|

市场调查报告书

商品编码

1939152

热感喷涂:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Thermal Spray - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

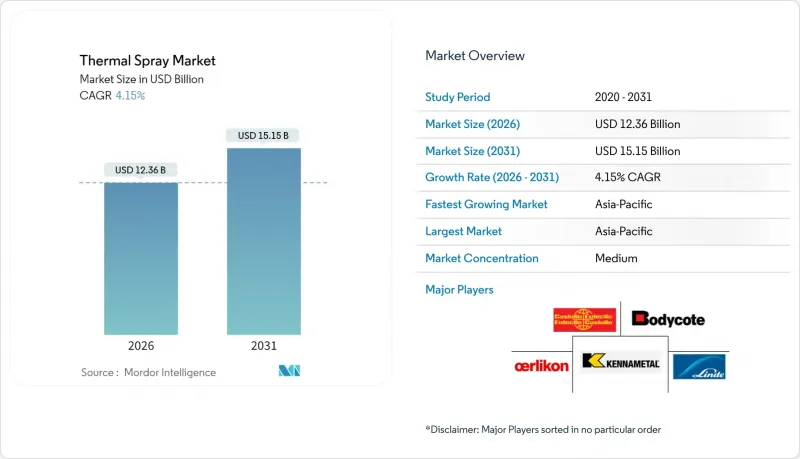

热感喷涂市场预计将从 2025 年的 118.7 亿美元成长到 2026 年的 123.6 亿美元,预计到 2031 年将达到 151.5 亿美元,2026 年至 2031 年的复合年增长率为 4.15%。

随着航太、医疗设备和新一代汽车製造商用高性能涂层取代传统的表面处理工艺,延长零件寿命并改善温度控管,市场对高性能涂层的需求正在增长。对自动化设备和即时製程监控的投资持续缓解着技术纯熟劳工短缺的问题,而向电动喷涂技术的转变也恰逢其时,满足了日益严格的环境法规的要求。亚太地区的製造地正在迅速扩张,推动了该地区对电子产品和电动动力传动系统总成部件用涂层材料和承包喷涂单元的需求。

全球热感喷涂市场趋势及展望

热感喷涂羟基磷灰石涂层在整形外科和人工植牙中的应用日益广泛

热感喷涂羟基磷灰石涂层能显着促进骨骼生长并降低排异率,使其成为承重整形外科螺丝、人工髋关节柄和牙科植入物的理想表面处理材料。製程控制能够设计出与鬆质骨形态相符的微孔结构,加速骨整合并缩短復原时间。该技术已获得美国FDA II类医疗设备和CE核准,并被全球植入製造商迅速采用。随着美国、德国和日本人口老化,外科手术数量持续成长,对磷酸钙粉末的原料需求也随之增加。设备供应商目前提供封闭回路型机器人与在线连续厚度计相结合的解决方案,以确保涂层的可重复性并解决外科医生对涂层剥离的担忧。随着医院对感染指标的监测日益密切,羟基磷灰石表面的生物活性特性带来了更多临床益处,推动热感喷涂市场稳定成长。

旋转设备和液压桿中硬铬镀层的替代品

REACH 和 OSHA 关于六价铬的法规日益严格,迫使原始设备製造商 (OEM) 寻求替代技术,高速火焰喷涂 (HVOF) 涂层成为一种永续的替代方案。 HVOF 涂层通常可达到 60 HRC 以上的硬度,同时将孔隙率降低到 1% 以下,使液压轴和压缩机叶轮的使用寿命延长一倍以上。维护成本的降低意味着製程工业停机成本的降低,从而增强了整体拥有成本 (TCO) 优势,推动了热感喷涂市场的普及。自动化臂架机械手使 HVOF 能够在难以触及的孔洞中进行喷涂,从而扩大了适用部件的范围。北美一家油气钻井船队的初步改造计画表明,投资回收期不到 18 个月,这促使亚洲铸造厂广泛采用该技术。随着 ESG审核收紧供应链评估标准,从镀铬槽转向无溶剂喷涂室可立即带来减少排放的益处。

