|

市场调查报告书

商品编码

1939073

超级电容:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Supercapacitors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

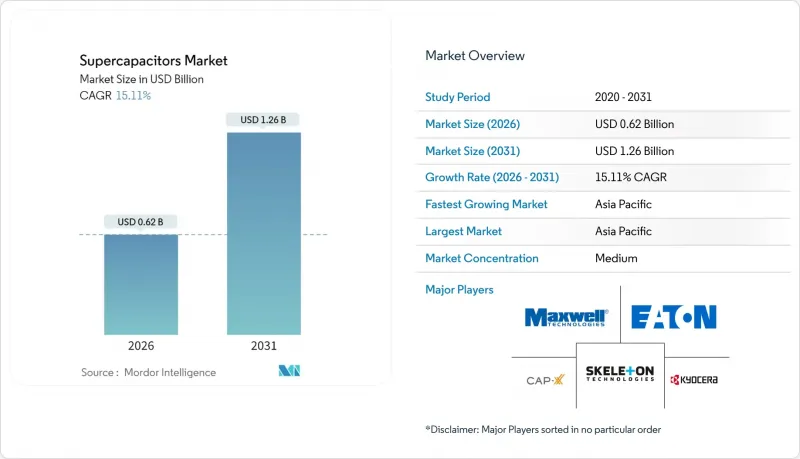

超级电容市场预计将从 2025 年的 5.4 亿美元成长到 2026 年的 6.2 亿美元,到 2031 年将达到 12.6 亿美元,2026 年至 2031 年的复合年增长率为 15.11%。

这项成长主要受以下因素驱动:电气化法规,例如欧盟的48伏轻度混合动力汽车强制令;人工智慧(AI)需求成长带动资料中心对不断电系统(UPS)的需求不断增长;以及将电池和超级电容相结合以实现快速频率响应的电网现代化计划。中国继续保持其作为生产和研发中心的地位,而随着锂离子电池市场份额的下降,韩国製造商正将重心转向能源储存系统。产品创新主要集中在将能量密度提升至接近电池等级的混合动力设计,以及用于製造超薄穿戴装置的石墨烯电极。活性碳价格和离子液体电解质相关的供应链风险限制了短期利润率,但也推动了地域多角化。

全球超级电容市场趋势与洞察

电动公车队快速采用超级电容模组进行再生製动

城市交通系统正日益普及结合电池和超级电容的再生煞车系统,与纯电池系统相比,动能可提高高达85%。宾士的Inturo混合动力公车采用48伏特超级电容组,可承受数百万次充放电循环而不劣化,进而降低5%的油耗。中国城市率先采用这项技术,目前正将混合动力汽车停车场连接到电网,用于车辆充电和电网稳定服务。系统供应商正在整合演算法,以控制超级电容和电池之间的功率转换,使其与线路地形相匹配,从而降低整体拥有成本。随着电动公车采购量的成长,这项特性增强了超级电容在公共运输电气化领域的市场竞争力。

电网级电池-超级电容混合储能係统

电力公司看重超级电容的瞬时频率调节能力。示范测试表明,与独立的锂离子电池组相比,超级电容器可将频率下降降低17.43%,经济效益是纯电池方案的3.2倍。美国能源局预测,随着电池生产自动化程度的提高,到2030年,储能的平准化成本将达到每度电0.337美元。此外,电力公司也重视超级电容的环境优势,因为它们不含钴或镍。这些因素正推动超级电容市场发展成为电网的关键资源,在可再生能源占比高的场景中,超级电容器可与长时电池储能形成互补。

认证差距(IEC 62391)限制了住宅应用

IEC 62391 测试程序延长了认证时间并增加了成本,尤其对中小企业而言更是如此。对比研究表明,该标准比 Maxwell 和 QC/T 741-2014通讯协定耗时更长,导致产品上市延迟长达 12 个月。此外,该标准过度强调高电流测试,这与典型的住宅用电模式不符。这一行政障碍阻碍了超级电容在住宅储能领域的市场渗透,而简化的合格评定流程本来可以创造新的市场需求。

