|

市场调查报告书

商品编码

1940850

欧洲干粉砂浆:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Europe Dry Mix Mortar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

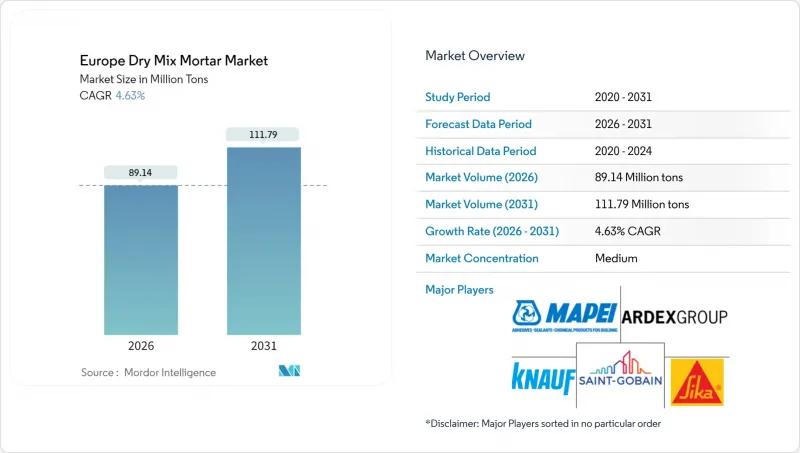

欧洲干混砂浆市场预计将从 2025 年的 8,519 万吨成长到 2026 年的 8,914 万吨,预计到 2031 年将达到 1.1179 亿吨,2026 年至 2031 年的复合年增长率为 4.63%。

この成长轨道は、同地域における低炭素建设への决定的な移行、公共部门の大规模维修予算、欧州绿色交易に基づく规制の整合性から生じています。老朽化した住宅存量の维修活动、自动サイロバッチングの普及拡大、再生材配合に関する急速な製品革新が、いずれも需要を后押ししています。竞争戦略は、原材料価格の変动を缓和する垂直统合と、厳格なVOC(挥発性有机化合物)およびシリカ粉尘の阈值を満たす継続的な製品研究开発に重点を置いています。竞合情势全体では、数位化された工场や循环型経済添加剤への投资が新たな市场机会を开拓すると同时に、永续性に関する认证における差别化を可能にしております。

欧洲干粉砂浆市场趋势与洞察

老旧建筑存量推动了维修需求

欧州の建筑物の4分の3以上は1990年以前に建设され、现在のエネルギー性能基准を満たしていません。ドイツの连邦政府による补助金制度やフランスのMaPrimeRenovプログラムにより、左官用モルタル、断热モルタル、补修用モルタルへの安定した需要が生まれています。この维修需要の高い环境下では、接着性向上、低粉尘、繊维混入などの特殊配合が竞争优位性を持っており、小规模な请负业者でも现场施工が容易な配合の拡大がメーカーに促されています。同时に、自动サイロシステムは熟练左官职人の不足を缓和し、密集した都市区の现场においても安定した混合品质を提供しております。

欧盟脱碳和能源效率指令

修订后的《建筑能源性能指令》(EPBD) 要求所有新建建筑在 2030 年前达到近零能耗标准,并对现有建筑进行大规模维修。这些法规迫使产品开发商采用低碳配方,其中包含再生细料和水泥基辅助材料。由于修订后的《建筑产品法规》预计将强制要求提交环境产品声明 (EPD),因此,能够证明其生产过程排放低于每吨 250 公斤二氧化碳当量 (CO2e) 的领先,很可能在公共竞标中获得优先权。

原物料价格波动

2024年,受能源通膨和欧盟排放交易体系(EU ETS)下碳排放权成本上涨的影响,水泥价格上涨。同时,由于物流瓶颈和更严格的采矿许可证规定,骨材价格也随之上涨。由于原物料成本占生产成本的70%之多,没有避险策略的製造商面临利润空间被压缩和合约价格调整延迟的困境。德国和荷兰部分地区的砂石短缺导致特种细砂价格上涨,迫使生产商对再生玻璃和碎混凝土进行认证,以作为替代填充材。在成本转嫁机制和替代原材料稳定之前,这些原材料成本的波动将限制生产成长。