推出高硬度三价铬涂层,只需少量资本投入即可实现。

新一代三价铬镀液仅需入门级高速火焰喷涂(HVOF)单元三分之一的投资即可达到50 HRC的硬度,对于成本敏感型市场的小规模液压桿修復商提案,极具吸引力。供应商强调其与现有工具的兼容性,无需新建通风和除尘系统。早期现场测试结果证实,对于运作低于200°C的齿轮轴,其耐腐蚀性良好,这抑制了这些细分市场近期对热感喷涂替代方案的需求。然而,三价铬难以应用于厚涂层,且不能应用于暴露于燃烧气体的零件。因此,它仍然主要作为航太和油气泵领域的热隔离层和耐磨覆盖层。所以,这项技术更被视为一种选择性阻碍因素,而非普遍威胁。

细分市场分析

预计到 2031 年,设备类别将以 6.06% 的复合年增长率成长,超过涂料的成长速度。涂料在 2025 年占据了整个热感喷涂市场 76.82% 的份额。配备六轴机器人和封闭回路型流量控制的自动化单元可将涂层之间的差异降低到 2µm 以下,这是涡轮机 OEM 为实现零计划外停机时间而设定的要求。

粉末和丝材的持续收入仍然至关重要,因为每沉积一公斤都会对更换喷嘴和等离子电极产生阻力。碳化钨钴粉末仍然是耐磨配方中的主流,但供不应求和价格波动促使人们更加关注能够延长喷嘴寿命的工艺配方和过喷回收技术。供应商目前正在推广模组化送料装置,这些装置可以在10分钟内完成细颗粒和粗颗粒之间的切换,从而提高工厂的柔软性。降噪室和旋风除尘器正经历两位数的成长率,这创造了一个辅助但盈利的细分市场,符合德国和韩国的工厂安全法规。

热感喷涂市场报告按产品类型(涂层、材料、热感喷涂设备)、热感喷涂涂层和表面处理方式(燃烧能和电能)、终端用户行业(航太、工业燃气涡轮机、汽车、电子、石油天然气等)以及地区(亚太、北美、欧洲、南美、中东和非洲)进行细分。市场预测以美元计价。

区域分析

预计到2025年,亚太地区将占热感喷涂市场34.20%的份额,年复合成长率达4.98%。这反映了中国半导体工厂的积极回流以及日本先进电池工厂的扩张。区域各国政府正在补贴智慧机械的进口,降低了采用自动化喷涂室的门槛。然而,技术纯熟劳工短缺问题依然存在,促使原始设备製造商(OEM)与印度和马来西亚的职业培训机构合作,这些机构提供基于ISO 14924标准的操作员认证。

北美和欧洲现有的飞机机队和严格的职业安全准则为无铬涂层的应用提供了支援。美国仍然是碳化钨粉末的最大单一买家,而德国则是电浆炬出口的主导。这两个地区都在加大对耐氢涂层研发的投入。

儘管南美和中东及非洲地区的绝对收入落后于其他地区,但与石化工厂升级和矿山输送机维修相关的设备订单正稳步增长,增速达两位数。因此,儘管每个地区的市场发展都受到不同终端市场驱动因素的影响,但全球热感喷涂市场正朝着数位化、环保型表面处理解决方案的通用方向发展。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 热感喷涂羟基磷灰石涂层在整形外科和牙科植入中的应用日益广泛

- 旋转设备和液压桿中硬铬镀层的替代品

- 新一代窄体飞机引擎对耐高温、轻质合金的需求

- 汽车产业向氢燃料内燃机和电动动力传动系统的转型,正在推动对耐磨气缸涂层的需求。

- 用于极端地热和太空应用的高熵合金(HEA)涂层

- 市场限制

- 低成本投资的兴起导致硬质三价铬电镀成本上升

- 亚洲和拉丁美洲合约加工商的工艺可重复性和熟练劳动力短缺问题

- 重要原料(碳化钨、钴、稀土元素氧化物)的价格波动风险与供应风险

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 依产品类型

- 涂层

- 材料

- 涂层材料

- 粉末

- 陶瓷

- 金属

- 聚合物和其他粉末

- 线材/桿

- 其他涂层材料

- 粉末

- 补充资料(辅助资料)

