|

市场调查报告书

商品编码

1940586

永续包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Sustainable Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

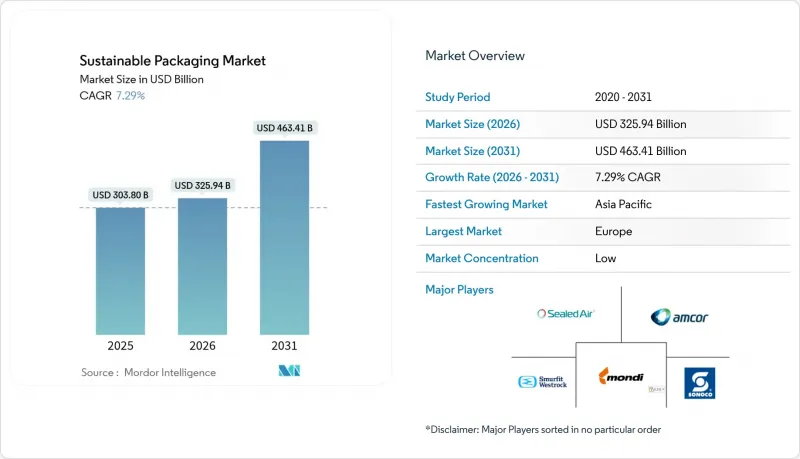

2025年永续包装市场价值为3,038亿美元,预计到2031年将达到4,634.1亿美元,高于2026年的3,259.4亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 7.29%。

这项发展势头得益于生产者延伸责任制(EPR)法规的整合,目前已涵盖63个国家,消除了监管套利,并实现了跨境规模化的效率提升。品牌对最低再生材料含量的承诺、化学回收技术的快速发展以及不断增长的电子商务规模对合适包装的需求,都在加速向循环解决方案注入资金。创投对菌丝体和海藻基质的投入,结合人工智慧驱动的分拣技术以提高材料利用率,正在缩小再生材料和原生材料之间的创业投资资金差距。同时,像安姆科与贝瑞世界这样的策略併购正在整合研发资源,加速下一代产品形式的商业化。

全球永续包装市场趋势与洞察

生产者延伸责任法促进监理协调

63个司法管辖区逐步趋同的生产者延伸责任制(EPR)义务正在减少监管碎片化。欧盟《包装与包装废弃物法规》将于2025年2月生效,该法规规定PET食品包装的再生材料含量目标为30%,并禁止使用全氟烷基和多氟烷基物质(PFAS)。经合组织(OECD)和金砖国家也正在引入类似的框架。肯亚的新法效法了欧盟的收费系统,奥勒冈州和科罗拉多将从2025年7月起要求品牌方出资设立生产者责任组织(PRO)。统一的时间表使全球品牌能够大规模部署单一的设计方案,从而降低合规成本,并加速永续包装市场的应用。

品牌致力于推动PCR内容标准化,使其高于监管最低标准。

如今,大型消费品公司正超越法律要求,公开承诺到2030年,其所有产品系列中将使用25%至50%的消费后回收材料(PCR)。联合利华的目标是到2025年实现所有包装可回收、可重复使用或可堆肥,而安姆科为吉百利包装供应1000吨再生塑料,这些都是自愿性目标逐渐成为行业事实上的标准的绝佳例证。美国塑胶公约的标准化PCR测量工具包简化了检验,提高了采购流程的透明度,并有助于永续包装市场的发展。

PCR树脂供应限製成策略瓶颈

目前,品牌承诺的用量超过了透明食品级消费后回收树脂(PCR树脂)的供应量。牛奶消费量的下降导致天然高密度聚乙烯(HDPE)供应量减少,推高了高价,迫使企业依赖进口,损害了国内回收企业的利益。这种供需失衡威胁到监管配额的及时完成,并阻碍了永续包装在大众市场的扩张。

细分市场分析

儘管可回收包装形式在2025年之前仍保持44.88%的市场份额,但可堆肥和可生物降解产品的市场以12.32%的复合年增长率增长,反映出投资者对B'Zeos等生物基材料(例如其海藻薄膜)的信心。可堆肥包装市场规模的成长主要受餐饮服务业和个人护理品牌的需求所驱动,这些品牌寻求无需粉碎微塑胶的解决方案。然而,美国祇有30%的城市拥有工业堆肥设施,这限制了可堆肥包装在短期内的普及。为此,《堆肥法案》(COMPOST Act)提案津贴20亿美元扩大堆肥能力,预计将直接提高废弃物回收率和长期成长前景。

消费者对垃圾处理的困惑持续导致有机废弃物污染,因此亟需更清晰的标籤和公共意识宣传活动。厌氧消化正逐渐成为一种替代方案,它透过产生沼气收入来提高计划经济效益,并部分弥补基础设施的不足。随着政策与处理技术之间的差距逐渐缩小,可堆肥包装预计将在永续包装市场中占据越来越大的份额。

到2025年,纸和纸板将占总收入的39.96%,这主要得益于成熟的回收系统和消费者的信任。同时,植物来源基材正以11.21%的复合年增长率稳定发展,主要得益于Straenso的干式模塑纤维线,生产线可减少75%的用水量和30%的能源消耗,进而提升其对循环经济的贡献。由于PFAS禁令的实施和更严格的再生材料含量法规,聚烯在永续包装市场的份额预计将逐步萎缩。

先进回收技术的进步,例如伯克利实验室的260°C汽化製程(可将聚乙烯转化为原料,回收率高达98%),使得食品级回收成为可能,并减少了降级回收。菌丝泡棉和木质PET替代品的应用范围正在从小众领域扩展到更广泛的领域,这标誌着材料转化技术在永续包装市场中广泛应用。

区域分析

到2025年,欧洲将占据34.18%的收入份额,这反映了其领先的监管立场,该立场促成了成熟的回收基础设施和生态设计标准。根据循环利用绩效调整生产者延伸责任(EPR)费用,鼓励使用高再生材料含量的包装,并加强供应商的创新循环。统一的押金返还系统简化了回收流程,使欧洲成为先进回收示范计画和生物基材料商业化的标竿市场。总部位于该地区的跨国品牌进一步推动了需求成长,为永续包装市场在当地持续测试和推广创新奠定了坚实的基础。

亚太地区预计将实现11.05%的复合年增长率,成为成长最快的地区,这主要得益于日本、韩国和澳洲日益严格的监管,以及中国和印度试点推行的生产者责任延伸制度(EPR)。日本将于2024年生效的强制性再生塑胶法规,以及2025年6月生效的再生食品接触树脂正面表列,将释放再生塑胶的巨大应用潜力,并刺激国内树脂再加工投资。在中国,不断完善的再生塑胶监管政策,加上强劲的电子商务成长,正在推动再生塑胶使用量的成长。越南的纸包装产业预计到2026年将达到35亿美元,是出口导向製造业推动区域扩张的典型案例。

在北美,各州推行的生产者延伸责任制(EPR)计画以及大型消费品公司积极主动的自愿倡议已被证明行之有效。奥勒冈州、科罗拉多和加利福尼亚州的计画为扩大上门回收系统提供了资金支持,有助于增加消费后回收材料(PCR)的原材料供应,并缩小成本差距。诸如澳洲的克罗克斯诉讼案等「漂绿」诉讼促使企业制定了更严格的资讯揭露要求,从而提升了消费者信任度,并促进了供应链的透明度。中东、非洲和南美地区虽然仍在发展中,但其政策正在迅速趋同,基础设施也在不断完善,这为早期技术进入者创造了尚未开发的机会。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 经合组织和金砖国家市场中生产者延伸责任制(EPR)法律的普及

- 品牌所有者的承诺推动产品组合中超过 25% 的 PCR 含量。

- 零售商的回收和再利用试点项目正在电子商务物流领域不断扩展。

- 利用人工智慧分类技术提高废弃产品回收率

- 食品级聚烯化学回收技术突破

- 一家专注于菌丝体和海藻包装的新创公司获得了创业投资。

- 市场限制

- 高品质PCR树脂的供需缺口

- 与原生基材相比的通膨成本溢价

- 北美和亚太地区的堆肥基础设施分散

- 由于面临「绿色清洗」诉讼风险,行销宣传内容有所变更

- 供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 竞争对手之间的竞争

- 替代品的威胁

- 评估微观经济因素的影响

第五章 市场规模与成长预测

- 透过流程

- 可重复使用的包装

- 可回收包装

- 可堆肥/可生物降解包装

- 可食用包装

- 依材料类型

- 纸和纸板

- 塑胶

- 玻璃

- 金属(铝、钢)

- 植物来源材料(甘蔗渣、蘑菇等)

- 按包装类型

- 死板的

- 灵活的

- 按功能

- 初级包装

- 二级包装

- 三级包装/运输包装

- 最终用户

- 食品/饮料

- 製药和医疗保健

- 化妆品和个人护理

- 电子商务与零售

- 家用电子电器

- 其他最终用户

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲和纽西兰

- 亚太其他地区

- 中东和非洲

- 中东

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 埃及

- 其他非洲地区

- 中东

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Amcor plc

- Smurfit WestRock Company

- Tetra Pak International SA

- Sonoco Products Company

- Sealed Air Corporation

- Mondi plc

- Huhtamaki Oyj

- BASF SE

- Ardagh Group SA

- Ball Corporation

- Crown Holdings Inc.

- Genpak LLC

- International Paper Company

- Stora Enso Oyj

- Graphic Packaging Holding Co.

- Uflex Ltd.

- Novolex Holdings Inc.

- Ecovative LLC

第七章 市场机会与未来展望

The sustainable packaging market was valued at USD 303.80 billion in 2025 and estimated to grow from USD 325.94 billion in 2026 to reach USD 463.41 billion by 2031, at a CAGR of 7.29% during the forecast period (2026-2031).

Momentum is anchored in converging Extended Producer Responsibility (EPR) regulations that now span 63 countries, eliminating regulatory arbitrage and unlocking cross-border scale efficiencies. Brand commitments to minimum recycled-content thresholds, rapid progress in chemical recycling technologies, and rising e-commerce volumes that demand packaging right-sizing are accelerating capital deployment toward circular solutions. Venture funding into mycelium and seaweed-based substrates, coupled with AI-enabled sortation that improves material yields, is narrowing the cost gap between recycled and virgin feedstocks. Simultaneously, strategic mergers-such as the Amcor-Berry Global tie-up-are consolidating research and development resources to speed commercialization of next-generation formats.

Global Sustainable Packaging Market Trends and Insights

Extended Producer-Responsibility Laws Create Compliance Convergence

Converging EPR mandates in 63 jurisdictions are dismantling regulatory fragmentation. The European Union's Packaging and Packaging Waste Regulation, effective February 2025, sets 30% recycled-content targets for PET food packaging and bans PFAS, prompting similar frameworks across OECD and BRICS economies. New Kenyan statutes mirror EU fee structures, while Oregon and Colorado require brand-funded Producer Responsibility Organizations from July 2025. Harmonized timelines let global brands deploy single-design solutions at scale, lowering compliance costs and accelerating adoption across the sustainable packaging market.

Brand Commitments Drive PCR Content Standardization Beyond Regulatory Minimums

Major consumer-goods firms now exceed legislation by pledging 25-50% post-consumer recycled (PCR) content portfolio-wide by 2030. Unilever's 2025 goal for all packaging to be recyclable, reusable, or compostable and Amcor's supply of 1,000 tons of recycled plastic for Cadbury wrappers exemplify voluntary targets setting de facto industry baselines. Standardized PCR measurement toolkits from the U.S. Plastics Pact streamline verification, catalyzing procurement clarity and fueling growth in the sustainable packaging market.

PCR Resin Supply Constraints Create Strategic Bottlenecks

Brand pledges now outstrip supply of clear, food-grade PCR. Declining milk volumes shrink the natural HDPE stream, inflating premiums and forcing import reliance that undercuts domestic reclaimers. This imbalance threatens timely fulfillment of regulatory quotas, slowing mass-market expansion of the sustainable packaging market.

Other drivers and restraints analyzed in the detailed report include:

- E-commerce Logistics Pilots Scale Reusable Packaging Systems

- AI-Enhanced Sortation Technologies Improve Recycling Economics

- Cost Premium Persistence Challenges Mass-Market Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recyclable formats retained a 44.88% share in 2025, yet compostable and biodegradable offerings are growing at a 12.32% CAGR, reflecting investor faith in biomaterials such as B'Zeos' seaweed films. The sustainable packaging market size for compostables is riding demand from food-service and personal-care brands seeking solutions free from microplastic fragmentation. However, only 30% of U.S. municipalities have access to industrial composting sites, curbing near-term penetration. In response, the U.S. COMPOST Act proposes USD 2 billion in grants to expand capacity, which would directly lift diversion rates and long-run growth prospects.

Consumer confusion over end-of-life handling still triggers contamination in organic-waste streams, calling for clearer labeling and public-education campaigns. Anaerobic digestion has emerged as an alternate pathway, generating biogas revenue that improves project economics and partially offsets infrastructure shortfalls. With policy and processing gaps gradually closing, compostable formats are set to capture an expanding slice of the sustainable packaging market.

Paper and paperboard represented 39.96% of 2025 revenue owing to mature recycling systems and consumer trust. Plant-based substrates, however, are advancing at 11.21% CAGR, propelled by Stora Enso's dry-forming fiber lines that cut water use by 75% and energy by 30%, boosting circularity credentials. The sustainable packaging market share of polyolefins is expected to contract gradually as PFAS bans and recycled-content rules intensify.

Advanced recycling breakthroughs, including Berkeley's 260 °C vaporization process that converts polyethylene into feedstock with 98% recovery, enable food-grade loops and mitigate downcycling. Mycelium foams and wood-based PET replacements are expanding addressable use cases beyond niche segments, signaling a broader materials transition within the sustainable packaging market.

The Sustainable Packaging Market Report is Segmented by Process (Reusable, Recyclable, and More), Material Type (Paper and Paperboard, Plastics, and More), Packaging Format (Rigid, Flexible), Function (Primary, Secondary, Tertiary/Transport), End User (Food and Beverage, Pharmaceutical and Healthcare, Cosmetics and Personal Care, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe's 34.18% revenue share in 2025 reflects its first-mover regulatory stance that has birthed mature recycling infrastructure and eco-design norms. EPR fee modulation by circularity performance incentivizes high-recycled-content packaging, reinforcing supplier innovation cycles. Harmonized deposit-return schemes streamline collection, making Europe the reference market for both advanced recycling pilots and bio-based material commercialization. Multinational brand headquarters located in the region further amplify demand density, ensuring the sustainable packaging market continues to test and scale breakthroughs locally.

Asia-Pacific is on track for the fastest 11.05% CAGR thanks to tightening rules in Japan, South Korea, Australia, and pilot EPR frameworks in China and India. Japan's recycled-plastic mandate effective 2024 and its positive list for food-contact recycled resins entering force in June 2025 unlock high-margin applications and spur domestic resin reprocessing investments. China's evolving supervision policy for recycled plastics coupled with strong e-commerce growth accelerates volume uptake. Vietnam's paper-packaging sector, projected at USD 3.5 billion by 2026, exemplifies regional expansion anchored in export-oriented manufacturing.

North America benefits from state-level EPR adoption and aggressive voluntary commitments by consumer-goods leaders. Oregon, Colorado, and California programs fund curbside upgrades, boosting PCR feedstock availability and narrowing cost spreads. Greenwashing litigation-exemplified by Australia's recent Clorox action-raises disclosure rigor, bolstering consumer trust and driving transparent supply chains. Middle East & Africa and South America remain nascent but show rapid policy convergence, opening white-space opportunities for early technology entrants as infrastructure scales.

- Amcor plc

- Smurfit WestRock Company

- Tetra Pak International SA

- Sonoco Products Company

- Sealed Air Corporation

- Mondi plc

- Huhtamaki Oyj

- BASF SE

- Ardagh Group SA

- Ball Corporation

- Crown Holdings Inc.

- Genpak LLC

- International Paper Company

- Stora Enso Oyj

- Graphic Packaging Holding Co.

- Uflex Ltd.

- Novolex Holdings Inc.

- Ecovative LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Extended producer-responsibility (EPR) laws surge in OECD and BRICS markets

- 4.2.2 Brand-owner pledges driving >25 % PCR content across portfolios

- 4.2.3 Retailer take-back and reuse pilots scaling in e-commerce logistics

- 4.2.4 AI-enabled sortation raising post-consumer recycling yields

- 4.2.5 Food-grade chemical recycling breakthroughs for polyolefins

- 4.2.6 Emerging mycelium and seaweed packaging securing venture capital

- 4.3 Market Restraints

- 4.3.1 Supply-demand gap in high-quality PCR resins

- 4.3.2 Inflation-driven cost premium vs. virgin substrates

- 4.3.3 Fragmented composting infrastructure in North America and APAC

- 4.3.4 "Greenwashing" litigation risk altering marketing claims

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitutes

- 4.8 Assessment of Impact of Microeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Process

- 5.1.1 Reusable Packaging

- 5.1.2 Recyclable Packaging

- 5.1.3 Compostable / Biodegradable Packaging

- 5.1.4 Edible Packaging

- 5.2 By Material Type

- 5.2.1 Paper and Paperboard

- 5.2.2 Plastics

- 5.2.3 Glass

- 5.2.4 Metal (Aluminum, Steel)

- 5.2.5 Plant-based Materials (Bagasse, Mushroom, etc.)

- 5.3 By Packaging Format

- 5.3.1 Rigid

- 5.3.2 Flexible

- 5.4 By Function

- 5.4.1 Primary Packaging

- 5.4.2 Secondary Packaging

- 5.4.3 Tertiary / Transport Packaging

- 5.5 By End User

- 5.5.1 Food and Beverage

- 5.5.2 Pharmaceutical and Healthcare

- 5.5.3 Cosmetics and Personal Care

- 5.5.4 E-commerce and Retail

- 5.5.5 Consumer Electronics

- 5.5.6 Other End User

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 United Arab Emirates

- 5.6.4.1.2 Saudi Arabia

- 5.6.4.1.3 Turkey

- 5.6.4.1.4 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Nigeria

- 5.6.4.2.3 Egypt

- 5.6.4.2.4 Rest of Africa

- 5.6.4.1 Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 Smurfit WestRock Company

- 6.4.3 Tetra Pak International SA

- 6.4.4 Sonoco Products Company

- 6.4.5 Sealed Air Corporation

- 6.4.6 Mondi plc

- 6.4.7 Huhtamaki Oyj

- 6.4.8 BASF SE

- 6.4.9 Ardagh Group SA

- 6.4.10 Ball Corporation

- 6.4.11 Crown Holdings Inc.

- 6.4.12 Genpak LLC

- 6.4.13 International Paper Company

- 6.4.14 Stora Enso Oyj

- 6.4.15 Graphic Packaging Holding Co.

- 6.4.16 Uflex Ltd.

- 6.4.17 Novolex Holdings Inc.

- 6.4.18 Ecovative LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

可回收种植袋市场:按材料、应用、最终用户、分销管道和层数划分-2026-2032年全球市场预测

可回收种植袋市场:按材料、应用、最终用户、分销管道和层数划分-2026-2032年全球市场预测 2026年全球永续产品市场报告

2026年全球永续产品市场报告 永续和环保材料市场预测至2034年:按材料类型、产品、技术、应用、最终用户和地区分類的全球分析

永续和环保材料市场预测至2034年:按材料类型、产品、技术、应用、最终用户和地区分類的全球分析 全球永续包装市场规模、份额、趋势和成长分析报告(2026-2034年)

全球永续包装市场规模、份额、趋势和成长分析报告(2026-2034年) 日本永续包装市场规模、份额、趋势及预测(按材料、类型、包装形式、工艺、应用和地区划分,2026-2034年)2026年全球永续包装市场报告2026年全球环保包装市场报告

日本永续包装市场规模、份额、趋势及预测(按材料、类型、包装形式、工艺、应用和地区划分,2026-2034年)2026年全球永续包装市场报告2026年全球环保包装市场报告 永续包装市场-全球产业规模、份额、趋势、机会和预测:按材料、工艺、最终用途、地区和竞争格局划分,2021-2031年零废弃包装市场-2026-2031年预测永续与升级再造食品配料市场预测至2032年:按配料类型、来源、形态、分销管道、应用和地区分類的全球分析

永续包装市场-全球产业规模、份额、趋势、机会和预测:按材料、工艺、最终用途、地区和竞争格局划分,2021-2031年零废弃包装市场-2026-2031年预测永续与升级再造食品配料市场预测至2032年:按配料类型、来源、形态、分销管道、应用和地区分類的全球分析