|

市场调查报告书

商品编码

1940665

特种车辆:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)Specialty Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

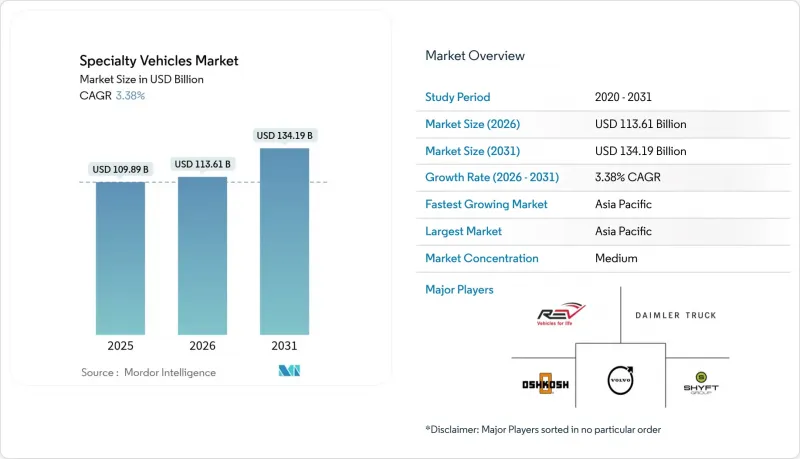

2025年特种车辆市场价值为1,098.9亿美元,预计到2031年将达到1,341.9亿美元,而2026年为1,136.1亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 3.38%。

强劲的需求主要来自非选择性支出领域,例如紧急医疗服务、公共和工业支援车辆。不断扩大的城市基础设施、人口老化带来的紧急应变需求以及政府对零排放车辆的激励措施,共同支持全球采购活动。随着优先发展电动车的新兴参与企业利用模组化设计和互联技术缩短客製化前置作业时间并降低营运成本,竞争日益激烈。同时,老牌製造商则透过认证平台和覆盖全国的售后服务网络来捍卫市场份额。

全球特种车辆市场趋势与洞察

对紧急医疗救援车辆的需求不断增长

人口老化和更严格的回应时间规定迫使医疗系统扩充救护车队。美国医疗保险和医疗补助服务中心 (CMS) 扩大了社区紧急医疗服务的报销范围,增加了对高级生命支持车辆的拨款。都市区密度的增加进一步提高了对配备齐全、能够快速到达现场的车辆的需求。社区健康计画也强调移动诊所的重要性,这些诊所可以提供诊断、疫苗接种和慢性病后续照护。这些因素共同促成了永续采购,即便市政营运预算面临压力。在不断扩展的零排放都市区地区,电动动力传动系统正越来越多地应用于营运週期。

建筑和矿业服务车辆的成长

大型计划和资源开采作业正在将特种车辆市场拓展至严苛环境。美国《基础建设投资与就业法案》在2022至2026财年累计1.2兆美元,用于支援移动式油罐车、服务车厢和现场指挥中心的需求。中国的「一带一路」倡议也同样刺激了亚太和非洲地区对特种服务车辆的需求。日益严格的安全法规要求车辆配备防尘系统、即时远端资讯处理系统和紧急疏散设施。偏远矿区正在部署行动环境监测实验室,以满足ESG(环境、社会和管治)要求。儘管建设週期仍易受宏观经济波动的影响,但老旧车辆的更新换代为年度需求提供了基础。

高额的购置成本与生命週期成本

由于专用设备、小批量生产和严格的相容性测试,专用车辆的价格通常比主流商用平台高出 40% 至 60%。电动车的价格更高,但其燃油和维护成本的节省可在 7 至 10 年内累积。许多市政当局推迟车队升级,并将车队使用寿命延长至超出建议週期,增加了运作风险。由于更换零件和专业维修费用上涨,保险费率也在上涨。小规模私人业者感受到的压力最大,有时会选择租赁模式以避免资本支出。从不銹钢罐到医疗用电子设备,持续高昂的投入成本可能会阻碍预算灵活性有限的地区的采用。

