|

市场调查报告书

商品编码

1939745

亚太地区合约物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Asia-Pacific Contract Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

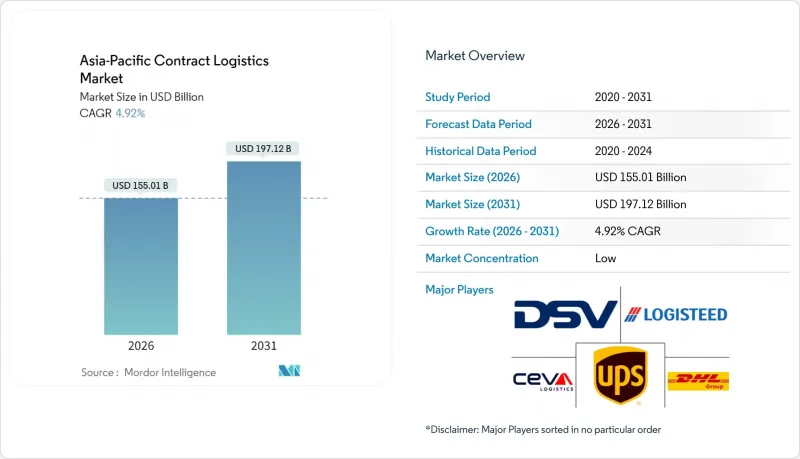

预计到 2026 年,亚太地区的合约物流市场规模将达到 1,550.1 亿美元。

这意味着从 2025 年的 1,477.4 亿美元成长到 2031 年的 1,971.2 亿美元,2026 年至 2031 年的年复合成长率(CAGR)为 4.92%。

亚太地区合约物流市场的当前规模反映了该地区作为全球外包价值链管理中心的地位,预计复合年增长率表明,随着托运人履约网络进行现代化改造并拓展附加价值服务,市场将持续增长。电子商务的快速发展、大规模的近岸外包和回岸外包,以及政府对公路、铁路、港口和数位基础设施的大量投资,正在加速製造业、零售业和医疗保健行业对合约物流的采用。整合网路设计、自动化和数据平台的长期伙伴关係正在取代短期交易协议,使供应商即使在劳动力和房地产资源受限的环境下也能提供稳定的供给能力。南海航道拥挤导致海上保险费上涨,以及对温度敏感的航线上持续存在的低温运输瓶颈,虽然增加了市场的复杂性,但也为能够提供严格品管和跨境规服务的供应商创造了利润丰厚的市场机会。

亚太地区合约物流市场趋势与洞察

亚太地区电子商务爆炸性成长

数位商务的蓬勃发展正在重塑亚太地区合约物流市场的履约经济格局。线上销售的快速成长迫使品牌商采用全通路库存分配、微型仓配点和专用逆向物流迴路,而这些是大多数企业内部物流网路无法实现的。印尼和越南的线上销售额年增率远超过实体店,迫使仓库开发商增建夹层以实现自动化拣货和包装,并增设温控单元用于存放高端食品杂货。由于区域退货率通常高达15%至30%,合约物流供应商现在正将再製造生产线、重新包装站和即时视觉化仪錶板整合到其整合提案中。

供应链近岸外包/回流(中国+1策略)

跨国公司正将零件采购和最终组装转移到东南亚和印度,以分散地缘政治风险并降低总到岸成本。越南北部经济区和印尼巴塘工业园区等新兴生产中心需要原材料预处理、为准时制生产线供料以及整合出口货物——所有这些现有供应商都可以透过跨国控制中心提供。双重采购策略要求对中国和海外工厂的营运进行跨工厂视觉化管理,因此,托运人越来越多地将运输规划、里程碑管理和供应商管理库存外包给物流专家。印度的生产连结奖励计画计划和印尼的综合法案等政府倡议正在加速工厂搬迁,随着新的物流走廊日趋成熟,亚太地区的合约物流市场预计将在中期内实现成长。

