|

市场调查报告书

商品编码

1937337

生物炭:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Biochar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

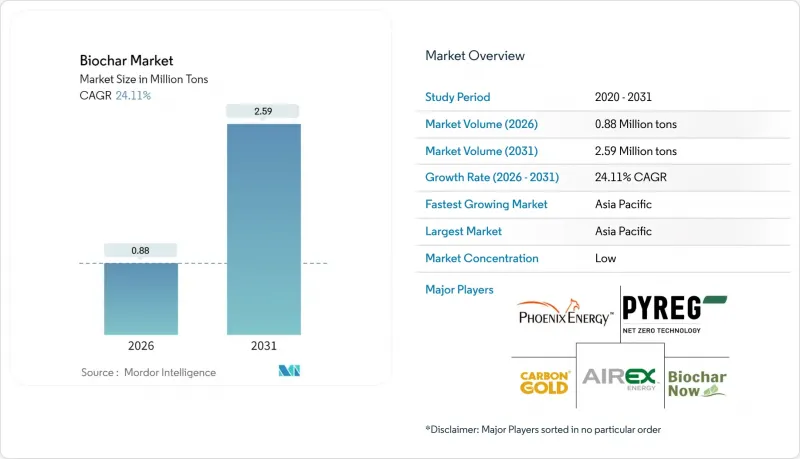

预计到 2026 年,生物炭市场规模将达到 88 万吨,高于 2025 年的 71 万吨,预计到 2031 年将达到 259 万吨。

预计从 2026 年到 2031 年,其复合年增长率将达到 24.11%。

快速规模化生产与气候政策支持、对负排放技术的需求以及农业恢復土壤健康面临的日益增长的压力密切相关。排碳权、不断扩大的工业应用案例以及单位成本降低技术的进步正在拓展收入来源并提高计划资金筹措,尤其是在拥有明确碳移除通讯协定的地区。亚太地区目前约占生物炭市场40.26%的份额,北美和欧盟强有力的政府奖励正在推动新增产能的扩张。原料多样化,从高成本的木质生物质转向农业残余物,正在缓解长期存在的供应限制。同时,分散式热解装置的引入缩短了物流距离并减少了范围3排放,从而增强了生物炭的气候友善特性。

全球生物炭市场趋势及展望

来自有机和再生农业的需求不断增长

为了获得优质认证所需的高土壤有机碳含量,有机农户正以生物炭取代合成投入品。美国已有20个州实施了NRCS土壤碳改良808标准,该标准为检验的生物炭施用提供补助。产量试验表明,第一年产量可提高约9%,六个种植季后累积增幅超过20%,尤其是在养分匮乏的土壤中。源自未经加工生物质的生物炭已获准用于美国农业部认证的有机系统,这项放鬆管制措施消除了关键的市场壁垒,并有助于提高价格。生物炭的「级联」概念——先将其用作过滤材料或牲畜垫料,然后再将其还田——实现了收入来源多元化,并符合循环经济的理念。由于投入品价格持续波动,农民将生物炭视为一种对冲工具,以确保养分供应稳定和长期碳信用。

政府对负碳材料和废弃物资源化利用的激励措施

政策槓桿正在刺激需求。 《通货膨胀控制法案》扩大了第45Q和45V条税额扣抵,将碳利用途径纳入其中,允许合格的生物炭生产企业在向美国国税局提交生命週期分析后申请可兑换的碳排放权证书。同时,欧盟委员会的碳移除认证框架正在製定专门针对生物炭的量化规则,这将规范永久性证明,并有可能吸引机构资本。包括华盛顿州在内的几个美国州根据《清洁空气法案》修正案将火焰覆盖窑合法化,从而实现了分散式生产模式,减少了物料运输距离。这些激励措施降低了合规风险,提高了偿债率,并鼓励私人投资者参与大型计划。

高昂的生产和物流成本

原料采购、预处理和热解解转换是重要的成本驱动因素,使得单位经济效益难以实现。学术成本曲线估计,生物炭的完全生产成本在每吨106美元至170美元之间,具体金额取决于水分含量、工厂规模和当地能源价格。由于生物炭的堆积密度低,一个40英尺货柜能装的生物炭吨数远少于合成肥料,这推高了长途运输的每吨运费。生产商可以选择使用跟随原料来源的移动热解装置,或建造铁路连接的枢纽以提高物流效率,但这两种策略都需要小规模业者难以资金筹措的资本支出。只有等到自动化、高通量工厂普及后,规模经济才能缓慢显现。

