|

市场调查报告书

商品编码

1940688

东协干混砂浆:市占率分析、产业趋势与统计、成长预测(2026-2031)ASEAN Dry Mix Mortar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

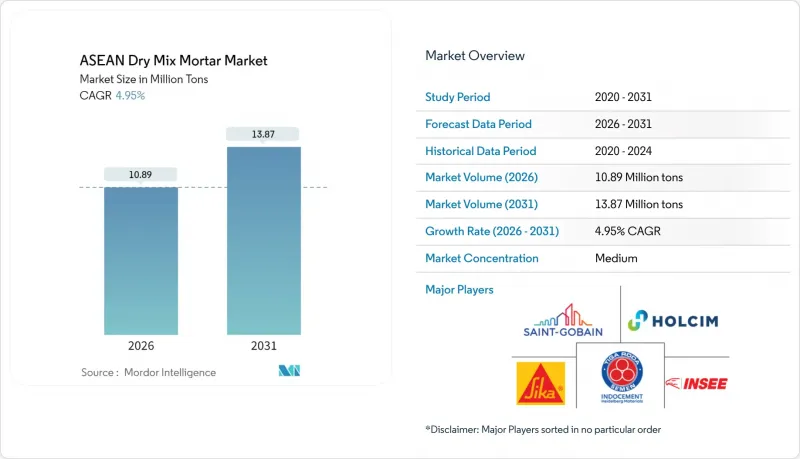

预计东协地区干混砂浆市场将从 2025 年的 1,038 万吨成长到 2026 年的 1,089 万吨,到 2031 年将达到 1,387 万吨,2026 年至 2031 年的复合年增长率为 4.95%。

这一扩张反映了大规模公共住宅项目、私人房地产市场的復苏以及工业产能的提升,从而推动了全部区域对砂浆的需求。东协干混砂浆市场受惠于快速的都市区进程、不断提高的建筑标准以及劳动成本的上升,预混预混合料解决方案因此受益。随着跨国製造商扩大本地工厂规模,以及国内水泥巨头向下游扩张并进入高附加价值砂浆市场,日益激烈的竞争正透过价值链管理和产品差异化来提升利润率。岛屿市场的物流限制和原材料价格波动仍构成结构性挑战,但也为本地工厂和能够降低运输成本的高端特种砂浆创造了机会。永续性的迫切需求,特别是低碳粘合剂体系的采用,预计将推动企业优先采购符合新环保标准的配方产品。

东协干混砂浆市场趋势及洞察

快速的都市化和大规模计划

预计到2030年,东协都市区将增加8,400万,都市化将达到56%,这将持续推高住宅、交通走廊和社会基础设施的需求。基础设施年需求量估计为600亿美元,其中跨苏门答腊收费公路和图阿斯大型港口等计划将带动砂浆消费。印尼2024年建设策略强调价值链的弹性,要求本地生产商扩大产能以满足专案进度要求。首都地区以外的区域城市正成为新的成长中心,重塑砂浆供应商的分销格局。从防洪到海岸防护,应对气候变迁需要能够承受恶劣环境的专用外加剂,从而推动对高附加价值产品的需求。

劳动力短缺导致袋装砂浆需求增加。

马来西亚和新加坡外籍劳工配额的减少和劳动力老化加剧了劳动力短缺问题。这促使建筑商采用预製砂浆,从而最大限度地减少现场施工技能要求。中小企业越来越倾向于使用标准化混合料,以确保品质稳定且施工速度快。数位化商务解决方案使中小型建筑商能够在线上订购袋装混合料,绕过经销商,缩短前置作业时间。对于高层计划而言,统一的混合料能够减少返工和材料浪费,从而提升价值。新加坡住宅发展局(HDB)已製定公共住宅聚合物改质砂浆的官方规范,为先进产品树立了区域标准。

非正规住宅用户的价格敏感性

在印尼、菲律宾和缅甸的农村地区,自建房住宅更倾向于使用手工搅拌的砂浆,因为与包装好的砂浆相比,它具有更高的附加价值。这些以现金交易为主的群体融资管道有限,难以透过长期的绩效提升来弥补前期成本。小规模计划很少制定品质标准,因此最便宜的材料往往更订单。通膨衝击会增加家庭支出,导致计划延期,并直接降低价格敏感族群对砂浆的需求。