主要基地房地产和人事费用上涨

2024年,由于土地供应紧张以及资料中心营运商的竞争需求,新加坡、香港和东京的优质仓库租金飙升。同时,澳洲和韩国的堆高机驾驶人和拣货员的基本工资正以两位数的速度成长,挤压着大量营运的利润空间。合约物流业者正透过机器人货物搬运、自动堆垛机和节能空调系统来缓解这些压力,但这些升级需要大量的资本支出和较长的投资回收期。这些经济状况促使以柔佛新山和千叶等低成本卫星城市为基地的枢纽辐射式网路兴起,但大都会圈的「最后一公里」配送时效性仍然是一个挑战,导致服务水准协议更加严格,短期价格上涨空间有限。

细分市场分析

到2025年,运输环节将占亚太地区合约物流市场收入的62.55%,这主要得益于中国密集的道路运输网络和印尼发达的国内海运网络。在地域分散的情况下,物流供应商正在协调长途公路运输、铁路联运和短途海运支线,以平衡成本和速度。同时,受製造商对延迟出货、套件组装以及在区域配销中心内简化组装能力的需求推动,附加价值服务预计将在2031年之前实现最高的复合年增长率(CAGR),达到4.03%。日益复杂的家电标籤法规促使合约物流供应商安装本地印刷和贴标生产线。同时,时尚品牌正在利用仓库内的缝纫单元来加快尺寸调整速度并提高销售转换率。这种转变正在扩大利润率并降低对波动较大的公路货运价格的依赖。亚太地区合约物流市场规模在高附加价值领域正经历结构性扩张。

仓储和配送业务依然是核心业务,并随着电子商务小包裹量和全通路库存策略的推进而同步扩张。高密度穿梭运输系统减少了城市中心偏远地区的面积,而靠近海港的越库作业布局则缩短了对温度敏感的农产品的停留时间。具有前瞻性的营运商正在将仓库管理系统与即时运输视觉化平台集成,以识别预计到达时间并提供异常警报,从而改善客户体验。空运货量同样在成长,而高价值小包裹和生技药品的直接投递模式需要从始发地到最终目的地的多模态管理,这支撑了亚太地区合约物流市场的整体成长。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 亚太地区电子商务渗透率爆炸性成长

- 供应链近岸外包/回流(中国+1策略)

- 政府对物流基础建设进行大规模投资

- 製造业和零售业的外包重点

- 电动车电池超级工厂对厂内物流的需求

- 数位化海关平台加速跨境物流

- 市场限制

- 主要城市的房地产和人事费用不断上涨

- 亚太地区国家标准和许可製度的碎片化

- 生物製药低温运输能力瓶颈

- 南海航线海上保险费正在上涨

- 价值/供应链分析

- 监管环境

- 技术展望(自动化、人工智慧、物联网、仓库管理系统)

- 波特五力模型

- 新进入者的威胁

- 替代品的威胁

- 买方的议价能力

- 供应商的议价能力

- 竞争对手之间的竞争

- 政府措施和经济特区现状

- 交通走廊(海运、铁路、公路)

- 电子商务洞察(国内和跨境)

- 逆向物流的考量

- 回顾新冠疫情和地缘政治事件的影响

第五章 市场规模与成长预测

- 按服务类型

- 运输

- 路

- 铁路

- 空运

- 海上运输

- 仓储/配送

- 附加价值服务(组装、贴标、套件包装)

- 运输

- 按合约期限

- 1-3年

- 3年或以上

- 按最终用户行业划分

- 製造业和汽车业

- 食品/饮料

- 零售与电子商务

- 医疗/製药

- 化学品

- 其他行业

- 按国家/地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 新加坡

- 马来西亚

- 印尼

- 泰国

- 亚太其他地区

第六章 竞争情势

- 市场集中度分析

- 策略趋势(併购、合资、自动化资本投资)