细分市场分析

到2025年,救护车将占据特种车辆市场最大份额,收入占比达31.05%,这主要得益于强制性更新週期和社区紧急医疗服务部署的增加。随着人口老化和监管机构对快速反应时间的重视,这一细分市场有望继续保持其主导地位。行动医疗车虽然绝对规模较小,但却是快速成长的品类,在预防医学和临时疫苗接种点兴起的推动下,其复合年增长率将达到5.30%。消防车将维持来自公共部门的稳定订单,而由于灾害管理日益复杂,对指挥中心的需求也将增加。

在人口密集的城市中心运作的救护车队中,电气化进程最为迅速,因为夜间在车库充电可以配合轮班安排,而且零排放区也在不断扩大。消防车的电气化进程相对滞后,主要是因为需要高功率水泵,但混合动力辅助系统正在试验中。工业设施专用油罐车由于续航里程和负载容量的要求,仍然使用柴油动力。那些能够实现底盘和电气系统标准化,同时保持模组化内饰的製造商,将在这个特种车辆市场占据越来越大的份额。

到2025年,医疗保健服务将占总需求的35.62%,这主要得益于医院网路的现代化和紧急运输保险报销范围的扩大。远端医疗的发展推动了连网行动诊断设备的采购,使农村患者能够与都市区的专家进行沟通。休閒和餐饮车辆(包括豪华巴士和行动餐车)将成为成长最快的应用领域,年复合成长率达3.96%,主要受消费者对体验式休閒活动偏好的驱动。

在工业公用事业领域,移动变电站、电网维修车辆和管道检测设备的订单仍然强劲,这些设备能够降低停机成本。执法机关正在更新其车队,配备防弹装置和人工智慧态势情境察觉的新一代战术响应车辆,但订单量远不及医疗行业。活动组织者正在增加移动指挥中心和医疗分诊拖车的租赁,以满足安全标准,这进一步增强了该专业车辆市场的共享经济效应。在医疗产业,遵守美国消防协会(NFPA)救护车标准和美国食品药物管理局(FDA)医疗设备法规仍然是一大挑战,但即使在景气衰退,稳定的预算拨款也是其优势所在。

区域分析

预计到2025年,亚太地区将以36.28%的市占率引领特种车辆市场,并在2031年之前维持3.83%的复合年增长率。中国医院扩建计画和正在进行的「一带一路」建设将支撑对救护车和油罐车的强劲需求,而印度的智慧城市计画将为指挥中心和消防设备提供资金。由于旅游业的主导发展,东南亚国家的采购需求也在加速成长,这主要得益于饭店和工业服务车辆的增加。日本和韩国的汽车製造商正在为适用于人口密集城区的紧凑型电动救护车提供技术创新。

北美在特种车辆市场占有成熟且技术先进的地位。与美国消防协会(NFPA)指南修订相关的更新週期促使消防部门不断更新车队,而《基础设施投资与就业法案》则为公共产业和建筑车辆提供了资金支持。加拿大的资源型经济支撑着非公路服务车队的发展,而墨西哥以出口为导向的製造业正在订购行动维修车,以最大限度地减少生产线停机时间。零排放车辆强制令,加上广泛的气候目标,正在加速纽约、洛杉矶和多伦多的电气化进程。

欧洲在收紧监管方面处于主导,儘管年复合成长率较为缓慢。计划于2030年推出的零排放都市区区域将确保对纯电动救护车和垃圾车的需求,而欧盟的二氧化碳排放标准正推动混合动力消防车原型进入实地试验阶段。德国先进的工程技术能力正在加速模组化底盘的普及,而英国国民医疗服务体系(NHS)的车辆更新计画也在预算限制下推动了采购工作。北欧国家拥有丰富的绿氢能计划,正率先引进氢燃料电池救援车辆。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 对紧急医疗救援车辆的需求不断增长

- 建筑和矿业服务车辆增加

- 拓展移动现场工业服务

- 政府对零排放特种车辆的奖励

- 支援5G的远端控制连接平台

- 模组化底盘平台,缩短客製化前置作业时间

- 市场限制

- 高额的购置成本与生命週期成本

- 复杂的多辖区监理核准

- 定制设备领域技术纯熟劳工短缺

- 小批量生产中关键零件的采购前置作业时间较长

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按车辆类型

- 救护车

- 消防车

- 移动式油轮

- 移动指挥控制中心

- 行动医疗诊所

- 其他的

- 透过使用

- 执法机关与公共

- 医疗保健服务

- 工业和公共产业服务

- 休閒与饭店

- 其他的

- 按推进系统/动力传动系统

- 柴油引擎

- 汽油

- 杂交种

- 电动车

- 替代燃料(CNG/LNG/H2)