细分市场分析

鑑于其成熟的生产线和在工业功率缓衝领域久经考验的耐用性,电动超级电容器将在2025年保持54.62%的超级电容市场份额。混合型超级电容融合了类似电池的储能特性和传统电容器的功率输出特性,预计到2031年将达到17.62%的复合年增长率。这种混合型方案满足了原始设备製造商(OEM)对能够承受数秒电压骤降并保持更长放电曲线的设备的需求。

锂离子电容器技术的快速研发正在缩小能量密度差距,并扩大动作温度范围。在汽车逆变器和併网系统中的先导计画已证明,混合型超级电容器的循环寿命超过一百万次。这些特性使混合型超级电容器成为超级电容行业的下一个性能标竿。

模组化组件,得益于整合的平衡电路以及与公车、起重机和风力发电机的即插即用相容性,将在2025年占据超级电容市场57.12%的份额。然而,在电网营运商和电动车製造商向更高电压堆(超过800V)发展趋势的推动下,电池组配置预计将以每年16.95%的速度成长。到2031年,受电力公司采用亚秒频率响应技术的推动,电池组级超级电容的市场规模可能会翻倍。

在穿戴式装置和工业控制器领域,电池产品仍然具有重要意义,因为基板级整合和成本仍然是关键因素。供应商现在提供模组化架构,可以以 50 伏特为增量扩展能量容量,从而缩短计划设计週期。先进的温度控管功能进一步拓展了其在严苛环境下的应用。

区域分析

到2025年,中国将占全球超级电容器市场收入的27.88%,这主要得益于其在活性碳加工领域的规模优势和深厚的研究基础,中国发表了65.4%的高影响力论文。国内电动车製造商和国家支持的电网计划带来的需求正在支撑市场规模的成长。国家优先发展国内储能技术的政策也进一步强化了超级电容市场的供应链生态系统。

预计到2031年,韩国及全部区域的复合年增长率将达到15.96%,主要得益于LG能源解决方案、三星SDI和SK安等公司超过200亿美元的新增产能投资。韩国企业正利用电极涂层技术为北美公用事业公司开发组件级储能係统。日本为高可靠性汽车模组提供精密製造技术,而东南亚国家则吸引寻求供应链多元化的组装厂。

美国正利用《通膨控制法案》的激励措施,促进生产在地化,并推动超大规模资料中心采用基于超级电容的UPS设备。欧洲仍以监管主导,欧7法规结构刺激了汽车需求,电网现代化基金则支持混合储能先导工厂。拉丁美洲和中东等新兴地区正在试用超级电容组来稳定微电网,预示着超级电容市场具有长期成长潜力。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 电动公车队快速采用超级电容模组进行再生製动

- 电网级电池-超级电容混合储能係统

- 石墨烯电极技术的创新使超薄穿戴装置成为可能

- 欧盟48V轻混动力系统强制令推动了对12-48V模组的需求。

- 资料中心超大规模资料中心业者采用基于超级电容的UPS来实现ESG目标

- 市场限制

- 活性碳前驱体的价格波动推高了组件成本。

- 认证差距(IEC 62391)限制了其在住宅领域的应用。

- 能量密度平台期(约 10 Wh/kg)限制了长续航力电动车的普及。

- 离子液体电解质供应链中的瓶颈导致前置作业时间延长

- 监管与技术展望(电极材料、容量额定值、电解液、电压范围)

- 宏观经济因素和贸易关税的影响

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 投资与资金筹措分析

第五章 市场规模与成长预测

- 依成分(类型)

- 双电层电容器(EDLC)

- 赝电容器

- 混合型超级电容

- 按外形规格

- 细胞

- 模组

- 包裹

- 依安装类型(分立元件)

- 表面黏着技术

- 径向引线

- 卡扣式

- 螺丝端子

- 按最终用户行业划分

- 家用电子电器

- 穿戴式装置

- 智慧型手机和平板电脑

- SSD 和记忆体备份

- 能源与公共产业

- 电网频率调整

- 可再生能源併网(风能、太阳能)

