|

市场调查报告书

商品编码

1939162

混凝土外加剂:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Concrete Admixtures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

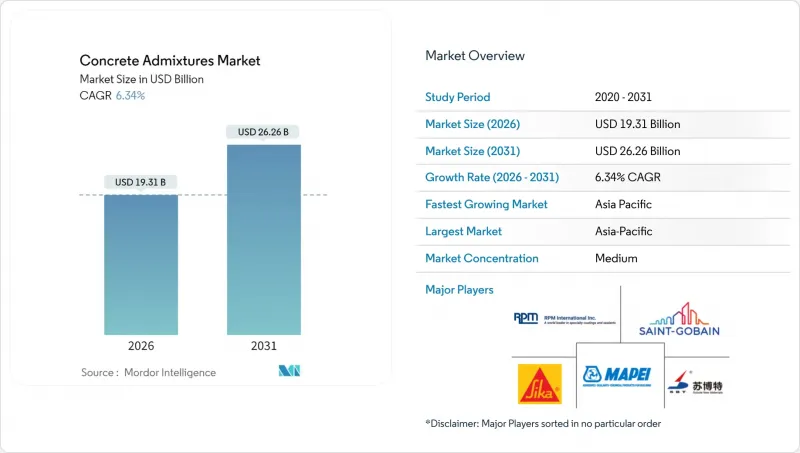

2025年混凝土外加剂市场价值为181.6亿美元,预计到2031年将达到262.6亿美元,而2026年为193.1亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 6.34%。

亚太地区政府主导的基础设施项目、已开发国家严格的节水标准以及自密实混凝土的快速普及推动了市场成长。自密实混凝土在提高生产效率的同时,也减少了材料浪费。建筑商越来越多地采用人工智慧辅助配料平台,这有助于提高混凝土混合料的均匀性,并减少外加剂的过度使用。住宅产业的復苏以及消费者对生物基化学品的日益青睐,也为市场创造了更多成长机会。由于全球供应商专注于聚合物技术的专利申请和数位化能力的整合,市场竞争强度仍然适中。而本地製造商则凭藉其物流优势和对当地法规的熟悉程度,占据了一定的市场定位。然而,石化原料价格的波动以及甲醛排放法规的不断变化,可能会带来短期成本和合规方面的挑战,导致利润率下降和配方研发週期延长。

全球混凝土外加剂市场趋势与洞察

亚太地区的大型计划

政府在区域铁路走廊、机场和智慧城市项目上的支出正在重新定义规范标准,从而推动了对能够在不同气候带保持坍落度和耐久性的外加剂的需求。中国的「一带一路」倡议正在扩大跨境计划储备,而印尼的新首都规划和印度的国家基础设施规划则推动了稳定的订单前景。计划业主倾向于选择即使在长途运输下也能保持流变性能的高品质添加剂,这使得拥有技术文件的供应商能够获得更高的利润率。由于公共竞标不再仅仅列出商品等级,而是采用性能条款,并且经过价值工程优化的替代方案必须通过严格的测试通讯协定,混凝土外加剂市场正受益于平均售价的上涨。

快速铺设高性能混凝土和自密实混凝土

随着承包商寻求节省人工成本和确保可靠的质量,自密实混凝土的应用正从预製件转向现场浇筑。自密实混凝土的浇筑週期缩短高达 40%,表面缺陷显着减少,因此正成为高层建筑核心筒和复杂模板工程的首选材料。抗压强度目标超过 8,000 psi 的计划越来越多地采用高效减水剂与水泥基钢筋结合使用,混凝土外加剂市场也正朝着更先进的技术支援方案发展。欧洲耐久性标准作为全球参考标准,促使在北美和亚洲营运的跨国公司满足更严格的混凝土混合料性能标准。

石油化学原料价格波动

乙烯和丙烯衍生物季度价格波动超过30%,直接推高了高效减水剂的成本结构,尤其对于缺乏避险能力的生产商而言更是如此。物流附加费和关税加剧了区域差异,造成现货价格差异,并使竞标报价更加复杂。中小企业难以应对这些衝击,在某些情况下,甚至会因拥有长期合约的大型垂直整合企业而失去市场份额。因此,混凝土外加剂市场正经历暂时的利润空间压缩,并促使市场对更高的预付价格和非石油基替代品产生兴趣。

