|

市场调查报告书

商品编码

1940615

超薄玻璃:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Ultra-Thin Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

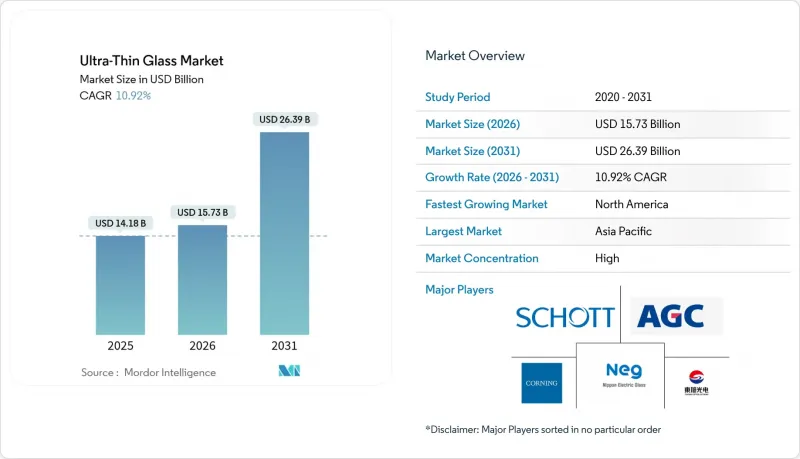

2025年超薄玻璃市场价值141.8亿美元,预计2031年将达到263.9亿美元,高于2026年的157.3亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 10.92%。

多项技术变革正在推动这一扩张:折迭式消费性电子设备需要可弯曲的保护玻璃,电动车指定使用轻质玻璃以减轻电池负载,而基于晶片组的处理器则需要玻璃中介层来维持日益密集的I/O上的讯号保真度。亚毫米级的厚度也为microLED和柔性OLED显示器开闢了新的光学堆迭结构,而化学强化面板则提高了高阶智慧型手机的抗摔性和抗刮擦性。半导体巨头不断增加对玻璃基板的资本投入,加上汽车製造商转向全景抬头显示器,正在推动三大高附加价值价值链的需求成长。儘管原料纯度要求和精密成型製程仍然推高了成本结构,但由于连续浮法和熔融拉丝生产线的不断升级,与传统平板玻璃的价格差距正在缩小。

全球超薄玻璃市场趋势及展望

家用电器需求不断成长

超薄玻璃市场仍然高度依赖消费性电子产品,智慧型手机、平板电脑和穿戴式装置的出货量激增是推动这一市场成长的主要动力。三星Galaxy Z Fold 6采用厚度小于100微米的化学强化玻璃,使其能够承受数十万次的弯曲,同时保持光学清晰度。康宁的第二代大猩猩玻璃陶瓷则整合了奈米晶体,在不牺牲透明度的前提下提高了硬度。设备製造商还在产品中加入了超薄玻璃天线窗口,以最大限度地提高5G吞吐量,从而增强了跨组件的需求。越南和印度的供应链本地化进一步提高了出货速度,并促进了面板製造商和玻璃供应商之间更紧密的合作。这些因素共同推动了单一设备平均玻璃面积的增加,即使在出货量成长放缓的情况下也是如此,为超薄玻璃市场奠定了稳定且持续多年的收入基础。

折迭式智慧型手机和笔记型电脑的快速普及

柔性萤幕的出现将推动面积增长,因为折迭式萤幕的玻璃面积将是传统智慧型手机的两到三倍。肖特公司厚度仅30微米的超薄玻璃,在1毫米半径下可承受超过30万次的弯曲,创下了行业纪录。笔记型电脑製造商目前正在开发可将17吋折迭式机型折迭至13吋的原型机,这将增加每台设备的基板需求。双方共同开发的防爆涂层能够分散表面应力,使组装能够从聚酰亚胺薄膜转向更坚硬的玻璃表面。随着价格差异的缩小,预计到2027年,折迭式设备在旗舰机型出货量中的占比将达到两位数,这将为超薄玻璃市场带来强劲的销售成长动力。

高纯度原料及精密加工成本高成本

半导体级砂的纯度必须达到99.999%。北卡罗来纳州斯普鲁斯派恩的矿床是少数的来源之一,根据供应商价目表,其价格为每吨1万美元。熔拉炉需要铂铑合金通道和超洁净气氛,因此,一条用于生产第十代显示器尺寸的生产线需要3.5亿美元的资本投入。小规模的新参与企业难以摊销这些支出,导致产能部署缓慢,并在短期规划週期内限制了超薄玻璃市场的成长速度。

