|

市场调查报告书

商品编码

1937409

建筑幕墙:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Facade - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

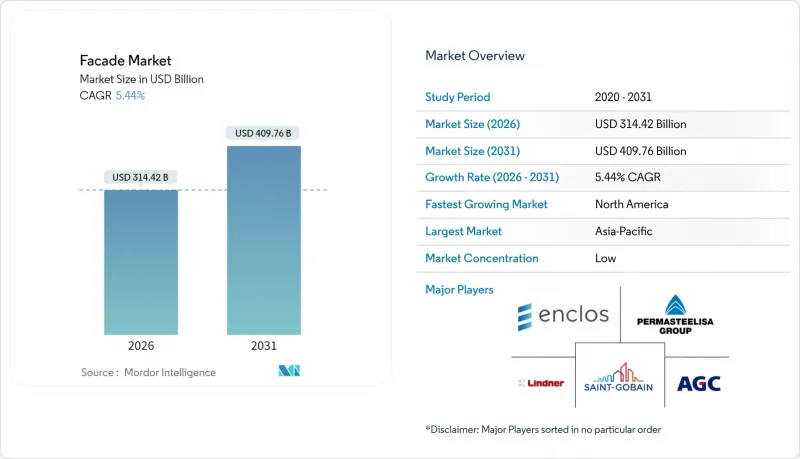

2025年,建筑幕墙市场价值为2,982亿美元,预计到2031年将达到4,097.6亿美元,而2026年为3,144.2亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 5.44%。

这一成长轨迹反映了强劲的需求,而这种需求的驱动力来自于建筑一体化太阳能光电系统、智慧外围结构控制系统和单元式帷幕墙的广泛应用。亚太地区将在2024年引领营收成长,其中中东和非洲地区的成长速度最快。随着高层建筑开发商将热性能放在首位,通风系统将继续保持其设计优势;即使在更严格的能源标准下住宅维修加速进行,商业建筑仍将是重要的收入来源。

圣戈班在2024年的一系列收购后,产业整合的压力增加,但整体供应结构仍分散,区域性专业公司和全球集团并存。铝价波动和日益严格的消防法规持续挤压计划利润率,但符合规范的建筑幕墙可享受保险折扣,以及光伏建筑一体化(BIPV)成本下降,维持了投资势头。

全球建筑幕墙市场趋势与洞察

亚太和中东地区的高层建筑热潮

中国、印度和海湾地区高层建筑的激增,对建筑性能提出了更高的要求,使得建筑幕墙不再只是装饰性的外立面,而是核心基础设施组成部分。预计到2023年,全球将有超过176栋200公尺以上的摩天大楼竣工,而未来的建设计画也十分强劲,这主要得益于沙乌地阿拉伯的穆卡布大厦和中国的黄金金融117大厦等大型企划的推动。模组化异地组装技术正在缩短关键路径时间,例如,一座26层高的塔楼仅用五天就建成。因此,开发商正在寻求供应商提供工厂预製的多功能建筑幕墙,将结构支撑、能源产出和数位监控等功能整合到单一的围护结构解决方案中。

更严格的节能建筑标准

世界各国政府正将脱碳目标转化为严格的建筑外围护结构法规,并要求建筑商实现净零排放。日本2025年的法规强制要求中型新建建筑安装太阳能光电发电系统,而美国暖气、冷气与空调工程师协会(ASHRAE)90.1-2022标准则将美国的能源效率标准提高了9.8%。加州第24号法规和纽约市的地方法规鼓励在资本週期内对建筑幕墙维修,并对性能缺陷处以罚款。通风层、动态遮阳和低U值玻璃的补贴计画正在推动对先进建筑外围护结构的需求,尤其是在消防安全和能源效率法规重迭的地区。

铝和玻璃价格波动

预计到2025年初,铝价将达到每吨2,763美元,这将导致成本上涨10%,并挤压采用固定竞标合约计划的利润空间。地缘政治紧张局势和高能源价格限制了冶炼厂的产量,而汽车和可再生能源产业的需求则加剧了供应紧张。流动资金有限的小规模建筑幕墙承包商难以对冲风险,这加速了产业向拥有商品风险管理计画的垂直整合供应商的整合。