细分市场分析

2025年,基础设施领域在混凝土外加剂市场中占据39.62%的份额,主要得益于政府在交通走廊和公共产业升级方面的支出。受疫情期间住宅奖励策略的支持,住宅正以6.78%的复合年增长率增长,预计到2031年将缩小与基础设施领域的差距。住宅领域混凝土外加剂市场的扩张与预製板的采用密切相关,预製板对混凝土混合料的均匀性要求很高。在独栋住宅的地基工程中,为了提高耐久性并抑制泌水(外加剂分离),减水剂的使用日益增加。同时,为了确保混凝土的泵送性能,高性能减水剂也被应用于30层以上的高层多用户住宅。

商业计划(尤其是办公大楼维修和资料中心)约占总需求的四分之一,这类专案偏好兼具早期强度和低收缩率的添加剂。工业和公共建筑项目则占剩余部分,这类项目要求地板材料和结构构件具备耐化学腐蚀性能。市场结构表明,公共工程项目的基础设施需求稳定,而房屋抵押贷款市场的繁荣和都市区人口密度增加的趋势可能带来住宅。

区域分析

预计到2025年,亚太地区将占混凝土外加剂市场31.58%的份额,复合年增长率(CAGR)为6.79%。中国仍然是核心市场,但监管政策的转变,尤其是对品质和环境管理的重视,正在推动市场对符合数十年耐久性标准的高品质外加剂的需求。大规模交通基础设施和城市发展项目正在推动印度和印尼的市场成长,而日本和韩国则在采用数位化配料技术方面处于领先。儘管区域供应商享有物流优势,但性能标准的国际化正在推动外国高效减水剂品牌的渗透。

北美成熟的建筑生态系统持续保持稳定的需求,这主要得益于基础设施维修和住宅开工。劳动力短缺推动了自密实混凝土的应用,使得数位化配料控製成为大型预拌混凝土车队的必备条件。联邦基础设施立法推动了桥樑和道路维修支出的增加,进而带动了外加剂需求转移到防腐蚀和减少收缩类别。

欧洲市场份额的成长主要得益于欧盟分类法等严格的永续性法规,这些法规推动了碳优化混凝土混合料的使用。德国和英国的消费成长主要源自于铁路扩建和城市更新项目,而法国和义大利则致力于推广需要统一颜色和裸露饰面的建筑应用。在东欧,由凝聚基金支持的高速公路计划为成长提供了空间,低渗透性混凝土的规格也日益增加。

南美洲、中东和非洲的总合份额较小,但受巴西和阿联酋等大型企划计画的推动,部分地区实现了两位数的成长。汇率波动和商品週期使采购变得复杂,但由于进口关税优惠政策,当地生产商通常能够维持较高的运转率。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 亚太地区的大型计划

- 高性能混凝土和自密实混凝土(SCC)的快速普及

- 更严格的节水剂法规

- 基于人工智慧的积层製造优化平台

- 由农业废弃物製成的生物基添加剂

- 市场限制

- 石化原料价格波动

- 一种低成本的传统混凝土替代方案

- 违反甲醛排放法规的风险

- 价值链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 应用领域

- 商业的

- 工业和机构

- 基础设施

- 住宅

- 依产品类型

- 加速器

- 空气引射器

- 高效减水剂(超塑化剂)

- 缓速器

- 收缩抑制

- 黏度调节剂

- 减水剂(增塑剂)

- 其他类型

- 按地区

- 亚太地区

- 澳洲

- 中国

- 印度

- 印尼

- 日本

- 马来西亚

- 韩国

- 泰国

- 越南

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- CEMEX SAB de CV

- CICO Group

- CMB

- Guangdong Redwall New Materials Co.,Ltd

- Jiangsu Subote New Materials Co., Ltd.

- Kao Corporation

- MAPEI SpA

- MC-Bauchemie

- MUHU(China)Construction Materials Co., Ltd.

- Pidilite Industries Limited

- RPM International

- Saint-Gobain

- Sika AG

- SOCHEM

- Xypex Chemical Corp.

第七章 市场机会与未来展望

第八章:执行长面临的关键策略问题

The Concrete Admixtures Market was valued at USD 18.16 billion in 2025 and estimated to grow from USD 19.31 billion in 2026 to reach USD 26.26 billion by 2031, at a CAGR of 6.34% during the forecast period (2026-2031).

The market's growth is driven by government-backed infrastructure programs in the Asia-Pacific region, stricter water-reduction standards in developed economies, and the rapid adoption of self-consolidating concrete, which boosts productivity while reducing material waste. Contractors are broadening the adoption of AI-guided dosage platforms, which refine mix consistency and trim admixture overuse. The residential sector's rebound and mounting preference for bio-based chemistries further widen opportunity windows. Competitive intensity remains moderate because regional producers occupy niche positions based on logistics advantages and local regulatory familiarity, even as global suppliers strive to patent polymer innovations and integrate digital features. Volatile petrochemical feedstock prices and evolving formaldehyde emission limits pose short-term cost and compliance challenges that can squeeze margins and lengthen formulation timelines.