细分市场分析

慢速/中速热解系统凭藉其稳定的产量、灵活的原料范围以及包含生质油和合成气在内的产品组合,预计到2025年将占据生物炭市场44.72%的份额。这些优势使得营运商除了核心的生物炭销售收入外,还能获得电力和热能收益,进而提高计划的整体内部报酬率(IRR)。虽然大型设施主要采用资本密集的迴转窑设计,但小规模蒸馏系统正被应用于旨在促进再生农业的农场计画。连续进料反应器的日益普及提高了製程控制水平,从而实现了更稳定的产量和更严格的排放气体管理,有助于在空气品质敏感地区获得许可。

由于无需昂贵的预干燥即可处理高水分基材,替代工艺正日益受到关注。水热碳化在180至260°C的温度范围内运作,可将污水污泥转化为富碳水炭,适用于土壤改良和能源应用。气化系统虽然炭产率较低,但易于与热电联产模组集成,使市政废弃物管理人员能够将废弃物转化为基本负载电力和炭产品。一个日德联合研发机构正在进行微波辅助热解的初步试验,该技术有望提高能源效率并缩短停留时间,从而缩小与现有热化学处理方法的成本差距。这些新兴系统预计在预测期内将以24.63%的复合年增长率成长,逐步削弱热解技术的主导地位,并随着新型原料类别的引入,推动生物炭市场整体规模的扩大。

到2025年,木质生物质将占总量的61.15%,这得益于其可靠的林业剩余物来源、均匀的粒径以及可预测的木炭质量的化学成分。不列颠哥伦比亚省和斯堪地那维亚的纳维亚半岛等木材资源丰富的地区已实施疏伐计划以降低野火风险,从而持续供应低价值的剩余物,生物炭工厂可以透过多年合约获得这些剩余物。软木部分木质素含量高,有助于提高碳固定率,而碳信用审核认为这项指标在永久性计算中至关重要。

随着玉米秸秆、稻壳和甘蔗渣进入商业供应协议,竞争格局正在改变。移动式热解和碳化装置已证明在源头转化散装残渣的物流可行性,避免了高成本的打包运输。预计到2031年,农业残渣的复合年增长率将达到25.05%,因为废弃物焚化禁令和掩埋税促使经济模式转向高附加价值处理。污水污泥和牲畜粪便可提供营养丰富的最终产品,但必须符合欧洲化肥法规中更严格的污染物标准。巴西和印度的大都会圈正在探索公私合营,将污水处理、可再生能源和生物炭信用销售相结合,这预示着生物炭市场的原料组合正在扩大。

生物炭市场报告按技术(热解、气化系统等)、原料(木质生物质、农业残余物等)、形态(粉末、颗粒/球粒、液体悬浮液)、应用(农业、畜牧业等)和地区(亚太地区、北美、欧洲、南美、中东和非洲)进行细分。市场预测以吨为单位。

区域分析

亚太地区拥有丰富的生物质资源、新兴的碳去除目标以及雄厚的公共研发资金,预计2025年将占全球生物炭出货量的39.88%。仅中国每年就发表200多篇经同行评审的生物炭论文,展现了主导在反应器设计、农艺试验和排碳权通讯协定开发方面的领先地位。地方政府的补贴降低了农村地区热解装置的建造成本,使小规模的市镇能够将农作物残渣转化为符合国家土壤修復目标的产品。

北美碳排放总量位居第二,但在商业性碳信用交易方面领先。一些备受瞩目的企业销售协议,例如微软与其位于太平洋西北地区的工厂签订的多年期采购协议(采购量为9.5万吨二氧化碳当量),提供了可预测的收入来源,并降低了债务融资风险。联邦政府的激励措施,从生产税额扣抵到美国农业部的成本分摊津贴,进一步鼓励了工厂层级的投资。虽然成熟的法规结构将加速碳排放的普及,但由于领先采用者已经获得了大部分现成的原料,预计北美碳排放的成长速度将低于新兴亚洲地区。

在欧洲,围绕着品质标准和政策一致性正在形成丛集。欧盟拟议的碳移除检验条例将鼓励成员国协调调查方法,并促进跨境碳移除额度交易。面临严峻国内净零排放期限的斯堪地那维亚国家正在试点区域供热合作项目,该项目利用废木材热解提供热能和高碳生物炭。同时,拉丁美洲和撒哈拉以南非洲地区拥有丰富的农业残余物,具备长期成长潜力,但资金筹措和基础建设却落后。发展金融机构正在试行混合资本基金,以开拓这些新兴市场,并有望在2028年以后为全球生物炭市场带来显着的增量。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 来自有机和再生农业的需求不断增长