细分市场分析

到2025年,通风建筑幕墙将占市场收入的51.65%,透过自然对流将空调负载降低高达25%,从而为满足建筑规范要求提供了清晰的途径。随着连续空气层和防雨功能在炎热潮湿地区的高层计划中变得日益重要,预计到2031年,通风建筑幕墙设计的市场规模将以5.48%的复合年增长率增长。新兴的物联网风门可即时调整空腔内的气流,进而提高能源效率并延长帷幕墙的使用寿命。虽然在气候温暖的市场中,为了降低建造成本,仍会采用非通风帷幕墙,但更严格的碳排放法规正推动兼顾成本和性能的混合空腔建筑幕墙进入经济型市场。

对于低层住宅和仓库项目而言,非通风结构仍然很受欢迎,因为在这些项目中,建筑表现力比隔热性能更为重要。製造商提供纹理丰富的覆层、再生复合复合材料和简化的紧固系统,显着缩短了此类专案的安装週期。混合建筑幕墙正被应用于多功能塔楼,将阳光照射面上的通风结构与阴凉面上的经济型覆层结合。这种选择性方法既能优化计划整体预算,又能满足建筑设计意图。

到2025年,帷幕墙将占总需求的43.58%,其中单元式帷幕墙产品将以5.52%的复合年增长率增长,这主要得益于开发商对施工进度确定性的追求。由于组合式框架面临熟练劳动力短缺的问题,工厂预涂漆建筑幕墙目前在高层建筑计划占据主导地位。帷幕墙的防火性能以及在製造过程中易于整合光伏建筑一体化(BIPV)组件,进一步巩固了其市场份额。物流中心和资料中心越来越重视可靠的防风雨性能而非极致的透明度,促使雨幕式帷幕墙系统日益普及。

先进的幕墙组件包括电致变色玻璃、整合遮阳鳍片以及可连接楼宇管理系统的感测器套件。在发生多起备受瞩目的外墙火灾后,保险公司也更倾向于选择经过验证的帷幕墙结构,因此其保费低于实验性替代方案。儘管雨幕供应商已采用矿物纤维芯材和不燃百叶片等技术进行改良以保持竞争力,但幕墙仍然是豪华高层建筑性能的标竿。

区域分析

亚太地区将在建筑幕墙市场中主导,无论从价值或销售来看,预计到2025年将占全球销售额的39.58%。中国和印度的大型企划,以及日本针对中型建筑的光伏一体化(BIPV)法规,使得工厂使用率接近满载运转。国内玻璃和铝材生产商已稳定了供应链,但区域性城市仍面临熟练安装人员短缺的问题。开发商正从欧洲进口专用锚固件和智慧嵌装玻璃,以满足高端规格要求。

预计到2031年,中东和非洲地区的建筑业将以6.18%的复合年增长率增长,这主要得益于沙乌地阿拉伯的NEOM、The Line和Mukab项目,以及杜拜和多哈的高层建筑开发项目。严酷的沙漠气候促使人们采用透气建筑幕墙和电致变色玻璃来降低冷气负荷。当地製造商正透过从欧洲幕墙专家那里获得技术许可来扩大规模,而各国政府也在鼓励在地采购以支持经济多元化。

在欧洲,维修、日益严格的消防安全标准以及製造业的碳排放管理正在推动建筑幕墙需求。德国在建筑一体化光伏(BIPV)幕墙创新方面处于领先地位,而法国则引入了能源性能证书(EPC)以强调建筑幕墙的能源效率。在英国,格伦费尔大楼火灾后收紧的法规增加了对符合A2-s1-d0标准的材料的需求,并逐步淘汰不符合标准的覆层材料。为了应对严寒的冬季,北欧国家优先考虑隔热框架和三层玻璃窗,这反映了不同气候条件下的多样化需求。

在北美,重点在于老旧办公大楼和大学校园的维修。加州、纽约州和马萨诸塞州日益严格的能源法规推动了智慧玻璃和蒸气控制系统的改进。劳动力短缺促使承包商转向单元式系统,从而推动了国内投资,例如YKK AP在乔治亚投资1.25亿美元扩建工厂。拉丁美洲市场虽然规模较小,但在沿海城市正稳定成长,因为抗飓风外墙可以保护房地产资产。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 亚太和中东地区的高层建筑热潮

- 更严格的节能建筑标准

- 快速过渡到模组化帷幕墙系统

- 建筑幕墙整合光伏(BIPV)的激增

- 防火建筑幕墙可享保险折扣

- 人工智慧建筑幕墙维护和检测的采用现状

- 市场限制

- 铝和玻璃价格波动

- 复杂的跨辖区消防安全法规

- 保险公司检验的外部系统列入黑名单。

- 合格的建筑幕墙施工人员短缺

- 建筑幕墙产业中使用的不同结构概述

- 定价分析

- 价值/供应链分析

- 监管环境

- 技术展望

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 消费行为分析(建筑商、建筑师、开发商、私人买家、设施和物业经理/业主)

