|

市场调查报告书

商品编码

1939670

半导体在医疗保健领域的应用:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)Semiconductor Applications In Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

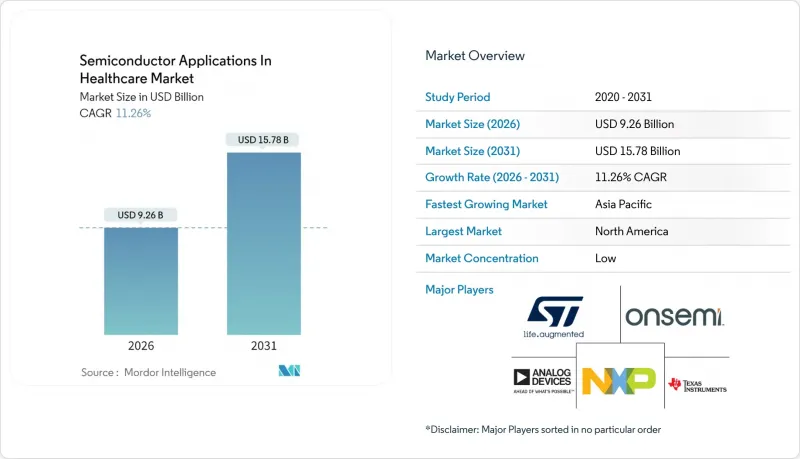

预计到 2026 年,医疗保健领域半导体应用的市场规模将达到 92.6 亿美元,高于 2025 年的 83.2 亿美元。

预计到 2031 年将达到 157.8 亿美元,2026 年至 2031 年的复合年增长率为 11.26%。

この急速な成长は、病院における人工知能(AI)画像诊断、埋め込み型バイオMEMS、集中检查室から検査を分散させる实验室晶片诊断技术への投资に起因します。また、超低消费电力の系统晶片(SoC)やセキュアエレメントデバイスがネットワークエッジで患者データを収集・处理・保护する「コネクテッドケア」への决定的な推进も成长要素です。高度なパッケージング技术、生体适合性材料、长期製品サポートを组み合わせられるチップメーカーは、临床医が长年安定运作する认证済みハードウェアを求める中、泛用ベンダーを上回る成长が见込まれます。最后に、各国の半导体奨励プログラムが供给基盘を再构筑し、医疗认证済みシリコンの前置作业时间短缩と単一地域生产拠点への依存低减を促进しています。

全球医疗保健领域半导体应用市场趋势与洞察

接続型医疗设备とIoTの普及

智能监护仪、输液泵和辅助生活设备正被部署到全球医院和居家医疗生态系统中,用于持续记录生命体征。这些系统依赖整合了蓝牙低功耗 (Bluetooth LE)、Wi-Fi 6 或 5G 无线电模组、感测器介面和加密储存的无线系统单晶片 (SoC),并在睡眠週期内以微瓦级功耗运作。长寿命纽扣电池的出现推动了对支持能源采集功能的电源管理集成电路 (PMIC) 的需求,促使供应商对无线电协议栈和电源域进行协同优化。这些设备还集成了硬件信任根模块,使临床医生能够验证韧体更新。随着报销机制向基于结果的模式转变,医疗服务提供者越来越多地采用边缘处理资料来降低延迟和网路拥塞,从而增加了每个设备的目标晶片容量。

人工智慧成像系统的应用日益普及

放射线科では、事后的な画像読影から、主机上で提供されるリアルタイムの意思决定支援へと移行しています。光子计数型CTスキャナーはより高い频谱分解能を提供するため、生データの量が増加し、画像再构成や深层学习アルゴリズムを数ミリ秒で実行可能なオンボードアクセラレータアレイが必要となります。半导体设计者は、2.5Dインターポーザー内で高频宽HBMスタックと低ジオメトリロジック晶粒を组み合わせることで、コンパクトなフットプリントを维持しながらスループットを向上させています。并行して、ガリウムヒ素やペロブスカイト材料を用いた化合物半导体检测器は、より低い放射线量でより鲜明なコントラストを実现し、専用のアナログフロントエンドや高电圧ドライバに対するバックエンド需要を生み出しています。