- 微电网和不断电系统(UPS)

- 工业设备

- 机器人与自动化

- 电动工具

- 重型机械和起重机

- 汽车和运输设备

- 搭乘用车

- 48V轻混

- 启停式微混合动力

- 商用车辆

- 公车

- 追踪

- 铁路和路面电车

- 航空航太太空产业

- 搭乘用车

- 资料中心和通信

- 国防与航太

- 其他(医疗设备、农业无人机)

- 家用电子电器

- 按地区

- 我们

- 欧洲

- 中国

- 日本

- 韩国及其他亚太地区

- 世界其他地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Maxwell Technologies Inc.(Tesla)

- Skeleton Technologies SA

- CAP-XX Ltd.

- Eaton Corporation plc

- Panasonic Holdings Corp.

- LS Mtron Ltd.

- Kyocera Corp.

- Nippon Chemi-Con Corp.

- Supreme Power Solutions Co.

- Shanghai Aowei Technology Development Co.

- Samwha capacitor Group

- Nanoramic Laboratories(FastCAP)

- Nawa Technologies SAS

- Cornell Dubilier Electronics Inc.

- Toyo capacitor Co.

- Shenzhen Topmay Electronic Co.

- Liaoning Brother Electronics Technology Co.

- Chengdu ZT-Energy Tech Co.

- Loxus Inc.

- Nantong Jianghai capacitor Co. Ltd

- Beijing HCC Energy

- Jinzhou Kaimei Power Co. Ltd(KAM)

- Shanghai Green Tech Co. Ltd(GTCAP)

- Shenzhen Topmay Electronic Co. Ltd

- SEMG(Seattle Electronics Manufacturing Group(HK)Co. Ltd)

- Shanghai Pluspark Electronics Co. Ltd

第七章 市场机会与未来展望

The supercapacitors market is expected to grow from USD 0.54 billion in 2025 to USD 0.62 billion in 2026 and is forecast to reach USD 1.26 billion by 2031 at 15.11% CAGR over 2026-2031.

Growth is supported by electrification rules such as the European Union's 48-volt mild-hybrid mandate, datacenter demand for uninterruptible power during artificial-intelligence (AI) surges, and grid-modernization projects that blend batteries with supercapacitors for rapid frequency response. China continues to anchor production and research, while Korean manufacturers pivot toward energy-storage systems as their lithium-ion share slips. Product innovation centres on hybrid designs that lift energy density toward battery-like levels and graphene electrodes that enable ultra-thin wearables. Supply-chain risks around activated-carbon prices and ionic-liquid electrolytes temper near-term margins but also encourage regional diversification.

Global Supercapacitors Market Trends and Insights

Rapid adoption of regenerative-braking supercapacitor modules in e-bus fleets

Urban transit agencies are scaling regenerative-braking systems that pair batteries with supercapacitors, recovering up to 85% more kinetic energy than battery-only setups. Mercedes-Benz's Intouro hybrid bus cut fuel use by 5% using a 48-volt supercapacitor pack that endures millions of charge cycles without degradation. Chinese cities were first movers and now link hybrid depots to the grid for both vehicle charging and grid-stability services. System suppliers integrate algorithms that shift power between supercapacitors and batteries to match route topography, which lowers total cost of ownership. As electric-bus procurements rise, this capability strengthens the competitive position of the supercapacitors market in mass-transit electrification.

Grid-scale battery-supercapacitor hybrid storage

Utilities value supercapacitors for instant frequency regulation. Demonstrations showed a 17.43% reduction in frequency-drop rates versus standalone lithium-ion arrays, delivering economic benefits 3.2-times greater than battery-only solutions. The U.S. Department of Energy projects levelized storage costs of USD 0.337 per kWh by 2030 as automated cell production scales. Operators also cite environmental advantages because supercapacitors avoid cobalt and nickel. These factors position the supercapacitors market as an essential grid-forming resource that complements long-duration batteries under high-renewable penetration scenarios.