- 政府对负碳材料和废弃物回收提供奖励

- 土壤碳封存计划中排碳权的货币化

- 扩大园艺和温室种植

- 用于绿建筑的生物炭增强沥青混凝土

- 市场限制

- 高昂的生产和物流成本

- 低成本替代品的可用性

- 化肥登记方面的监理模糊性

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 透过技术

- 热解

- 气化系统

- 其他技术(水热碳化)

- 按原料

- 木质生物质

- 农业残余物

- 牲畜粪便

- 污水污泥和有机废弃物

- 按形式

- 粉末

- 颗粒/粒状物

- 液体悬浮液

- 透过使用

- 农业

- 畜牧业

- 产业

- 其他用途(建筑材料、能源等)

- 按地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 东南亚国协

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧国家

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Airex Energy

- Applied Carbon

- Arsta Eco

- Biochar Now LLC

- BIOSORRA

- Black Owl Biochar.

- Carbofex Ltd.

- Carbon Gold Ltd

- CharGrow

- Karr Group

- Myno Carbon

- Pacific Biochar Benefit Corporation

- Phoenix Energy

- Pyreg GmbH

- Standard Bio AS

- Swiss Biochar GmbH

- Wakefield Biochar

- Wonjin Group

第七章 市场机会与未来展望

Biochar market size in 2026 is estimated at 0.88 Million tons, growing from 2025 value of 0.71 Million tons with 2031 projections showing 2.59 Million tons, growing at 24.11% CAGR over 2026-2031.

Rapid scale-up is tied to supportive climate policies, the need for negative-emission technologies, and mounting pressure on agriculture to restore soil health. Premium carbon-credit pricing, a widening set of industrial use-cases, and technology advances that cut unit costs are expanding revenue streams and improving project bankability, especially in regions with clear carbon-removal protocols. Asia-Pacific leads today's biochar market with an estimated 40.26% volume share, while robust government incentives in North America and the European Union encourage new capacity additions. Feedstock diversification away from high-cost woody biomass toward agricultural residues is easing long-standing supply constraints. At the same time, distributed pyrolysis units are shrinking logistics distances and lowering scope-3 emissions, reinforcing biochar's climate credentials.

Global Biochar Market Trends and Insights

Rising Demand from Organic and Regenerative Farming

Organic farmers are replacing synthetic inputs with biochar as they chase higher soil-organic-carbon scores required for premium certification. Twenty US states have already activated the NRCS Soil Carbon Amendment 808 standard, which reimburses growers for verified biochar applications. Yield trials show first-year productivity gains near 9% and cumulative boosts that exceed 20% after six seasons, especially in nutrient-poor soils. Biochar qualifies for use in USDA-certified organic systems when sourced from untreated biomass, a rule that removes a major market barrier and supports premium pricing. The cascading-use concept-deploying biochar first in filtration or livestock bedding and later reincorporating it into fields-multiplies income streams and aligns with circular-economy mandates. As input prices remain volatile, growers view biochar as a hedge that locks in stable nutrient supply and long-term carbon credits.

Government Incentives for Negative-Carbon Materials and Waste Valorization

Policy levers are accelerating demand. The Inflation Reduction Act broadened Section 45Q and 45V tax credits to include carbon-utilisation pathways, letting qualified biochar facilities claim monetisable certificates once lifecycle analyses are filed with the IRS. In parallel, the European Commission's Carbon Removal Certification Framework is drafting biochar-specific quantification rules that should standardise permanence proofs and attract institutional capital. Several US states, notably Washington, have legalised flame-cap kilns under updated clean-air codes, clearing the way for distributed production models that shorten feedstock haulage. These incentives lower compliance risk and improve debt-service coverage ratios, nudging private investors toward large-scale projects.

High Production and Logistics Costs

Unit economics remain challenging because feedstock, preprocessing, and thermal conversion each add sizeable cost blocks. Academic cost curves place fully-loaded production between USD 106 and USD 170 per ton depending on moisture content, plant scale, and regional energy tariffs. Low bulk density means a 40-foot container carries far fewer tonnes of biochar than of synthetic fertiliser, inflating per-tonne freight costs on long-haul routes. Producers either adopt mobile pyrolysis units that follow feedstock sources or build rail-linked hubs to capture logistics efficiencies, yet both strategies demand capital outlays that small operators struggle to finance. Until automated, high-throughput plants gain traction, scale economies will arrive slowly.

