|

市场调查报告书

商品编码

1939611

平板玻璃:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Flat Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

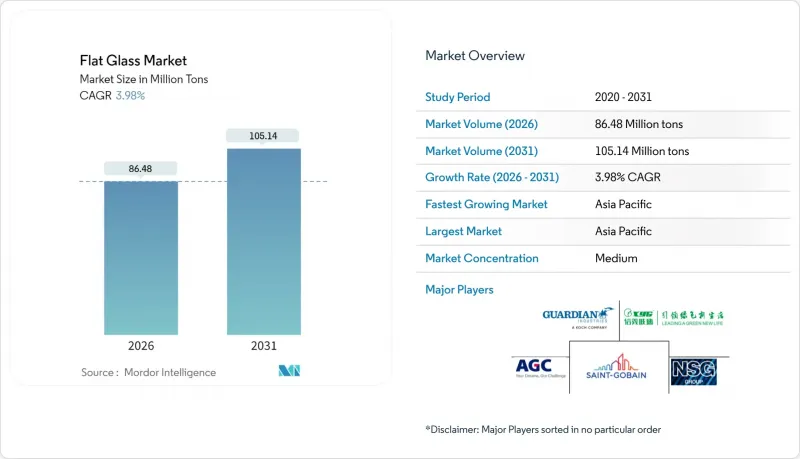

预计平板玻璃市场将从 2025 年的 8,317 万吨增长到 2026 年的 8,648 万吨,到 2031 年将达到 1.0514 亿吨,2026 年至 2031 年的复合年增长率为 3.98%。

更严格的建筑能源标准、太阳能光电发电装置的快速扩张以及对先进玻璃产品需求旺盛的轻型车辆,共同推动了市场对玻璃的强劲需求。製造商正转向低碳熔炼、绿氢能试点计画以及氧电混合熔炉,以确保在永续性的竞标中获得溢价。用于光学模组的玻璃、用于医疗设施的抗菌涂层以及用于高层建筑维修的超薄三层玻璃,都丰富了玻璃产品的收入来源。亚太地区是玻璃生产和消费的核心区域,而北美和欧洲则正在投资熔炉电气化改造,以应对能源价格波动和即将到来的碳排放关税。

全球平板玻璃市场趋势及展望

加大对商业和住宅建筑的投资

受借贷成本下降和开发商景气增强的推动,全球建筑支出预计将会增加。独栋住宅价格上涨正推动多用户住宅加速成长,从而持续刺激对采用Low-E低辐射镀膜玻璃和三层中空玻璃的幕墙和窗户系统的需求。开发商为获得LEED认证而指定使用高性能玻璃,这进一步推高了对溅镀膜和充氩气隔热产品的需求。建筑规范中对窗墙比的限制鼓励采用先进的玻璃解决方案,因此直接惠及平板玻璃市场。

由于电动车的安全性和轻量化,对汽车玻璃的需求增加。

电动车平台推动了对结构玻璃的需求,同时也促使人们采用轻质玻璃来抵消电池重量。福耀集团决定在2024年投资91亿元人民币(约12.6亿美元)新建两座工厂,以满足新能源车的需求。超薄夹层挡风玻璃、全景天窗和抬头显示器挡风玻璃等产品正在推动加工玻璃的应用。感测器组件的整合提高了单车附加价值,在平板玻璃市场中形成了一个盈利的成长领域。更薄的玻璃带来的空气动力学性能提升也有助于优化续航里程,巩固了玻璃在预测期内作为轻量化关键基材的地位。

聚合物、丙烯酸和聚碳酸酯替代品的兴起

汽车製造商正在试用聚碳酸酯侧窗和全景天窗,其重量比同类玻璃面板轻50%。虽然聚碳酸酯具有更高的光学清晰度和紫外线稳定性,但其耐刮擦性和耐热性仍不如玻璃。严格的挡风玻璃法规限制了聚碳酸酯的应用,而替代风险主要集中在非承重玻璃领域。玻璃回收的优点以及更严格的报废循环利用目标将进一步保障平板玻璃的市场规模。

细分市场分析

从2026年到2031年,加工玻璃将以4.65%的复合年增长率(CAGR)实现最快成长,超过整体平板玻璃市场。夹层玻璃和强化玻璃广泛应用于对抗衝击性要求极高的应用领域,例如汽车挡风玻璃、帷幕墙和安全建筑幕墙。截至2025年,钢化玻璃的产量仍将占据主导地位,占总产量的79.62%,因为它是下游加工的基础。该细分市场的成本优势将确保其在通用建筑领域继续保持核心地位,但随着更严格的建筑和安全规范增加对增值加工的需求,其市场份额预计将会放缓。