细分市场分析

到2025年,抹灰砂浆将占据东协干粉砂浆市场40.62%的份额,这主要得益于其在潮湿气候下兼具的保护和装饰双重功能。瓷砖黏合剂预计到2031年将以6.31%的复合年增长率成长,这主要受收入水准提高的推动,从而带动了高层公寓和零售室内对高檔陶瓷地板材料的需求。预计从2026年到2031年,随着都市区公寓建设需求的增长,东协用于瓷砖黏合剂的干粉砂浆市场也将随之扩张。水泥浆在基础设施接缝领域保持着稳定的市场份额,而防水浆料在需要抵御强降雨的沿海城市的需求正在增加。在混凝土保护和维修领域,老旧桥樑和港口需要耐用的覆盖层解决方案,这推动了市场需求。诸如SNI 6880:2016等国家标准授权使用预包装干粉混合料进行结构混凝土施工,从而增强了专用混合料的可靠性。

具有内置防水性能、可缩短维护週期的第二代抹灰材料正逐渐被公共住宅规范所采纳。瓷砖黏合剂製造商正在提供变形等级,以适应新型大尺寸陶瓷瓷砖。数位商务平台正在推广即用型产品计算器,以方便安装人员使用。对防水浆料的需求与优先考虑建筑围护结构完整性的气候变迁调适投资一致。低碳黏合剂和再生骨材填充材的创新将成为致力于永续维修的供应商的差异化优势。

东协干混砂浆市场报告按应用领域(抹灰、粉刷、瓷砖黏合剂、防水浆料、混凝土保护与维修等)、终端用户产业(住宅、商业、基础设施、工业及公共设施)和地区(马来西亚、印尼、泰国、新加坡、菲律宾、越南、缅甸、东南亚国协其他地区)进行细分。市场预测以吨为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 快速都市化和大型企划

- 劳动力短缺导致预包装砂浆需求增加。

- 绿建筑标准和低碳排放要求

- 高层计划中现场筒仓系统的引入

- 透过电子商务平台扩大中小承包商的进入管道

- 市场限制

- 非正规住宅用户的价格敏感性

- 群岛地区工厂及筒仓物流的高资本投资成本

- 添加剂供应链变异性(聚合物粉末)

- 价值链分析

- 监管环境

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 透过使用

- 石膏

- 渲染

- 磁砖黏合剂

- 水泥浆

- 防水浆料

- 混凝土保护与维修

- 保温和饰面系统

- 其他的

- 按最终用户行业划分

- 住宅

- 商业的

- 基础设施

- 工业和公共设施

- 按地区

- 马来西亚

- 印尼

- 泰国

- 新加坡

- 菲律宾

- 越南

- 缅甸

- 其他东南亚国协

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Ardex Group

- Greco Asia Sdn Bhd

- Holcim Ltd.

- JORAKAY CORPORATION CO.,LTD

- Knauf Group

- Laticrete International

- Mapei SpA

- Pidilite Industries

- PT Drymix Indonesia

- PT Indocement Tunggal Prakarsa Tbk

- Saint-Gobain

- Siam City Cement Group

- Sika AG

- Starken Drymix Solutions Sdn Bhd

第七章 市场机会与未来展望

The ASEAN Dry Mix Mortar Market is expected to grow from 10.38 million tons in 2025 to 10.89 million tons in 2026 and is forecast to reach 13.87 million tons by 2031 at 4.95% CAGR over 2026-2031.

This expansion reflects large public-sector housing programs, private real-estate recovery, and industrial capacity additions, pushing mortar volumes across the region. The ASEAN dry mix mortar market benefits from rapid urban migration, stronger building codes, and rising labor costs that favor pre-mixed solutions. Competitive intensity is growing as multinational producers add local plants and domestic cement majors move downstream into value-added mortars, creating a landscape where supply-chain control and product differentiation determine margin performance. Logistics constraints in archipelagic markets and raw-material price swings remain structural challenges, yet they also open opportunities for localized plants and premium specialty grades that reduce transport cost ratios. Sustainability mandates, particularly adopting low-carbon binder systems, are expected to tilt procurement choices toward formulations that meet new green codes.