- 涂层材料

- 热感喷涂设备

- 热感喷涂系统

- 除尘器

- 喷枪和喷嘴

- 送料设备

- 备用零件

- 隔音罩

- 其他热感喷涂设备

- 热感喷涂涂层和表面处理

- 燃烧

- 电能

- 按最终用户行业划分

- 航太

- 工业用燃气涡轮机

- 车

- 电子设备

- 石油和天然气

- 医疗设备

- 能源与电力

- 其他终端用户产业

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 土耳其

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 卡达

- 阿拉伯聯合大公国

- 奈及利亚

- 埃及

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Thermal Spray Coatings Companies

- APS Materials, Inc.

- ASB Industries Inc

- BODYCOTE

- CHROMALLOY GAS TURBINE LLC

- Curtiss-Wright Corporation

- Fisher Barton

- FM Industries

- Lincotek Trento SpA

- Linde PLC

- OC Oerlikon Management AG

- Thermion

- TOCALO Co., Ltd.

- Thermal Spray Equipment Companies

- Aimtek, Inc.

- Air Products and Chemicals, Inc.

- Arzell, Inc.

- Camfil

- Castolin Eutectic

- CenterLine(Windsor)Limited

- Donaldson Company, Inc.

- Flame Spray Technologies BV

- GTV VerschleiBschutz GmbH

- HAI Inc

- Hannecard Roller Coatings, Inc.-ASB Industries

- Imperial Systems, Inc.

- Kennametal Inc

- Lincoteck Equipment SPA

- Linde PLC

- Metalizing Equipment Co Pvt Ltd

- Metallisation Limited

- OC Oerlikon Management AG

- Powder Feed Dynamics, Inc

- Progressive Surface

- Saint-Gobain

- Surface Technology Services BV

- Thermion

- Thermal Spray Materials Companies

- AIM MRO Holdings, LLC.

- Aimtek, Inc.

- AlSher APM, LLC

- AMETEK, Inc.

- C&M Technologies GmbH

- Castolin Eutectic

- CenterLine(Windsor)Limited

- Elmet Technologies

- Fisher Barton

- Global Tungsten & Powders

- HAI Inc

- Hoganas AB

- Hunter Chemical, LLC

- Kennametal Inc

- Linde PLC

- LSN Diffusion Limited

- Metallisation Limited

- Metallizing Equipment Co. Pvt. Ltd

- OC Oerlikon Management AG

- Polymet

- Powder Alloy Corporation

- Saint-Gobain

- Sandvik AB

- Thermion

- Thermal Spray Coatings Companies

第七章 市场机会与未来展望

The Thermal Spray market is expected to grow from USD 11.87 billion in 2025 to USD 12.36 billion in 2026 and is forecast to reach USD 15.15 billion by 2031 at 4.15% CAGR over 2026-2031.

Demand is rising as aerospace, medical-device, and next-generation automotive manufacturers replace legacy surface treatments with high-performance coatings that extend part life and improve thermal management. Investments in automated equipment and real-time process monitoring continue to ease skilled-labor constraints, while the shift to electric energy spray techniques aligns with tightening environmental regulations. The Asia-Pacific manufacturing base is expanding rapidly, driving regional consumption of both coating materials and turnkey spray cells aimed at electronics and e-powertrain components.

Global Thermal Spray Market Trends and Insights

Increasing Use of Thermally-Sprayed Hydroxyapatite Coatings in Orthopedic and Dental Implants

Thermally-sprayed hydroxyapatite coatings significantly improve bone ingrowth and reduce rejection rates, making them the preferred surface finish for load-bearing orthopedic screws, hip stems, and dental fixtures. Process control enables tailored porosity that matches cancellous bone morphology, accelerating osseointegration and shortening rehabilitation periods. Regulatory acceptance under U.S. FDA class II devices and CE marking frameworks supports rapid adoption among global implant makers. Growing geriatric populations in the United States, Germany, and Japan keep procedural volumes expanding, sustaining raw-material demand for calcium-phosphate powders. Equipment suppliers now bundle closed-loop robots and inline thickness gauges that assure repeatability, addressing surgeon concerns regarding coating delamination. As hospitals track infection metrics more closely, the bioactive nature of hydroxyapatite surfaces provides an additional clinical advantage that keeps the thermal spray market on a steady upswing.