- 依所有权类型

- 政府和地方政府

- 私人车队营运商

- 出租/租赁

- 按地区

- 北美洲

- 我们

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ASEAN

- 澳洲和纽西兰

- 亚太其他地区

- 中东和非洲

- GCC

- 土耳其

- 南非

- 奈及利亚

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- REV Group

- Daimler Truck AG(Mercedes-Benz Special Trucks)

- Oshkosh Corporation

- Volvo Group

- Shyft Group

- LDV Inc.

- Matthews Specialty Vehicles

- Farber Specialty Vehicles

- Force Motors Limited

- Emergency One Group

- Rosenbauer International AG

- Wietmarscher Ambulanz-und Sonderfahrzeug GmbH

- XCMG Group(Special Purpose Division)

- Hyundai Everdigm

- Morita Holdings Corporation

- KME Fire Apparatus

第七章 市场机会与未来展望

The specialty vehicles market was valued at USD 109.89 billion in 2025 and estimated to grow from USD 113.61 billion in 2026 to reach USD 134.19 billion by 2031, at a CAGR of 3.38% during the forecast period (2026-2031).

Demand resilience comes from non-discretionary spending across emergency medical services, public safety, and industrial support fleets. Expansion of urban infrastructure, aging populations that raise emergency response needs, and government incentives for zero-emission fleets collectively sustain global procurement activity. Competitive intensity is rising as electric-first entrants leverage modular designs and connected technologies to compress customization lead times and lower operating costs. Meanwhile, established manufacturers protect share by pairing certified platforms with nationwide after-sales networks.

Global Specialty Vehicles Market Trends and Insights

Rising Demand for Emergency Medical Response Vehicles

Growing elderly populations and tighter response-time mandates are prompting healthcare systems to enlarge ambulance fleets. The Centers for Medicare & Medicaid Services widened reimbursement for community paramedicine, boosting capital budgets for advanced life-support vehicles. Urban density further intensifies the need for well-equipped units capable of faster scene arrival. Community-based healthcare programs also favor mobile medical clinics that can supply diagnostics, immunizations, and chronic-care follow-ups. Collectively these factors underpin sustained procurement even when municipal operating budgets face pressure. Electric powertrains are increasingly specified for city duty cycles where zero-emission zones loom.

Growth in Construction and Mining Service Fleets

Infrastructure mega-projects and resource extraction ventures are extending the specialty vehicle market's reach into rugged environments. The U.S. Infrastructure Investment and Jobs Act earmarked USD 1.2 trillion over five fiscal years (2022-2026), underpinning demand for mobile fuel tankers, service bodies, and onsite command centers . China's Belt and Road Initiative similarly keeps specialty service fleets active across Asia-Pacific and Africa. Stricter safety rules now require vehicles outfitted with dust-suppression systems, real-time telematics, and emergency shelters. Remote mines adopt mobile environmental-monitoring labs to satisfy ESG commitments. Although construction cycles remain sensitive to macroeconomic swings, replacement of aging fleets ensures a baseline of annual demand.

High Acquisition and Lifecycle Costs

Specialty vehicles often cost 40-60% more than mainstream commercial platforms due to bespoke equipment, small-batch production, and rigorous compliance testing. Electric versions elevate sticker prices even further, though fuel and maintenance savings accrue over 7-10 years. Many municipalities defer fleet refreshes, extending service life beyond recommended cycles and heightening downtime risk. Insurance premiums trend higher because replacement parts and skilled repairs command premium rates. Smaller private operators feel pressure most acutely, sometimes opting for rental models to circumvent capital outlays. Persistently high input prices-from stainless steel tanks to medical electronics-could dampen adoption where budget elasticity is limited.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Mobile On-Site Industrial Services

- Government Incentives for Zero-Emission Specialty Fleets

- Complex Multi-Jurisdictional Regulatory Approvals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ambulances generated the largest slice of the specialty vehicle market in 2025, capturing 31.05% revenue amid mandated replacement cycles and heightened community paramedicine deployment. The sub-segment is well-positioned to retain dominance given aging demographics and regulatory focus on faster response times. Mobile medical clinics, though smaller in absolute dollars, represent the breakout category with a 5.30% CAGR, reflecting healthcare's pivot to preventive outreach and pop-up vaccination hubs. Fire apparatus continues to post dependable public-sector orders, while command centers gain traction as disaster-management complexity increases.