Certification gaps (IEC 62391) limiting residential adoption

IEC 62391 testing procedures prolong qualification timelines and raise costs, especially for smaller firms. Comparative studies show the standard takes longer than Maxwell and QC/T 741-2014 protocols, stretching product launches by up to 12 months. The heavy focus on high-current testing is mismatched with typical household power profiles. This administrative hurdle slows the supercapacitors market from penetrating residential energy-storage segments where simplified compliance would unlock new demand.

Other drivers and restraints analyzed in the detailed report include:

- Graphene-based electrode breakthroughs enabling ultra-thin wearables

- EU 48 V mild-hybrid mandate accelerating demand for 12-48 V modules

- Energy-density plateau (~10 Wh/kg) restricting long-range EV penetration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electric Double-Layer Capacitors maintained a 54.62% share of the supercapacitors market in 2025, reflecting established production lines and proven durability in industrial power buffering. Hybrid Supercapacitors are on track for an 17.62% CAGR to 2031 as they merge battery-like energy storage with classic capacitor power delivery. The hybrid approach answers OEM calls for devices that can ride through seconds-long voltage dips and also sustain longer discharge profiles.

Rapid R&D advances, including lithium-ion capacitor variants, narrow the energy-density gap and extend operating temperatures. Pilot projects in automotive inverters and grid-forming systems showcase cycle lifetimes beyond one million cycles. These traits position hybrids as the next performance benchmark within the supercapacitors industry.

Module assemblies captured 57.12% of the supercapacitors market in 2025 thanks to integrated balancing circuitry and drop-in compatibility for buses, cranes, and wind turbines. Pack configurations, however, are projected to grow 16.95% annually as grid operators and EV makers opt for higher-voltage stacks that exceed 800 V. The supercapacitors market size for pack-level products could double by 2031 as utilities deploy them for sub-second frequency response.

Cell products retain relevance in wearables and industrial controllers where board-level integration and cost sensitivity remain critical. Vendors now offer modular architectures that let customers scale energy in 50-volt increments, shortening project design cycles. Advanced thermal-management features further widen adoption across harsh-duty environments.

The Supercapacitors Market Report is Segmented by Configuration (Type) (Electric Double-Layer Capacitors (EDLC), Pseudo Capacitors, and Hybrid Supercapacitors), Form Factor (Cell, Module, and Pack), Mounting Type (Discrete Components) (Surface-Mount, Radial Leaded, Snap-In, and More), End-User Industry (Consumer Electronics, Energy and Utilities, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

China controlled 27.88% of global revenue in 2025 due to scale in activated-carbon processing and a deep research base that publishes 65.4% of high-impact papers. Domestic demand from electric-vehicle makers and state-backed grid projects underpins volume growth. State policies that prioritise local energy-storage content further entrench supply-chain ecosystems for the supercapacitors market.

Korea and the broader Asia region are set for a 15.96% CAGR through 2031, propelled by LG Energy Solution, Samsung SDI, and SK On investments that exceed USD 20 billion in new capacity. Korean firms channel expertise in electrode coatings toward pack-level storage systems aimed at North American utilities. Japan contributes precision manufacturing for high-reliability automotive modules, while Southeast Asian nations attract assembly plants seeking diversified supply bases.

The United States leverages Inflation Reduction Act incentives to localise production and deploy supercapacitor-based UPS units in hyperscale datacenters. Europe remains regulation-driven, with the Euro 7 framework spurring automotive demand and grid-modernization funds supporting hybrid storage pilot plants. Emerging regions in Latin America and the Middle East trial supercapacitor packs for microgrid stability, signalling long-term addressable growth for the supercapacitors market.

List of Companies Covered in this Report:

- Maxwell Technologies Inc. (Tesla)

- Skeleton Technologies SA

- CAP-XX Ltd.

- Eaton Corporation plc

- Panasonic Holdings Corp.

- LS Mtron Ltd.

- Kyocera Corp.

- Nippon Chemi-Con Corp.

- Supreme Power Solutions Co.

