|

市场调查报告书

商品编码

1934893

新加坡资料中心建置:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Singapore Data Center Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

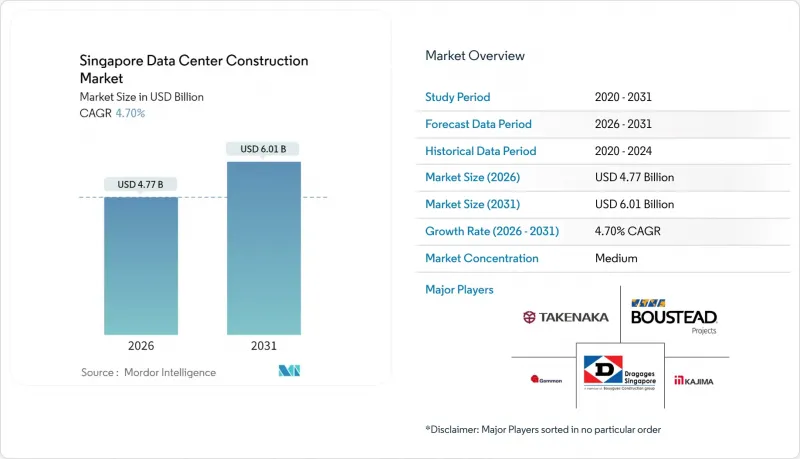

预计新加坡资料中心建设市场规模将从 2025 年的 45.6 亿美元成长到 2026 年的 47.7 亿美元,到 2031 年将达到 60.1 亿美元,2026 年至 2031 年的复合年增长率为 4.70%。

新加坡严格的电力分配政策、强大的海底光缆连接以及作为金融中心的地位,为持续投资提供了支撑。然而,营运商面临土地短缺和高昂的建设成本。绿色资料中心蓝图下不断完善的法规正在推动设计方案实现更高的电源使用效率 (PUE),达到 1.3 或更高,这改变了竞标规范和设备选择。超大规模资料中心业者持续部署高密度 GPU 基础设施,平均机架功耗超过 50kW,刺激了对先进开关设备、液冷技术和模组化预製件的需求。同时,连接新加坡和柔佛的双枢纽策略透过提供过剩容量并保持核心工作负载低于 5 毫秒的延迟,缓解了当地的资源限制。投资者对资料中心房地产投资信託基金 (REITs) 的兴趣支撑着健康的企划案融资管道,帮助开发商抵消新加坡高昂的土地和人事费用。

新加坡资料中心建置市场趋势与洞察

根据绿色直流蓝图公布电力分配方案

新加坡修订后的绿色资料中心蓝图承诺,在资料中心PUE值低于1.3的前提下,至少分配300兆瓦的新增IT负荷,这正推动新加坡资料中心建设市场转型为高效节能设计。其中三分之二的配额将用于整合可再生能源和替代备用燃料的计划,促使开发商采用氢能发电机和热回收冷却器。领先正在部署人工智慧驱动的冷却控制系统,将能耗降低高达30%。有限的兆瓦电力资源竞标日益激烈,带动了对设计咨询服务的需求,并使拥有成熟永续性经验的公司更具优势。中期来看,该政策将加速市场向液冷和现场太阳能+储能混合系统的转型。这些因素共同为新加坡资料中心建设市场的专业承包商和设备供应商拓展了潜在机会。

AI/GPU密集型工作负载的快速成长对新的建筑规范提出了要求。

生成式人工智慧的浪潮正推动机架密度突破50kW,迫使新加坡资料中心建设市场转向采用浸没式冷却和晶片级直接冷却技术来冷却机械和电气设备。这种转变在大型园区维修计划中尤其明显,这些工程正采用设定温度为27°C的冷冻水循环系统和液冷迴路。高密度部署需要更长的布线距离和更大的母线槽,这会增加材料成本,并将试运行时间延长15-20%。为了应对这项挑战,开发商正在采用后门式热交换器和中压(22kV)配电系统来减少铜线用量。随着人工智慧推理在金融、医疗保健和公共部门工作负载中日益普及,建设计划越来越多地预留閒置频段用于放置GPU模组。儘管国家电力供应受到限制,新加坡的资料中心建设市场仍保持着两位数的计划成长率。

