合,成为推动市场需求成长的主要动力。同时,政府对智慧基础设施的大量投入正在加速其大规模应用。对自动驾驶汽车、精密农业和可再生能源监测的投资加剧了雷射雷达、环境和振动感测技术的竞争。持续的地缘政治摩擦促使人们迫切需要将氮化镓和碳化硅基板的供应链迁回国内。策略併购,特别是意法半导体计画以9.5亿美元收购恩智浦半导体的感测器部门,标誌着市场正向垂直整合平台转型,这些平台能够提供安全可靠的、支援人工智慧的感测器融合功能。

美洲感测器市场趋势与洞察

消费性物联网设备的快速普及

智慧家庭在美国和加拿大的主要城市正逐步市场层级,形成对低功耗无线感测器的持续需求,这类感测器只需一枚纽扣电池即可运作数年。美国运输部的SMART津贴正在推动城市交通和空气品质感测器的部署,确保采购预算并规范连接通讯协定。这些设备中嵌入的边缘AI晶片组消除了云端延迟并保护了资料隐私,这对于实施严格数位主权规则的地区至关重要。由此带来的销售成长正在帮助MEMS供应商实现规模经济,并刺激拉丁美洲大都市地区升级公共运输网路的需求。

美洲製造业自动化投资不断成长

美国和墨西哥的原始设备製造商 (OEM) 正在改造生产线,加装振动、声学和热传感器,这些传感器能够为预测性维护算法提供信息,从而显着减少计划外停机时间。巴西石油公司 (Petrobras) 在巴西的工厂正在部署基于感测器的能源仪表板,以降低公用事业成本并履行环境、社会和治理 (ESG) 报告义务。道达尔能源 (Total Energies) 炼油厂无线振动感测器的试点部署在一个季度内实现了零计划外停机,证明了大规模部署的投资回报率 (ROI)。随着感测器在从底特律到蒙特雷和圣保罗的汽车、金属和食品加工产业走廊得到应用,这些成果正在加速跨境技术转移。

对安全关键感测器的严格监管认证

汽车功能安全法规将检验週期延长了至多18个月,这使得没有专门合规团队的新创公司处于不利地位。 FDA对临床级穿戴装置的监管要求包括高成本的生物相容性测试和上市后监管审核,随着美洲感测器产业的整合,这进一步巩固了现有企业的优势。

细分市场分析

环境感测器以7.86%的复合年增长率成为成长最快的市场,这主要得益于企业竞相达到范围1排放目标,以及政府机构强制要求提供即时空气品质数据。然而,温度测量设备占据了美洲感测器市场19.46%的最大份额,这主要归功于其在暖通空调系统和家用电子电器的广泛应用。压力和液位感测器在能源管道和智慧水网中的应用日益普及,这一趋势主要受美国西部地区抗旱计划的推动。随着工厂向无人营运转型,流量和接近感测器在机器人和包装生产线中的应用也日益广泛。Honeywell为国防承包商进行的量子磁力计和惯性测量单元试验,预示着超高精度导航应用时代的到来。

二次渗透效应在农业领域显而易见,振动感测器和化学感测器分别用于评估土壤压实度和养分含量。嵌入穿戴式装置的微型MEMS湿度感测器正在推动健康监测应用,而磁感测器则有助于追踪可再生能源涡轮机的位置。这些趋势共同推动环境解决方案在采购计画中占据优先地位,并不断扩大其在美洲感测器市场的份额。

随着汽车OEM厂商最终敲定下一代ADAS平台,雷射雷达(LiDAR)的复合年增长率(CAGR)高达8.02%,超过了所有其他应用类别。同时,电容式感测器在出货量方面保持了17.88%的领先地位,这主要得益于消费和工业领域对触控萤幕、近距离感应和液位监测等应用的持续需求。光学和成像感测器受益于边缘AI增强的噪音抑制技术,其在远端医疗和空气品质分析领域的应用日益广泛。电阻式感测器和生物感测器则在对精度和校准漂移高度敏感的低温运输物流和连续血糖监测领域开闢了一片天地。

除了防碰撞系统之外,雷达模组的应用范围正在扩展到周界安防和工业起重机自动化领域,填补了光学视距(LOS)失效环境下的性能空白。整合了雷射雷达、雷达和成像单元的多模融合堆迭正逐渐成为自动驾驶班车的标准架构,进一步扩大了美洲自动驾驶解决方案的感测器市场。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 消费性物联网设备的快速普及