细分市场分析

2025年、欧州の干式モルタル市场において住宅计划が52.00%を占めました。これは、加速する省エネ维修义务化により、隔热材料、レンダリング、スクリードの需要が増加したためです。商业施设は规模こそ小さいもの、ハイブリッドオフィスの维修や小売店舗のフォーマット更新が活性化するため、2031年までにCAGR6.2%と最も高い伸び率を示すと予测されます。产业・公共施设向け需要は、抗菌タイル黏合剂を好む製薬用クリーンルーム建设に支えられています。TEN-T(欧州横断交通网)に基づくインフラ更新により、アンカー材、补修用水泥浆、防水スラリーの需要が安定的に増加しています。

住宅领域的主导地位主要得益于德国2024年创纪录的120万套维修,而法国的目标是每年完成50万套大型维修。采用生物基纤维和相变微胶囊的高性能抹灰系统价格不菲,同时又能满足严格的U值标准。商业领域的成长则源自于业主希望将办公空间重新配置为协作区域,从而推动了对速凝找平材料的需求。工业活动依赖监管奖励,这些措施强制要求建立清洁的生产工厂,使得低VOC(挥发性有机化合物)的地面砂浆成为必需品。承包商指出,自动化筒仓配料可以缓解劳动力短缺(在住宅维修尤为突出),防止工期延误,并提高最终的施工品质。

欧洲干粉砂浆市场报告按最终用途产业(商业、工业及公共、基础设施、住宅)、应用领域(抹灰、粉刷、瓷砖黏合剂、水泥浆、防水浆料、混凝土保护与维修等)以及地区(法国、德国、义大利、俄罗斯、西班牙、英国、欧洲其他地区)进行细分。市场预测以吨为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 老旧建筑存量推动了维修需求。

- 欧盟脱碳和能源效率指令

- 预製/异地建造的成长

- 疫情后绿色基础设施奖励策略

- 采用自动筒仓配料

- 市场限制

- 原物料价格波动

- 严格的挥发性有机化合物(VOC)和二氧化硅粉尘法规

- 熟练喷涂和抹灰工人短缺

- 价值链分析

- 法律规范

- 波特五力模型

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按最终用途面积

- 商业的

- 工业和公共设施

- 基础设施

- 住宅

- 透过使用

- 石膏

- 渲染

- 磁砖黏合剂

- 水泥浆

- 防水浆料

- 混凝土保护与维修

- 保温和饰面系统

- 其他用途

- 按国家/地区

- 法国

- 德国

- 义大利

- 俄罗斯

- 西班牙

- 英国

- 其他欧洲地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Ardex Group

- Baumit Group

- Cemex SAB DE CV

- Fassa Bortolo

- Holcim

- Kerakoll Spa

- Knauf Group

- LATICRETE International, Inc.

- MAPEI SpA

- Murexin GmbH

- Saint-Gobain

- Sika AG

- SOPREMA International

- Terraco Group

第七章 市场机会与未来展望

第八章:执行长面临的关键策略挑战

The Europe Dry Mix Mortar Market is expected to grow from 85.19 million tons in 2025 to 89.14 million tons in 2026 and is forecast to reach 111.79 million tons by 2031 at 4.63% CAGR over 2026-2031.

This growth trajectory stems from the region's decisive shift toward lower-carbon construction, substantial public-sector renovation budgets, and regulatory alignment under the European Green Deal. Renovation activity in the aging housing stock, the wider adoption of automated silo batching, and rapid product innovation around recycled content formulations are all reinforcing demand. Competitive strategies center on vertical integration to buffer raw material volatility and on continuous product research and development that meets strict VOC and silica dust thresholds. Across the competitive landscape, investments in digitalized plants and circular economy additives are unlocking new market opportunities while enabling differentiation in sustainability credentials.

