|

市场调查报告书

商品编码

1939081

汽车空调系统:市占率分析、产业趋势与统计、成长预测(2026-2031)Automotive HVAC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

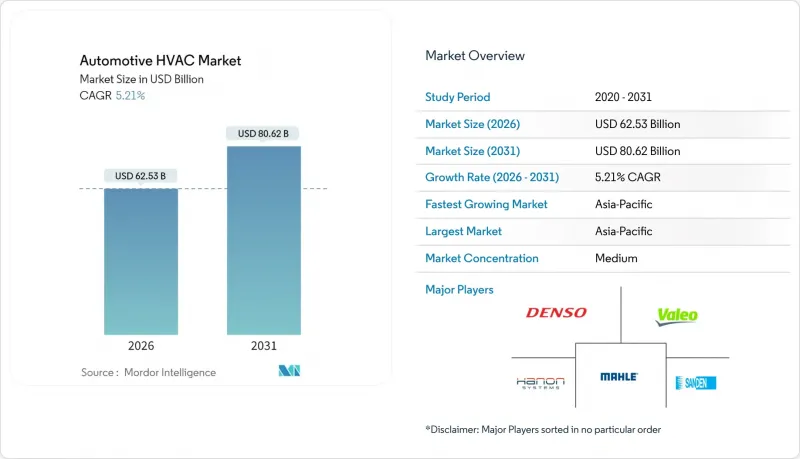

2025年汽车HVAC市场价值为594.4亿美元,预计到2031年将达到806.2亿美元,而2026年为625.3亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 5.21%。

这一稳步增长反映了向电动动力传动系统的转型、日益严格的舒适性法规以及不断提高的消费者期望。亚太地区仍然是重要的製造地,而更严格的排放气体法规正在推动温度控管技术的持续改进。同时,自动空调系统在量产车型的应用降低了以往只有豪华车型才具备的溢价。供应商正透过电子控制、先进的过滤技术和低全球暖化潜值(GWP)冷媒相容性来实现差异化,从而将空调系统从辅助舒适模组转变为推动车辆电气化的关键因素。

全球汽车暖通空调市场趋势与洞察

电动汽车热泵系统的暖通空调效率需求

电动车的广泛普及使空调系统成为与续航里程直接相关的关键子系统。在-10°C的低温环境下,性能係数为3.0或更高的热泵每行驶300公里可节省高达11千瓦时的电量,显着降低使用电阻式加热器时高达40%的续航里程损失。汽车製造商正在电池、电力电子设备和车厢之间整合冷却迴路以回收废热。这迫使供应商提供专为低温蒸气喷射而设计的多端口阀和变频压缩机。诸如中国工信部(MIIT)的节能补贴等旨在提高车辆能效的监管奖励,正鼓励汽车製造商即使在入门级电动车中也采用高端空调系统。

自动气候控制舒适性的需求

随着车辆朝向互联架构发展,实现远端空调控制、语音指令和使用者画像学习等功能,消费者对自动驾驶系统的偏好日益增长。精准的温度控制能够减少驾驶者的疲劳和注意力分散,这与SUV车型日益普及带来的安全需求不谋而合。汽车製造商正将自动空调系统与资讯娱乐系统捆绑销售,以提高平均成交价格,而感测器成本的下降也推动了紧凑型车型配备该系统。在新兴经济体,随着收入的成长,人们对舒适性的期望也越来越高,自动驾驶系统的普及速度也正在加快。在电池式电动车(BEV)中,自动驾驶控制系统能够协调节能的座舱加热策略,并在都市区通勤期间保持电池电量。

自动空调系统的单位成本和复杂度增加

与手动系统相比,电子膨胀阀、步进马达致动器和多感测器丛集会使零件成本增加高达 50%,从而限制了它们在入门级掀背车中的应用。服务网路需要诊断扫描工具和技师再培训,这进一步推高了生命週期成本。由于半导体短缺导致的采购波动,儘管消费者对此感兴趣,巴西和印尼的汽车製造商仍推迟了自动空调系统的标准化进程。