强制性隔热标准正推动镀膜玻璃、反射玻璃和Low-E低辐射镀膜玻璃的同步发展。 AGC Glass Europe 的「5.5 kg CO2 eq/m2 低碳玻璃」便是产品差异化并获得溢价的典范。在电动车 (EV) 中使用有色玻璃有助于车内降温并提高电池效率。镜面玻璃和图案玻璃虽然仍属于小众市场,但在室内装潢和隐私保护方面的需求正在不断增长。总体而言,预计日益专业化的趋势将推高平均售价,并使加工产品在预测期内扩大其在平板玻璃市场的份额。

平板玻璃市场报告按产品类型(冷加工玻璃、镀膜玻璃、加工玻璃、镜面玻璃、压花玻璃)、终端用户产业(建筑、汽车、太阳能玻璃及其他终端用户产业)和地区(亚太、北美、欧洲、南美、中东和非洲)进行细分。市场预测以吨为单位。

区域分析

到2025年,亚太地区将占全球出货量的63.88%,年复合成长率最高,达4.63%。在印度,根据旭硝子印度玻璃公司与INOX空气产品公司签署的为期20年的承购协议,一项新的浮法生产线扩建专案和绿色氢反应器测试正在进行中。

欧洲致力于引领脱碳进程。在欧盟创新基金的支持下,圣戈班和AGC已开始测试一种混合式炉,该炉采用50%的电气化和富氧燃烧技术,可减少75%的二氧化碳排放。将于2026年生效的碳边境调节机制(CBAM)附加税有望鼓励在地采购,并可能促进区域内销售。北美製造商正在升级生产线,以增强其应对天然气价格波动和环境、社会及公司治理(ESG)监管的能力,其中以Vitro公司1.8亿美元的现代化计画和Oi公司在英国的投资为代表。

南美洲和中东及非洲地区正经历快速的都市化,但同时也面临基础设施短缺和亚洲进口产品的竞争。新的浮法玻璃计划仍然受到严格筛选,但区域製造商越来越倾向于使用本地生产的面板以避免高昂的运费,预计这将推动产量逐步成长。总体而言,区域格局的转变将使亚洲巩固其在平板玻璃生产中的份额,而其他地区则继续在平板玻璃市场追求更高价值的特殊产品。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 扩大对商业和住宅建筑领域的投资

- 由于电动车的安全性和轻量化要求,对汽车玻璃的需求增加。

- 光电模组用玻璃产能快速扩张

- 节能建筑规范推动了对低辐射和三层玻璃的需求。

- 抗菌玻璃在医疗和酒店业的应用

- 市场限制

- 聚合物、丙烯酸和聚碳酸酯替代品的供应情况

- 碱灰和天然气投入成本波动;

- 遵守欧盟碳边境调节机制的成本

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争程度

第五章 市场规模与成长预测

- 依产品类型

- 强化玻璃

- 透明玻璃

- 有色玻璃

- 镀膜玻璃

- 反射玻璃

- Low-E低辐射镀膜玻璃

- 加工玻璃

- 夹层玻璃

- 强化玻璃

- 镜面玻璃

- 花纹玻璃

- 强化玻璃

- 按最终用户行业划分

- 建筑/施工

- 车

- 太阳能玻璃

- 其他终端用户产业

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 西班牙

- 北欧国家

- 土耳其

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 卡达

- 阿拉伯聯合大公国

- 奈及利亚

- 埃及

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Adamant Holding Company

- AGC Inc.

- Cardinal Glass Industries Inc.

- Central Glass Co., Ltd.

- China Glass Holdings Limited

- Euroglas

- Fuyao Group

- Guardian Industries

- Nippon Sheet Glass Co. Ltd

- Phoenicia

- Saint-Gobain

- SCHOTT

- Sisecam

- Taiwan Glass Industry Corporation

- Vitro

- Xinyi Glass Holdings Limited

第七章 市场机会与未来展望

The Flat Glass market is expected to grow from 83.17 Million tons in 2025 to 86.48 Million tons in 2026 and is forecast to reach 105.14 Million tons by 2031 at 3.98% CAGR over 2026-2031.

Demand resilience stems from stricter construction energy codes, rapid photovoltaic build-outs, and automotive lightweighting that favors advanced glazing. Manufacturers are shifting toward low-carbon melting, green hydrogen trials, and oxy-electric hybrid furnaces to secure price premiums in sustainability-conscious tenders. Solar module glass, antimicrobial coatings for healthcare facilities, and ultra-thin triple units for high-rise retrofits are expanding the revenue mix. Asia-Pacific anchors both production and consumption, while North America and Europe invest in furnace electrification to counter energy-price swings and looming carbon tariffs.