- 北美和南美製造业自动化投资增加

- 政府对智慧基础设施维修的激励措施

- 随着电动车和自动驾驶汽车的日益普及,对多感测器套件的需求也日益增长。

- 低功耗边缘人工智慧的兴起使得感测器端分析成为可能。

- 可印刷/柔性感测器在医疗穿戴设备中的应用日益广泛

- 市场限制

- 对安全关键感测器的严格监管认证

- MEMS生产线的高资本投入

- 特种材料(GaN、SiC)供应链的集中化

- 与感测器资料完整性相关的网路安全责任

- 产业价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 宏观经济因素如何影响市场

第五章 市场规模与成长预测

- 透过测量参数

- 温度

- 压力

- 等级

- 流动

- 邻近性

- 环境

- 化学

- 惯性测量单元

- 磁的

- 振动

- 其他参数

- 按操作模式

- 光学

- 电阻

- 生物感测器

- 压阻式

- 影像

- 电容式

- 压电

- LiDAR

- 雷达

- 其他模式

- 透过感测器技术

- MEMS感测器

- 非MEMS感测器

- 按最终用户行业划分

- 车

- 家用电子电器

- 智慧型手机

- 平板电脑、笔记型电脑、电脑

- 穿戴式装置

- 智慧家庭设备

- 其他家用电子电器

- 能源与公共产业

- 工业自动化

- 医疗卫生领域

- 建筑业、农业、矿业

- 航太

- 国防与安全

- 按国家/地区

- 我们

- 加拿大

- 巴西

- 墨西哥

- 阿根廷

- 智利

- 其他美洲国家

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Texas Instruments Incorporated

- TE Connectivity Ltd.

- Omega Engineering Inc.

- Honeywell International Inc.

- Rockwell Automation Inc.

- Siemens AG

- ams-OSRAM AG

- NXP Semiconductors NV

- Infineon Technologies AG

- Bosch Sensortec GmbH

- SICK AG

- ABB Ltd.

- OMRON Corporation

- STMicroelectronics NV

- Analog Devices, Inc.

- Microchip Technology Inc.

- Sensata Technologies Holding plc

- Murata Manufacturing Co., Ltd.

- Panasonic Holdings Corporation

- Qualcomm Incorporated

第七章 市场机会与未来展望

The Americas sensor market is expected to grow from USD 40.75 billion in 2025 to USD 43.24 billion in 2026 and is forecast to reach USD 58.17 billion by 2031 at 6.12% CAGR over 2026-2031.

Quantum-enabled navigation systems, low-power edge-AI processing, and MEMS miniaturization together create the strongest pull on demand, while heavy public-sector funding for smart infrastructure accelerates large-scale deployments. Investments in autonomous vehicles, precision agriculture, and renewable-energy monitoring are intensifying competition around LiDAR, environmental, and vibration sensing technologies. Supply-chain reshoring for gallium-nitride and silicon-carbide substrates gains urgency as geopolitical frictions persist. Strategic M&A - most notably STMicroelectronics' planned USD 950 million purchase of NXP's sensor unit - signals a shift toward vertically integrated platforms offering secure, AI-ready sensor fusion capabilities.

Americas Sensor Market Trends and Insights

Rapid Proliferation of Consumer IoT Devices

Smart-home penetration now reaches mass-market levels in major U.S. and Canadian cities, creating sustained demand for low-power wireless sensors that can operate for years on a coin cell. The U.S. Department of Transportation's SMART Grants are catalyzing citywide traffic and air-quality sensor rollouts, locking in procurement budgets and standardizing connectivity protocols. Edge-AI chipsets embedded inside these devices eliminate cloud latency and protect data privacy - critical for jurisdictions implementing strict digital sovereignty rules. The resulting volume lift underpins economies of scale for MEMS suppliers, with spillover demand in Latin American metros upgrading public-transport networks.

Rising Automation Investments in North and South American Manufacturing

OEMs across the United States and Mexico retool production lines with vibration, acoustic, and thermal sensors that feed predictive-maintenance algorithms, slashing unplanned downtime. Petrobras-supplied Brazilian plants deploy sensor-based energy dashboards to curb utility costs and satisfy ESG reporting mandates. TotalEnergies' refinery pilot with wireless vibration sensors demonstrated a full quarter without unscheduled shutdowns, validating ROI for widescale rollouts. These wins accelerate cross-border knowledge transfer, hardwiring sensor adoption into automotive, metals, and food-processing corridors from Detroit to Monterrey and Sao Paulo.

