|

市场调查报告书

商品编码

1940861

欧洲生物炭:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Europe Biochar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

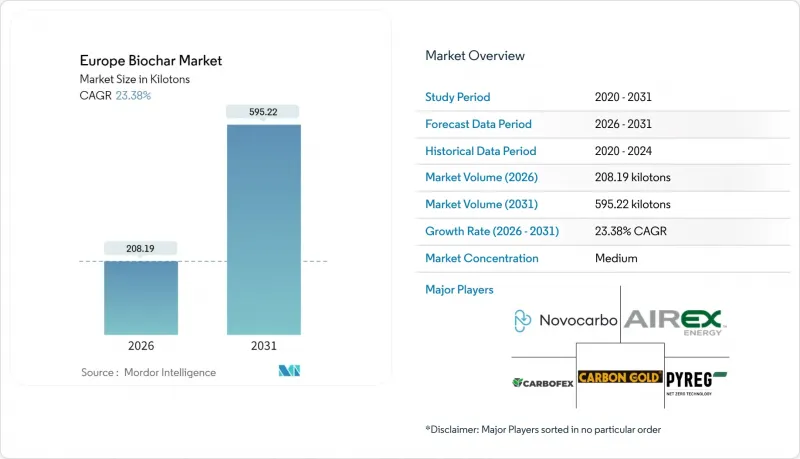

预计到 2026 年,欧洲生物炭市场规模将达到 208.19 千吨。

这意味着从 2025 年的 168.77 千吨增长到 2031 年的 595.22 千吨,2026 年至 2031 年的复合年增长率为 23.38%。

随着欧盟将生物炭指定为碳移除认证框架下的认可碳移除途径,以及《肥料产品法规》中的CMC14分类消除品质模糊性并允许跨境贸易,市场需求正在增长。从钢铁製造商到地方供水事业,工业买家纷纷签署多年期合同,以确保新增产能;投资者则将区域供热热解装置视为可同时产生热能和碳信用额的双重收益资产。德国以29.41%的市占率主导,这得益于其60多家商业化工厂、经认证的生产通讯协定以及与可再生供热网络的密切合作。然而,生物质物流分散以及缺乏欧盟范围内的农艺田间施用量指南阻碍了成本竞争力和农场应用,凸显了原料集约化和农业标准统一化的必要性。

欧洲生物炭市场趋势与洞察

欧盟27国可再生和有机农业计画需求激增

欧盟2023-2027年通用农业政策(CAP)下的生态计画对农民的碳封存措施(包括生物炭)进行补偿。荷兰温室种植者透过将精准施肥管理与生物炭结合,番茄产量提高了20%,从而促进了生物炭在高价值园艺领域的应用。在德国,经认证的生物炭正被应用于有机农田(占该国农田面积的10.20%),以实现净零排放目标并维持土壤肥力。政策与现有补贴计画的协调一致,稳定了生产者的收入,并减少了对波动较大的排碳权价格的依赖,从而促进了生物炭的稳定推广。随着成员国将农村发展预算分配给碳农业,欧洲生物炭市场正受益于主流农业计画带来的可预测需求。

碳信用购买协议的快速扩张

自2024年碳移除认证架构正式实施以来,生物炭信用额(以二氧化碳移除证书的形式发放)已在企业永续发展核算中获得标准化累计。北欧企业已签署多年期认证移除合同,为ECOERA等生产商提供了可靠的收入来源,以支持工厂扩张。第三方审核检验有机碳含量低于0.3,这不仅强化了永续性声明,也使其能够获得溢价,有时甚至达到农业木炭价格的两倍。企业需求的激增缩短了新热解能的投资回收期,吸引了机构资本进入欧洲生物炭市场,并促进了认证供应的成长。