レガシー医疗设备の高额なアップグレード费用

许多医院仍在运作十年前购置的核磁共振扫描仪、床旁监护仪和输液泵,这限制了用于半导体密集型升级的资金。这迫使原始设备製造商 (OEM) 推出适用于现有设备的即插即用型电路板,而不是全新的系统,减缓了下一代人工智慧处理器的普及。资金缺口在小规模的私立诊所和新兴经济体中尤为突出,这些地区的报销延迟,采购周期也远超西方平均水平。为了解决这一障碍,供应商提供了一系列融资方案,将晶片成本分摊到多年维护合约和基于使用量的服务模式中。

细分市场分析

至2025年,医疗影像将占半导体应用市场总收入的35.22%,凸显其作为医疗保健领域半导体应用市场核心价值创造者的地位。该领域采用超音波模块,集成高分辨率数字化仪、现场可编程闸阵列(FPGA)和人工智能晶粒,用于计算机断层扫描(CT)、磁振造影(MRI)和超声主机。频谱CT和光子计数CT的普及推动了处理能力的提升,促使原始设备制造商(OEM)采用支持HBM的SoC,以处理超过4GB/s的数据速率。同时,携带式超音波系统利用单芯片集成技术,在紧急情况下实现照护现场诊断。根据预测模型,到2031年,医疗影像领域在医疗保健领域半导体应用市场的复合年增长率(CAGR)预计将维持在12.06%。

消费医疗电子领域也带来了互补性成长,例如,连网血压计、血糖仪和心电图贴片等产品正在整合安全的无线功能和低功耗微控制器。诊断性病患监测和治疗设备也在稳步扩张,医院正在逐步采用联网的生命体征中心,并将数据传输到电子健康记录系统。医疗设备领域虽然较为稳定,但增长速度相对较慢,其重点在于采用成熟的65纳米及以上模拟工艺节点实现实验室自动化,并优先考虑精度和使用寿命。

区域分析

北米は2025年に32.74%の収益シェアを维持し、高精度诊断机器の偿还が可能な成熟した医疗保険者エコシステムに牵引され、主导的地位を保っています。连邦政府の奖励により国内のアナログ・ミックスドシグナルウエハー生产が加速し、FDA认可部品の前置作业时间短缩が図られています。カリフォルニア州、マサチューセッツ州、德克萨斯州を中心とした学术机関と医疗机関の连携により、神経调节や埋め込み型センサーのプロトタイプが継続的に供给され、迅速に临床试験へ移行しています。ただし、特定の高频宽AIアクセラレータに対する输出规制の考虑事项は、世界中にイメージング主机を出荷する多国籍OEMメーカーの计画に复雑さを生じています。

亚太地区以13.08%的复合年增长率呈现最快增长态势,这主要得益于中国、印度和东南亚地区对医院基础设施的大规模公共投资。深圳一家晶圆厂专注于医疗级ASIC芯片的生产,并提供符合ISO 13485标准的承包组装服务,帮助区域内医疗设备Start-Ups缩短设计周期。在印度,政府主导的数字健康宣传活动正在推动对集成低功耗蓝牙和低功耗RISC-V内核的成本优化型SoC的需求,从而实现农村诊所的生命体征采集。日本製造商则专注于精度和材料创新,近期已成功过渡到8吋碳化硅晶圆,用于支援MRI梯度放大器中的高压电源。

欧州では医疗设备规则(MDR)を通じ、部品のトレーサビリティや市贩后调査の要件を规定するなど、强力な规制発信力を维持しています。EUチップ法では、差し迫ったPFAS规制に対応するため、无溶剤ダイアタッチ化学薬品を采用するパッケージング工场への津贴が指定されています。泛欧州购买コンソーシアムは、サプライヤーの可再生エネルギー利用実绩を重视する倾向が强まっており、チップメーカーに対し、カーボン削减蓝图の文书化を促しています。全体的な成长率はアジア太平洋地域に后れを取っていますが、欧州が永续性とデータ保护コンプライアンスを重视しているため、セキュアな处理と暗号化シリコンに対する高付加価値の注文が安定して発生しています。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第2章调查方法