Global Flat Glass Market Trends and Insights

Growing Investments in Commercial and Residential Construction

Global construction outlays are forecast to climb, aided by lower borrowing costs and an uptick in developer sentiment. Multifamily starts accelerate in response to single-family affordability gaps, channeling sustained demand for curtain wall and window systems that integrate Low-E and triple-glazed units. Developers specify higher-performance glass to secure LEED credits, driving volume growth for sputter-coated and argon-filled insulating products. The flat glass market, therefore, benefits directly from code-driven window-to-wall ratios that favor advanced glazing solutions.

Rising Automotive Glazing Requirements for EV Safety and Lightweighting

Electric vehicle platforms intensify structural glazing needs while mandating lighter glass to offset battery mass. Fuyao committed CNY 9.1 billion (USD 1.26 billion) in 2024 for two new plants aimed at new-energy vehicle demand. Thin laminated windshields, panoramic roofs, and heads-up display-ready windscreens expand processed glass penetration. Embedded sensor packages elevate value per car, creating a lucrative growth pocket inside the broader flat glass market. Aerodynamic gains from slimmer profiles further align with range optimization, cementing glass as a critical lightweight substrate over the forecast horizon.

Availability of Polymer, Acrylic and Polycarbonate Substitutes

Automakers trial polycarbonate side windows and panoramic roofs that weigh up to 50% less than comparable glass panels. Optical clarity and UV stability have improved, yet scratch resistance and thermal tolerance still lag glass. Stringent windshield regulations keep polycarbonate use niche, confining substitution risk mostly to non-load-bearing glazing. Glass recycling advantages and tighter end-of-life circularity goals further insulate flat glass market volumes.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Capacity Additions for Solar PV Module Glass

- Energy-Efficient Building Codes Boosting Low-E and Triple Glazing Demand

- Volatile Soda-Ash and Natural-Gas Input Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Processed glass generated the fastest 4.65% CAGR between 2026 and 2031, outpacing the broader flat glass market. Laminated and tempered variants supply automotive windscreens, curtain walls, and security facades where impact resistance is critical. Annealed output still dominated in 2025 with 79.62% of volume because it serves as the base substrate for downstream upgrades. The segment's cost edge keeps it central to commodity construction, yet its share is set to moderate as codes and safety norms elevate demand for value-added treatments.

Coated, reflective, and Low-E sheets advance in parallel due to mandatory thermal standards. AGC Glass Europe's 5.5 kg CO2 eq/m2 Low-Carbon Glass exemplifies product differentiation that commands premium bids. Tinted glass usage in EVs supports cabin cooling and battery efficiency. Mirror and patterned glass remain niche but attractive for interior and privacy applications. Altogether, specialization raises average selling prices, widening the processed share in the flat glass market size over the forecast horizon.

The Flat Glass Report is Segmented by Product Type (Annealed Glass, Coated Glass, Processed Glass, Mirror Glass, and Patterned Glass), End-User Industry (Building and Construction, Automotive, Solar Glass, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

The Asia-Pacific region secured 63.88% of 2025 shipments and is expanding at a 4.63% CAGR, the highest among regions. India is scaling new float lines while testing green hydrogen furnaces under a 20-year offtake pact between Asahi India Glass and INOX Air Products.

Europe focuses on decarbonization leadership. Saint-Gobain and AGC started trials of a hybrid furnace that cuts CO2 by 75% through 50% electrification and oxy-fuel combustion, supported by the EU Innovation Fund. Carbon Border Adjustment Mechanism fees, effective 2026 incentivize local sourcing, potentially boosting intra-regional sales. North American producers, led by Vitro's USD 180 million modernization and O-I's UK investment, upgrade lines to withstand gas-price volatility and ESG scrutiny.

South America, the Middle East, and Africa post rising urbanization but face infrastructure deficits and competition from Asian imports. Green-field float projects remain selective, though regional builders prefer local panes to avoid freight surcharges, supporting gradual volume growth. Altogether, geographic shifts keep Asia unchallenged in volume share while other regions chase value-added specialties within the flat glass market.

- Adamant Holding Company

- AGC Inc.

- Cardinal Glass Industries Inc.

- Central Glass Co., Ltd.