- 市占率分析

- 公司简介

- Deutsche Post DHL Group

- DSV

- CEVA Logistics

- UPS Supply Chain Solutions

- Logisteed Ltd

- CJ Logistics

- Nippon Express Co. Ltd

- Toll Group

- Yusen Logistics Co. Ltd

- Kuehne+Nagel

- Kerry Logistics Network Ltd

- Hellmann Worldwide Logistics

- Rhenus Logistics

- Geodis

- GAC

- Silk Contract Logistics

- Linc Group

- Rohlig Logistics

- Allcargo Logistics Ltd

- Broekman Logistics

第七章 市场机会与未来展望

第八章附录

- 按行业和地区分類的GDP分布

- 资金流分析

- 外贸统计

Asia-Pacific Contract Logistics Market size in 2026 is estimated at USD 155.01 billion, growing from 2025 value of USD 147.74 billion with 2031 projections showing USD 197.12 billion, growing at 4.92% CAGR over 2026-2031.

The current Asia-Pacific Contract Logistics market size reflects the region's role as the global center for outsourced supply-chain management, and the forecast CAGR points to sustained momentum as shippers modernize fulfillment networks and extend value-added services. Rapid e-commerce expansion, large-scale near- and re-shoring, and government mega-investments in road, rail, port, and digital infrastructure are accelerating contract-logistics adoption across manufacturing, retail, and healthcare sectors. Long-term partnerships that align network design, automation, and data platforms continue to replace short-term, transactional arrangements, allowing providers to deliver resilient capacity in tight labor and real-estate environments. Rising marine-insurance premiums on congested South-China-Sea routes and persistent cold-chain bottlenecks in temperature-sensitive corridors add complexity, but they also create high-margin niches that reward providers capable of rigorous quality control and cross-border compliance.

Asia-Pacific Contract Logistics Market Trends and Insights

Explosive E-commerce Penetration Across Asia-Pacific

Digital commerce growth is redefining fulfillment economics across the Asia-Pacific Contract Logistics market. Online sales velocity is forcing brands to adopt omnichannel inventory allocation, micro-fulfillment nodes, and dedicated reverse-logistics loops that most in-house networks cannot match. Indonesia and Vietnam record annual online-sales expansion far above brick-and-mortar growth, pushing warehouse developers to add mezzanine floors for pick-and-pack automation and temperature-controlled cells for premium groceries. Regional return rates often reach 15-30%, demanding refurbishment lines, re-boxing stations, and real-time visibility dashboards that contract-logistics providers now bundle into integrated propositions.

Near-/Re-shoring of Supply Chains ("China+1")

Multinational corporations are reallocating component sourcing and final assembly to Southeast Asia and India to diversify geopolitical risk and lower total landed cost. New production clusters in Vietnam's Northern Economic Zone and Indonesia's Batang Industrial Park demand inbound raw-material staging, just-in-sequence line feeding, and export consolidation that established providers can deliver from multi-country control towers. Dual-sourcing strategies require visibility across Chinese and non-Chinese plants, prompting shippers to hand over transport planning, milestone monitoring, and supplier-managed inventory to logistics specialists. Government programs such as India's Production-Linked Incentive scheme and Indonesia's Omnibus Law further accelerate factory relocations, locking in mid-term growth for the Asia-Pacific Contract Logistics market as new corridors mature.

Soaring Real-estate & Labor Costs in Tier-1 Hubs

Prime-grade warehouse rents rose sharply across Singapore, Hong Kong, and Tokyo in 2024, driven by constrained land supply and competing demand from data-center operators. Simultaneously, base wages for forklift drivers and order-pickers climbed in double digits in Australia and South Korea, eroding profit margins for high-volume operations. Contract-logistics providers mitigate these pressures through goods-to-person robotics, automated palletizers, and energy-efficient HVAC systems, but such upgrades require heavy capital outlays and lengthier payback periods. The economics encourage hub-and-spoke networks anchored in lower-cost satellite cities such as Johor Bahru and Chiba, yet last-mile cut-off times in megacities remain challenging, tightening service-level agreements and limiting rate increases in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Government Mega-spend on Logistics Infrastructure