- 永续发展趋势

第五章 市场区隔

- 按类型

- 通风

- 不通风的

- 其他的

- 依建筑幕墙系统类型

- 防雨外墙材料

- 帷幕墙系统

- 其他的

- 材料

- 玻璃

- 金属

- 塑胶和纤维

- 石材

- 其他的

- 透过安装

- 新房产

- 维修和维修工程

- 最终用户

- 商业的

- 住宅

- 其他的

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 亚太其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 奈及利亚

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Saint-Gobain SA

- AGC Glass Europe

- Enclos Corp.

- Permasteelisa SpA

- Kawneer Company

- Kingspan Group

- Lindner Group

- Norsk Hydro ASA

- Schuco International

- YKK AP

- Reynaers Aluminium

- AluK Group

- Jangho Group

- Rockpanel Group

- Sto SE & Co. KGaA

- Trimo doo

- Gutmann AG

- AFS International

- Aluplex

- SRG Global Ltd.*

第七章 市场机会与未来展望

The Facade Market was valued at USD 298.20 billion in 2025 and estimated to grow from USD 314.42 billion in 2026 to reach USD 409.76 billion by 2031, at a CAGR of 5.44% during the forecast period (2026-2031).

This trajectory reflects resilient demand anchored in building-integrated photovoltaics, smart envelope controls, and unitised curtain wall adoption. Asia-Pacific led revenue in 2024, while the Middle East & Africa provided the quickest incremental growth. Ventilated systems preserved design primacy because high-rise developers value thermal performance, and commercial buildings remained the chief revenue stream even as residential retrofits accelerated under tighter energy codes.

Consolidation pressures rose after Saint-Gobain's 2024 acquisition series, yet overall supply stays fragmented as regional specialists coexist with global conglomerates. Volatile aluminum prices and stricter fire-safety rules continue to squeeze project margins, but insurance discounts for compliant facades and falling BIPV costs sustain investment momentum.

Global Facade Market Trends and Insights

High-rise construction boom in Asia-Pacific and Middle East

Soaring skylines in China, India, and Gulf states seed complex performance demands that make facades core infrastructure components rather than decorative skins. More than 176 buildings surpassing 200 m were completed worldwide in 2023, and the pipeline remains robust through mega-projects such as Saudi Arabia's Mukaab and resumed work on China's Goldin Finance 117. Modular off-site assembly shortens critical-path schedules, evidenced by a 26-story tower completed in just five days. Developers consequently press suppliers for factory-finished, multi-functional facades that blend structural support, energy generation, and digital monitoring into a single envelope solution.

Stricter energy-efficiency building codes

Governments translate decarbonization goals into tougher envelope rules, forcing builders to target net-zero operations. Japan's 2025 regulations require photovoltaics on new mid-size structures, and ASHRAE 90.1-2022 raises U.S. energy-savings baselines by 9.8%. California's Title 24 and New York City Local Laws levy penalties for poor performance, spurring facade retrofits during capital cycles. Credits for ventilated cavities, dynamic shading, and low-U-value glass elevate advanced envelope demand, particularly where fire-safety and energy-efficiency mandates overlap.

Volatile aluminum and glass prices

Aluminum is projected to hit USD 2,763 / t in early 2025, producing 10% cost inflation that squeezes margins on projects locked into fixed-bid contracts. Geopolitical tensions and energy-price spikes limit smelter output, while demand from automotive and renewables tightens supply. Smaller facade contractors-often operating on thin working-capital lines-struggle to hedge exposure, hastening consolidation toward vertically integrated suppliers with commodity-risk programs.

Other drivers and restraints analyzed in the detailed report include:

- Rapid shift to unitised curtain-wall systems

- Surge in facade-integrated photovoltaics

- Complex multi-jurisdictional fire-safety rules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ventilated assemblies contributed 51.65% of 2025 revenue, reflecting clearer paths to code compliance where natural convection reduces HVAC loads by up to 25%. The facades market size for ventilated designs is projected to rise at a 5.48% CAGR through 2031 as high-rise projects in hot-humid belts value continuous air gaps and rain-screen performance. Emerging IoT-enabled dampers now regulate cavity airflow in real time, enhancing energy efficiency and extending envelope life. Markets with milder climates still specify non-ventilated facades to save capital, though tightening carbon rules push even budget segments toward hybrid cavities that balance cost and performance.