Stringent Regulatory Certification for Safety-Critical Sensors

Automotive functional-safety regulations extend validation cycles by up to 18 months, disfavoring venture-backed startups that lack dedicated compliance teams. FDA mandates for clinical-grade wearables impose costly biocompatibility and post-market surveillance audits, reinforcing incumbent advantage as the Americas sensor industry consolidates.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives for Smart-Infrastructure Retrofits

- Expansion of Electric and Autonomous Vehicles Requiring Multi-Sensor Suites

- Supply-Chain Concentration in Exotic Materials (GaN, SiC)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Environmental sensors post the fastest 7.86% CAGR as corporates race to meet Scope-1 emissions targets and municipal bodies mandate real-time air-quality data. Temperature devices nonetheless hold the largest 19.46% slice of the Americas sensor market share, thanks to ubiquitous HVAC and consumer-electronics integration. Pressure and level sensors scale within energy pipelines and smart water networks, a trend amplified by drought-mitigation projects across the Western United States. Flow and proximity sensing gain traction in robotics and packaging lines as factories pivot to lights-out operations. Quantum magnetometers and inertial units - piloted by Honeywell for defense contracts - hint at a coming wave of ultra-precise navigation applications.

Second-order adoption effects surface in agriculture, where vibration and chemical sensors diagnose soil compaction and nutrient levels, respectively. Miniaturized MEMS humidity sensors embedded in wearables push health-monitoring use cases, while magnetic sensors underpin renewable-energy turbine position tracking. Collectively, these dynamics keep environmental solutions front and center in procurement roadmaps and increase their proportion of the Americas sensor market.

LiDAR's 8.02% CAGR outpaces all other operational classes as automotive OEMs lock in next-generation ADAS platforms. Simultaneously, capacitive devices maintain an 17.88% leading share by unit shipments because of sustained touchscreen, proximity, and fill-level applications across consumer and industrial sectors. Optical and imaging sensors deepen penetration in telemedicine and air-quality analytics, benefitting from edge-AI-enhanced noise suppression. Electrical-resistance and biosensors carve niches in cold-chain logistics and continuous glucose monitoring-segments highly sensitive to accuracy and calibration drift.

Radar modules extend beyond collision-avoidance systems into perimeter security and industrial crane automation, filling performance gaps where optical LOS is compromised. Multi-mode fusion stacks that co-package LiDAR, radar, and imaging units emerge as the reference architecture for autonomous shuttles, further expanding the Americas sensor market size attached to autonomy solutions.

The Americas Sensor Market Report is Segmented by Parameters Measured (Temperature, Pressure, Level, Flow, and More), Mode of Operations (Optical, Electrical Resistance, Biosensor, Piezoresistive, and More), Sensor Technology (MEMS Sensors, and More), End-User Industry (Automotive, Consumer Electronics, Energy, and More), and Country (United States, Canada, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Texas Instruments Incorporated

- TE Connectivity Ltd.

- Omega Engineering Inc.

- Honeywell International Inc.

- Rockwell Automation Inc.

- Siemens AG

- ams-OSRAM AG

- NXP Semiconductors N.V.

- Infineon Technologies AG

- Bosch Sensortec GmbH

- SICK AG

- ABB Ltd.

- OMRON Corporation

- STMicroelectronics N.V.

- Analog Devices, Inc.

- Microchip Technology Inc.

- Sensata Technologies Holding plc

- Murata Manufacturing Co., Ltd.

- Panasonic Holdings Corporation

- Qualcomm Incorporated

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid proliferation of consumer IoT devices

- 4.2.2 Rising automation investments in North and South American manufacturing

- 4.2.3 Government incentives for smart-infrastructure retrofits

- 4.2.4 Expansion of electric and autonomous vehicles requiring multi-sensor suites

- 4.2.5 Emergence of low-power edge AI enabling on-sensor analytics

- 4.2.6 Increasing adoption of printable/flexible sensors in healthcare wearables

- 4.3 Market Restraints

- 4.3.1 Stringent regulatory certification for safety-critical sensors

- 4.3.2 High capital expenditure for MEMS fabrication lines

- 4.3.3 Supply-chain concentration in exotic materials (GaN, SiC)