细分市场分析

钠钙玻璃配方具有规模化和成长潜力,预计到2025年将占据45.52%的市场份额,并维持11.55%的复合年增长率。与铝硅酸盐相比,其熔点更低,可降低高达15%的炉能耗,符合脱碳承诺。 NSG的UFF浮法玻璃符合AMOLED保护玻璃的光学平整度要求,同时含有35%的玻璃屑。新型铝硅酸盐产品,如康宁的Gorilla Glass,硬度高达800维氏硬度,广泛应用于高阶行动电话和汽车内装。硼硅酸和无碱玻璃具有卓越的抗热衝击性能,适用于半导体电介质。

高阶市场推高了平均售价,但钠钙玻璃强大的生产能力为大批量生产的行动电话机型提供了成本优势,确保其在超薄玻璃市场中占据基石地位。製造商正在对钠钙玻璃片材进行离子交换处理以弥补其耐用性不足,而特製的锂铝铝硅酸盐玻璃则用于晶圆级光学元件和AR波导管应用。

到2025年,浮法和微浮法生产线将占总收入的50.12%,达到12.24%的最高复合年增长率。这主要得益于现代镀锡槽能够生产厚度仅0.4毫米、表面波纹度小于0.1微米的镀带。皮尔金顿最新的工厂采用逆流氮气幕抑制锡沉积,从而获得接近光学级的表面。康宁公司首创的熔融拉丝製程无需研磨或抛光即可生产无缺陷的表面,这对于高解析度显示器至关重要。下拉技术可将厚度控制在30微米以内,为折迭式盖玻片生产线提供支援。同时,卷对卷分切拉丝技术可生产用于可穿戴感测器的连续软性玻璃薄膜。

浮法玻璃的损益平衡产量仍然最低,巩固了其作为新进者进入超薄玻璃市场首选途径的地位。然而,熔融玻璃无缺陷的表面使其价格越来越高,迫使供应商实施混合生产模式,并将风险分散到各个应用领域。

区域分析

到2025年,亚太地区将占全球营收的49.08%,这主要得益于中国、韩国和日本高度整合的显示器和半导体生态系统。三星显示器第八代半OLED工厂和台积电先进封装生产线等扩建计划,支撑了浮法和熔融基板的稳定需求。日本企业正在增加用于扩增实境光学的特殊玻璃,而台湾组装正从试生产转向量产玻璃内嵌(TG)技术。然而,随着地缘政治贸易限制的收紧,区域多元化的需求变得日益迫切,韩国和日本供应商正在东南亚联合投资建设生产线,以降低物流风险。

预计北美将达到最高成长率,到2031年复合年增长率将达到11.32%,这主要得益于半导体产业的復苏以及电动车对玻璃的广泛应用。英特尔位于亚利桑那州的玻璃基板园区已安装专用熔化设备,计画于2026年开始量产。康宁公司2025年第一季财报显示,其核心销售额成长13%至37亿美元,主要得益于用于资料中心光学组件和生成式人工智慧的专用材料。此外,由中西部某州津贴在俄亥俄州建立的玻璃技术研究中心正在支持循环回收试验,这标誌着消除超薄玻璃市场废弃物瓶颈的第一步已经迈出。

欧洲是一个高科技地区,但成长速度相对较慢。 AGC Glass Europe正在投资0.3毫米厚平板玻璃的真空绝热玻璃生产线,其窗户的热传导係数(U值)低于0.5W/m²K。 Guardian和Verux正在合作开发用于净零能耗建筑的钢化真空绝热玻璃板,以满足政策主导的需求。德国和芬兰的汽车玻璃专家正在为高端电动车平台供应全景天窗,保持均衡的成长轨迹,并建立了能够引起监管机构和买家共鸣的永续性资格。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 家用电子电器需求不断成长

- 折迭式智慧型手机和笔记型电脑的快速普及

- 柔性OLED和MicroLED显示器生产线发展

- 汽车玻璃零件和抬头显示器(HUD)减轻重量的必要性

- 用于小晶片封装的玻璃中介层

- 市场限制

- 高纯度原料高成本。

- 大面积加工过程中脆性和产量比率损失

- 直径大于0.3毫米的玻璃废弃物的回收途径有限。

- 价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 按玻璃类型

- 铝硅酸盐(例如:大猩猩玻璃、龙迹玻璃)