Replacement of Hard-Chrome Plating in Rotating Equipment and Hydraulic Rods

Tightening REACH and OSHA rules on hexavalent chromium have forced OEMs to seek alternatives, positioning high-velocity oxygen fuel (HVOF) coatings as the sustainable successor. HVOF layers routinely exceed 60 HRC hardness while slashing porosity below 1%, more than doubling component lifetimes for hydraulic shafts and compressor impellers. Reduced maintenance translates into lower down-time costs for process industries, bolstering the total cost-of-ownership argument in favor of thermal spray market adoption. Automated boom manipulators now apply HVOF inside hard-to-reach bores, extending the addressable part universe. Early conversion programs in North American oil-and-gas drill fleets demonstrated payback periods under 18 months, spurring wider replication in Asian foundries. As ESG auditors tighten supply-chain scorecards, the switch from chrome baths to solvent-free spray booths provides an immediate emissions win.

Emergence of Hard Trivalent Chrome Coatings with Lower CAPEX

Next-generation trivalent chrome baths provide 50 HRC hardness at investment levels one-third those of an entry-level HVOF cell, a value proposition that appeals to small hydraulic-rod refurbishers in cost-sensitive markets. Suppliers emphasize drop-in compatibility with existing fixtures, eliminating the need for new ventilation or dust-collection systems. Early field results confirm acceptable corrosion resistance for gear shafts operating below 200 °C, blunting near-term replacements by the thermal spray market in those niches. However, trivalent chrome struggles at higher thicknesses and cannot serve components exposed to combustion gases, which preserves the advantage for thermal barrier and wear-resistant overlays in aerospace as well as oil-and-gas pumps. The technology therefore acts as a selective restraint rather than a universal threat.

Other drivers and restraints analyzed in the detailed report include:

- Demand for High-Temperature Lightweight Alloys in Next-Gen Narrow-Body Aircraft Engines

- Automotive Shift Toward Hydrogen ICE and E-Powertrains Requiring Wear-Resistant Cylinder Coatings

- Process Repeatability and Skilled-Operator Shortage in Asia and Latin America Job-Shops

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The equipment category is projected to expand at a 6.06% CAGR through 2031, surpassing consumables in growth momentum even though coatings retained a 76.82% share of the overall thermal spray market in 2025. Automated cells equipped with six-axis robots and closed-loop mass-flow control reduce coat-to-coat variance below 2 µm, a requirement set by turbine OEMs aiming for zero unplanned downtime.

Recurring revenues from powders and wires remain pivotal, as every kilogram deposited creates a pull-through effect for replacement nozzles and plasma electrodes. Tungsten carbide-cobalt powders continue to dominate wear-protection formulas, but scarcity and price volatility have sparked process recipes that extend tip life or recycle overspray. Suppliers now promote modular feeder units that switch between fine and coarse fractions in under 10 minutes, enhancing shop flexibility. Noise-attenuating booths and cyclone-based dust collectors clock double-digit growth rates, an ancillary but lucrative niche aligned with factory-safety mandates in Germany and South Korea.

The Thermal Spray Report is Segmented by Product Type (Coatings, Materials, and Thermal-Spray Equipment), Thermal Spray Coatings and Finishes (Combustion and Electric Energy), End-User Industry (Aerospace, Industrial Gas Turbines, Automotive, Electronics, Oil and Gas, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific contributed 34.20% of the thermal spray market in 2025 and is forecast to climb at a 4.98% CAGR, reflecting aggressive onshoring of semiconductor fabs in China and advanced battery plants in Japan. Regional governments channel subsidies into smart-machinery imports, lowering payback barriers for automated spray booths. Still, the skilled-labor gap persists, pushing OEMs to partner with vocational institutes in India and Malaysia that offer operator certification under ISO 14924 standards.