Global Concrete Admixtures Market Trends and Insights

Infrastructure Mega-Projects in Asia-Pacific

Government outlays for regional rail corridors, airports, and smart-city programs are redefining specification criteria, moving demand toward admixtures that deliver extended slump retention and durability across varied climatic zones. China's Belt and Road Initiative amplifies cross-border project pipelines, while Indonesia's new capital and India's National Infrastructure Pipeline add steady order visibility. Project owners favor premium additives that maintain rheology under long haul times, enabling suppliers with technical documentation to secure higher margins. The concrete admixtures market benefits from average selling price uplift because public tenders list performance clauses rather than commodity grades, and value-engineered alternatives must clear rigorous test protocols.

Rapid Adoption of High-Performance and SCC Concrete

Self-consolidating concrete has shifted from precast exclusivity to cast-in-place usage as contractors seek labor savings and quality reliability. Placement cycle times decrease by up to 40%, and surface defects noticeably drop, making SCC a preferred option in high-rise cores and complex formwork applications. Projects exceeding 8,000 psi compressive strength targets increasingly combine superplasticizers with supplementary cementitious materials, nudging the concrete admixtures market toward higher technical support bundles. European durability codes act as global reference points, pushing multinationals operating in North America and Asia to align with stricter mix performance thresholds.

Volatile Petrochemical Feedstock Prices

Quarterly swings of 30% or more in ethylene and propylene derivatives directly inflate superplasticizer cost structures, especially for producers without hedging capacity. Logistics surcharges and customs duties exacerbate regional disparities, resulting in spot-price spreads that complicate tender quotations. Smaller enterprises struggle to absorb shocks, sometimes ceding share to vertically integrated majors that lock in term contracts. The concrete admixtures market thus faces temporary margin compression and heightened interest in non-petroleum alternatives, albeit at higher initial price points.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Water-Reduction Regulations

- AI-Guided Dosage Optimization Platforms

- Formaldehyde-Emission Compliance Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The infrastructure segment retained 39.62% of the concrete admixtures market share in 2025, fueled by sovereign spending on transit corridors and utility upgrades. Residential construction, aided by pandemic-era housing stimulus packages, is progressing at a 6.78% CAGR and is on track to narrow the gap by 2031. The expansion of the concrete admixtures market size in housing aligns with the adoption of prefabricated panels, where stringent mix consistency is crucial. Single-family foundations increasingly specify water-reducing agents that cut bleed while boosting durability, whereas multifamily towers incorporate superplasticizers for pumpability at heights exceeding 30 stories.

Commercial projects, notably office retrofits and data centers, occupy about one-quarter of demand, selecting admixtures that balance early strength with low-shrinkage finishes. Industrial and institutional builds round out the remainder, seeking chemical resistance in floors and structural components. The segment mix implies stable base volume from public works, with upside from a healthier mortgage market and urban residential densification trends.

The Concrete Admixtures Market Report is Segmented by End-Use Sector (Commercial, Industrial and Institutional, Infrastructure, and Residential), Product Type (Accelerator, Air-Entraining, High-Range Water-Reducer, Retarder, Shrinkage-Reducing, Viscosity Modifier, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

The Asia-Pacific region carried 31.58% of the concrete admixtures market in 2025 and is projected to grow at a 6.79% CAGR. China remains pivotal, yet its regulatory shift toward quality and environmental stewardship intensifies demand for premium admixtures that meet multi-decade durability benchmarks. India and Indonesia provide incremental momentum through marquee transport and city-building programs, while Japan and South Korea lead the way in digital batching adoption. Regional suppliers benefit from lower logistics hurdles; however, the penetration of foreign superplasticizer brands widens as performance standards integrate international norms.

North America's mature construction ecosystem registers steady volume tied to infrastructure refurbishments and residential starts. Labor constraints have driven the adoption of self-consolidating concrete, making digital dosage control a must-have in large ready-mix fleets. Federal infrastructure bills shift spending toward bridge and roadway rehabilitation, steering admixture demand toward corrosion-inhibiting and shrinkage-reducing categories.

Europe's share stems from robust sustainability regulations, such as the EU Taxonomy, which push for carbon-optimized mixes. Germany and the United Kingdom lead the way in consumption, with rail extensions and urban renewal plans, whereas France and Italy are advancing architectural applications that require color consistency and exposed finishes. Eastern Europe offers growth headroom through cohesion fund-backed highway projects, which increasingly stipulate low-permeability concrete.