严格的300兆瓦年度电力配额和暂停令的影响

新加坡的电力配额上限在暂停三年后于2024年恢復实施,但其增速落后于区域需求成长,导致许多计画中的超大规模资料中心建设项目停滞不前。开发商被迫参与竞争性招标,而招标过程侧重于电力使用效率(PUE)和碳排放强度,从而推高了前期咨询成本。兆瓦级电力短缺促使一些营运商将部分产能转移到巴淡岛和柔佛州,限制了新加坡资料中心建设市场的收入潜力。长期不确定性也使变压器和发电机的订购週期更加复杂,由于全球供应限制,前置作业时间已延长。预计这些因素将共同导致预测的复合年增长率下降约1.4个百分点。

细分市场分析

到2025年,电气设备包将占新加坡资料中心建设市场总支出的37.38%,反映出超大规模资料中心业者资料中心营运商对22kV电源、智慧开关设备和专为50kW及以上GPU机架运作的大容量母线槽的偏好。虽然液冷仍属于机械设备的一个子类别,但它是成长最快的组件,预计到2031年将为新加坡资料中心建设市场贡献6.285亿美元。浸没式水箱和后门式热交换器的应用减少了面积机架的閒置频段,使託管业者能够实现更高的收入密度。由于业主寻求PUE目标的承包检验,设计建造整合和试运行等服务的单价可能会更高。在预测期内,随着人工智慧驱动的最佳化平台需要电力和冷却迴路的即时遥测数据,电气设备和控制系统的整合将进一步加深。这种组合将提升能够透过单一合约涵盖电气和机械方面的公司的策略价值,从而巩固其在新加坡资料中心建立市场的竞争优势。

在机械设备领域,传统冷却器正被泵送式冷媒系统和介质浸没式冷却系统所取代,后者能够为每个晶片散发1200瓦的热量。一项联合工程将冷却能耗降低了29%,每个机架每年可节省约2.5万美元,为其他业者树立了成本节约的标竿。由于新加坡严格的建筑规范要求采用多层外壳、抗震加强和防爆建筑幕墙一般建筑工程保持着稳定的贡献。随着高密度布局需要更粗的光纤主干和人工智慧优化的拓扑结构, IT基础设施设施(机架、网路架构和线缆管理)的支出也不断增加。总而言之,这些变化凸显了随着工作负载复杂性的增加,专业分包商在新加坡资料中心建设市场中占据更大市场份额的趋势。

到2025年,Tier III级资料中心凭藉其均衡的提案和99.982%的运转率保证,占据了新加坡资料中心建设市场份额的53.22%。企业和云端服务供应商优先考虑可同时维护的基础设施,这种基础设施支援在运作中升级,无需像2N系统那样进行重复的资本投资。然而,在金融科技、交易平台和需要99.995%可用性的主权云端工作负载的推动下,Tier IV级资料中心正以5.03%的复合年增长率快速成长。这些高可靠性资料中心通常部署2N UPS、双燃料机房和独立的冷水机组,其机电设备(MEP)规模是Tier III级的两倍,从而推动了新加坡高端数据中心建设市场规模的成长。

Iron Mountain位于新加坡的资料中心具备Tier IV级标准,设有三个地理位置分散的会议室和一个生物安全通道。 Tier I和Tier II级计划仍在继续,主要面向边缘运算和通讯业者应用,但其收入贡献仍然有限。展望未来,监管机构和客户对资料中心弹性需求的不断增长预计将推动Tier III级标准向Tier IV级靠拢,模糊两者之间的界限。这将推动新加坡资料中心建设市场每兆瓦的基准支出水准上升。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 根据绿色直流蓝图(2024年起)释放电力配额

- AI/GPU密集型工作负载的激增需要新的建筑规范。

- 超大规模资料中心业者的「新加坡+柔佛」双枢纽建设策略

- 加速主权云端和新加坡金融管理局本地化监管

- 投资者对资料中心房地产投资信託基金(DC-REIT)转换的兴趣(吉宝资料中心、NTT资料中心REIT)