- Outsourcing Focus of Manufacturers & Retailers

- Fragmented Standards & Permits Across Asia-Pacific Nations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The transportation slice of the Asia-Pacific Contract Logistics market generated 62.55% of revenue in 2025, anchored by dense road fleets in China and sprawling domestic maritime lanes in Indonesia. Providers orchestrate synchronized long-haul trucking, rail shuttles, and short-sea feeder loops to balance cost and speed across fragmented geography. Meanwhile, value-added services are expected to post the strongest 4.03% CAGR to 2031 as manufacturers seek postponement, kitting, and light-assembly capabilities inside regional distribution centers. Growing label-compliance complexity in consumer electronics pushes contract operators to install on-site print-and-apply lines, while fashion brands use in-warehouse sewing cells for rapid size adjustments that elevate sell-through rates. The shift broadens margins and reduces reliance on volatile linehaul rates, reinforcing the structural expansion of the Asia-Pacific Contract Logistics market size within higher-value niches.

Warehouse-and-distribution operations remain central, scaling with e-commerce parcel volumes and omni-inventory strategies. High-density shuttle systems reduce footprint in urban infill sites, whereas cross-docking layouts near seaports cut dwell time for temperature-sensitive produce. Progressive operators couple warehouse-management systems with real-time transport-visibility platforms, unlocking predictive arrival windows and exception alerts that sharpen customer experience. Airfreight forwarding volumes climb in parallel as direct-injection models for high-value parcels and biologics require multi-modal control from origin to doorstep, buttressing growth across the Asia-Pacific Contract Logistics market.

The Asia-Pacific Contract Logistics Market Report is Segmented by Service Type (Transportation, Warehousing & Distribution, and Value-Added Services), Contract Duration (1-3 Years and Above 3 Years), End-User Industry (Manufacturing & Automotive, , Retail & E-Commerce, Healthcare & Pharmaceuticals, Chemicals, and More), Country (China, India, Japan, Australia, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Deutsche Post DHL Group

- DSV

- CEVA Logistics

- UPS Supply Chain Solutions

- Logisteed Ltd

- CJ Logistics

- Nippon Express Co. Ltd

- Toll Group

- Yusen Logistics Co. Ltd

- Kuehne + Nagel

- Kerry Logistics Network Ltd

- Hellmann Worldwide Logistics

- Rhenus Logistics

- Geodis

- GAC

- Silk Contract Logistics

- Linc Group

- Rohlig Logistics

- Allcargo Logistics Ltd

- Broekman Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive e-commerce penetration across Asia-Pacific

- 4.2.2 Near-/re-shoring of supply chains ("China+1")

- 4.2.3 Government mega-spend on logistics infrastructure

- 4.2.4 Outsourcing focus of manufacturers & retailers

- 4.2.5 EV battery gigafactories' in-plant logistics demand

- 4.2.6 Digital customs platforms speeding cross-border flows

- 4.3 Market Restraints

- 4.3.1 Soaring real-estate & labour costs in tier-1 hubs

- 4.3.2 Fragmented standards & permits across Asia-Pacific nations

- 4.3.3 Cold-chain capacity bottlenecks for biologics

- 4.3.4 Rising marine-insurance premiums in South-China-Sea lanes

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook (Automation, AI, IoT, WMS)

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Threat of Substitutes

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Bargaining Power of Suppliers

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Government Initiatives & SEZ Landscape

- 4.9 Transport Corridors (Maritime, Rail, Road)

- 4.10 Insights on E-commerce (Domestic & Cross-Border)

- 4.11 Insights on Reverse Logistics

- 4.12 COVID-19 & Geo-Political Events Impact Review

5 Market Size & Growth Forecasts

- 5.1 By Service Type

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Air

- 5.1.1.4 Sea

- 5.1.2 Warehousing & Distribution

- 5.1.3 Value-added Services (Assembly, Labelling, Kitting)