Other drivers and restraints analyzed in the detailed report include:

- Carbon-Credit Monetisation for Soil Sequestration Projects

- Expanding Horticulture and Greenhouse Adoption

- Availability of Low-Cost Substitutes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Slow and intermediate pyrolysis systems held 44.72% of biochar market share in 2025 thanks to reliable throughput, flexible feedstock windows, and a coproduct slate that includes bio-oil and syngas. These attributes let operators layer electricity or heat revenue onto core biochar sales, raising overall project internal-rate-of-return figures. Capital-intensive rotary-kiln designs dominate high-volume installations, while smaller retort units serve on-farm programmes that target regenerative agriculture. The wider diffusion of continuous-feed reactors has triggered process-control improvements, enabling better yield consistency and tighter emissions control, an aspect that simplifies permitting in air-quality-sensitive regions.

Alternative routes are gaining mindshare because they process high-moisture substrates without costly pre-drying. Hydrothermal carbonisation runs at 180-260 °C and converts sewage sludge into carbon-rich hydrochar suitable for soil amendment or energy applications. Gasification systems, though producing lower char yields, integrate readily with combined-heat-and-power modules, allowing municipal waste managers to transform refuse into baseload electricity and char by-products. R&D consortia in Japan and Germany are piloting microwave-assisted pyrolysis that promises higher energy efficiency and reduced residence times, innovations that could narrow cost gaps against incumbent thermochemical options. Over the forecast window, these emerging systems are anticipated to grow at a 24.63% CAGR, gradually diluting pyrolysis dominance yet collectively lifting the biochar market size as new feedstock classes come online.

Woody biomass provided 61.15% of total volume in 2025 due to reliable forestry residues, uniform particle sizes, and chemical compositions that yield predictable char quality. Timber-rich geographies such as British Columbia and Scandinavia run dedicated thinning programmes to mitigate wildfire risk, generating a continuous stream of low-value residues that biochar plants can secure on multi-year contracts. High lignin content in conifer fractions also enhances fixed-carbon percentages, a metric prized by carbon-credit auditors for permanence calculations.

The competitive landscape is shifting as corn stover, rice husks, and sugarcane bagasse enter commercial supply agreements. Mobile torrefaction and pyrolysis rigs have demonstrated the logistical viability of converting loose residues where they are generated, bypassing costly bale transport. Agricultural residues are forecast to expand at 25.05% CAGR to 2031, helped by waste-burn bans and landfill taxes that tilt economics toward valorisation. Sewage sludge and animal manure offer nutrient-enriched end-products but must clear tighter contaminant hurdles under European fertiliser regulations. Large urban centres in Brazil and India are exploring public-private partnerships that marry wastewater treatment, renewable power, and biochar credit sales, pointing to an eventual broadening of feedstock portfolios across the biochar market.

The Biochar Market Report is Segmented by Technology (Pyrolysis, Gasification Systems, and More), Feedstock (Woody Biomass, Agricultural Residues, and More), Form (Powder, Pellets/Granules, and Liquid Suspension), Application (Agriculture, Animal Farming, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific captured 39.88% of global shipments in 2025, reflecting an abundant biomass resource base, emerging carbon-removal targets, and generous public R&D funding. China alone publishes over 200 peer-reviewed biochar papers each year, underpinning its leadership in reactor design, agronomic testing, and carbon-credit protocol development. Provincial subsidies lower the capital cost of rural pyrolysis units, enabling small municipalities to turn crop residues into products that meet national soil-restoration goals.

North America ranks second in volume but leads in commercial carbon-credit transactions. High-profile corporate offtake agreements, including Microsoft's multi-year procurement of 95,000 tCO2e from Pacific-Northwest facilities, provide predictable revenue tails that derisk debt financing. Federal incentives-ranging from production tax credits to USDA cost-share grants-further catalyse plant-level investment. Although the region's mature regulatory framework accelerates deployment, growth rates will moderate compared with emerging Asia because early movers have already secured a large share of easily accessible feedstocks.

Europe clusters around quality standards and policy alignment. Draft EU rules governing carbon-removal verification encourage member states to harmonise methodologies, facilitating cross-border trade in removal credits. Scandinavian countries, confronted with stringent national net-zero deadlines, are testing district-heating link-ups where waste-wood pyrolysis supplies both thermal energy and high-carbon biochar. Meanwhile, Latin America and Sub-Saharan Africa present long-term upside tied to abundant agricultural residues yet lag on financing and infrastructure. Development-finance institutions are piloting blended-capital funds that could unlock these frontier markets, potentially adding significant incremental tonnage to the global biochar market after 2028.

- Airex Energy

- Applied Carbon

- Arsta Eco

- Biochar Now LLC

- BIOSORRA

- Black Owl Biochar.

- Carbofex Ltd.

- Carbon Gold Ltd

- CharGrow

- Karr Group

- Myno Carbon

- Pacific Biochar Benefit Corporation

- Phoenix Energy

- Pyreg GmbH

- Standard Bio AS

- Swiss Biochar GmbH

- Wakefield Biochar

- Wonjin Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand from Organic and Regenerative Farming

- 4.2.2 Government Incentives for Negative-Carbon Materials and Waste Valorization

- 4.2.3 Carbon-Credit Monetisation for Soil Sequestration Projects

- 4.2.4 Expanding Horticulture and Greenhouse Adoption

- 4.2.5 Biochar-Enhanced Asphalt and Concrete for Green Construction

- 4.3 Market Restraints

- 4.3.1 High Production and Logistics Costs

- 4.3.2 Availability of Low-Cost Substitutes

- 4.3.3 Regulatory Ambiguity on Fertiliser Registration

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Technology

- 5.1.1 Pyrolysis

- 5.1.2 Gasification Systems

- 5.1.3 Other Technologies (Hydrothermal Carbonization)

- 5.2 By Feedstock

- 5.2.1 Woody Biomass

- 5.2.2 Agricultural Residues

- 5.2.3 Animal Manure

- 5.2.4 Sewage Sludge and Organic Waste

- 5.3 By Form

- 5.3.1 Powder

- 5.3.2 Pellets/Granules

- 5.3.3 Liquid Suspension

- 5.4 By Application

- 5.4.1 Agriculture

- 5.4.2 Animal Farming

- 5.4.3 Industrial Uses

- 5.4.4 Other Applications (Construction Materials, Energy, etc.)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Airex Energy

- 6.4.2 Applied Carbon

- 6.4.3 Arsta Eco

- 6.4.4 Biochar Now LLC

- 6.4.5 BIOSORRA

- 6.4.6 Black Owl Biochar.

- 6.4.7 Carbofex Ltd.

- 6.4.8 Carbon Gold Ltd

- 6.4.9 CharGrow

- 6.4.10 Karr Group

- 6.4.11 Myno Carbon

- 6.4.12 Pacific Biochar Benefit Corporation

- 6.4.13 Phoenix Energy

- 6.4.14 Pyreg GmbH

- 6.4.15 Standard Bio AS

- 6.4.16 Swiss Biochar GmbH

- 6.4.17 Wakefield Biochar

- 6.4.18 Wonjin Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

生物炭市场:2026-2032年全球市场预测(依製造技术、原料类型、产品形态、反应器配置、活化类型、应用、通路和最终用户划分)

生物炭市场:2026-2032年全球市场预测(依製造技术、原料类型、产品形态、反应器配置、活化类型、应用、通路和最终用户划分) 全球生物炭市场(2026-2036)

全球生物炭市场(2026-2036) 欧洲生物炭:市场占有率分析、产业趋势与统计、成长预测(2026-2031)全球生物炭市场规模、份额、趋势和成长分析报告(2026-2034年)全球生物炭市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034)

欧洲生物炭:市场占有率分析、产业趋势与统计、成长预测(2026-2031)全球生物炭市场规模、份额、趋势和成长分析报告(2026-2034年)全球生物炭市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034) 日本生物炭市场规模、份额、趋势及预测(按原料类型、技术类型、产品形式、应用和地区划分,2026-2034年)

日本生物炭市场规模、份额、趋势及预测(按原料类型、技术类型、产品形式、应用和地区划分,2026-2034年) 生物炭市场规模、份额和趋势分析报告:按技术、应用、地区和细分市场预测(2026-2033 年)

生物炭市场规模、份额和趋势分析报告:按技术、应用、地区和细分市场预测(2026-2033 年) 生物炭市场-全球产业规模、份额、趋势、机会及预测,依技术(热解、气化、其他)、应用(农业、工业、其他)、地区及竞争细分,2020-2030 年预测

生物炭市场-全球产业规模、份额、趋势、机会及预测,依技术(热解、气化、其他)、应用(农业、工业、其他)、地区及竞争细分,2020-2030 年预测 全球浓缩生物炭市场

全球浓缩生物炭市场 生物炭燃烧器市场按类型、技术和地区划分

生物炭燃烧器市场按类型、技术和地区划分