- 在土地使用限制条件下,采用模组化预製构件缩短施工时间

- 市场限制

- 更严格的300兆瓦年度电力配额和暂停令的遗留问题

- 亚太地区最高建设成本:1,170万美元/兆瓦,收费系统19美分/度

- 棕地地短缺;地下/高层建筑施工的可行性仍有检验

- 熟练机电工人短缺导致计划工期延长

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 新加坡主要资料中心建置统计数据

- 新加坡2023年及2024年装置容量(兆瓦)

- 新加坡在建IT总负荷(兆瓦),2025-2030年

- 在新加坡建造资料中心的平均资本支出和营运支出

- 新加坡资料中心基础设施领域的主要资本支出者

第五章 市场规模与成长预测

- 透过基础设施

- 电气设备

- 配电解决方案

- 配电单元

- 开关设备

- 其他的

- 备用电源解决方案

- UPS

- 发电机

- 配电解决方案

- 机械和设备

- 冷却系统

- 液冷法

- 空气冷却法

- 机架和机柜

- 其他机械和设备

- 冷却系统

- IT基础设施

- 伺服器

- 贮存

- 其他IT基础设施

- 一般建筑

- 服务

- 设计与咨询

- 一体化

- 支援与维护

- 电气设备

- 按层级标准

- 一级和二级

- 三级

- 四级

- 按最终用户行业划分

- 银行、金融服务和保险

- 资讯科技/通讯

- 政府/国防

- 卫生保健

- 其他最终用户

- 依资料中心类型

- 託管设施

- 超大规模/内部建设

- 企业/边缘/模组化

第六章 竞争情势

- 市占率分析

- 公司简介

- Boustead Projects

- Dragages Singapore(Bouygues)

- Takenaka Corp.

- Gammon Pte Ltd(Balfour Beatty)

- Sato Kogyo

- Kajima Overseas Asia

- Woh Hup(Private)Ltd

- China Construction(South Pacific)Dev.

- SsangYong Engineering and Construction

- Hyundai Engineering and Construction

- Obayashi Singapore

- Lendlease Singapore

- Keppel Data Centre Development

- ST Telemedia Global DC

- Equinix Construction Services

- Digital Realty(Digital Singapore)

- AIMS APAC REIT(DC builder arm)

- NTT Global DC Singapore

- M1 Net/Keppel DC and M1 JV

- AirTrunk(Blackstone)

- EdgeConneX

- Princeton Digital Group

- Microsoft(self-build campus)

- Amazon Web Services-Construction Ops

- Google Singapore DC Projects

第七章 市场机会与未来展望

The Singapore data center construction market is expected to grow from USD 4.56 billion in 2025 to USD 4.77 billion in 2026 and is forecast to reach USD 6.01 billion by 2031 at 4.70% CAGR over 2026-2031.

Singapore's tightly managed power-allocation policy, robust subsea connectivity, and status as a financial hub anchor sustained investment even as operators confront land scarcity and high build costs. Regulatory momentum under the Green Data Centre Roadmap encourages designs that achieve Power Usage Effectiveness (PUE) of 1.3 or better, reshaping tender specifications and equipment choices. Hyperscalers continue to deploy GPU-dense infrastructure that pushes average rack power beyond 50 kW, accelerating demand for advanced switchgear, liquid cooling, and modular prefabrication. Meanwhile, the twin-hub strategy that links Singapore with Johor mitigates local constraints by allowing capacity spill-over while preserving sub-5 ms latency to core workloads. Investor appetite for data-center REITs supports a healthy project finance pipeline, helping developers offset the city-state's premium land and labor costs.

Singapore Data Center Construction Market Trends and Insights

Power-Allocation Release Under Green DC Roadmap

Singapore's revised Green Data Centre Roadmap commits at least 300 MW of new IT load on the condition that facilities demonstrate PUE of 1.3 or lower, pivoting the Singapore data center construction market toward highly efficient designs. Two-thirds of the quota rewards projects that integrate renewables or alternative backup fuels, prompting developers to specify hydrogen-ready generators and heat-recovery chillers. Early movers have implemented AI-driven cooling control to reduce energy use by up to 30%. Competitive bidding for scarce megawatts intensifies, raising design consultancy demand and favoring firms with a proven sustainability track record. Over the medium term, the policy accelerates the market's migration toward liquid cooling and on-site solar plus energy-storage hybrids. These elements together enlarge the addressable opportunity for specialist contractors and equipment vendors within the Singapore data center construction market.