- 5.1.1 Transportation

- 5.2 By Contract Duration

- 5.2.1 1 - 3 Years

- 5.2.2 Above 3 years

- 5.3 By End-user Industry

- 5.3.1 Manufacturing & Automotive

- 5.3.2 Food & Beverage

- 5.3.3 Retail & E-commerce

- 5.3.4 Healthcare & Pharmaceuticals

- 5.3.5 Chemicals

- 5.3.6 Other Industries

- 5.4 By Country

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 South Korea

- 5.4.5 Australia

- 5.4.6 Singapore

- 5.4.7 Malaysia

- 5.4.8 Indonesia

- 5.4.9 Thailand

- 5.4.10 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration Analysis

- 6.2 Strategic Moves (M&A, JVs, Automation Cap-ex)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Deutsche Post DHL Group

- 6.4.2 DSV

- 6.4.3 CEVA Logistics

- 6.4.4 UPS Supply Chain Solutions

- 6.4.5 Logisteed Ltd

- 6.4.6 CJ Logistics

- 6.4.7 Nippon Express Co. Ltd

- 6.4.8 Toll Group

- 6.4.9 Yusen Logistics Co. Ltd

- 6.4.10 Kuehne + Nagel

- 6.4.11 Kerry Logistics Network Ltd

- 6.4.12 Hellmann Worldwide Logistics

- 6.4.13 Rhenus Logistics

- 6.4.14 Geodis

- 6.4.15 GAC

- 6.4.16 Silk Contract Logistics

- 6.4.17 Linc Group

- 6.4.18 Rohlig Logistics

- 6.4.19 Allcargo Logistics Ltd

- 6.4.20 Broekman Logistics

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

8 Appendix

- 8.1 GDP Distribution by Activity & Region

- 8.2 Capital-Flow Insights

- 8.3 External Trade Statistics

2026年全球合约物流市场报告

2026年全球合约物流市场报告 合约物流市场:2026-2032年全球市场预测(依服务类型、货物类型、运输方式、客户规模及最终用途划分)

合约物流市场:2026-2032年全球市场预测(依服务类型、货物类型、运输方式、客户规模及最终用途划分) 欧洲合约物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)北美合约物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

欧洲合约物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031)北美合约物流:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 日本合约物流市场报告(按类型(内部物流、外部物流)、最终用户(汽车、消费品和零售、能源、高科技和医疗保健、工业和航太、技术及其他)和地区划分,2026-2034 年)

日本合约物流市场报告(按类型(内部物流、外部物流)、最终用户(汽车、消费品和零售、能源、高科技和医疗保健、工业和航太、技术及其他)和地区划分,2026-2034 年) 合约物流市场规模及预测 2021 - 2031、全球及地区份额、趋势及成长机会分析报告涵盖范围:按类型、服务类型、最终用户及地理划分

合约物流市场规模及预测 2021 - 2031、全球及地区份额、趋势及成长机会分析报告涵盖范围:按类型、服务类型、最终用户及地理划分 美国合约物流市场:依服务、类型、产业、运输方式、地区、机会及预测,2018-2032

美国合约物流市场:依服务、类型、产业、运输方式、地区、机会及预测,2018-2032 合约物流的全球市场(2025年)

合约物流的全球市场(2025年) 合约物流市场-全球产业规模、份额、趋势、机会和预测(按类型、按服务、按应用、按地区、按竞争划分,2020-2030 年预测)

合约物流市场-全球产业规模、份额、趋势、机会和预测(按类型、按服务、按应用、按地区、按竞争划分,2020-2030 年预测) 合约物流市场规模、份额、趋势分析报告:按服务、类型、运输方式、产业、地区和细分市场预测,2025 年至 2030 年

合约物流市场规模、份额、趋势分析报告:按服务、类型、运输方式、产业、地区和细分市场预测,2025 年至 2030 年