细分市场分析

感测器价格的下降以及利用远端资讯处理平台的舒适性订阅服务的普及,正逐步提升自动化系统的市场份额。儘管如此,手排和半自动解决方案仍将主导汽车空调系统市场,预计到2025年将占58.12%的市场份额。然而,到2031年,自动化系统将以9.25%的复合年增长率成长,创造约168亿美元的附加价值。基于人工智慧的学习模式将改善用户体验,而与电池预热功能的整合将使纯电池式电动车受益。

C级车单区自动控制系统的标准化正在缩小与手动旋钮式控制系统的成本差距。在高阶车型上,双区和三区配置则构成了额外的价格因素。掌握了自主演算法开发的供应商正在交叉销售软体咨询服务,而传统的机械製造商则正与微控制器专家合作以保持竞争力。

到 2025 年,乘用车将占汽车 HVAC 市场份额的 79.62%,然而,随着政府出台有关乘客舒适度的法规,预计到 2031 年,公共汽车和长途客车市场将以 6.55% 的复合年增长率超越乘用车。共享小巴服务公司为了赢得政府合同,更倾向于使用内建 HEPA 过滤器的车顶式空调机组。

负责最后一公里物流的轻型商用车(LCV)正在采用辅助电动空调,以便在引擎关闭的情况下完成包裹配送,从而减少低排放气体区怠速罚款。印度、印尼和墨西哥的中型和重型卡车正在转向原厂安装空调,以满足新的安全法规,这增加了对能够承受多尘运作的坚固耐用型压缩机设计的需求。

区域分析

预计到2025年,亚太地区将占据汽车空调系统市场48.55%的份额,并在2031年之前保持5.55%的复合年增长率。中国2025年的新能源汽车销售配额迫使本土汽车製造商采用即使在北方冬季(-20°C)也能高效运行的整合式热泵模组。印度强制所有重型卡车安装空调,带动了对能够承受高振动环境的重型压缩机的大量订单。日本和韩国正在出口高精度电子膨胀阀,完善了该地区的价值链。

北美市场既成熟又技术先进。皮卡和SUV需要大容量冷凝器来满足大型车厢的需求,而加拿大和美国北部严寒的气候则充分展现了寒冷气候热泵的卓越性能。三菱电机斥资1.435亿美元对其肯塔基州工厂的变速压缩机生产线进行维修,显示该地区正着力于电动车暖通空调设备的本土化采购。

欧洲最严格的低全球暖化潜值(GWP)冷媒实施计画即将生效,这将加速R1234yf的推广应用,并迫使供应商开发天然冷媒R744的原型,以满足2030年后的相关法规要求。德国和法国的城市公车电气化计画指定使用节能型热泵系统以满足竞标要求。 ISO 13043:2011标准制定的性能标准对供应商的品管系统产生连锁反应,确保整个欧洲大陆系统的一致性。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 电动汽车热泵系统的暖通空调效率需求

- 自动气候舒适性的需求

- 疫情后,人们更加关注车厢空气品质和过滤系统。

- 新兴市场的安全与舒适法规

- 对改装共乘汽车的需求激增

- 基于人工智慧的预测和分区冷却

- 市场限制

- 自动空调系统的单位成本不断上升,且系统日益复杂。

- 暖通空调负载降低/电动车行驶里程目标

- 过渡到低全球暖化潜势冷媒的相关成本增加

- 缺乏接受过新型冷媒训练的技术人员

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模及成长预测(价值(美元))

- 依技术类型

- 手动/半自动空调系统

- 自动空调系统

- 按车辆类型

- 搭乘用车

- 轻型商用车(LCV)

- 中型和重型商用车辆

- 公车和长途客车

- 按组件

- 压缩机

- 冷凝器

- 蒸发器

- 膨胀阀/节流管

- 接收器干燥器和蓄能器

- 电子和感测器套件

- 依推进类型

- 内燃机车辆

- 混合动力汽车和插电式混合动力汽车

- 电池式电动车

- 按销售管道

- 原厂配套

- 售后改装和服务

- 按地区

- 北美洲

- 我们

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 埃及

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Denso Corporation

- Valeo Group

- Hanon Systems Co., Ltd.