Non-ventilated configurations remain popular for low-rise housing and warehouse schemes where architectural expression supersedes thermal stringency. Manufacturers court this segment with textured cladding, recycled composites, and simplified anchorage that slashes installation cycles. Hybrid facades appear on mixed-use towers, marrying ventilated orientations on sun-exposed elevations with cost-savvy layers on shaded sides. This selective approach satisfies architectural intent while optimizing total project budgets.

Curtain walls held 43.58% of 2025 demand, and unitised offerings are adding 5.52% CAGR as developers chase schedule certainty. Because stick-built framing struggles with shrinking trade labor pools, factory-glazed panels now dominate skyline projects. The facades market share for curtain walls is reinforced by demonstrated fire performance and the ease of embedding BIPV modules during fabrication. Rainscreen cladding gains ground in logistics hubs and data centers that prize robust weather shielding over maximum transparency.

Advanced curtain-wall packages include electrochromic glass, integrated shading fins, and sensor suites that feed building-management systems. Insurance underwriters also favor proven curtain-wall rigs after high-profile cladding fires, translating into lower premiums versus experimental alternatives. Rainscreen suppliers respond with mineral-fiber cores and non-combustible lamellas to stay competitive, but curtain walls still set the performance benchmark for premium towers.

The Facades Market Report is Segmented by Type (Ventilated, Non-Ventilated, Others), Facade System Type (Rainscreen Cladding, Curtain Wall Systems, Others), Material (Glass, Metal, Plastic and Fibres, Stones, Others), Installation (New Construction, Renovation & Retrofit), End-User (Commercial, Residential, Others), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, Asia-Pacific accounted for 39.58% of global revenue, leading the facades market by value and volume. Mega-projects in China and India, along with Japan's BIPV regulations for medium-sized buildings, keep factories near full capacity. Domestic glass and aluminum producers stabilize supply chains, though skilled installer shortages persist in tier-two cities. Developers import proprietary anchors and smart glazing from Europe to meet premium specifications.

The Middle East and Africa are projected to grow at a 6.18% CAGR through 2031, driven by Saudi Arabia's NEOM, The Line, and Mukaab projects, alongside high-rise developments in Dubai and Doha. Extreme desert climates drive the adoption of ventilated facades and electrochromic glass to reduce cooling loads. Local fabricators expand through technology licenses from European curtain-wall specialists, while governments incentivize local content to support economic diversification.

In Europe, facade demand is driven by renovation, fire-safety upgrades, and embodied-carbon controls. Germany leads in BIPV curtain wall innovation, while France implements energy-performance certificates emphasizing facade efficiency. The U.K. enforces stricter post-Grenfell regulations, increasing demand for compliant A2-s1-d0 materials and phasing out non-compliant cladding. Nordic countries prioritize triple-glazed, thermally broken frames to address harsh winters, reflecting diverse climatic needs.

North America focuses on upgrading aging office buildings and university campuses. Stricter energy codes in California, New York, and Massachusetts encourage smart glazing and improved vapor control. Labor shortages push contractors toward unitized systems, driving domestic investments such as YKK AP's USD 125 million factory expansion in Georgia. Latin American markets remain smaller but show steady growth in coastal cities, where hurricane-rated facades protect real estate assets.

- Saint-Gobain S.A.

- AGC Glass Europe

- Enclos Corp.

- Permasteelisa S.p.A

- Kawneer Company

- Kingspan Group

- Lindner Group

- Norsk Hydro ASA

- Schuco International

- YKK AP

- Reynaers Aluminium

- AluK Group

- Jangho Group

- Rockpanel Group

- Sto SE & Co. KGaA

- Trimo d.o.o.