ASEAN Dry Mix Mortar Market Trends and Insights

Rapid Urbanization and Infrastructure Megaprojects

ASEAN cities are forecast to absorb 84 million additional residents by 2030, lifting urbanization to 56% and driving sustained demand for housing, transport corridors, and social infrastructure. Annual infrastructure needs run to USD 60 billion, with projects such as the Trans-Sumatra toll road and Tuas mega-port underpinning mortar consumption. Indonesia's 2024 construction strategy highlights supply-chain agility, ensuring local producers scale capacity to meet pipeline timelines. Secondary cities outside national capitals now represent growth nodes, reshaping distribution maps for mortar suppliers. From flood mitigation to coastal defenses, climate adaptation requires specialty mixes that withstand aggressive environments, amplifying value-added volume opportunities.

Labor-Scarcity-Driven Demand for Pre-Bagged Mortars

Tighter foreign-worker quotas and an aging workforce have sharpened labor shortages in Malaysia and Singapore, encouraging contractors to adopt ready-mixed mortars that minimize on-site skill requirements. Small and medium enterprises increasingly favor standardized mixes that guarantee consistent quality and faster application. Digital commerce solutions let SME builders order pre-bagged formulations online, bypassing traditional distributors and shortening lead times. High-rise projects gain added value because uniform mixes reduce rework and material waste. Singapore's Housing and Development Board has formal specifications for polymer-modified mortars in public housing, setting a regional benchmark for advanced products.

Price Sensitivity of Informal Residential Users

Self-build homeowners in rural Indonesia, the Philippines, and Myanmar favor manual sand-cement mixes because packaged mortars carry price premiums they are unwilling to absorb. Cash transactions dominate these segments, limiting financing options that could justify higher upfront outlays through long-term performance gains. Smaller projects rarely specify quality benchmarks, so cheapest materials often win orders. Inflation shocks raise household costs and trigger project deferrals, directly trimming mortar demand in price-sensitive tiers.the

Other drivers and restraints analyzed in the detailed report include:

- Green-Building Codes and Low-Carbon Mandates

- On-Site Silo Systems Adoption in High-Rise Projects

- High CAPEX for Plant and Silo Logistics in Archipelagos

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Render accounted for 40.62% of the ASEAN dry mix mortar market share in 2025, supported by its dual protective and decorative roles in humid climates. Tile adhesives are expected to post a 6.31% CAGR through 2031 as rising income levels drive demand for premium ceramic flooring in high-rise apartments and retail interiors. The ASEAN dry mix mortar market size for tile adhesives is forecast to expand by 2026-2031 alongside urban condominium pipelines. Grout maintains a steady niche in infrastructure joints, while waterproofing slurries grow in coastal cities coping with heavy rainfall. Concrete protection and renovation receive support from aging bridges and ports requiring durable overlay solutions. National standards such as SNI 6880:2016 authorize packaged dry combined materials for structural concrete, reinforcing confidence in specialty formulations.

Second-generation renders with integral water repellents are winning specifications in public housing because they cut maintenance cycles. Tile adhesive producers offer deformability classes to fit new large-format porcelain tiles. Digital commerce platforms spotlight ready-to-use product calculators, easing contractor adoption. Waterproofing slurry demand dovetails with climate adaptation investments that prioritize building-envelope integrity. Innovation in low-carbon binders and recycled aggregate infill is set to differentiate suppliers targeting sustainable renovation.

The ASEAN Dry Mix Mortar Market Report is Segmented by Application (Plaster, Render, Tile Adhesive, Water Proofing Slurry, Concrete Protection and Renovation, and More), End-User Industry (Residential, Commercial, Infrastructure, and Industrial and Institutional), and Geography (Malaysia, Indonesia, Thailand, Singapore, Philippines, Vietnam, Myanmar, and Rest of ASEAN). The Market Forecasts are Provided in Terms of Volume (Tons).

List of Companies Covered in this Report:

- Ardex Group

- Greco Asia Sdn Bhd

- Holcim Ltd.

- JORAKAY CORPORATION CO.,LTD

- Knauf Group

- Laticrete International

- Mapei S.p.A.