Europe Dry Mix Mortar Market Trends and Insights

Ageing Building Stock Drives Renovation Demand

More than three-quarters of Europe's buildings were erected before 1990 and fail to meet today's energy-performance thresholds. Germany's federal incentives and France's MaPrimeRenov programs channel steady demand toward render, insulation, and repair mortars. Specialized blends with improved adhesion, low dust, and embedded fibers hold a competitive advantage in this retrofit-heavy environment, encouraging manufacturers to scale formulations that ease site application for smaller contractor crews. At the same time, automated silo systems are mitigating skilled-plasterer shortages and delivering consistent mix quality on dense urban job sites.

EU Decarbonisation and Energy-Efficiency Directives

The recast Energy Performance of Buildings Directive (EPBD) requires all new buildings to achieve nearly zero-energy status by 2030 and mandates the deep renovation of the existing stock. These mandates are prompting product developers to adopt lower-carbon-embodied recipes that incorporate recycled fines and supplementary cementitious materials. With environmental product declarations (EPDs) set to become compulsory under the revised Construction Products Regulation, early movers that can certify cradle-to-gate emissions under 250 kg CO2e per ton are likely to seize specification priority across public tenders.

Raw-Material Price Volatility

Cement prices rose in 2024, driven by energy inflation and carbon allowance costs under the EU ETS, while aggregates increased amid logistical bottlenecks and tighter mining permits. Raw inputs represent up to 70% of production expenses, so unhedged manufacturers faced margin compression and adjustment lags in contract pricing. Sand scarcity in parts of Germany and the Netherlands added a premium on specialty fines, compelling producers to qualify recycled glass and crushed concrete as substitute fillers. Fluctuating input costs thereby temper volume growth until pass-through mechanisms or alternative raw materials stabilize.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Prefabricated/Off-Site Construction

- Post-Pandemic Green Infrastructure Stimulus

- Stringent VOC and Silica-Dust Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Residential projects accounted for 52.00% of the European dry mix mortar market in 2025, as accelerating energy-retrofit mandates drove increased demand for insulation, render, and screed volumes. Commercial premises, although smaller in scale, are projected to post the fastest 6.2% CAGR through 2031 as hybrid office refurbishments and retail format updates intensify. Industrial and institutional demand is fueled by pharmaceutical cleanroom builds that favor antimicrobial tile adhesives. Infrastructure upgrades under TEN-T add steady volumes in anchoring, repair grout, and waterproofing slurries.

The residential segment's primacy stems from Germany's 1.2 million-unit retrofit record in 2024 and France's target of 500,000 deep renovations annually. High-performance render systems integrating bio-based fibers and phase-change microcapsules secure premium pricing while meeting stringent U-value thresholds. Commercial growth benefits from owners' drive to repurpose office layouts into collaborative work zones, boosting demand for rapid-set leveling compounds. Industrial activity leans on legislative incentives for cleaner manufacturing plants, which mandate low-VOC flooring mortars. Contractors note that automated silo batching mitigates labor shortages, particularly those that are acute in residential refurbishment, thereby preventing delays and improving finishing quality.

The Europe Dry Mix Mortar Market Report is Segmented by End-Use Sector (Commercial, Industrial and Institutional, Infrastructure, and Residential), Application (Plaster, Render, Tile Adhesive, Grout, Waterproofing Slurry, Concrete Protection and Renovation, and More), and Geography (France, Germany, Italy, Russia, Spain, United Kingdom, and Rest of Europe). The Market Forecasts are Provided in Terms of Volume (Tons).

List of Companies Covered in this Report:

- Ardex Group

- Baumit Group

- Cemex S.A.B DE C.V.

- Fassa Bortolo

- Holcim

- Kerakoll Spa

- Knauf Group

- LATICRETE International, Inc.