- MAHLE GmbH

- Sanden Corporation

- Marelli Holdings Co., Ltd.

- Keihin Corporation

- Japan Climate Systems Corporation

- Mitsubishi Heavy Industries, Ltd.

- Samvardhana Motherson International Limited

- HELLA GmbH & Co. KGaA

- Subros Ltd.

- Aisin Corporation

- Eberspacher Group

- Brose Fahrzeugteile

第七章 市场机会与未来展望

The automotive HVAC market was valued at USD 59.44 billion in 2025 and estimated to grow from USD 62.53 billion in 2026 to reach USD 80.62 billion by 2031, at a CAGR of 5.21% during the forecast period (2026-2031).

This steady expansion reflects the sector's transition toward electrified powertrains, stricter comfort regulations, and rising consumer expectations. Asia-Pacific remains the principal manufacturing hub, and its tightening emissions rules spur continuous upgrades of thermal-management technology. Meanwhile, automatic climate-control systems enter mass-market vehicle lines, compressing the price premium that once confined them to luxury models. Component suppliers differentiate through electronic control, advanced filtration, and low-GWP refrigerant compatibility, repositioning HVAC from an auxiliary comfort module to a critical enabler of vehicle electrification.

Global Automotive HVAC Market Trends and Insights

HVAC Efficiency Requirements for EV Heat-Pump Systems

BEV adoption turns HVAC into a range-critical subsystem. Heat pumps that achieve a coefficient of performance above 3.0 at -10 °C can save up to 11 kWh during a 300 km winter drive, mitigating the 40% range penalty seen with resistive heaters. Automakers integrate coolant loops among battery, power electronics, and cabin to harvest waste heat, prompting suppliers to deliver multi-port valves and inverter-driven compressors tuned for low-temperature vapor injection. Regulatory incentives that reward vehicle efficiency, such as China's MIIT credits, incentivize OEMs to specify premium HVAC even for entry-segment EVs.

Demand for Automatic Climate-Control Comfort

Consumer preference for automatic systems intensifies as vehicles migrate to connected architectures that enable remote pre-conditioning, voice commands, and user-profile learning. Precise temperature maintenance reduces driver fatigue and distraction, aligning with safety priorities as SUVs with larger cabin volumes proliferate. OEMs bundle automatic HVAC with infotainment packages to lift average transaction prices, and falling sensor costs encourage deployment in compact models. Uptake accelerates in emerging economies where rising incomes elevate comfort expectations. In BEVs, automatic control also orchestrates energy-efficient cabin warming strategies that preserve battery state of charge during urban commutes.

Higher Unit Cost and Complexity for Automatic HVAC

Electronic expansion valves, stepper-motor actuators, and multi-sensor clusters elevate bill-of-materials cost by up to 50% relative to manual systems, limiting penetration in entry-segment hatchbacks. Service networks require diagnostic scan tools and technician retraining, further inflating lifecycle expense. Semiconductor shortages introduce procurement volatility, encouraging OEMs in Brazil and Indonesia to delay standardization of automatic climate control despite consumer interest.

Other drivers and restraints analyzed in the detailed report include:

- Post-Pandemic Focus on Cabin Air-Quality and Filtration

- Safety and Comfort Regulations in Emerging Markets

- HVAC Load Cutting EV Driving-Range Targets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Automatic systems capture incremental share as sensor prices fall and OEMs exploit telematics platforms to deliver comfort subscriptions. In 2025, manual and semi-automatic solutions still dominated with a 58.12% of the automotive HVAC market share in 2025. However, automatic setups will expand at a 9.25% CAGR through 2031, adding nearly USD 16.8 billion in incremental value. AI-based learning profiles elevate the user experience, while integration with battery preconditioning benefits BEVs.