- Pidilite Industries

- PT Drymix Indonesia

- PT Indocement Tunggal Prakarsa Tbk

- Saint-Gobain

- Siam City Cement Group

- Sika AG

- Starken Drymix Solutions Sdn Bhd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid urbanisation and infrastructure megaprojects

- 4.2.2 Labour-scarcity-driven demand for pre-bagged mortars

- 4.2.3 Green-building codes and low-carbon mandates

- 4.2.4 On-site silo systems adoption in high-rise projects

- 4.2.5 E-commerce platforms widening SME contractor access

- 4.3 Market Restraints

- 4.3.1 Price sensitivity of informal residential users

- 4.3.2 High CAPEX for plant and silo logistics in archipelagos

- 4.3.3 Additive supply-chain volatility (polymer powders)

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Application

- 5.1.1 Plaster

- 5.1.2 Render

- 5.1.3 Tile Adhesive

- 5.1.4 Grout

- 5.1.5 Water Proofing Slurry

- 5.1.6 Concrete Protection and Renovation

- 5.1.7 Insulation and Finishing System

- 5.1.8 Others

- 5.2 By End-user Industry

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Infrastructure

- 5.2.4 Industrial and Institutional

- 5.3 By Geography

- 5.3.1 Malaysia

- 5.3.2 Indonesia

- 5.3.3 Thailand

- 5.3.4 Singapore

- 5.3.5 Philippines

- 5.3.6 Vietnam

- 5.3.7 Myanmar

- 5.3.8 Rest of ASEAN

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Ardex Group

- 6.4.2 Greco Asia Sdn Bhd

- 6.4.3 Holcim Ltd.

- 6.4.4 JORAKAY CORPORATION CO.,LTD

- 6.4.5 Knauf Group

- 6.4.6 Laticrete International

- 6.4.7 Mapei S.p.A.

- 6.4.8 Pidilite Industries

- 6.4.9 PT Drymix Indonesia

- 6.4.10 PT Indocement Tunggal Prakarsa Tbk

- 6.4.11 Saint-Gobain

- 6.4.12 Siam City Cement Group

- 6.4.13 Sika AG

- 6.4.14 Starken Drymix Solutions Sdn Bhd

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

干混砂浆添加剂及化学品市场:依砂浆类型、添加剂类型、形态、应用方法及最终用途划分-2026-2032年全球市场预测

干混砂浆添加剂及化学品市场:依砂浆类型、添加剂类型、形态、应用方法及最终用途划分-2026-2032年全球市场预测 2026年工业用预拌干粉砂浆全球市场报告干粉砂浆市场:按类型、包装、计划类型、应用、最终用途和分销管道划分-2026-2032年全球市场预测2026年全球干混砂浆市场报告

2026年工业用预拌干粉砂浆全球市场报告干粉砂浆市场:按类型、包装、计划类型、应用、最终用途和分销管道划分-2026-2032年全球市场预测2026年全球干混砂浆市场报告 干混砂浆:市场占有率分析、产业趋势与统计、成长预测(2026-2031)欧洲干粉砂浆:市场占有率分析、产业趋势与统计、成长预测(2026-2031)2026年全球干混砂浆添加剂和化学品市场报告塔式干粉砂浆搅拌站市场按产品类型、搅拌能力、应用、最终用途和分销管道划分-2026-2032年全球预测自流平砂浆添加剂市场按类型、形态、应用、终端用户产业和分销管道划分,全球预测,2026-2032年预拌建筑砂浆市场(依产品类型、形态、包装类型、应用、最终用途及通路划分)-2026-2032年全球预测

干混砂浆:市场占有率分析、产业趋势与统计、成长预测(2026-2031)欧洲干粉砂浆:市场占有率分析、产业趋势与统计、成长预测(2026-2031)2026年全球干混砂浆添加剂和化学品市场报告塔式干粉砂浆搅拌站市场按产品类型、搅拌能力、应用、最终用途和分销管道划分-2026-2032年全球预测自流平砂浆添加剂市场按类型、形态、应用、终端用户产业和分销管道划分,全球预测,2026-2032年预拌建筑砂浆市场(依产品类型、形态、包装类型、应用、最终用途及通路划分)-2026-2032年全球预测