- Shanghai Aowei Technology Development Co.

- Samwha capacitor Group

- Nanoramic Laboratories (FastCAP)

- Nawa Technologies SAS

- Cornell Dubilier Electronics Inc.

- Toyo capacitor Co.

- Shenzhen Topmay Electronic Co.

- Liaoning Brother Electronics Technology Co.

- Chengdu ZT-Energy Tech Co.

- Loxus Inc.

- Nantong Jianghai capacitor Co. Ltd

- Beijing HCC Energy

- Jinzhou Kaimei Power Co. Ltd (KAM)

- Shanghai Green Tech Co. Ltd (GTCAP)

- Shenzhen Topmay Electronic Co. Ltd

- SEMG (Seattle Electronics Manufacturing Group (HK) Co. Ltd)

- Shanghai Pluspark Electronics Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid adoption of regenerative-braking supercapacitor modules in e-bus fleets

- 4.2.2 Grid-scale battery-supercapacitor hybrid storage

- 4.2.3 Graphene-based electrode breakthroughs enabling ultra-thin wearables

- 4.2.4 EU 48 V mild-hybrid mandate accelerating demand for 12-48 V modules

- 4.2.5 Supercapacitor-based UPS deployment by Datacenter hyperscalers to meet ESG targets

- 4.3 Market Restraints

- 4.3.1 Activated-carbon precursor price volatility inflating BOM costs

- 4.3.2 Certification gaps (IEC 62391) limiting the residential adoption

- 4.3.3 Energy-density plateau (~10 Wh/kg) restricting long-range EV penetration

- 4.3.4 Ionic-liquid electrolyte supply-chain bottlenecks elongating lead-times

- 4.4 Regulatory and Technological Outlook (Electrode Material, Capacity Ratings, Electrolyte, Voltage Range)

- 4.5 Impact of Macroeconomic Factors and Trade Tarrifs

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Investment and Funding Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Configuration (Type)

- 5.1.1 Electric Double-Layer Capacitors (EDLC)

- 5.1.2 Pseudocapacitors

- 5.1.3 Hybrid Supercapacitors

- 5.2 By Form Factor

- 5.2.1 Cell

- 5.2.2 Module

- 5.2.3 Pack

- 5.3 By Mounting Type (Discrete Components)

- 5.3.1 Surface-Mount

- 5.3.2 Radial Leaded

- 5.3.3 Snap-in

- 5.3.4 Screw Terminal

- 5.4 By End-User Industry

- 5.4.1 Consumer Electronics

- 5.4.1.1 Wearables

- 5.4.1.2 Smartphones and Tablets

- 5.4.1.3 SSD and Memory Backup

- 5.4.2 Energy and Utilities

- 5.4.2.1 Grid Frequency Regulation

- 5.4.2.2 Renewable Integration (Wind, Solar)

- 5.4.2.3 Microgrid and UPS

- 5.4.3 Industrial Equipment

- 5.4.3.1 Robotics and Automation

- 5.4.3.2 Power Tools

- 5.4.3.3 Heavy Machinery and Cranes

- 5.4.4 Automotive and Transportation

- 5.4.4.1 Passenger Cars

- 5.4.4.1.1 48 V Mild Hybrid

- 5.4.4.1.2 Start-Stop Micro Hybrid

- 5.4.4.2 Commercial Vehicles

- 5.4.4.2.1 Buses

- 5.4.4.2.2 Trucks

- 5.4.4.3 Rail and Tram

- 5.4.4.4 Aviation and Aerospace

- 5.4.4.1 Passenger Cars

- 5.4.5 Data Centers and Telecom

- 5.4.6 Defense and Space

- 5.4.7 Others (Medical Devices, Agri-drones)

- 5.4.1 Consumer Electronics

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Europe

- 5.5.3 China

- 5.5.4 Japan

- 5.5.5 Korea and Rest of Asia-Pacific

- 5.5.6 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Maxwell Technologies Inc. (Tesla)

- 6.4.2 Skeleton Technologies SA

- 6.4.3 CAP-XX Ltd.