Standardizing single-zone automatic control in C-segment cars compresses the cost gap relative to manual rotary dials. In premium models, dual- and tri-zone configurations underpin add-on pricing. Suppliers that mastered in-house algorithm development now cross-sell software consultancy, while legacy mechanical firms partner with microcontroller specialists to stay competitive.

Passenger cars account for 79.62% of the automotive HVAC market share in 2025, yet buses and coaches will outpace at a 6.55% CAGR to 2031 as governments legislate passenger comfort mandates. Ride-sharing minibus services favor roof-mounted units with integrated HEPA filtration to win municipal contracts.

Light commercial vehicles serving last-mile logistics adopt auxiliary electric air-conditioning to allow engine-off parcel drops, reducing idling penalties in low-emission zones. Medium and heavy trucks in India, Indonesia, and Mexico shift toward factory-fit AC to comply with new safety rules, enlarging volume for robust compressor designs that tolerate dusty duty cycles.

The Automotive HVAC Market Report is Segmented by Technology Type (Manual/Semi-automatic HVAC and Automatic HVAC), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Component (Compressor, Condenser, and More), Propulsion Type (ICE Vehicles, Hybrid and Plug-In Hybrid Vehicles, and More), Sales Channel (OEM Factory-Fit and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 48.55% of the automotive HVAC market share in 2025 and is set to maintain the lead with a 5.55% CAGR through 2031. China's 2025 NEV sales quota compels local OEMs to adopt integrated heat-pump modules that operate efficiently in -20 °C northern winters. India's blanket AC mandate for heavy trucks fuels bulk orders for rugged compressors built to tolerate high vibration. Japan and South Korea export high-precision electronic expansion valves, reinforcing the region's value-chain completeness.

North America reflects a mature yet technologically progressive market. Pickup trucks and SUVs require high-capacity condensers to serve large cabin volumes, and frigid climates in Canada and the northern United States validate cold-weather heat-pump performance. Mitsubishi Electric's USD 143.5 million retrofit of its Kentucky plant for variable-speed compressor lines underscores the region's strategic focus on domestically sourced HVAC for EV applications.

Europe enforces the most aggressive low-GWP refrigerant timeline, accelerating the adoption of R1234yf and pushing suppliers toward natural refrigerant R744 prototypes for post-2030 compliance. Urban bus electrification programs in Germany and France stipulate energy-efficient heat-pump systems to meet tender requirements. ISO 13043:2011 sets performance benchmarks that ripple through supplier quality-management systems, ensuring system integrity across the continent .

- Denso Corporation

- Valeo Group

- Hanon Systems Co., Ltd.

- MAHLE GmbH

- Sanden Corporation

- Marelli Holdings Co., Ltd.

- Keihin Corporation

- Japan Climate Systems Corporation

- Mitsubishi Heavy Industries, Ltd.

- Samvardhana Motherson International Limited

- HELLA GmbH & Co. KGaA

- Subros Ltd.

- Aisin Corporation

- Eberspacher Group

- Brose Fahrzeugteile

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 HVAC Efficiency Requirements for EV Heat-Pump Systems

- 4.2.2 Demand for Automatic Climate-Control Comfort

- 4.2.3 Post-Pandemic Focus on Cabin Air-Quality and Filtration

- 4.2.4 Safety and Comfort Regulations in Emerging Markets

- 4.2.5 Ride-Hailing Fleet Retro-Fit Demand Surge

- 4.2.6 AI-Based Predictive and Zonal Climate Functions

- 4.3 Market Restraints

- 4.3.1 Higher Unit Cost and Complexity for Automatic HVAC

- 4.3.2 HVAC Load Cutting EV Driving-Range Targets

- 4.3.3 Costly Transition to Low-GWP Refrigerants

- 4.3.4 Shortage of Technicians Trained on New Refrigerants

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Technology Type

- 5.1.1 Manual / Semi-automatic HVAC

- 5.1.2 Automatic HVAC

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles (LCV)