第3章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 接続型医疗设备およびIoTの普及

- 人工智慧成像系统的应用日益普及

- 慢性病负担加重推动远距监测

- 政府对医疗专用晶圆厂的奖励措施

- Power-Supply-on-Chipを备えた埋め込み型バイオMEMS

- 实验室晶片诊断技术による中央检查室依存度の低减

- 市场限制

- レガシー医疗设备の高额なアップグレード费用

- チップ変更に対する厳格な规制核准サイクル

- 小型化されたウェアラブル/植入机器における热问题

- 特殊基板におけるサプライチェーンの集中化

- 产业价值链分析

- 监管环境

- 技术展望

- ポーターの五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 评估主要宏观趋势的影响

第五章 市场规模与成长预测

- 透过申请

- 医学影像

- 民生用医疗电子机器

- 诊断・病患监测および治疗

- 医疗设备

- 按组件

- 积体电路

- 模拟

- 逻辑

- 记忆

- 微型组件

- 光电子学

- 感应器

- 离散组件

- 研究所

- 积体电路

- 技术ノード别

- 28nm未満

- 28-65nm

- 65nm以上

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 东南亚

- 亚太其他地区

- 中东

- 非洲

- 北美洲

第6章 竞合情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Analog Devices Inc.

- ams Osram AG

- Broadcom Inc.

- Dialog Semiconductor Ltd.

- Infineon Technologies AG

- Mediatek Inc.

- Microchip Technology Inc.

- Micron Technology Inc.

- Nordic Semiconductor ASA

- NXP Semiconductors NV

- ON Semiconductor Corp.

- Qualcomm Inc.

- Renesas Electronics Corp.

- Rohm Semiconductor

- Samsung Electronics Co. Ltd.

- Sensirion AG

- Skyworks Solutions Inc.

- STMicroelectronics NV

- Taiwan Semiconductor Manufacturing Co. Ltd.

- Texas Instruments Inc.

- Toshiba Electronic Devices & Storage Corp.

- Vishay Intertechnology Inc.

- Zilog Inc.

第七章 市场机会与未来展望

The semiconductor applications in the healthcare market size in 2026 is estimated at USD 9.26 billion, growing from 2025 value of USD 8.32 billion with 2031 projections showing USD 15.78 billion, growing at 11.26% CAGR over 2026-2031.

Rapid gains stem from hospital investments in artificial-intelligence imaging, implantable bio-MEMS, and lab-on-chip diagnostics that shift testing away from centralized laboratories. Growth also reflects a decisive push toward connected care, where ultra-low-power system-on-chips (SoCs) and secure element devices capture, process, and protect patient data at the network edge. Chipmakers able to combine advanced packaging, biocompatible materials, and long-lifecycle product support are positioned to outpace general-purpose vendors as clinicians demand certified hardware that runs reliably for years. Finally, national semiconductor incentive programs are reshaping the supply base, shortening lead times for medically validated silicon and reducing dependence on single-region production hubs.

Global Semiconductor Applications In Healthcare Market Trends and Insights

Proliferation of Connected Medical Devices and IoT

Global hospital and home-care ecosystems now deploy smart monitors, infusion pumps, and ambient-assisted living tools that continuously log vital signs. These systems rely on wireless SoCs that merge Bluetooth LE, Wi-Fi 6, or 5G radios with sensor interfaces and encrypted storage while consuming microwatts during sleep cycles. Long-life coin-cell operation reinforces demand for energy-harvesting PMICs, prompting suppliers to co-optimize radio stacks and power domains. Device fleets also incorporate hardware root-of-trust modules, allowing clinicians to authenticate firmware updates. As reimbursement frameworks shift toward outcome-based models, providers are increasingly favoring edge-processed data that reduces latency and network congestion, thereby expanding the addressable silicon content per device.