Electrification is emerging fastest inside ambulance fleets operating in dense urban cores, where overnight depot charging aligns with duty patterns and zero-emission zones expand. Fire truck electrification lags due to high-draw pump requirements, yet hybrid assist systems are entering trials. Specialty tankers servicing industrial sites maintain diesel reliance because of range and payload needs. Manufacturers that standardize chassis and electrics while retaining modular interiors stand to capture a growing slice of this specialty vehicle market.

Medical and healthcare services accounted for 35.62% of overall 2025 demand, underpinned by hospital network modernization and expanded insurance reimbursements for ambulance transport. Telehealth growth stimulates procurement of connected mobile diagnostics units able to link rural patients to urban specialists. Recreational and hospitality vehicles, enveloping luxury motor coaches and mobile food units, form the fastest-expanding application cluster with a 3.96% CAGR as consumers favor experiential leisure activities.

Industrial utilities sustain significant orders for mobile substations, grid-repair trucks, and pipeline inspection rigs that mitigate downtime costs. Law enforcement agencies refresh fleets with next-generation tactical response vehicles featuring ballistic protection and AI-enabled situational awareness, although volumes trail medical orders. Event organizers increasingly lease mobile command suites and medical triage trailers to meet safety codes, reinforcing the sharing-economy effect across this specialty vehicle market. Compliance with NFPA ambulance standards and FDA medical device rules remains the chief hurdle in the healthcare slice, but reward comes via consistent budget allocations even in economic contractions.

The Specialty Vehicles Market Report is Segmented by Vehicle Type (Ambulances, Fire Trucks, and More), Application (Law Enforcement and Public Safety, Medical and Healthcare Services, and More), Propulsion/Powertrain (Diesel, Gasoline, and More), Ownership Model (Government and Municipal, Private Fleet Operators, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific leads the specialty vehicle market with a 36.28% share in 2025 and is tracking a 3.83% CAGR through 2031. China's hospital expansion programs and continued Belt and Road construction corridors sustain high ambulance and tanker demand, while India's Smart Cities Mission finances command centers and firefighting apparatus. Southeast Asian nations add procurement momentum as tourism-driven hospitality vehicles and industrial service fleets grow. Japanese and South Korean OEMs contribute innovation in compact electric ambulances that suit dense city streets.

North America represents a mature but technology-forward slice of the specialty vehicle market. Replacement cycles keyed to NFPA guideline updates keep fire departments renewing fleets, and the Infrastructure Investment and Jobs Act funnels funds to utility and construction vehicles. Canada's resource economy sustains off-road service rigs, while Mexico's export-oriented manufacturing base orders mobile maintenance trucks to minimize line stoppage. Electrification gathers pace in New York, Los Angeles, and Toronto where zero-emission fleet mandates converge with broader climate goals.

Europe shows moderate CAGR but leads regulatory stringency. Urban zero-emission zones slated for 2030 guarantee demand for battery-electric ambulances and refuse trucks, and EU CO2 standards push hybrid fire apparatus prototypes into field pilots. Germany's engineering depth accelerates modular chassis adoption, and the United Kingdom's NHS fleet renewal propels procurements despite fiscal constraints. Nordic countries pioneer hydrogen fuel-cell rescue vehicles on account of abundant green hydrogen projects.

- REV Group

- Daimler Truck AG (Mercedes-Benz Special Trucks)

- Oshkosh Corporation

- Volvo Group

- Shyft Group

- LDV Inc.