- 4.3.4 Cyber-security liabilities tied to sensor data integrity

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Parameter Measured

- 5.1.1 Temperature

- 5.1.2 Pressure

- 5.1.3 Level

- 5.1.4 Flow

- 5.1.5 Proximity

- 5.1.6 Environmental

- 5.1.7 Chemical

- 5.1.8 Inertial

- 5.1.9 Magnetic

- 5.1.10 Vibration

- 5.1.11 Other Parameters

- 5.2 By Mode of Operation

- 5.2.1 Optical

- 5.2.2 Electrical Resistance

- 5.2.3 Biosensor

- 5.2.4 Piezoresistive

- 5.2.5 Image

- 5.2.6 Capacitive

- 5.2.7 Piezoelectric

- 5.2.8 LiDAR

- 5.2.9 Radar

- 5.2.10 Other Modes

- 5.3 By Sensor Technology

- 5.3.1 MEMS Sensors

- 5.3.2 Non-MEMS Sensors

- 5.4 By End-user Industry

- 5.4.1 Automotive

- 5.4.2 Consumer Electronics

- 5.4.2.1 Smartphones

- 5.4.2.2 Tablets, Laptops and Computers

- 5.4.2.3 Wearable Devices

- 5.4.2.4 Smart Appliances

- 5.4.2.5 Other Consumer Electronics

- 5.4.3 Energy and Utilities

- 5.4.4 Industrial Automation

- 5.4.5 Medical and Wellness

- 5.4.6 Construction, Agriculture and Mining

- 5.4.7 Aerospace

- 5.4.8 Defense and Security

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Brazil

- 5.5.4 Mexico

- 5.5.5 Argentina

- 5.5.6 Chile

- 5.5.7 Rest of Americas

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Texas Instruments Incorporated

- 6.4.2 TE Connectivity Ltd.

- 6.4.3 Omega Engineering Inc.

- 6.4.4 Honeywell International Inc.

- 6.4.5 Rockwell Automation Inc.

- 6.4.6 Siemens AG

- 6.4.7 ams-OSRAM AG

- 6.4.8 NXP Semiconductors N.V.

- 6.4.9 Infineon Technologies AG

- 6.4.10 Bosch Sensortec GmbH

- 6.4.11 SICK AG

- 6.4.12 ABB Ltd.

- 6.4.13 OMRON Corporation

- 6.4.14 STMicroelectronics N.V.

- 6.4.15 Analog Devices, Inc.

- 6.4.16 Microchip Technology Inc.

- 6.4.17 Sensata Technologies Holding plc

- 6.4.18 Murata Manufacturing Co., Ltd.

- 6.4.19 Panasonic Holdings Corporation

- 6.4.20 Qualcomm Incorporated

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

感测器市场分析及预测(至2035年):依类型、产品、技术、最终用户、材料、测量参数及输出划分

感测器市场分析及预测(至2035年):依类型、产品、技术、最终用户、材料、测量参数及输出划分 薄膜感测器市场:依产品类型、技术、基板类型和最终用途产业划分-2026-2032年全球市场预测大气感测器市场:2026-2032年全球市场预测(按感测器类型、技术、安装方式、应用和最终用户划分)感测器市场:按感测器类型、技术类型、连接方式、最终用户产业和应用划分-2026-2032年全球市场预测

薄膜感测器市场:依产品类型、技术、基板类型和最终用途产业划分-2026-2032年全球市场预测大气感测器市场:2026-2032年全球市场预测(按感测器类型、技术、安装方式、应用和最终用户划分)感测器市场:按感测器类型、技术类型、连接方式、最终用户产业和应用划分-2026-2032年全球市场预测 钢材接近感测器市场报告:趋势、预测和竞争分析(至2035年)电导率仪市场:全球市场按产品类型、测量范围、电极类型、应用和最终用户分類的预测——2026-2032年

钢材接近感测器市场报告:趋势、预测和竞争分析(至2035年)电导率仪市场:全球市场按产品类型、测量范围、电极类型、应用和最终用户分類的预测——2026-2032年 2026年全球自由落体金属探测器市场报告互动式感测器市场:依技术、应用、最终用途、连接方式和外形规格-2026-2032年全球市场预测整合感测器市场:按技术、感测器类型、输出讯号和应用划分-2026-2032年全球市场预测

2026年全球自由落体金属探测器市场报告互动式感测器市场:依技术、应用、最终用途、连接方式和外形规格-2026-2032年全球市场预测整合感测器市场:按技术、感测器类型、输出讯号和应用划分-2026-2032年全球市场预测 频谱感测器市场:商业机会、成长要素、产业趋势分析及2026-2035年预测

频谱感测器市场:商业机会、成长要素、产业趋势分析及2026-2035年预测