Growing Adoption of AI-Enabled Imaging Systems

Radiology suites are transitioning from retrospective image reads to real-time decision support delivered on-console. Photon-counting CT scanners offer higher spectral resolution, thereby increasing the raw data volume and necessitating on-board accelerator arrays capable of executing image reconstruction and deep-learning algorithms in milliseconds. Semiconductor designers address this by pairing high-bandwidth HBM stacks with low-geometry logic dies within 2.5-D interposers, thereby boosting throughput while maintaining compact footprints. In parallel, compound-semiconductor detectors using gallium arsenide or perovskite materials deliver sharper contrast at lower radiation doses, creating back-end demand for specialized analog front-ends and high-voltage drivers.

High Upgrade Costs for Legacy Medical Equipment

Many hospitals continue operating MRI scanners, bedside monitors, and infusion pumps purchased a decade ago, leaving limited capital for semiconductor-intensive upgrades. Original equipment manufacturers (OEMs), therefore, face pressure to release drop-in boards rather than entirely new systems, which slows the penetration of next-generation AI processors. Funding gaps are most acute in small private clinics and emerging economies, where reimbursements lag and procurement cycles extend well beyond Western averages. To counter the barrier, suppliers bundle financing packages and usage-based service models that amortize silicon costs over multi-year maintenance contracts.

Other drivers and restraints analyzed in the detailed report include:

- Rising Chronic-Disease Burden Driving Remote Monitoring

- Government Incentives for Healthcare-Specific Fabs

- Stringent Regulatory Approval Cycles for Chip Changes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Medical imaging contributed 35.22% of 2025 revenue, underscoring its role as the core value generator for the semiconductor applications in the healthcare market. Within this arena, computed tomography, magnetic resonance imaging, and ultrasound consoles incorporate multi-die modules that combine high-resolution digitizers, field-programmable gate arrays, and AI accelerators. The migration toward spectral and photon-counting CT elevates processing demand, prompting OEMs to specify HBM-enabled SoCs that manage data rates exceeding 4 GB/s. Meanwhile, handheld ultrasound systems leverage single-chip integration to deliver point-of-care diagnostics in emergency settings. Forecast models indicate medical imaging will sustain a 12.06% CAGR in the semiconductor applications in the healthcare market by 2031.

Complementary growth stems from consumer medical electronics, where connected blood-pressure cuffs, glucose monitors, and ECG patches integrate secure radios and power-efficient microcontrollers. Diagnostic patient monitoring and therapy equipment also expand steadily as hospitals standardize on networked vital-sign hubs that stream data into electronic health records. Medical instruments remain a stable but less dynamic category, concentrating on laboratory automation that favors tried-and-tested 65 nm and above analog nodes for precision and longevity.

The Semiconductor Applications in Healthcare Market Report is Segmented by Application (Medical Imaging, Consumer Medical Electronics, Medical Instruments, and More), Component (Integrated Circuits, Optoelectronics, Sensors, and More), Technology Node (Less Than 28 Nm, 28-65 Nm, Above 65 Nm), and Geography (North America, South America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retains its leadership position, with 32.74% revenue in 2025, driven by a mature healthcare payer ecosystem that can reimburse premium diagnostics. Federal incentives have accelerated domestic analog and mixed-signal wafer starts, reducing lead times for FDA-cleared components. Academic-medical partnerships centered in California, Massachusetts, and Texas sustain a continuous pipeline of neuromodulation and implantable sensor prototypes that transition swiftly into clinical trials. However, export-control considerations on certain high-bandwidth AI accelerators introduce planning complexity for multinational OEMs shipping imaging consoles worldwide.

The Asia-Pacific region posts the fastest trajectory at a 13.08% CAGR, fueled by large-scale public investments in hospital infrastructure across China, India, and Southeast Asia. Shenzhen-based fabs specializing in medical-grade ASIC production now offer turnkey ISO 13485 assembly services, shortening design cycles for regional device startups. In India, government digital-health campaigns are spurring demand for cost-optimized SoCs that integrate Bluetooth LE and power-efficient RISC-V cores, enabling vital-sign collection in rural clinics. Japanese manufacturers emphasize precision and materials innovation; recent transitions to 8-inch SiC wafers support high-voltage supplies inside MRI gradient amplifiers.