欧盟生物质废弃物物流中断推高原料成本

由于生物炭原料网路采用分散的区域收集点而非统一的商品交易所运作,运输距离增加,导致交付德国工厂的生物质价格上涨25%至40%。小规模生产商缺乏谈判规模来签订长期合同,往往依赖现货采购,使其营运利润易受价格波动的影响。与颗粒燃料产业不同,生物炭原料没有统一的分级或水分含量标准,这使得原料在成员国之间运输时,品质检验变得更加复杂。投资建设集中式收集站和数位化溯源平台可以降低物流成本,但此类基础设施需要跨国政策协调,而这方面的工作才刚起步。

细分市场分析

2025年,热解占据欧洲生物炭市场74.32%的份额,预计到2031年将以23.88%的复合年增长率增长,这主要得益于连续流反应器、自动温度控制和合成气回收技术带来的成本降低。热解法之所以占据主导地位,是因为它能够处理木材残渣、农作物秸秆和污水污泥等多种原料,同时满足CMC14污染物排放标准。气化法主要针对高水分原料,占小规模的市场份额,而热解和水热碳化法则为活性碳市场提供特殊煤。

设施的经济效益越来越依赖能源的综合利用。例如,萨克森州和斯科讷省的联合热解和区域供热厂,其运作热成本为负,并可将节省的资金用于原料预处理,从而提高整体碳产量。自动化取样和在线连续光谱分析降低了批次间的差异,这是实现工业买家所需的窄孔径分布的关键因素。这些製程优势巩固了德国设备供应商的高端品牌价值,并强化了热解作为拓展欧洲生物炭市场基石的地位。

欧洲生物炭市场报告按技术(热解、气化系统、其他技术)、应用(农业、畜牧业、工业应用、其他应用)和地区(德国、英国、法国、义大利、西班牙、北欧国家、土耳其、俄罗斯、欧洲其他地区)进行细分。市场预测以吨为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 欧盟27国再生农业和有机农业计画需求激增

- 碳信用购买协议的快速扩张

- 欧盟肥料产品法规中CMC14生物炭的适用范围

- 区域供热热解装置中工业余热回收的经济性。

- 利用生物炭从污水污泥中回收磷

- 市场限制

- 欧盟内部生物质废弃物分销网络的碎片化将推高原料成本。

- 欧盟范围内缺乏生物炭施用量的统一农艺指南

- 未经认证的木炭可能有长期多环芳烃/重金属污染风险

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 科技

- 热解

- 气化系统

- 其他技术

- 目的

- 农业

- 畜牧业

- 工业用途

- 其他用途

- 地区

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 土耳其

- 俄罗斯

- 其他欧洲地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Airex Energy

- Bussme Energy AB

- Carbofex Ltd

- Carbon Centric

- Carbon Finland Oy

- Carbon Gold Ltd

- CARBUNA

- CharLine GmbH

- Circular Carbon GmbH

- EGoS GmbH

- EOC Energy Ocean

- LUCRAT GmbH

- Nettenergy BV

- NOVOCARBO GMBH

- PYREG GmbH

- Sonnenerde GmbH

- Verora AG

第七章 市场机会与未来展望

Europe Biochar Market size in 2026 is estimated at 208.19 kilotons, growing from 2025 value of 168.77 kilotons with 2031 projections showing 595.22 kilotons, growing at 23.38% CAGR over 2026-2031.

Demand rises as the European Union positions biochar as an accredited carbon-removal pathway under the Carbon Removal Certification Framework, while the CMC14 classification inside the Fertilising Products Regulation removes quality ambiguity and opens cross-border trade. Industrial buyers-from steel producers to municipal water utilities-are entering multi-year offtake contracts that underwrite new capacity, and investors view district-heating pyrolysis plants as dual-revenue assets that monetize heat and carbon credits. Germany leads with a 29.41% volume share thanks to more than 60 commercial plants, certified production protocols and close integration with renewable-heat networks. However, fragmented biomass logistics and the absence of pan-EU agronomic field-rate guidelines weigh on cost competitiveness and farm adoption, underscoring the need for tighter feedstock aggregation and harmonized agricultural standards.