Surge in AI/GPU-Dense Workloads Requiring New Build Specs

The generative-AI wave lifts rack densities above 50 kW, forcing mechanical and electrical packages in the Singapore data center construction market to pivot toward immersion and direct-to-chip cooling. A major campus upgrade showcases this shift, featuring chilled-water and liquid-cooling loops designed for 27 °C set-points. High-density deployment elongates cable runs and upsizes busways, which increases bill-of-materials value yet lengthens commissioning time by 15-20%. Developers respond by adopting rear-door heat exchangers and medium-voltage (22 kV) power distribution to reduce copper usage. As AI inferencing proliferates across finance, healthcare, and public-sector workloads, construction pipelines increasingly bundle specialized white space for GPU pods, helping the Singapore data center construction market sustain double-digit project count growth despite the national power cap.

Tight 300 MW Annual Power Quota and Moratorium Legacy

Singapore's power-allocation ceiling, reinstated in 2024 after a three-year moratorium, falls below regional demand growth, stalling many planned hyperscale builds. Developers must compete in a Call-for-Application process whose scoring heavily weights PUE and carbon intensity, inflating pre-construction consultancy fees. The scarcity of megawatts drove some operators to shift incremental capacity to Batam or Johor, dampening the full revenue potential of the Singapore data center construction market. Long-term uncertainty also complicates transformer and generator ordering cycles, with lead times already stretched by global supply constraints. Together, these factors shave an estimated 1.4 percentage points from forecast CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Hyperscaler "Singapore-plus-Johor" Twin-Hub Build Strategies

- Accelerating Sovereign-Cloud and MAS FSI Localization Rules

- Highest APAC Construction Cost and Premium Power Tariffs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The electrical package accounted for 37.38% of overall spend within the Singapore data center construction market in 2025, reflecting hyperscaler preference for 22 kV feeds, intelligent switchgear, and high-capacity busways designed for GPU racks running at 50 kW and above. Liquid-based cooling, though still a subset of mechanical infrastructure, is the fastest-growing line item and will contribute USD 628.5 million to the Singapore data center construction market size by 2031. Adoption of immersion tanks and rear-door heat exchangers reduces white-space real estate per rack, enabling higher revenue density for colocation operators. Services such as design-build integration and commissioning enjoy premium billing rates because owners demand turnkey validation of PUE targets. Over the forecast window, integration between electrics and controls will deepen as AI-driven optimization platforms require real-time telemetry from both power and cooling loops. This convergence elevates the strategic value of firms that can span electrical and mechanical scopes in a single contract, cementing their competitive position within the Singapore data center construction market.

The mechanical segment is evolving from traditional chillers toward pumped refrigerant and dielectric immersion systems capable of dissipating 1,200 W per chip. A joint program cut cooling energy by 29%, saving roughly USD 25,000 per rack annually and setting a cost-avoidance benchmark other operators now target. General construction remains a steady contributor driven by multi-story shells, seismic reinforcement, and blast-resistant facades required under Singapore's stringent codes. IT infrastructure-racks, network fabric, and cable management-captures incremental spend as high-density layouts demand thicker fiber trunks and AI-optimized topologies. Collectively, these shifts underscore how rising workload complexity expands wallet share for specialized subcontractors in the Singapore data center construction market.

Tier III facilities delivered 53.22% of the Singapore data center construction market share in 2025 thanks to their balanced cost-reliability proposition and 99.982% uptime guarantee. Enterprises and cloud providers value concurrently maintainable infrastructure that supports live upgrades without the doubled capex of 2N systems. Nevertheless, Tier IV pipelines are expanding at 5.03% CAGR, fueled by fintech, trading desks, and sovereign-cloud workloads that demand 99.995% availability. These fault-tolerant sites typically deploy 2N UPS, dual fuel farms, and independent chilled-water plants, doubling MEP scope relative to Tier III and lifting the Singapore data center construction market size for high-tier builds.