Europe maintains a strong regulatory voice through its Medical Device Regulation, which shapes the requirements for component traceability and post-market surveillance. The EU Chips Act earmarks grants for packaging plants that adopt solvent-free die-attach chemistries to comply with impending PFAS restrictions. Pan-European purchasing consortiums increasingly weigh suppliers' renewable-energy footprints, encouraging chipmakers to document carbon-reduction roadmaps. While overall growth trails that of the Asia-Pacific region, Europe's emphasis on sustainability and data-protection compliance ensures consistent high-value orders for secure processing and encryption silicon.

- Analog Devices Inc.

- ams Osram AG

- Broadcom Inc.

- Dialog Semiconductor Ltd.

- Infineon Technologies AG

- Mediatek Inc.

- Microchip Technology Inc.

- Micron Technology Inc.

- Nordic Semiconductor ASA

- NXP Semiconductors N.V.

- ON Semiconductor Corp.

- Qualcomm Inc.

- Renesas Electronics Corp.

- Rohm Semiconductor

- Samsung Electronics Co. Ltd.

- Sensirion AG

- Skyworks Solutions Inc.

- STMicroelectronics N.V.

- Taiwan Semiconductor Manufacturing Co. Ltd.

- Texas Instruments Inc.

- Toshiba Electronic Devices & Storage Corp.

- Vishay Intertechnology Inc.

- Zilog Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of connected medical devices and IoT

- 4.2.2 Growing adoption of AI-enabled imaging systems

- 4.2.3 Rising chronic-disease burden driving remote monitoring

- 4.2.4 Government incentives for healthcare-specific fabs

- 4.2.5 Implantable bio-MEMS with on-chip power

- 4.2.6 Lab-on-chip diagnostics reducing central-lab dependence

- 4.3 Market Restraints

- 4.3.1 High upgrade costs for legacy medical equipment

- 4.3.2 Stringent regulatory approval cycles for chip changes

- 4.3.3 Thermal issues in miniaturised wearable/implantables

- 4.3.4 Supply-chain concentration in specialist substrates

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Impact of Key Macro Trends

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Medical Imaging

- 5.1.2 Consumer Medical Electronics

- 5.1.3 Diagnostic Patient Monitoring and Therapy

- 5.1.4 Medical Instruments

- 5.2 By Component

- 5.2.1 Integrated Circuits

- 5.2.1.1 Analog

- 5.2.1.2 Logic

- 5.2.1.3 Memory

- 5.2.1.4 Micro-components

- 5.2.2 Optoelectronics

- 5.2.3 Sensors

- 5.2.4 Discrete Components

- 5.2.5 Research Institutes

- 5.2.1 Integrated Circuits

- 5.3 By Technology Node

- 5.3.1 Less than 28 nm

- 5.3.2 28-65 nm

- 5.3.3 Above 65 nm

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 South-East Asia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.6 Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Analog Devices Inc.

- 6.4.2 ams Osram AG

- 6.4.3 Broadcom Inc.

- 6.4.4 Dialog Semiconductor Ltd.

- 6.4.5 Infineon Technologies AG

- 6.4.6 Mediatek Inc.

- 6.4.7 Microchip Technology Inc.

- 6.4.8 Micron Technology Inc.

- 6.4.9 Nordic Semiconductor ASA

- 6.4.10 NXP Semiconductors N.V.

- 6.4.11 ON Semiconductor Corp.

- 6.4.12 Qualcomm Inc.

- 6.4.13 Renesas Electronics Corp.

- 6.4.14 Rohm Semiconductor

- 6.4.15 Samsung Electronics Co. Ltd.

- 6.4.16 Sensirion AG

- 6.4.17 Skyworks Solutions Inc.

- 6.4.18 STMicroelectronics N.V.

- 6.4.19 Taiwan Semiconductor Manufacturing Co. Ltd.

- 6.4.20 Texas Instruments Inc.

- 6.4.21 Toshiba Electronic Devices & Storage Corp.

- 6.4.22 Vishay Intertechnology Inc.

- 6.4.23 Zilog Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment