|

市场调查报告书

商品编码

1940761

商用车远端资讯处理:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Commercial Vehicle Telematics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

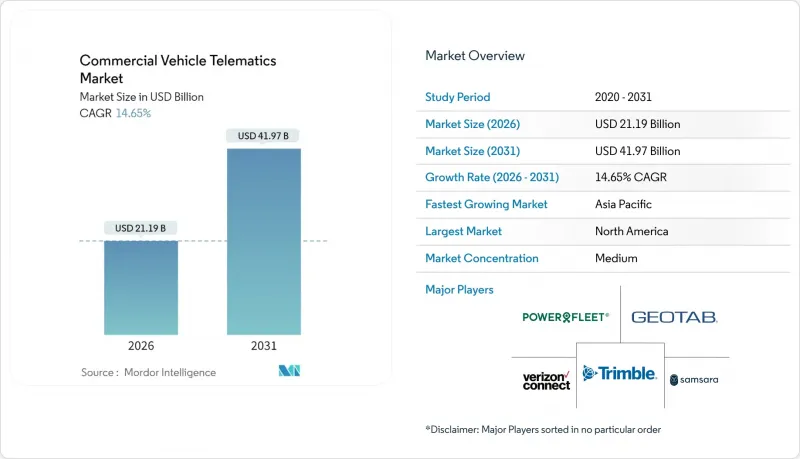

2025年商用车远端资讯处理市场价值为184.8亿美元,预计到2031年将达到419.7亿美元,而2026年为211.9亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 14.65%。

随着车队从被动维护转向预测性、数据驱动的最佳化,市场需求正在加速成长,而电子记录设备和安全法规等法律强制要求也推动了这一趋势。现代重型卡车每分钟可从100多个感测器产生高达20GB的数据,这使得机器学习模型能够预防77%的计划外故障。基于订阅的数据货币化模式、用于远端路线的混合蜂窝/卫星通讯以及降低总体拥有成本的经济需求,都在推动市场成长。产业整合正在重塑竞争格局,Platform Science以3亿美元的历史收入收购Trimble的远端资讯处理部门便是一个例证。

全球商用车远端资讯处理市场趋势与洞察

重型卡车中工厂出货时装载OEM远端资讯处理系统的采用率不断提高

OEM整合正在将价值从售后改装转移到利用车辆专用网路的原厂系统,从而提高资料完整性并降低安装成本。沃尔沃的最新平台连接了欧洲各地85,000辆卡车,每月产生4,000条预测性维护警报,并预防了77%的故障。车队透过保固完整性和无缝的空中升级,获得了高投资报酬率(ROI)。 OEM厂商正在将远端资讯处理作为标准配置,从而改变了与独立供应商之间的竞争格局。

强制性电子记录设备(ELD)和安全法规

美国联邦道路运输安全管理局 (FMCSA) 2025 年的修订案将把自动紧急煞车、限速器以及扩大药物和酒精检测范围纳入现有的电子记录设备 (ELD) 要求,从而加大合规压力。欧盟也紧随其后,颁布了第 2024/2220 号法规,强制要求在 2026 年 1 月前使用事件资料记录器。统一的标准将提高供应商的规模经济效益,并透过自动化文件处理减轻承运商的审核负担。

连网商用车辆的网路安全漏洞

不断扩大的攻击面使煞车和转向等关键系统面临被恶意攻击者入侵的风险。欧盟安全法规强制要求对汽车网路安全进行管理,这不仅增加了合规的复杂性,也凸显了潜在的责任风险。空中下载 (OTA) 更新进一步扩大了攻击面,因此,健全的安全框架和第三方审核对于确保车队可靠性至关重要。

细分市场分析

到2025年,解决方案将占据商用车远端资讯处理市场62.85%的份额,因为车队依赖核心模组进行追踪、合规性和预测性维护。同时,随着系统复杂性的增加,营运商将分析和管理功能外包,託管服务将以16.04%的复合年增长率成长。商用车远端资讯处理市场服务的扩张反映了市场重心从技术应用转向价值创造。

Geotab 的应用程式市场提供数百个第三方应用程序,这些应用程式在基础资料馈送之上迭加了分析和工作流程自动化功能。车队营运商越来越愿意支付订阅费以获取持续的洞察讯息,而不是直接购买硬体。这种服务趋势正在重新平衡供应商的收入来源,并提高客户留存率。