- Matthews Specialty Vehicles

- Farber Specialty Vehicles

- Force Motors Limited

- Emergency One Group

- Rosenbauer International AG

- Wietmarscher Ambulanz- und Sonderfahrzeug GmbH

- XCMG Group (Special Purpose Division)

- Hyundai Everdigm

- Morita Holdings Corporation

- KME Fire Apparatus

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Emergency Medical Response Vehicles

- 4.2.2 Growth in Construction and Mining Service Fleets

- 4.2.3 Expansion of Mobile On-Site Industrial Services

- 4.2.4 Government Incentives for Zero-Emission Specialty Fleets

- 4.2.5 5G-Enabled Connected Platforms for Remote Operations

- 4.2.6 Modular Chassis Platforms That Cut Customization Lead-Time

- 4.3 Market Restraints

- 4.3.1 High Acquisition and Lifecycle Costs

- 4.3.2 Complex Multi-Jurisdictional Regulatory Approvals

- 4.3.3 Skilled Labor Shortages in Custom Up-Fitting

- 4.3.4 Long Lead-Times for Low-Volume Critical Components

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Vehicle Type

- 5.1.1 Ambulances

- 5.1.2 Fire Trucks

- 5.1.3 Mobile Fuel Tankers

- 5.1.4 Mobile Command and Control Centers

- 5.1.5 Mobile Medical Clinics

- 5.1.6 Others

- 5.2 By Application

- 5.2.1 Law Enforcement and Public Safety

- 5.2.2 Medical and Healthcare Services

- 5.2.3 Industrial and Utility Services

- 5.2.4 Recreational and Hospitality

- 5.2.5 Others

- 5.3 By Propulsion / Powertrain

- 5.3.1 Diesel

- 5.3.2 Gasoline

- 5.3.3 Hybrid

- 5.3.4 Electric

- 5.3.5 Alternative Fuels (CNG / LNG / H2)

- 5.4 By Ownership Model

- 5.4.1 Government and Municipal

- 5.4.2 Private Fleet Operators

- 5.4.3 Rental / Leasing

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Australia and New Zealand

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 Turkey

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 REV Group

- 6.4.2 Daimler Truck AG (Mercedes-Benz Special Trucks)

- 6.4.3 Oshkosh Corporation

- 6.4.4 Volvo Group

- 6.4.5 Shyft Group

- 6.4.6 LDV Inc.

- 6.4.7 Matthews Specialty Vehicles

- 6.4.8 Farber Specialty Vehicles

- 6.4.9 Force Motors Limited

- 6.4.10 Emergency One Group

- 6.4.11 Rosenbauer International AG

- 6.4.12 Wietmarscher Ambulanz- und Sonderfahrzeug GmbH

- 6.4.13 XCMG Group (Special Purpose Division)

- 6.4.14 Hyundai Everdigm

- 6.4.15 Morita Holdings Corporation

- 6.4.16 KME Fire Apparatus

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

装甲巴士市场按防护等级、座位容量、动力类型、应用和销售管道,全球预测(2026-2032年)

装甲巴士市场按防护等级、座位容量、动力类型、应用和销售管道,全球预测(2026-2032年) 2026-2034年全球特种商用车市场规模、份额、趋势和成长分析报告

2026-2034年全球特种商用车市场规模、份额、趋势和成长分析报告 专用车辆市场-全球产业规模、份额、趋势、机会和预测(按类型、应用、车辆类型、地区和竞争细分,2020-2030 年)

专用车辆市场-全球产业规模、份额、趋势、机会和预测(按类型、应用、车辆类型、地区和竞争细分,2020-2030 年) 专用车辆市场:依车辆类型和地区划分

专用车辆市场:依车辆类型和地区划分 全球专用车辆市场

全球专用车辆市场 专用商用车市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

专用商用车市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 特殊车辆的全球市场:各类型,各用途,推进系统,各地区,机会,预测,2018年~2032年

特殊车辆的全球市场:各类型,各用途,推进系统,各地区,机会,预测,2018年~2032年 2030 年特种车辆市场预测:按车辆类型、推进类型、应用和地区分類的全球分析

2030 年特种车辆市场预测:按车辆类型、推进类型、应用和地区分類的全球分析 特种车辆市场,按车辆类型、燃料类型、最终用户、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

特种车辆市场,按车辆类型、燃料类型、最终用户、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测 全球特种车辆市场:按类型、应用、推进领域、电池化学、最终用途产业、地区 - 预测(至 2030 年)

全球特种车辆市场:按类型、应用、推进领域、电池化学、最终用途产业、地区 - 预测(至 2030 年)