- 不含硼硼硅酸/无碱

- 超薄钠钙

- 其他(例如铝铝硅酸盐等)

- 透过製造工艺

- 融合绘图

- 下流/溢出

- 浮子和微型浮子

- 分切/卷对卷

- 透过使用

- 半导体基板

- 触控面板显示幕

- 指纹感应器

- 汽车玻璃

- 其他应用(例如,汽车显示器和玻璃製品)

- 按最终用户行业划分

- 家用电子电器

- 车

- 生物技术

- 其他终端用户产业(能源、电力等)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- AGC Inc.

- Central Glass Co., Ltd.

- Changzhou Almaden Co., Ltd.

- Corning Incorporated

- CSG Holding Co., Ltd.

- Emerge Glass

- Fraunhofer

- Irico Group New Energy Company Limited

- Nippon Electric Glass Co., Ltd.

- Nippon Sheet Glass Co., Ltd.

- Nitto Denko Corporation.

- OFILM

- Samsung

- SCHOTT AG

- Taiwan Glass Ind. Corp.

- Tunghsu Optoelectronic Technology

- Xinyi Glass Holdings Limited.

第七章 市场机会与未来展望

The Ultra-Thin Glass Market was valued at USD 14.18 billion in 2025 and estimated to grow from USD 15.73 billion in 2026 to reach USD 26.39 billion by 2031, at a CAGR of 10.92% during the forecast period (2026-2031).

Multiple technology transitions propel this expansion: foldable consumer devices need bendable cover lenses, electric vehicles specify lightweight glazing that trims battery load, and chiplet-based processors require glass interposers that preserve signal fidelity at ever-higher I/O densities. Thinness below 1 millimeter also unlocks new optical stacks for micro-LED and flexible OLED displays, while chemical-strengthened panels extend drop and scratch resistance in premium handsets. Rising capital outlays by semiconductor leaders for glass substrates, combined with automakers' shift toward panoramic head-up displays, broaden addressable demand across three high-value supply chains. Raw-material purity requirements and precision forming still elevate cost structures, yet continuous float and fusion draw line upgrades are narrowing the delta with conventional sheet glass.

Global Ultra-Thin Glass Market Trends and Insights

Growing Demand from Consumer Electronics

Surging smartphone, tablet, and wearable volumes keep the ultra-thin glass market firmly anchored to consumer electronics. Samsung's Galaxy Z Fold6 employs sub-100 µm chemically strengthened glass that bends hundreds of thousands of times while retaining optical clarity. Corning's Gorilla Glass Ceramic 2 integrates nanocrystals for higher hardness without compromising transparency. Device makers also embed thin-glass antenna windows to maximise 5G throughput, reinforcing cross-component pull. Supply-chain localisation within Vietnam and India further raises shipment velocity, tightening collaboration between panel makers and glass suppliers. These factors collectively push average glass area per handset upward even as unit growth moderates, cementing a stable multi-year revenue foundation for the ultra-thin glass market.

Rapid Adoption in Foldable Smartphones & Notebooks

Flexible form factors drive incremental square metres because each foldable display uses two to three times the glass area of a bar-type phone. SCHOTT's ultra-thin glass reached 30 µm thickness while withstanding over 300,000 bends at 1 mm radius, an industry record. Notebook makers now prototype 17-inch fold-outs that collapse into 13-inch footprints, multiplying substrate demand per device. Co-developed anti-shatter coatings distribute surface stress, letting assemblers trade polyimide films for harder glass facings. With price premiums narrowing, foldable penetration is expected to hit double-digit share of flagship shipments by 2027, embedding strong volume tailwinds within the ultra-thin glass market.

High Cost of High-Purity Raw Materials & Precision Processing

Semiconductor-grade sand must achieve 99.999% purity; deposits in Spruce Pine, North Carolina are one of the few sources and regularly command USD 10,000 per ton according to supplier price lists. Fusion draw furnaces require platinum-rhodium channels and ultra-clean atmospheres, inflating capital intensity to USD 350 million per line for Gen-10 display sizes. Smaller entrants struggle to amortise such outlays, slowing capacity diffusion and tempering the ultra-thin glass market growth rate in near-term planning cycles.

Other drivers and restraints analyzed in the detailed report include:

- Advancements in Flexible OLED & Micro-LED Display Lines

- Weight-Reduction Needs in Automotive Glazing & HUDs

- Brittleness & Yield Loss During Large-Area Handling

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soda-lime compositions delivered scale and growth, posting a 45.52% share in 2025 while maintaining a 11.55% CAGR outlook. Their lower melting temperatures cut furnace energy by up to 15% versus aluminosilicate, aligning with decarbonisation pledges. NSG's UFF float glass now integrates 35% cullet yet meets optical flatness for AMOLED cover lenses. Aluminosilicate entrants like Corning's Gorilla Glass reach 800 Vickers hardness, serving premium phones and automotive interiors. Borosilicate and alkali-free variants underpin semiconductor dielectrics owing to superior thermal shock resistance.

Premium segments lift average selling prices, but soda-lime's entrenched production base provides cost leverage for mass handset models, ensuring it remains the anchor of the ultra-thin glass market. Manufacturers layer ion-exchange treatments on soda-lime sheets to bridge durability gaps, while specialized lithium-aluminosilicate grades address wafer-level optics and AR waveguide applications.

Float and microfloat lines generated 50.12% of 2025 revenue and enjoy the highest 12.24% CAGR because modern tin baths now output ribbons as thin as 0.4 mm with surface waviness under 0.1 µm. Pilkington's latest plant leverages counter-current nitrogen curtains to suppress tin pick-up, delivering near-optical-grade surfaces. Pioneered by Corning, fusion draw methods yield defect-free surfaces without grinding or polishing, crucial for high-resolution displays. Down-draw techniques allow 30 µm thickness control, servicing foldable cover glass lines, while roll-to-roll slit draw opens continuous flexible glass webs for wearable sensors.

Break-even throughput for float remains the lowest, cementing its status as the entry route for new participants in the ultra-thin glass market. Yet fusion's pristine surfaces increasingly command premium price tiers, pushing suppliers to run hybrid operations and diversify risk across application buckets.

The Ultra-Thin Glass Market Report Segments the Industry by Glass Type (Aluminosilicate, Soda-Lime Ultra-Thin, and More), Manufacturing Process (Fusion Draw, Down-Draw / Overflow, and More), Application (Semiconductor Substrate, Touch Panel Displays, and More), End-User Industry (Automotive, Biotechnology, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 49.08% of 2025 revenue thanks to densely integrated display and semiconductor ecosystems in China, South Korea, and Japan. Expansion programs such as Samsung Display's Gen-8.6 OLED fab and TSMC's advanced packaging lines provide stable pull for float and fusion substrates. Japanese firms add specialised glass for augmented-reality optics, while Taiwanese assemblers ramp through-glass via pilot runs. Regional diversification, though, gains urgency as geopolitical trade rules tighten, prompting Korean and Japanese suppliers to co-invest in lines within Southeast Asia to derisk logistics.

North America is projected to register the fastest 11.32% CAGR through 2031 due to semiconductor reshoring and electric-vehicle glass adoption. Intel's Arizona glass substrate campus targets risk production in 2026 and has already procured specialised fusion equipment. Corning's 2025 first-quarter results showed 13% core sales growth to USD 3.7 billion, buoyed by specialty materials for generative-AI data-centre optics. Midwest state incentives also fund a Glass Centre of Excellence in Ohio that supports circular recycling trials, an early step toward easing waste bottlenecks for the ultra-thin glass market.

Europe remains a technology-rich yet moderately paced terrain. AGC Glass Europe invests in vacuum-insulated glass lines that leverage 0.3 mm panes to hit <0.5 W/m2K window U-factors. Guardian and VELUX co-develop tempered VIG panes for net-zero buildings, underscoring policy-driven demand. Automotive glazing specialists in Germany and Finland supply panoramic roofs for premium EV platforms, sustaining a balanced growth path and embedding sustainability credentials that resonate with regulators and buyers alike.

- AGC Inc.

- Central Glass Co., Ltd.

- Changzhou Almaden Co., Ltd.

- Corning Incorporated

- CSG Holding Co., Ltd.

- Emerge Glass

- Fraunhofer

- Irico Group New Energy Company Limited

- Nippon Electric Glass Co., Ltd.

- Nippon Sheet Glass Co., Ltd.

- Nitto Denko Corporation.

- OFILM

- Samsung

- SCHOTT AG

- Taiwan Glass Ind. Corp.

- Tunghsu Optoelectronic Technology

- Xinyi Glass Holdings Limited.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand from consumer electronics

- 4.2.2 Rapid adoption in foldable smartphones & notebooks

- 4.2.3 Advancements in flexible OLED & micro-LED display lines

- 4.2.4 Weight-reduction needs in automotive glazing & HUDs

- 4.2.5 Glass interposers for chiplet packaging

- 4.3 Market Restraints

- 4.3.1 High cost of high-purity raw materials & precision processing

- 4.3.2 Brittleness & yield loss during large-area handling

- 4.3.3 Limited recycling streams for greater than 0.3 mm glass waste

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Glass Type

- 5.1.1 Aluminosilicate (e.g., Gorilla, Dragontrail)

- 5.1.2 Borosilicate / Alkali-Free

- 5.1.3 Soda-Lime Ultra-Thin

- 5.1.4 Others (Lithium-Aluminosilicate, etc.)

- 5.2 By Manufacturing Process

- 5.2.1 Fusion Draw

- 5.2.2 Down-Draw / Overflow

- 5.2.3 Float & Microfloat

- 5.2.4 Slit Draw / Roll-to-Roll

- 5.3 By Application

- 5.3.1 Semiconductor Substrate

- 5.3.2 Touch Panel Displays

- 5.3.3 Fingerprint Sensors

- 5.3.4 Automotive Glazing

- 5.3.5 Other Applications (Automotive Displays and Glazing, etc.)

- 5.4 By End-User Industry

- 5.4.1 Consumer Electronics

- 5.4.2 Automotive

- 5.4.3 Biotechnology

- 5.4.4 Other End-User Industries (Energy and Power, etc.)

- 5.5 By Region

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 AGC Inc.

- 6.4.2 Central Glass Co., Ltd.

- 6.4.3 Changzhou Almaden Co., Ltd.

- 6.4.4 Corning Incorporated

- 6.4.5 CSG Holding Co., Ltd.

- 6.4.6 Emerge Glass

- 6.4.7 Fraunhofer

- 6.4.8 Irico Group New Energy Company Limited

- 6.4.9 Nippon Electric Glass Co., Ltd.

- 6.4.10 Nippon Sheet Glass Co., Ltd.

- 6.4.11 Nitto Denko Corporation.

- 6.4.12 OFILM

- 6.4.13 Samsung

- 6.4.14 SCHOTT AG

- 6.4.15 Taiwan Glass Ind. Corp.

- 6.4.16 Tunghsu Optoelectronic Technology

- 6.4.17 Xinyi Glass Holdings Limited.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

- 7.2 Development of Advanced Glass for Solar Energy Projects

超薄玻璃市场:按材料、厚度、製造流程、应用和最终用户划分-2026-2032年全球市场预测

超薄玻璃市场:按材料、厚度、製造流程、应用和最终用户划分-2026-2032年全球市场预测 超薄玻璃市场规模、份额和成长分析(按厚度、製造流程、应用、终端用户产业和地区划分)-2026-2033年产业预测

超薄玻璃市场规模、份额和成长分析(按厚度、製造流程、应用、终端用户产业和地区划分)-2026-2033年产业预测 全球超薄透明玻璃市场

全球超薄透明玻璃市场 全球超薄玻璃市场规模(按厚度范围、应用、最终用户产业、区域范围和预测)

全球超薄玻璃市场规模(按厚度范围、应用、最终用户产业、区域范围和预测) 2032年超薄玻璃市场预测:全球厚度、製造流程、应用、最终用户和地区分析

2032年超薄玻璃市场预测:全球厚度、製造流程、应用、最终用户和地区分析 超薄玻璃市场规模、份额、趋势分析报告:按应用、地区、细分市场、预测,2025-2030 年

超薄玻璃市场规模、份额、趋势分析报告:按应用、地区、细分市场、预测,2025-2030 年 超薄玻璃市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

超薄玻璃市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 超薄玻璃市场,按製造流程、按应用、按最终用户、按国家和地区划分 - 2024-2032 年行业分析、市场规模、市场份额和预测

超薄玻璃市场,按製造流程、按应用、按最终用户、按国家和地区划分 - 2024-2032 年行业分析、市场规模、市场份额和预测