到2025年,OEM解决方案将占据商用车远端资讯处理市场57.40%的份额,这主要得益于卡车製造商在工厂预装连网功能。售后市场供应商仍将维持15.46%的复合年增长率,主要服务于OEM捆绑包所忽略的改装和细分应用领域。与OEM平台相关的商用车远端资讯处理市场规模将与新车产量成正比增长,但由于第三方软体生态系统的开放性,传统界限正在变得模糊。

Platform Science斥资3亿美元收购Trimble子公司,打造了一个统一的车载市场,该市场基于OEM硬体运行,但支援客製化工作流程。资料存取的争夺战围绕着专有的CAN讯号展开,监管机构正在仔细审查如何确保独立服务供应商获得公平的存取权限。

区域分析

2025年,北美贡献了32.20%的收入,这得益于美国联邦道路运输安全管理局(FMCSA)严格的安全法规和广泛的行动网路覆盖范围。 2025年生效的强制自动紧急煞车系统将进一步推动其普及,而高昂的人事费用使得投资收益率(ROI)的计算至关重要。 Platform Science收购Trimble的资产以及GPS Trackit和Zonar Systems的合併重塑了竞争格局。数据货币化试点计画(车队营运商向保险公司出售匿名分析数据)凸显了该地区对订阅模式的强劲需求。

预计亚太地区将成为成长最快的地区,到2031年复合年增长率将达到17.05%。中国占全球电动货车销量的80%,因此需要整合电池更换调度和充电器分析的车载资讯系统。目前,中国已有40%的重型电动货车采用电池更换技术,这需要专用的应用程式介面(API)来实现即时能源管理。在澳洲和纽西兰,随着农业和矿业车辆数位化提高,预计到2028年,电动货车的普及率将从26.6%提高到39.5%。随着V2X技术在中国新车安全评估协会(NCAP)中成为强制性标准,汽车製造商正在整合C-V2X模组,从而加速系统性车载资讯系统的普及。

由于网路安全和事件资料记录器(EDR)的通用安全法规将于2026年生效,欧洲在该领域保持强大的影响力。针对2.5吨以上车辆的数位式行车记录器法规进一步扩大了潜在市场。双卡车DSRC和C-V2X标准化使得可以使用来自多个供应商的硬件,而无需担心供应商之间的兼容性问题。永续性目标正在推动零排放卡车远端资讯处理技术的应用,以优化充电计画和路线规划。公共采购通常要求在市政合约中提供远端资讯处理功能证明,这进一步促进了该技术的普及。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 重型卡车中工厂出货时装载OEM远端资讯处理系统的采用率不断提高

- 强制性电子记录设备(ELD)和安全法规

- 市场对人工智慧驱动的车队优化的需求日益增长,以降低整体拥有成本

- 电子商务最后一公里配送车辆的快速扩张

- 订阅式远端资讯处理资料市场的兴起

- 将远端资讯处理技术与零排放卡车的能源和充电管理系统集成

- 市场限制

- 连网商用车辆的网路安全漏洞

- 发展中地区连结基础建设碎片化

- 小规模车队营运商的成本和投资收益问题

- 资料所有权和隐私合规障碍

- 价值链分析

- 监管环境

- 波特五力分析

- 新进入者的威胁

- 买方和消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 宏观经济因素如何影响市场

第五章 市场规模与成长预测

- 报价

- 解决方案

- 车辆追踪和监控系统

- 驾驶员管理

- 保险远端资讯处理

- 安全与合规

- V2X解决方案

- 预测性维护和诊断

- 资产和拖车跟踪

- 服务

- 专业服务

- 託管服务

- 解决方案

- 按提供者类型

- OEM

- 售后市场

- 按车辆类别

- 轻型商用车

- 重型和中型商用车辆

- 透过通讯技术

- 蜂窝通讯(2G/3G/4G/5G)

- 卫星

- 混合(蜂巢+卫星)

- 终端用户产业

- 运输/物流

- 建筑和采矿

- 公共部门及紧急服务

- 公共产业

- 保险和租赁

- 零售与电子商务

- 其他(农业、废弃物管理等)

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 澳洲和纽西兰

- 亚太其他地区

- 中东和非洲

- 中东

- GCC

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Verizon Connect(Verizon Communications Inc.)