South America, the Middle East, and Africa collectively hold a smaller slice, yet they provide pockets of double-digit expansion aligned with megaproject calendars in Brazil and the UAE. Currency fluctuations and commodity cycles complicate procurement; yet, local producers often secure higher utilization rates thanks to import tariffs that favor domestic sourcing.

- CEMEX S.A.B. de C.V.

- CICO Group

- CMB

- Guangdong Redwall New Materials Co.,Ltd

- Jiangsu Subote New Materials Co., Ltd.

- Kao Corporation

- MAPEI S.p.A.

- MC-Bauchemie

- MUHU (China) Construction Materials Co., Ltd.

- Pidilite Industries Limited

- RPM International

- Saint-Gobain

- Sika AG

- SOCHEM

- Xypex Chemical Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infrastructure mega-projects in Asia-Pacific

- 4.2.2 Rapid adoption of high-performance and SCC concrete

- 4.2.3 Stricter water-reduction regulations

- 4.2.4 AI-guided dosage optimisation platforms

- 4.2.5 Bio-based admixtures from agri-waste streams

- 4.3 Market Restraints

- 4.3.1 Volatile petro-chemical feedstock prices

- 4.3.2 Low-cost conventional concrete alternatives

- 4.3.3 Formaldehyde-emission compliance risks

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By End-Use Sector

- 5.1.1 Commercial

- 5.1.2 Industrial and Institutional

- 5.1.3 Infrastructure

- 5.1.4 Residential

- 5.2 By Product Type

- 5.2.1 Accelerator

- 5.2.2 Air-Entraining

- 5.2.3 High-Range Water-Reducer (Superplasticizer)

- 5.2.4 Retarder

- 5.2.5 Shrinkage-Reducing

- 5.2.6 Viscosity Modifier

- 5.2.7 Water-Reducer (Plasticizer)

- 5.2.8 Other Types

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 Australia

- 5.3.1.2 China

- 5.3.1.3 India

- 5.3.1.4 Indonesia

- 5.3.1.5 Japan

- 5.3.1.6 Malaysia

- 5.3.1.7 South Korea

- 5.3.1.8 Thailand

- 5.3.1.9 Vietnam

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/ Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 CEMEX S.A.B. de C.V.

- 6.4.2 CICO Group

- 6.4.3 CMB

- 6.4.4 Guangdong Redwall New Materials Co.,Ltd

- 6.4.5 Jiangsu Subote New Materials Co., Ltd.

- 6.4.6 Kao Corporation

- 6.4.7 MAPEI S.p.A.

- 6.4.8 MC-Bauchemie

- 6.4.9 MUHU (China) Construction Materials Co., Ltd.

- 6.4.10 Pidilite Industries Limited

- 6.4.11 RPM International

- 6.4.12 Saint-Gobain

- 6.4.13 Sika AG

- 6.4.14 SOCHEM

- 6.4.15 Xypex Chemical Corp.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

8 Key Strategic Questions for CEOS

混凝土外加剂市场:按类型、原料、形态、应用和最终用户划分-2026-2032年全球市场预测

混凝土外加剂市场:按类型、原料、形态、应用和最终用户划分-2026-2032年全球市场预测 2026年全球减缩剂市场报告2026年全球混凝土外加剂市场报告

2026年全球减缩剂市场报告2026年全球混凝土外加剂市场报告 亚太地区混凝土外加剂:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

亚太地区混凝土外加剂:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 全球混凝土外加剂市场规模、份额、趋势和成长分析报告(2026-2034年)2026年全球多羧酸减水剂市场报告

全球混凝土外加剂市场规模、份额、趋势和成长分析报告(2026-2034年)2026年全球多羧酸减水剂市场报告 混凝土外加剂市场规模、份额和趋势分析报告:按类型、地区和细分市场预测(2026-2033 年)生物基混凝土外加剂市场:按类型、原料来源、通路和应用划分,全球预测(2026-2032年)全球水泥粉煤灰市场:市场规模、占有率、成长率、产业分析、类型、应用及区域分析,未来预测(2026-2034)

混凝土外加剂市场规模、份额和趋势分析报告:按类型、地区和细分市场预测(2026-2033 年)生物基混凝土外加剂市场:按类型、原料来源、通路和应用划分,全球预测(2026-2032年)全球水泥粉煤灰市场:市场规模、占有率、成长率、产业分析、类型、应用及区域分析,未来预测(2026-2034) 生物基混凝土外加剂市场规模、份额及成长分析(依产品类型、原料、应用及地区划分)-2026-2033年产业预测

生物基混凝土外加剂市场规模、份额及成长分析(依产品类型、原料、应用及地区划分)-2026-2033年产业预测