- MAPEI S.p.A.

- Murexin GmbH

- Saint-Gobain

- Sika AG

- SOPREMA International

- Terraco Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ageing building stock drives renovation demand

- 4.2.2 EU decarbonisation and energy-efficiency directives

- 4.2.3 Growth in prefabricated/off-site construction

- 4.2.4 Post-pandemic green infrastructure stimulus

- 4.2.5 Automated silo batching adoption

- 4.3 Market Restraints

- 4.3.1 Raw-material price volatility

- 4.3.2 Stringent VOC and silica-dust regulations

- 4.3.3 Skilled spray-plaster labour shortage

- 4.4 Value Chain Analysis

- 4.5 Regulatory Framework

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By End-Use Sector

- 5.1.1 Commercial

- 5.1.2 Industrial and Institutional

- 5.1.3 Infrastructure

- 5.1.4 Residential

- 5.2 By Application

- 5.2.1 Plaster

- 5.2.2 Render

- 5.2.3 Tile Adhesive

- 5.2.4 Grout

- 5.2.5 Waterproofing Slurry

- 5.2.6 Concrete Protection and Renovation

- 5.2.7 Insulation and Finishing Systems

- 5.2.8 Other Applications

- 5.3 By Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Russia

- 5.3.5 Spain

- 5.3.6 United Kingdom

- 5.3.7 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Ardex Group

- 6.4.2 Baumit Group

- 6.4.3 Cemex S.A.B DE C.V.

- 6.4.4 Fassa Bortolo

- 6.4.5 Holcim

- 6.4.6 Kerakoll Spa

- 6.4.7 Knauf Group

- 6.4.8 LATICRETE International, Inc.

- 6.4.9 MAPEI S.p.A.

- 6.4.10 Murexin GmbH

- 6.4.11 Saint-Gobain

- 6.4.12 Sika AG

- 6.4.13 SOPREMA International

- 6.4.14 Terraco Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

8 Key Strategic Questions for CEOs

干混砂浆添加剂及化学品市场:依砂浆类型、添加剂类型、形态、应用方法及最终用途划分-2026-2032年全球市场预测

干混砂浆添加剂及化学品市场:依砂浆类型、添加剂类型、形态、应用方法及最终用途划分-2026-2032年全球市场预测 2026年工业用预拌干粉砂浆全球市场报告干粉砂浆市场:按类型、包装、计划类型、应用、最终用途和分销管道划分-2026-2032年全球市场预测2026年全球干混砂浆市场报告

2026年工业用预拌干粉砂浆全球市场报告干粉砂浆市场:按类型、包装、计划类型、应用、最终用途和分销管道划分-2026-2032年全球市场预测2026年全球干混砂浆市场报告 东协干混砂浆:市占率分析、产业趋势与统计、成长预测(2026-2031)干混砂浆:市场占有率分析、产业趋势与统计、成长预测(2026-2031)2026年全球干混砂浆添加剂和化学品市场报告塔式干粉砂浆搅拌站市场按产品类型、搅拌能力、应用、最终用途和分销管道划分-2026-2032年全球预测自流平砂浆添加剂市场按类型、形态、应用、终端用户产业和分销管道划分,全球预测,2026-2032年预拌建筑砂浆市场(依产品类型、形态、包装类型、应用、最终用途及通路划分)-2026-2032年全球预测

东协干混砂浆:市占率分析、产业趋势与统计、成长预测(2026-2031)干混砂浆:市场占有率分析、产业趋势与统计、成长预测(2026-2031)2026年全球干混砂浆添加剂和化学品市场报告塔式干粉砂浆搅拌站市场按产品类型、搅拌能力、应用、最终用途和分销管道划分-2026-2032年全球预测自流平砂浆添加剂市场按类型、形态、应用、终端用户产业和分销管道划分,全球预测,2026-2032年预拌建筑砂浆市场(依产品类型、形态、包装类型、应用、最终用途及通路划分)-2026-2032年全球预测