- Geotab Inc.

- Samsara Inc.

- Trimble Inc.

- Teletrac Navman(Vontier Corporation)

- Powerfleet Inc.

- Omnitracs LLC

- Lytx Inc.

- CalAmp Corp.

- Webfleet Solutions

- PTC Inc.

- Octo Telematics SpA

- Zonar Systems, Inc.

- Gurtam Inc.

- Motive Technologies Inc.

- GPS Insight

- Sierra Wireless(Semtech Corporation)

- Cartrack Holdings Limited

- IntelliShift(Vehicle Tracking Solutions, LLC(VTS))

- Azuga Inc.

- Platform Science, Inc.

第七章 市场机会与未来展望

The Commercial Vehicle Telematics Market was valued at USD 18.48 billion in 2025 and estimated to grow from USD 21.19 billion in 2026 to reach USD 41.97 billion by 2031, at a CAGR of 14.65% during the forecast period (2026-2031).

Demand accelerates as fleets shift from reactive maintenance to predictive, data-driven optimization, aided by regulatory mandates such as electronic logging devices and safety regulations. Modern heavy-duty trucks generate up to 20 GB of data per minute across more than 100 sensors, enabling machine-learning models that prevent 77% of unplanned breakdowns . Growth is reinforced by subscription-based data monetization models, hybrid cellular-satellite connectivity for remote routes, and the economic imperative to reduce total cost of ownership. Consolidation is reshaping the competitive landscape, as illustrated by Platform Science's acquisition of Trimble's telematics units for USD 300 million in trailing revenue.

Global Commercial Vehicle Telematics Market Trends and Insights

Increasing adoption of factory-installed OEM telematics in heavy trucks

OEM integration shifts value from aftermarket retrofits to factory systems that leverage native vehicle networks, enhancing data integrity and reducing installation costs. Volvo's latest platform connects 85,000 trucks across Europe, issuing 4,000 predictive-maintenance alerts per month and preventing 77% of breakdowns. Fleets gain higher ROI through warranty alignment and seamless over-the-air updates. OEMs now bundle telematics as standard equipment, altering competitive dynamics against stand-alone providers.

Mandatory electronic logging-device and safety regulations

The FMCSA's 2025 update incorporates automatic emergency braking, speed limiters, and expanded drug and alcohol testing into existing ELD requirements, thereby increasing compliance pressure. The EU mirrors this trend with Regulation 2024/2220, which mandates the use of event data recorders by January 2026 . Uniform standards increase scale economies for vendors and automate documentation, reducing audit burdens for carriers.

Cyber-security vulnerabilities in connected commercial vehicles

Expanded attack surfaces expose critical systems such as braking and steering to malicious actors. EU safety regulations now require automotive cybersecurity management, imposing compliance complexity but also highlighting potential liability exposure . Over-the-air updates widen entry points, making robust security frameworks and third-party audits essential for fleet trust.

Other drivers and restraints analyzed in the detailed report include:

- Demand for AI-driven fleet optimization to cut total cost of ownership

- Rapid expansion of last-mile e-commerce delivery fleets

- Fragmented connectivity infrastructure in developing regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions retained 62.85% of the commercial vehicle telematics market share in 2025 as fleets relied on core modules for tracking, compliance, and predictive maintenance. Managed services, however, are growing at 16.04% CAGR because rising system complexity pushes operators to outsource analytics and administration. The commercial vehicle telematics market's expansion in services reflects a shift from technology adoption to value extraction.

Geotab's marketplace hosts hundreds of third-party apps that layer analytics and workflow automation onto base data feeds. Fleets increasingly pay subscription fees for continuous insight rather than purchasing hardware outright. This service's momentum rebalances revenue streams and creates stickier customer relationships for vendors.

OEM solutions controlled a 57.40% share of the commercial vehicle telematics market in 2025, as truck makers embedded connectivity at the factory. Aftermarket providers still post a 15.46% CAGR by addressing retrofits and niche applications that OEM bundles overlook. The commercial vehicle telematics market size tied to OEM platforms grows with every new vehicle roll-off, yet openness to third-party software ecosystems blurs traditional boundaries.