- Gutmann AG

- AFS International

- Aluplex

- SRG Global Ltd.*

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High-rise construction boom in APAC & Middle East

- 4.2.2 Stricter energy-efficiency building codes

- 4.2.3 Rapid shift to unitised curtain-wall systems

- 4.2.4 Surge in facade-integrated photovoltaics (BIPV)

- 4.2.5 Insurance premium discounts for fire-safe facades

- 4.2.6 AI-driven facade maintenance & inspection adoption

- 4.3 Market Restraints

- 4.3.1 Volatile aluminium & glass prices

- 4.3.2 Complex multi-jurisdictional fire-safety rules

- 4.3.3 Insurers black-listing untested cladding systems

- 4.3.4 Shortage of certified facade installers

- 4.4 Brief on Different Structures Used in the Facades Industry

- 4.5 Pricing Analysis

- 4.6 Value / Supply-Chain Analysis

- 4.7 Regulatory Landscape

- 4.8 Technological Outlook

- 4.9 Industry Attractiveness - Porter's Five Force Analysis

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Consumers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

- 4.10 Consumer Behavior Analysis (Contractors, Architects, Developers, Individual Buyers, Facility & Property Managers/Building Owners)

- 4.11 Sustainability Trends

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Ventilated

- 5.1.2 Non-Ventilated

- 5.1.3 Others

- 5.2 By Facade System Type

- 5.2.1 Rainscreen Cladding

- 5.2.2 Curtain Wall Systems

- 5.2.3 Others

- 5.3 By Material

- 5.3.1 Glass

- 5.3.2 Metal

- 5.3.3 Plastic and Fibres

- 5.3.4 Stones

- 5.3.5 Others

- 5.4 By Installation

- 5.4.1 New Construction

- 5.4.2 Renovation & Retrofit

- 5.5 By End-User

- 5.5.1 Commercial

- 5.5.2 Residential

- 5.5.3 Others

- 5.6 By Region

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East & Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East & Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Saint-Gobain S.A.

- 6.4.2 AGC Glass Europe

- 6.4.3 Enclos Corp.

- 6.4.4 Permasteelisa S.p.A

- 6.4.5 Kawneer Company

- 6.4.6 Kingspan Group

- 6.4.7 Lindner Group

- 6.4.8 Norsk Hydro ASA

- 6.4.9 Schuco International

- 6.4.10 YKK AP

- 6.4.11 Reynaers Aluminium

- 6.4.12 AluK Group

- 6.4.13 Jangho Group

- 6.4.14 Rockpanel Group

- 6.4.15 Sto SE & Co. KGaA

- 6.4.16 Trimo d.o.o.

- 6.4.17 Gutmann AG

- 6.4.18 AFS International

- 6.4.19 Aluplex

- 6.4.20 SRG Global Ltd.*

7 MARKET OPPORTUNITIES & FUTURE OUTLOOK

- 7.1 White-Space & Unmet-Need Assessment

2026年全球建筑幕墙系统市场报告

2026年全球建筑幕墙系统市场报告 欧洲建筑幕墙:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

欧洲建筑幕墙:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 帷幕墙市场-全球产业规模、份额、趋势、机会和预测,依产品、帷幕墙类型、建筑类型、地区和竞争格局划分,2021-2031年预测

帷幕墙市场-全球产业规模、份额、趋势、机会和预测,依产品、帷幕墙类型、建筑类型、地区和竞争格局划分,2021-2031年预测 日本建筑幕墙市场规模、份额、趋势及预测(按产品类型、材料、最终用途和地区划分,2026-2034年)

日本建筑幕墙市场规模、份额、趋势及预测(按产品类型、材料、最终用途和地区划分,2026-2034年) 自癒式帷幕墙材料市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

自癒式帷幕墙材料市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 帷幕建筑幕墙系统市场按材料类型、系统类型、应用、最终用途和功能划分-2025-2032年全球预测瓷质建筑幕墙市场:按产品类型、安装类型、材料、表面处理、应用、分销管道和最终用途 - 2025-2030 年全球预测2025年全球建筑幕墙锚固系统市场报告2025 年至 2033 年外墙市场报告,按产品类型(通风、非通风及其他)、材料(玻璃、金属、塑胶和纤维、石材及其他)、最终用途(商业、住宅、工业)和地区划分

帷幕建筑幕墙系统市场按材料类型、系统类型、应用、最终用途和功能划分-2025-2032年全球预测瓷质建筑幕墙市场:按产品类型、安装类型、材料、表面处理、应用、分销管道和最终用途 - 2025-2030 年全球预测2025年全球建筑幕墙锚固系统市场报告2025 年至 2033 年外墙市场报告,按产品类型(通风、非通风及其他)、材料(玻璃、金属、塑胶和纤维、石材及其他)、最终用途(商业、住宅、工业)和地区划分 全球建筑幕墙系统市场按产品类型、材料、最终用途、技术和地区划分

全球建筑幕墙系统市场按产品类型、材料、最终用途、技术和地区划分