North America and Europe are underpinned by legacy aerospace fleets and strict occupational safety guidelines favoring chrome-free overlays. The United States remains the largest single-country buyer of tungsten carbide powders, while Germany leads in plasma-torch exports. Both regions invest in research and development focused on hydrogen-compatible coatings.

South America and the Middle East and Africa trail in absolute revenues but post steady double-digit equipment orders linked to petrochemical plant upgrades and mining conveyor refurbishments. Each geography therefore plays to distinct end-market triggers, yet converges on a common trajectory of digitalized and environmentally compliant surface-engineering solutions within the global thermal spray market.

- Thermal Spray Coatings Companies

- Thermal Spray Equipment Companies

- Thermal Spray Materials Companies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing use of thermally-sprayed hydroxyapatite coatings in orthopedic and dental implants

- 4.2.2 Replacement of hard-chrome plating in rotating equipment and hydraulic rods

- 4.2.3 Demand for high-temperature lightweight alloys in next-gen narrow-body aircraft engines

- 4.2.4 Automotive shift toward hydrogen ICE and e-powertrains requiring wear-resistant cylinder coatings

- 4.2.5 Adoption of high-entropy alloy (HEA) coatings for extreme geothermal and space applications

- 4.3 Market Restraints

- 4.3.1 Emergence of hard trivalent chrome coatings with lower CAPEX

- 4.3.2 Process repeatability and skilled-operator shortage in Asia and LATAM job-shops

- 4.3.3 Volatile pricing and supply risk for critical feedstocks (WC-Co, rare-earth oxides)

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Coatings

- 5.1.2 Materials

- 5.1.2.1 Coating Materials

- 5.1.2.1.1 Powders

- 5.1.2.1.1.1 Ceramics

- 5.1.2.1.1.2 Metals

- 5.1.2.1.1.3 Polymers and Other Powders

- 5.1.2.1.2 Wires/Rods

- 5.1.2.1.3 Other Coating Materials

- 5.1.2.1.1 Powders

- 5.1.2.2 Supplementary Materials (Auxiliary Material)

- 5.1.2.1 Coating Materials

- 5.1.3 Thermal-Spray Equipment

- 5.1.3.1 Thermal Spray Coating Systems

- 5.1.3.2 Dust Collection Equipment

- 5.1.3.3 Spray Guns and Nozzles

- 5.1.3.4 Feeder Equipment

- 5.1.3.5 Spare Parts

- 5.1.3.6 Noise-reducing Enclosures

- 5.1.3.7 Other Thermal Spray Equipment

- 5.2 By Thermal Spray Coatings and Finishes

- 5.2.1 Combustion

- 5.2.2 Electric Energy

- 5.3 By End-user Industry

- 5.3.1 Aerospace

- 5.3.2 Industrial Gas Turbines

- 5.3.3 Automotive

- 5.3.4 Electronics

- 5.3.5 Oil and Gas

- 5.3.6 Medical Devices

- 5.3.7 Energy and Power

- 5.3.8 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Qatar

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Thermal Spray Coatings Companies

- 6.4.1.1 APS Materials, Inc.

- 6.4.1.2 ASB Industries Inc

- 6.4.1.3 BODYCOTE

- 6.4.1.4 CHROMALLOY GAS TURBINE LLC

- 6.4.1.5 Curtiss-Wright Corporation

- 6.4.1.6 Fisher Barton

- 6.4.1.7 FM Industries

- 6.4.1.8 Lincotek Trento S.p.A.

- 6.4.1.9 Linde PLC

- 6.4.1.10 OC Oerlikon Management AG

- 6.4.1.11 Thermion

- 6.4.1.12 TOCALO Co., Ltd.

- 6.4.2 Thermal Spray Equipment Companies

- 6.4.2.1 Aimtek, Inc.

- 6.4.2.2 Air Products and Chemicals, Inc.