Platform Science's purchase of Trimble's units for USD 300 million creates an integrated in-cab marketplace that can run on OEM hardware while supporting customized workflows. Data access wars center on proprietary CAN signals, with regulators monitoring to ensure fair access for independent service providers.

The Commercial Vehicle Telematics Market Report is Segmented by Offering (Solutions, Services), Provider Type (OEM, Aftermarket), Vehicle Class (Light Commercial Vehicles, Heavy and Medium Commercial Vehicles), Communication Technology (Cellular, Satellite, Hybrid), End-User Vertical (Transportation and Logistics, Construction and Mining, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 32.20% revenue in 2025, underpinned by FMCSA's tight safety regime and broad cellular coverage. Automatic emergency braking mandates, effective 2025, further elevate adoption, while high labor costs magnify ROI calculations. Platform Science acquired Trimble assets, and GPS Trackit merged with Zonar Systems, reshaping the competitive landscape. Data monetization pilots, where fleets sell anonymized insights to insurers, reflect the region's appetite for subscription models.

The Asia-Pacific region is the fastest-growing region, with a 17.05% CAGR through 2031. China commands 80% of global electric freight-truck sales, requiring telematics that integrate battery-swap scheduling and charger analytics. Battery swapping already covers 40% of Chinese heavy-duty e-trucks, demanding specialized APIs for real-time energy management. Australia and New Zealand anticipate a rise in penetration from 26.6% to 39.5% by 2028, as agriculture and mining fleets digitize their operations. V2X inclusion in China's NCAP prompts OEMs to embed C-V2X modules, accelerating the deployment of systemic telematics.

Europe maintains a robust presence due to General Safety Regulation provisions on cybersecurity and event data recorders, which will take effect starting in 2026. Digital tachograph rules, which extend to vehicles weighing more than 2.5 tonnes, broaden the addressable base. Dual-track DSRC and C-V2X standardization allows multi-vendor hardware without fragmentation. Sustainability goals promote zero-emission truck telematics that co-optimize route planning with charge scheduling. Public procurement often requires proof of telematics capability for municipal contracts, further boosting uptake.

- Verizon Connect (Verizon Communications Inc.)

- Geotab Inc.

- Samsara Inc.

- Trimble Inc.

- Teletrac Navman (Vontier Corporation)

- Powerfleet Inc.

- Omnitracs LLC

- Lytx Inc.

- CalAmp Corp.

- Webfleet Solutions

- PTC Inc.

- Octo Telematics SpA

- Zonar Systems, Inc.

- Gurtam Inc.

- Motive Technologies Inc.

- GPS Insight

- Sierra Wireless (Semtech Corporation)

- Cartrack Holdings Limited

- IntelliShift (Vehicle Tracking Solutions, LLC (VTS))

- Azuga Inc.

- Platform Science, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing adoption of factory-installed OEM telematics in heavy trucks

- 4.2.2 Mandatory electronic logging-device (ELD) and safety regulations

- 4.2.3 Demand for AI-driven fleet optimisation to cut total cost of ownership

- 4.2.4 Rapid expansion of last-mile e-commerce delivery fleets

- 4.2.5 Emergence of subscription-based telematics data marketplaces

- 4.2.6 Integration of telematics with zero-emission truck energy and charge management

- 4.3 Market Restraints

- 4.3.1 Cyber-security vulnerabilities in connected commercial vehicles

- 4.3.2 Fragmented connectivity infrastructure in developing regions

- 4.3.3 Cost and ROI concerns for small fleet operators

- 4.3.4 Data-ownership and privacy-compliance hurdles

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Solutions

- 5.1.1.1 Fleet Tracking and Monitoring

- 5.1.1.2 Driver Management

- 5.1.1.3 Insurance Telematics

- 5.1.1.4 Safety and Compliance

- 5.1.1.5 V2X Solutions

- 5.1.1.6 Predictive Maintenance and Diagnostics

- 5.1.1.7 Asset and Trailer Tracking

- 5.1.2 Services

- 5.1.2.1 Professional Services

- 5.1.2.2 Managed Services

- 5.1.1 Solutions

- 5.2 By Provider Type

- 5.2.1 OEM

- 5.2.2 Aftermarket

- 5.3 By Vehicle Class

- 5.3.1 Light Commercial Vehicles

- 5.3.2 Heavy and Medium Commercial Vehicles

- 5.4 By Communication Technology

- 5.4.1 Cellular (2G/3G/4G/5G)