- 5.2.3 Medium and Heavy Commercial Vehicles

- 5.2.4 Buses and Coaches

- 5.3 By Component

- 5.3.1 Compressor

- 5.3.2 Condenser

- 5.3.3 Evaporator

- 5.3.4 Expansion Valve / Orifice Tube

- 5.3.5 Receiver-Dryer and Accumulator

- 5.3.6 Electronic and Sensor Suite

- 5.4 By Propulsion Type

- 5.4.1 ICE Vehicles

- 5.4.2 Hybrid and Plug-in Hybrid Vehicles

- 5.4.3 Battery-Electric Vehicles

- 5.5 By Sales Channel

- 5.5.1 OEM Factory-Fit

- 5.5.2 Aftermarket Retro-Fit and Service

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Egypt

- 5.6.5.5 South Africa

- 5.6.5.6 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Denso Corporation

- 6.4.2 Valeo Group

- 6.4.3 Hanon Systems Co., Ltd.

- 6.4.4 MAHLE GmbH

- 6.4.5 Sanden Corporation

- 6.4.6 Marelli Holdings Co., Ltd.

- 6.4.7 Keihin Corporation

- 6.4.8 Japan Climate Systems Corporation

- 6.4.9 Mitsubishi Heavy Industries, Ltd.

- 6.4.10 Samvardhana Motherson International Limited

- 6.4.11 HELLA GmbH & Co. KGaA

- 6.4.12 Subros Ltd.

- 6.4.13 Aisin Corporation

- 6.4.14 Eberspacher Group

- 6.4.15 Brose Fahrzeugteile

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

2034年全球空调市场预测-按系统类型、组件、部署模式、能源来源、技术、应用、最终用户和地区分類的分析

2034年全球空调市场预测-按系统类型、组件、部署模式、能源来源、技术、应用、最终用户和地区分類的分析 汽车空调市场:依技术、产品类型、组件、车辆类型和销售管道划分-2026-2032年全球市场预测汽车PTC加热器市场:2026年至2032年全球市场预测(按车辆类型、材料、额定功率、技术、燃料类型、应用和最终用户划分)

汽车空调市场:依技术、产品类型、组件、车辆类型和销售管道划分-2026-2032年全球市场预测汽车PTC加热器市场:2026年至2032年全球市场预测(按车辆类型、材料、额定功率、技术、燃料类型、应用和最终用户划分) 汽车暖通空调系统市场规模、份额、趋势和预测报告:按组件、技术、车辆类型和地区划分,2026-2034年

汽车暖通空调系统市场规模、份额、趋势和预测报告:按组件、技术、车辆类型和地区划分,2026-2034年 汽车暖通空调市场机会、成长要素、产业趋势分析及2026-2035年预测

汽车暖通空调市场机会、成长要素、产业趋势分析及2026-2035年预测 汽车暖通空调(HVAC)全球市场规模、份额、趋势和成长分析报告(2026-2034)

汽车暖通空调(HVAC)全球市场规模、份额、趋势和成长分析报告(2026-2034) 汽车暖通空调市场:按类型、组件类型、销售管道、技术、国家及地区划分-全球产业分析、市场规模、市场份额及2025年至2032年预测日本汽车空调市场规模、份额、趋势及预测(按组件、技术、车辆类型及地区划分),2026-2034年

汽车暖通空调市场:按类型、组件类型、销售管道、技术、国家及地区划分-全球产业分析、市场规模、市场份额及2025年至2032年预测日本汽车空调市场规模、份额、趋势及预测(按组件、技术、车辆类型及地区划分),2026-2034年 2026年全球汽车暖通空调鼓风机马达市场研究报告

2026年全球汽车暖通空调鼓风机马达市场研究报告 2026年全球汽车冷藏库市场报告

2026年全球汽车冷藏库市场报告