Europe Biochar Market Trends and Insights

Soaring Demand from EU-27 Regenerative & Organic Farming Programs

European Union eco-schemes inside the 2023-2027 Common Agricultural Policy reimburse farmers for carbon-sequestration practices, and biochar now qualifies for these payments. Dutch greenhouse growers recorded yield gains of up to 20% in tomato production after integrating biochar with precision fertigation, prompting wider adoption across high-value horticulture. Germany's organic acreage-10.20% of national farmland-has embraced certified biochar to maintain soil fertility while meeting net-zero targets. The policy linkage to existing subsidy channels harmonizes revenue for growers and lessens exposure to volatile carbon-credit pricing, accelerating steady volume uptake. As member states earmark rural-development budgets for carbon farming, the Europe biochar market receives predictable pull-through from mainstream agricultural programs.

Rapid Scale-up of Carbon-Credit Purchase Agreements

Since the Carbon Removal Certification Framework became operational in 2024, biochar credits-issued as CO2 Removal Certificates-have gained standardized accounting across corporate sustainability ledgers. Nordic corporates are contracting multiyear tranches of certified removals, giving producers like ECOERA firm revenue visibility that supports plant expansions. Third-party audits that verify H/C_org ratios below 0.3 reinforce permanence claims and enable premium pricing often double that of agricultural-grade char. The surge in corporate demand accelerates payback periods on new pyrolysis assets, drawing institutional capital into the Europe biochar market and lifting credentialed volumes.

Fragmented EU Biomass-Waste Logistics Inflate Feedstock Costs

Biochar feedstock networks operate through decentralized, regional collection hubs instead of unified commodity exchanges, resulting in transport distances that lift delivered biomass prices by 25-40% for German plants. Smaller producers lack the bargaining scale to secure long-term contracts and often rely on spot sourcing, injecting price volatility into operating margins. Unlike the pellet sector, there is no uniform grading or moisture-content standard recognized across borders, complicating quality checks when material moves between member states. Investment in centralized aggregation depots and digital traceability platforms could compress logistics costs, but such infrastructure requires cross-border policy coordination that remains nascent.

Other drivers and restraints analyzed in the detailed report include:

- EU Fertilising Products Regulation Inclusion of CMC14 Biochar

- Industrial Heat-Recovery Economics from District-Heating Pyrolysis Plants

- Absence of Pan-EU Agronomic Guidelines for Biochar Field-Rates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pyrolysis accounted for 74.32% of the Europe biochar market share in 2025, and the pathway is on track for a 23.88% CAGR through 2031 as continuous-flow reactors, automated temperature control, and syngas recovery underpin cost reductions. This dominance stems from the technology's versatility to process wood residuals, crop straw, and sewage sludge while still meeting CMC14 contaminant thresholds. Gasification claims a smaller niche for high-moisture feedstocks, whereas torrefaction and hydrothermal carbonization supply specialty chars for activated-carbon markets.

Unit economics increasingly hinge on integrated energy use. Plants that couple pyrolysis with district-heating, such as facilities in Saxony and Skane, achieve negative operating heat costs and channel savings into feedstock pre-processing, improving overall carbon yields. Automated sampling and inline spectrometry reduce batch-to-batch variability, an essential factor as industrial buyers specify narrow pore-size distributions. These process gains reinforce the premium branding of German equipment suppliers and cement pyrolysis as the backbone of Europe biochar market expansion.

The Europe Biochar Market Report is Segmented by Technology (Pyrolysis, Gasification Systems, Other Technologies), Application (Agriculture, Animal Farming, Industrial Uses, Other Applications), and Geography (Germany, United Kingdom, France, Italy, Spain, Nordic Countries, Turkey, Russia, Rest of Europe). The Market Forecasts are Provided in Terms of Volume (Tons).