- 5.4.2 Satellite

- 5.4.3 Hybrid (Cellular + Satellite)

- 5.5 By End-user Vertical

- 5.5.1 Transportation and Logistics

- 5.5.2 Construction and Mining

- 5.5.3 Public Sector and Emergency Services

- 5.5.4 Utilities

- 5.5.5 Insurance and Leasing

- 5.5.6 Retail and E-commerce

- 5.5.7 Others (Agriculture, Waste Management, etc.)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 GCC

- 5.6.5.1.2 Turkey

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Verizon Connect (Verizon Communications Inc.)

- 6.4.2 Geotab Inc.

- 6.4.3 Samsara Inc.

- 6.4.4 Trimble Inc.

- 6.4.5 Teletrac Navman (Vontier Corporation)

- 6.4.6 Powerfleet Inc.

- 6.4.7 Omnitracs LLC

- 6.4.8 Lytx Inc.

- 6.4.9 CalAmp Corp.

- 6.4.10 Webfleet Solutions

- 6.4.11 PTC Inc.

- 6.4.12 Octo Telematics SpA

- 6.4.13 Zonar Systems, Inc.

- 6.4.14 Gurtam Inc.

- 6.4.15 Motive Technologies Inc.

- 6.4.16 GPS Insight

- 6.4.17 Sierra Wireless (Semtech Corporation)

- 6.4.18 Cartrack Holdings Limited

- 6.4.19 IntelliShift (Vehicle Tracking Solutions, LLC (VTS))

- 6.4.20 Azuga Inc.

- 6.4.21 Platform Science, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

商用车远端资讯处理市场:按组件、部署模式、通讯技术、车辆数量、应用和车辆类型划分-2026-2032年全球市场预测

商用车远端资讯处理市场:按组件、部署模式、通讯技术、车辆数量、应用和车辆类型划分-2026-2032年全球市场预测 2026年全球商用远端资讯处理市场报告

2026年全球商用远端资讯处理市场报告 商用车载资讯服务市场规模、份额、趋势及预测(按类型、系统类型、提供者类型、最终用户产业及地区划分),2026-2034年日本商用车载资讯服务市场规模、份额、趋势及预测(按类型、系统类型、供应商类型、最终用户产业及地区划分),2026-2034年

商用车载资讯服务市场规模、份额、趋势及预测(按类型、系统类型、提供者类型、最终用户产业及地区划分),2026-2034年日本商用车载资讯服务市场规模、份额、趋势及预测(按类型、系统类型、供应商类型、最终用户产业及地区划分),2026-2034年 商用车载资讯服务市场-全球产业规模、份额、趋势、机会及预测(依解决方案、应用、最终用户、地区及竞争格局划分),2021-2031年

商用车载资讯服务市场-全球产业规模、份额、趋势、机会及预测(依解决方案、应用、最终用户、地区及竞争格局划分),2021-2031年 北美商用车远端资讯处理市场:市场份额分析、产业趋势与统计及成长预测(2026-2031 年)

北美商用车远端资讯处理市场:市场份额分析、产业趋势与统计及成长预测(2026-2031 年) 商用车载资讯服务市场规模、份额及成长分析(依产品、解决方案类型、最终用户及地区划分)-2026-2033年产业预测

商用车载资讯服务市场规模、份额及成长分析(依产品、解决方案类型、最终用户及地区划分)-2026-2033年产业预测 商用车远端资讯处理市场规模、份额和成长分析(按组件、安装类型、应用和地区划分)-2026-2033年产业预测

商用车远端资讯处理市场规模、份额和成长分析(按组件、安装类型、应用和地区划分)-2026-2033年产业预测 商用车V2X技术-全球市占率及排名、总销售量及需求预测(2025-2031年)

商用车V2X技术-全球市占率及排名、总销售量及需求预测(2025-2031年) 商用车远端资讯处理市场预测(至 2032 年):按类型、连接类型、车辆类型、部署模式、技术、最终用户和地区进行的全球分析

商用车远端资讯处理市场预测(至 2032 年):按类型、连接类型、车辆类型、部署模式、技术、最终用户和地区进行的全球分析