Iron Mountain's Singapore facility typifies Tier IV attributes with three geographically diverse meet-me-rooms and bio-protected access corridors. Although Tier I and II projects persist in edge or telco applications, their contribution to revenue remains marginal. Over time, regulatory and customer pressure for resilience is expected to pull Tier III specifications closer to Tier IV, blurring distinctions and increasing the baseline spend per megawatt across the Singapore data center construction market.

The Singapore Data Center Construction Market is Segmented by Infrastructure (Electrical Infrastructure, Mechanical Infrastructure, and More), Tier Standard (Tier I and II, Tier III, and More), Data Center Type (Colocation, Hyperscale, and More), End User Industry (Banking, Financial Services, Insurance, IT and Telecommunications, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Boustead Projects

- Dragages Singapore (Bouygues)

- Takenaka Corp.

- Gammon Pte Ltd (Balfour Beatty)

- Sato Kogyo

- Kajima Overseas Asia

- Woh Hup (Private) Ltd

- China Construction (South Pacific) Dev.

- SsangYong Engineering and Construction

- Hyundai Engineering and Construction

- Obayashi Singapore

- Lendlease Singapore

- Keppel Data Centre Development

- ST Telemedia Global DC

- Equinix Construction Services

- Digital Realty (Digital Singapore)

- AIMS APAC REIT (DC builder arm)

- NTT Global DC Singapore

- M1 Net / Keppel DC and M1 JV

- AirTrunk (Blackstone)

- EdgeConneX

- Princeton Digital Group

- Microsoft (self-build campus)

- Amazon Web Services - Construction Ops

- Google Singapore DC Projects

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Power-allocation release under Green DC Roadmap (2024-)

- 4.2.2 Surge in AI / GPU-dense workloads requiring new build specs

- 4.2.3 Hyperscaler "Singapore-plus-Johor" twin-hub build strategies

- 4.2.4 Accelerating sovereign-cloud and MAS FSI localization rules

- 4.2.5 Investor appetite for DC-REIT conversions (Keppel DC, NTT DC REIT)

- 4.2.6 Modular prefabrication to compress build-times amid land caps

- 4.3 Market Restraints

- 4.3.1 Tight 300 MW annual power quota and moratorium legacy

- 4.3.2 Highest APAC construction cost US USD 11.7 m/MW and 19¢/kWh tariffs

- 4.3.3 Scarce brown-field plots; feasibility of underground / high-rise still unproven

- 4.3.4 Skilled MEP labour crunch inflating project timelines

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Key Singapore Data-Center Construction Statistics

- 4.8.1 Data Centers Total Installed Capacity (MW) in the Singapore , 2023 and 2024