List of Companies Covered in this Report:

- Airex Energy

- Bussme Energy AB

- Carbofex Ltd

- Carbon Centric

- Carbon Finland Oy

- Carbon Gold Ltd

- CARBUNA

- CharLine GmbH

- Circular Carbon GmbH

- EGoS GmbH

- EOC Energy Ocean

- LUCRAT GmbH

- Nettenergy BV

- NOVOCARBO GMBH

- PYREG GmbH

- Sonnenerde GmbH

- Verora AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Soaring demand from EU-27 regenerative and organic farming programmes

- 4.2.2 Rapid scale-up of carbon-credit purchase agreements

- 4.2.3 EU Fertilising Products Regulation inclusion of CMC14 biochar

- 4.2.4 Industrial heat-recovery economics from district-heating pyrolysis plants

- 4.2.5 Biochar-enabled phosphorus recycling from sewage-sludge streams

- 4.3 Market Restraints

- 4.3.1 Fragmented EU biomass-waste logistics inflate feedstock costs

- 4.3.2 Absence of pan-EU agronomic guidelines for biochar field-rates

- 4.3.3 Potential long-term PAH / heavy-metal liability for non-certified char

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 Technology

- 5.1.1 Pyrolysis

- 5.1.2 Gasification Systems

- 5.1.3 Other Technologies

- 5.2 Application

- 5.2.1 Agriculture

- 5.2.2 Animal Farming

- 5.2.3 Industrial Uses

- 5.2.4 Other Applications

- 5.3 Geography

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 France

- 5.3.4 Italy

- 5.3.5 Spain

- 5.3.6 Nordic Countries

- 5.3.7 Turkey

- 5.3.8 Russia

- 5.3.9 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)**/Ranking Analysis

- 6.4 Company Profiles (includes Global-Level Overview, Market-Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Airex Energy

- 6.4.2 Bussme Energy AB

- 6.4.3 Carbofex Ltd

- 6.4.4 Carbon Centric

- 6.4.5 Carbon Finland Oy

- 6.4.6 Carbon Gold Ltd

- 6.4.7 CARBUNA

- 6.4.8 CharLine GmbH

- 6.4.9 Circular Carbon GmbH

- 6.4.10 EGoS GmbH

- 6.4.11 EOC Energy Ocean

- 6.4.12 LUCRAT GmbH

- 6.4.13 Nettenergy BV

- 6.4.14 NOVOCARBO GMBH

- 6.4.15 PYREG GmbH

- 6.4.16 Sonnenerde GmbH

- 6.4.17 Verora AG

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

生物炭市场:2026-2032年全球市场预测(依製造技术、原料类型、产品形态、反应器配置、活化类型、应用、通路和最终用户划分)

生物炭市场:2026-2032年全球市场预测(依製造技术、原料类型、产品形态、反应器配置、活化类型、应用、通路和最终用户划分) 全球生物炭市场(2026-2036)

全球生物炭市场(2026-2036) 生物炭:市场占有率分析、产业趋势与统计、成长预测(2026-2031)全球生物炭市场规模、份额、趋势和成长分析报告(2026-2034年)全球生物炭市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034)

生物炭:市场占有率分析、产业趋势与统计、成长预测(2026-2031)全球生物炭市场规模、份额、趋势和成长分析报告(2026-2034年)全球生物炭市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034) 日本生物炭市场规模、份额、趋势及预测(按原料类型、技术类型、产品形式、应用和地区划分,2026-2034年)

日本生物炭市场规模、份额、趋势及预测(按原料类型、技术类型、产品形式、应用和地区划分,2026-2034年) 生物炭市场规模、份额和趋势分析报告:按技术、应用、地区和细分市场预测(2026-2033 年)

生物炭市场规模、份额和趋势分析报告:按技术、应用、地区和细分市场预测(2026-2033 年) 生物炭市场-全球产业规模、份额、趋势、机会及预测,依技术(热解、气化、其他)、应用(农业、工业、其他)、地区及竞争细分,2020-2030 年预测

生物炭市场-全球产业规模、份额、趋势、机会及预测,依技术(热解、气化、其他)、应用(农业、工业、其他)、地区及竞争细分,2020-2030 年预测 全球浓缩生物炭市场

全球浓缩生物炭市场 生物炭燃烧器市场按类型、技术和地区划分

生物炭燃烧器市场按类型、技术和地区划分