- 6.4.4 Eaton Corporation plc

- 6.4.5 Panasonic Holdings Corp.

- 6.4.6 LS Mtron Ltd.

- 6.4.7 Kyocera Corp.

- 6.4.8 Nippon Chemi-Con Corp.

- 6.4.9 Supreme Power Solutions Co.

- 6.4.10 Shanghai Aowei Technology Development Co.

- 6.4.11 Samwha capacitor Group

- 6.4.12 Nanoramic Laboratories (FastCAP)

- 6.4.13 Nawa Technologies SAS

- 6.4.14 Cornell Dubilier Electronics Inc.

- 6.4.15 Toyo capacitor Co.

- 6.4.16 Shenzhen Topmay Electronic Co.

- 6.4.17 Liaoning Brother Electronics Technology Co.

- 6.4.18 Chengdu ZT-Energy Tech Co.

- 6.4.19 Loxus Inc.

- 6.4.20 Nantong Jianghai capacitor Co. Ltd

- 6.4.21 Beijing HCC Energy

- 6.4.22 Jinzhou Kaimei Power Co. Ltd (KAM)

- 6.4.23 Shanghai Green Tech Co. Ltd (GTCAP)

- 6.4.24 Shenzhen Topmay Electronic Co. Ltd

- 6.4.25 SEMG (Seattle Electronics Manufacturing Group (HK) Co. Ltd)

- 6.4.26 Shanghai Pluspark Electronics Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

超级电容市场:2026年至2032年全球市场预测(按类型、电极材料、形状、电压范围、应用和销售管道)汽车超级电容市场:2026-2032年全球市场预测(按模组、车辆类型、技术、应用和最终用途划分)

超级电容市场:2026年至2032年全球市场预测(按类型、电极材料、形状、电压范围、应用和销售管道)汽车超级电容市场:2026-2032年全球市场预测(按模组、车辆类型、技术、应用和最终用途划分) 石墨烯基超级超级电容市场分析及预测(至2035年):类型、产品、技术、组件、应用、形式、材料类型、製程、最终用户、功能SMD超级电容市场按电压范围、产品类型、电解液类型、销售管道、应用和终端用户产业划分-全球预测(2026-2032年)超级电容材料市场(按电极材料类型、电解质类型、结构类型、封装类型和最终用途划分)-2026-2032年全球预测

石墨烯基超级超级电容市场分析及预测(至2035年):类型、产品、技术、组件、应用、形式、材料类型、製程、最终用户、功能SMD超级电容市场按电压范围、产品类型、电解液类型、销售管道、应用和终端用户产业划分-全球预测(2026-2032年)超级电容材料市场(按电极材料类型、电解质类型、结构类型、封装类型和最终用途划分)-2026-2032年全球预测 全球超级电容材料市场预测(至2032年):依材料类型、装置配置、最终用户和地区划分

全球超级电容材料市场预测(至2032年):依材料类型、装置配置、最终用户和地区划分 日本超级电容器市场报告(按产品类型、模组类型、材料类型、最终用途产业和地区划分,2026-2034年)

日本超级电容器市场报告(按产品类型、模组类型、材料类型、最终用途产业和地区划分,2026-2034年) 全球超级电容器市场:按类型、电极材料、电容、产业和地区划分 - 产业动态、市场规模、机会分析和预测(2026-2035 年)

全球超级电容器市场:按类型、电极材料、电容、产业和地区划分 - 产业动态、市场规模、机会分析和预测(2026-2035 年) 超级电容电池市场规模、份额和成长分析(按产品类型、材料类型、容量、应用、最终用户和地区划分)-2026-2033年产业预测

超级电容电池市场规模、份额和成长分析(按产品类型、材料类型、容量、应用、最终用户和地区划分)-2026-2033年产业预测 超级电容市场规模、份额和成长分析(按类型、应用、额定电压和地区划分)-2026-2033年产业预测

超级电容市场规模、份额和成长分析(按类型、应用、额定电压和地区划分)-2026-2033年产业预测