- China Glass Holdings Limited

- Euroglas

- Fuyao Group

- Guardian Industries

- Nippon Sheet Glass Co. Ltd

- Phoenicia

- Saint-Gobain

- SCHOTT

- Sisecam

- Taiwan Glass Industry Corporation

- Vitro

- Xinyi Glass Holdings Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Investments in Commercial and Residential Construction

- 4.2.2 Rising Automotive Glazing Requirements for EV Safety and Lightweighting

- 4.2.3 Rapid Capacity Additions for Solar PV Module Glass

- 4.2.4 Energy-Efficient Building Codes Boosting Low-E And Triple Glazing Demand

- 4.2.5 Uptake Of Antimicrobial Glass in Healthcare and Hospitality

- 4.3 Market Restraints

- 4.3.1 Availability of Polymer, Acrylic and Polycarbonate Substitutes

- 4.3.2 Volatile Soda-Ash and Natural-Gas Input Costs

- 4.3.3 EU Carbon Border Adjustment Mechanism Compliance Costs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Annealed Glass

- 5.1.1.1 Clear Glass

- 5.1.1.2 Tinted Glass

- 5.1.2 Coated Glass

- 5.1.2.1 Reflective Glass

- 5.1.2.2 Low-E Glass

- 5.1.3 Processed Glass

- 5.1.3.1 Laminated Glass

- 5.1.3.2 Tempered Glass

- 5.1.4 Mirror Glass

- 5.1.5 Patterned Glass

- 5.1.1 Annealed Glass

- 5.2 By End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Automotive

- 5.2.3 Solar Glass

- 5.2.4 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 Nordic Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Adamant Holding Company

- 6.4.2 AGC Inc.

- 6.4.3 Cardinal Glass Industries Inc.

- 6.4.4 Central Glass Co., Ltd.

- 6.4.5 China Glass Holdings Limited

- 6.4.6 Euroglas

- 6.4.7 Fuyao Group

- 6.4.8 Guardian Industries

- 6.4.9 Nippon Sheet Glass Co. Ltd

- 6.4.10 Phoenicia

- 6.4.11 Saint-Gobain

- 6.4.12 SCHOTT

- 6.4.13 Sisecam

- 6.4.14 Taiwan Glass Industry Corporation

- 6.4.15 Vitro

- 6.4.16 Xinyi Glass Holdings Limited

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

平板玻璃市场:按产品类型、镀膜类型、应用、最终用途和分销管道划分-全球市场预测(2026-2032 年)

平板玻璃市场:按产品类型、镀膜类型、应用、最终用途和分销管道划分-全球市场预测(2026-2032 年) 2026年全球平板玻璃市场报告平板玻璃製造机械市场:依产品类型、机器类型、技术、原料、产能和最终用途划分-全球预测,2026-2032年

2026年全球平板玻璃市场报告平板玻璃製造机械市场:依产品类型、机器类型、技术、原料、产能和最终用途划分-全球预测,2026-2032年 平板玻璃市场规模、份额、趋势和预测:按技术、产品类型、原材料、应用、类别、最终用途行业和地区划分,2026-2034年

平板玻璃市场规模、份额、趋势和预测:按技术、产品类型、原材料、应用、类别、最终用途行业和地区划分,2026-2034年 欧洲平板玻璃:市场占有率分析、产业趋势与统计、成长预测(2026-2031)日本平板玻璃市场报告(按技术、产品类型、最终用途行业和地区划分,2026-2034年)

欧洲平板玻璃:市场占有率分析、产业趋势与统计、成长预测(2026-2031)日本平板玻璃市场报告(按技术、产品类型、最终用途行业和地区划分,2026-2034年) 平板玻璃市场规模、份额和成长分析(按产品类型、技术、终端用户产业和地区划分)-2026-2033年产业预测

平板玻璃市场规模、份额和成长分析(按产品类型、技术、终端用户产业和地区划分)-2026-2033年产业预测 全球平板玻璃市场分析,市场规模(2025-2034 年)弯玻璃市场按产品类型、厚度、弯角、应用和分销管道划分-2025-2030 年全球预测

全球平板玻璃市场分析,市场规模(2025-2034 年)弯玻璃市场按产品类型、厚度、弯角、应用和分销管道划分-2025-2030 年全球预测 平板玻璃加工机械市场-全球产业规模、份额、趋势、机会及预测(按机械类型、最终用户产业、玻璃类型、自动化程度、地区及竞争情况划分,2020-2030 年预测)

平板玻璃加工机械市场-全球产业规模、份额、趋势、机会及预测(按机械类型、最终用户产业、玻璃类型、自动化程度、地区及竞争情况划分,2020-2030 年预测)