- 6.4.2.3 Arzell, Inc.

- 6.4.2.4 Camfil

- 6.4.2.5 Castolin Eutectic

- 6.4.2.6 CenterLine (Windsor) Limited

- 6.4.2.7 Donaldson Company, Inc.

- 6.4.2.8 Flame Spray Technologies B.V.

- 6.4.2.9 GTV VerschleiBschutz GmbH

- 6.4.2.10 HAI Inc

- 6.4.2.11 Hannecard Roller Coatings, Inc. - ASB Industries

- 6.4.2.12 Imperial Systems, Inc.

- 6.4.2.13 Kennametal Inc

- 6.4.2.14 Lincoteck Equipment SPA

- 6.4.2.15 Linde PLC

- 6.4.2.16 Metalizing Equipment Co Pvt Ltd

- 6.4.2.17 Metallisation Limited

- 6.4.2.18 OC Oerlikon Management AG

- 6.4.2.19 Powder Feed Dynamics, Inc

- 6.4.2.20 Progressive Surface

- 6.4.2.21 Saint-Gobain

- 6.4.2.22 Surface Technology Services BV

- 6.4.2.23 Thermion

- 6.4.3 Thermal Spray Materials Companies

- 6.4.3.1 AIM MRO Holdings, LLC.

- 6.4.3.2 Aimtek, Inc.

- 6.4.3.3 AlSher APM, LLC

- 6.4.3.4 AMETEK, Inc.

- 6.4.3.5 C&M Technologies GmbH

- 6.4.3.6 Castolin Eutectic

- 6.4.3.7 CenterLine (Windsor) Limited

- 6.4.3.8 Elmet Technologies

- 6.4.3.9 Fisher Barton

- 6.4.3.10 Global Tungsten & Powders

- 6.4.3.11 HAI Inc

- 6.4.3.12 Hoganas AB

- 6.4.3.13 Hunter Chemical, LLC

- 6.4.3.14 Kennametal Inc

- 6.4.3.15 Linde PLC

- 6.4.3.16 LSN Diffusion Limited

- 6.4.3.17 Metallisation Limited

- 6.4.3.18 Metallizing Equipment Co. Pvt. Ltd

- 6.4.3.19 OC Oerlikon Management AG

- 6.4.3.20 Polymet

- 6.4.3.21 Powder Alloy Corporation

- 6.4.3.22 Saint -Gobain

- 6.4.3.23 Sandvik AB

- 6.4.3.24 Thermion

- 6.4.1 Thermal Spray Coatings Companies

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

基于氧化钇的等离子喷涂粉末市场:按产品类型、製程类型、氧化钇含量范围、涂层厚度和最终用途产业划分,全球预测(2026-2032年)

基于氧化钇的等离子喷涂粉末市场:按产品类型、製程类型、氧化钇含量范围、涂层厚度和最终用途产业划分,全球预测(2026-2032年) 2026年全球热感喷涂市场报告热喷涂设备市场(依製程、最终用途产业、应用、材料与设备类型划分)-2025-2032年全球预测

2026年全球热感喷涂市场报告热喷涂设备市场(依製程、最终用途产业、应用、材料与设备类型划分)-2025-2032年全球预测 全球热喷涂材料市场

全球热喷涂材料市场 热喷涂设备:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

热喷涂设备:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年) 热喷涂市场规模、份额和成长分析(按材料、技术、应用和地区)- 产业预测 2025-2032热喷涂材料:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

热喷涂市场规模、份额和成长分析(按材料、技术、应用和地区)- 产业预测 2025-2032热喷涂材料:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年) 全球热喷涂材料市场(2024-2028)

全球热喷涂材料市场(2024-2028) 2024 - 2032 年热喷涂服务市场机会、成长动力、产业趋势分析与预测热喷涂设备市场机会、成长动力、产业趋势分析与预测 2024 - 2032

2024 - 2032 年热喷涂服务市场机会、成长动力、产业趋势分析与预测热喷涂设备市场机会、成长动力、产业趋势分析与预测 2024 - 2032