- 4.8.2 Total IT Load Under Construction in the Singapore, MW, 2025 - 2030

- 4.8.3 Average Capex and Opex for the Singapore Data Center Construction

- 4.8.4 Top Capex Spenders on Data Center Infrastructure in the Singapore

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Infrastructure

- 5.1.1 Electrical Infrastructure

- 5.1.1.1 Power Distribution Solutions

- 5.1.1.1.1 Power Distribution Units

- 5.1.1.1.2 Switchgears

- 5.1.1.1.3 Others

- 5.1.1.2 Power Backup Solutions

- 5.1.1.2.1 UPS

- 5.1.1.2.2 Generators

- 5.1.1.1 Power Distribution Solutions

- 5.1.2 Mechanical Infrastructure

- 5.1.2.1 Cooling Systems

- 5.1.2.1.1 Liquid-based Cooling

- 5.1.2.1.2 Air-based Cooling

- 5.1.2.2 Racks and Cabinets

- 5.1.2.3 Other Mechanical Infrastructure

- 5.1.2.1 Cooling Systems

- 5.1.3 IT Infrastructure

- 5.1.3.1 Servers

- 5.1.3.2 Storage

- 5.1.3.3 Other IT Infrastructure

- 5.1.4 General Construction

- 5.1.5 Services

- 5.1.5.1 Design and Consulting

- 5.1.5.2 Integration

- 5.1.5.3 Support and Maintenance

- 5.1.1 Electrical Infrastructure

- 5.2 By Tier Standard

- 5.2.1 Tier I and II

- 5.2.2 Tier III

- 5.2.3 Tier IV

- 5.3 By End-User Industry

- 5.3.1 Banking, Financial Services and Insurance

- 5.3.2 IT and Telecommunications

- 5.3.3 Government and Defense

- 5.3.4 Healthcare

- 5.3.5 Other End Users

- 5.4 By Data Center Type

- 5.4.1 Colocation Facilities

- 5.4.2 Hyperscale / Self-built

- 5.4.3 Enterprise / Edge / Modular

6 COMPETITIVE LANDSCAPE

- 6.1 Market Share Analysis

- 6.2 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.2.1 Boustead Projects

- 6.2.2 Dragages Singapore (Bouygues)

- 6.2.3 Takenaka Corp.

- 6.2.4 Gammon Pte Ltd (Balfour Beatty)

- 6.2.5 Sato Kogyo

- 6.2.6 Kajima Overseas Asia

- 6.2.7 Woh Hup (Private) Ltd

- 6.2.8 China Construction (South Pacific) Dev.

- 6.2.9 SsangYong Engineering and Construction

- 6.2.10 Hyundai Engineering and Construction

- 6.2.11 Obayashi Singapore

- 6.2.12 Lendlease Singapore

- 6.2.13 Keppel Data Centre Development

- 6.2.14 ST Telemedia Global DC

- 6.2.15 Equinix Construction Services

- 6.2.16 Digital Realty (Digital Singapore)

- 6.2.17 AIMS APAC REIT (DC builder arm)

- 6.2.18 NTT Global DC Singapore

- 6.2.19 M1 Net / Keppel DC and M1 JV

- 6.2.20 AirTrunk (Blackstone)

- 6.2.21 EdgeConneX

- 6.2.22 Princeton Digital Group

- 6.2.23 Microsoft (self-build campus)

- 6.2.24 Amazon Web Services - Construction Ops

- 6.2.25 Google Singapore DC Projects

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

资料中心建置市场:依资料中心类型、建设形式、等级、组件、建设服务类型及最终用户产业划分-2026-2032年全球市场预测

资料中心建置市场:依资料中心类型、建设形式、等级、组件、建设服务类型及最终用户产业划分-2026-2032年全球市场预测 2026年全球资料中心建置市场报告

2026年全球资料中心建置市场报告 全球资料中心建设市场规模、份额、趋势和成长分析报告(2026-2034)

全球资料中心建设市场规模、份额、趋势和成长分析报告(2026-2034) 资料中心建置市场分析及预测(至2035年):类型、产品、服务、技术、组件、应用、材料类型、部署模式、最终用户、设备

资料中心建置市场分析及预测(至2035年):类型、产品、服务、技术、组件、应用、材料类型、部署模式、最终用户、设备 资料中心建置市场规模、份额和趋势分析报告:按基础设施、层级、最终用途、地区和细分市场预测(2026-2033 年)

资料中心建置市场规模、份额和趋势分析报告:按基础设施、层级、最终用途、地区和细分市场预测(2026-2033 年) 2026-2030年全球资料中心建置市场

2026-2030年全球资料中心建置市场 资料中心建置市场报告:按建设类型、资料中心类型、等级标准、产业垂直领域和地区划分(2026-2034 年)

资料中心建置市场报告:按建设类型、资料中心类型、等级标准、产业垂直领域和地区划分(2026-2034 年) 资料中心建置市场-全球产业规模、份额、趋势、机会及预测(依基础设施类型、层级、资料中心规模、最终用户产业、地区及竞争格局划分,2021-2031)资料中心机械设备建置市场(依组件类型、液冷系统、建置类型、等级及计划类型划分)-2026-2032年全球预测

资料中心建置市场-全球产业规模、份额、趋势、机会及预测(依基础设施类型、层级、资料中心规模、最终用户产业、地区及竞争格局划分,2021-2031)资料中心机械设备建置市场(依组件类型、液冷系统、建置类型、等级及计划类型划分)-2026-2032年全球预测 拉丁美洲资料中心建置:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)

拉丁美洲资料中心建置:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)